On 19 July, the Australian Prudential Regulation Authority (APRA) announced that it will raise the minimum common equity Tier 1 (CET1) ratio for banks. The stricter capital requirements will make the banking system more resilient to any weakening of credit conditions, a credit positive.

Australia’s four biggest banks, the Australia and New Zealand Banking Group Ltd. (Aa3/Aa3 stable, a22), Commonwealth Bank of Australia (Aa3/Aa3 stable, a2), National Australia Bank Limited (Aa3/Aa3 stable, a2), and Westpac Banking Corporation (Aa3/Aa3 stable, a2), which use internal ratings based models for calculating risk-weighted assets, will be most affected. APRA increased the four banks’ minimum CET1 ratio 150 basis points to 9.5%, including a 1% charge for domestic systemically important banks (D-SIBs). Although the higher capital requirements will take effect in early 2021, APRA said that it expects banks to exceed the new requirement and have CET1 ratios of 10.5% by 1 January 2020 at the latest.

The minimum CET1 ratio for Macquarie Bank Limited (A2 stable, baa1), which also uses an internal ratings-based approach but is not a D-SIB, was similarly raised 150 basis points to 8.5%, effective 1 January 2020. For all the other banks, which use standardized models, the minimum CET1 ratio is 7.5%, a 50 basis point increase.

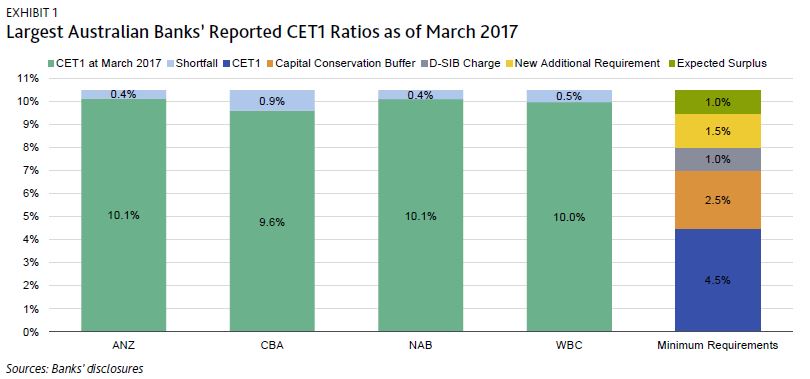

The new minimum CET1 ratio is an incremental increase from the banks’ current capital levels. The APRA has for some time indicated that it would tighten capital rules, and our Australian bank ratings fully reflect that possibility. To meet a CET1 target of 10.5%, the four big banks will need to raise their CET1 ratios between 40 and 90 basis points from their reported levels at March 2017 (see Exhibit 1). That translates into an aggregate capital shortfall of about AUD9.1 billion. However, the banks’ normalized annual internal capital generation is already around AUD6.5-AUD7.5 billion after dividend payments and dividend reinvestments. Also, in practice, they may need less additional capital because they have been actively reducing their risk-weighted assets by changing their business mixes.

Macquarie Bank’s CET1 ratio was 11.1% as of March 2017, well above its new 8.5% minimum. Smaller banks subject to a 7.5% minimum also mostly have CET1 ratios exceeding the requirement, so any capital shortage for them will be minimal.

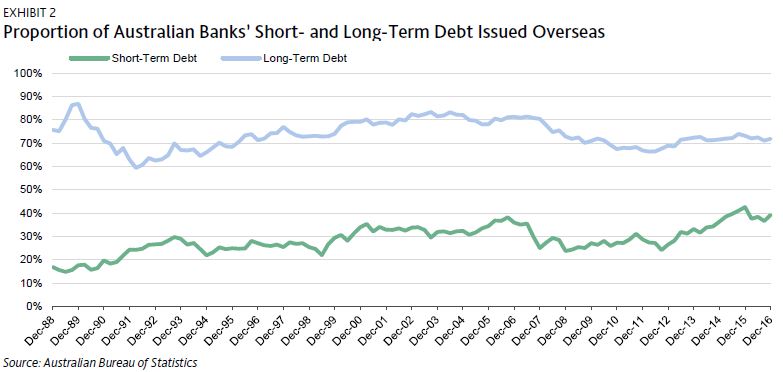

The tighter capital requirement reflects the APRA’s concern about Australian banks’ reliance on foreign wholesale funding, which makes them vulnerable to sudden shifts in foreign investor sentiment. Australian banks issue around 70% of their long-term debt and 40% of their short-term debt to foreign investors (see Exhibit 2).

The APRA has also flagged further increases in capital requirements in 2021. The regulator plans to increase the risk weights of certain assets, particularly for investor property loans and higher loan-to-value ratio loans. Although loss rates on mortgages remain low, housing loans make up 60% of Australian banks’ loan portfolios. Furthermore, a high and rising level of household debt has elevated risks within the household sector, making Australian banks’ credit quality more vulnerable to a shock. APRA also stated that its assessment of bank capital assumes that a framework for total loss-absorbing capacity will be introduced at a later date.