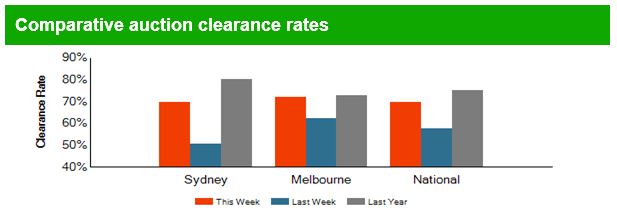

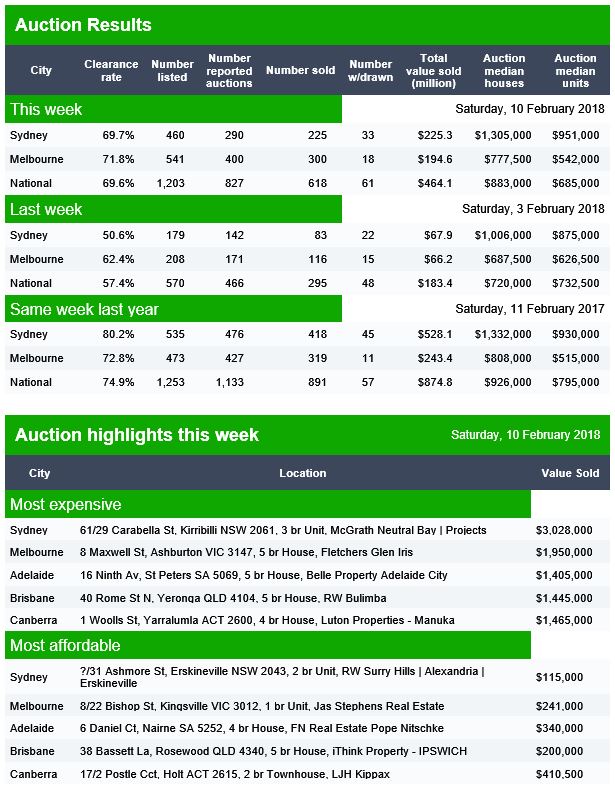

Domain has released the preliminary auction results for today. Volumes are up this week, but still well below this time last year. Sydney lags Melbourne in terms of clearance rate, the opposite to a year ago. Nationally 69.6% cleared against 74.9% last year. This is preliminary and the final results will likely settle lower.

Brisbane cleared 60% of 93 scheduled auctions, Adelaide 67% of 49 auctions and Canberra 65% of 60 listed.

Recent events have the potential to create a revolution in Australian Finance. We explore the 72 hours that changed banking forever.

Welcome to the Property Imperative Weekly to 10th February 2018.Watch the video or read the transcript.

In our latest weekly digest, we start with the batch of new reports, all initiated by the current Australian Government – and which combined have the potential to shake up the Financial Services sector, and reduce the excessive market power which the four major incumbents have enjoyed for years.

On Wednesday, the Productivity Commission, Australian Government’s independent research and advisory body released its draft report into Competition in the Australian Financial System. It’s a Doozy, and if the final report, after consultation takes a similar track it could fundamentally change the landscape in Australia. They leave no stone unturned, and yes, customers are at a significant disadvantage. Big Banks, Regulators and Government all cop it, and rightly so. They say, Australia’s financial system is without a champion among the existing regulators — no agency is tasked with overseeing and promoting competition in the financial system. It has also found that competition is weakest in markets for small business credit, lenders’ mortgage insurance, consumer credit insurance and pet insurance. The report demonstrates the inter-linkages between difference financial entities, and their links to the four majors. They criticised mortgage brokers and financial advisers for poor advice (influenced by commission and ownership structures) and the regulatory environment, where the shadowy Council of Finance Regulators (RBA, ASIC, APRA and Treasury) do not even release minutes of the meetings which set policy direction. You can watch our separate video blog on this.

On Thursday, the Treasurer released draft legislation to require the big four banks to participate fully in the credit reporting system by 1 July 2018. They say this measure will give lenders access to a deeper, richer set of data enabling them to better assess a borrower’s true credit position and their ability to pay a loan. This removes the current strategic advantage which the majors have thanks to the credit data asymmetry, and the current negative reporting. We note that there is no explicit consumer protection in this bill, relating to potential inaccuracies of data going into a credit record. This is, in our view a significant gap, especially as the proposed bulk uploading will require large volumes of data to be transferred. It does however smaller lenders to access information which up to now they could not, so creating a more level playing field. Consumers may benefit, but they should also beware of the implications of the proposals.

On Friday, Treasurer Morrison released the report by King & Wood Mallesons partner Scott Farrell in to open banking which aims to give consumers greater access to, and control over, their data and which mirrors developments in the UK. This “open banking” regime mean that customers, including small businesses, can opt to instruct their bank to send data to a competitor, so it can be used to price or offer an alternative product or service. Great news for smaller players and fintechs, and possibly for customers too. Bad news for the major players. The report recommends that the open banking regime should apply to all banks, though with the major banks to join it first. For non-banks and fintechs, the report wants a “graduated, risk-based accreditation standard”. Superannuation funds and insurers are not included for now. In terms of implementation, data holders should be required to allow customers to share information with eligible parties via a dedicated application programming interface, not screen scraping. A period of approximately 12 months between the announcement of a final Government decision on Open Banking and the Commencement Date should be allowed for implementation. From the Commencement Date, the four major Australian banks should be obliged to comply with a direction to share data under Open Banking. The remaining Authorised Deposit-taking Institutions should be obliged to share data from 12 months after the Commencement Date, unless the ACCC determines that a later date is more appropriate.

Then of course the Royal Commission in Financial Services starts this coming week. We discussed this on ABC The Business on Thursday. Lending Practice is on the agenda, highly relevant given the new UBS research (they of liar loans) suggesting that incomes of many more affluent households are significantly overstated on mortgage application forms. And The BEAR – the bank executive behaviour regime legalisation – passed the Senate, and as a result of amendments, Small and medium banking institutions have until 1 July 2019 to prepare for the BEAR while it will commence for the major banks on 1 July 2018.

APRA Chairman Wayne Byers spoke at the A50 Australian Economic Forum, Sydney. Significantly, he says the temporary measures taken to address too-free mortgage lending will morph into the more permanent focus on among other things, further strengthening of borrower serviceability assessments by lenders, strengthened capital requirements for mortgage lending, and the comprehensive credit reporting being mandated by the Government.

Adelaide Bank is ahead of the curve, as it introducing an alert system that will monitor property borrowers that are struggling with their repayments. The bank and its subsidiaries and affiliates will compare monthly mortgage repayments with borrowers’ income ratios. In addition, extra scrutiny will be applied where the loan-to-income ratio exceeds five times or monthly mortgage repayments exceed 35% of a borrower’s income.

But combined, data sharing, positive credit and banking competition and regulation are all up in the air, or are already coming into force and in each case it appears the big four incumbents are the losers, as they are forced to share customer data, and competition begins to put their excessive profitability under pressure. It highlights the dominance which our big banks have had in recent years, and the range of reforms which are in train. The face of Australian Banking is set to change, and we think customers will benefit. But wait for the rear-guard actions and heavy lobbying which will take place ahead.

Of course the RBA left the cash rate on hold this week, and signalled the next move will likely be up, but not for some time. Retail turnover for December fell 0.5% according to the ABS seasonally adjusted. This is the headline which will get all the coverage, but the trend estimate rose 0.2 per cent in December 2017 following a rise of 0.2 per cent in November 2017. Compared to December 2016 the trend estimate rose 2.0 per cent. This is in line with average income growth, but not good news for retailers.

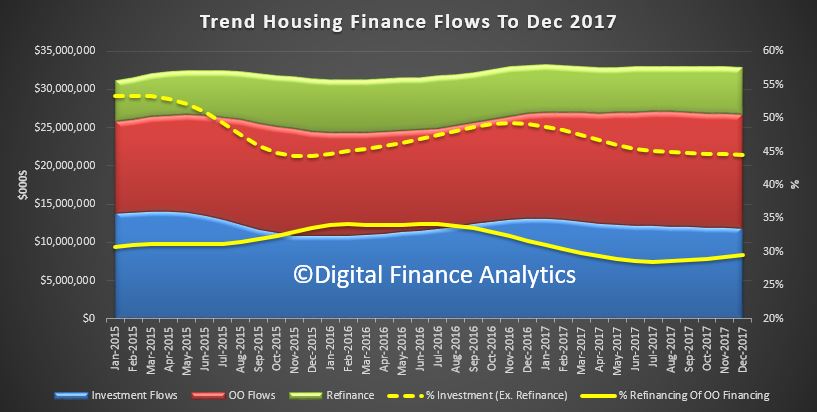

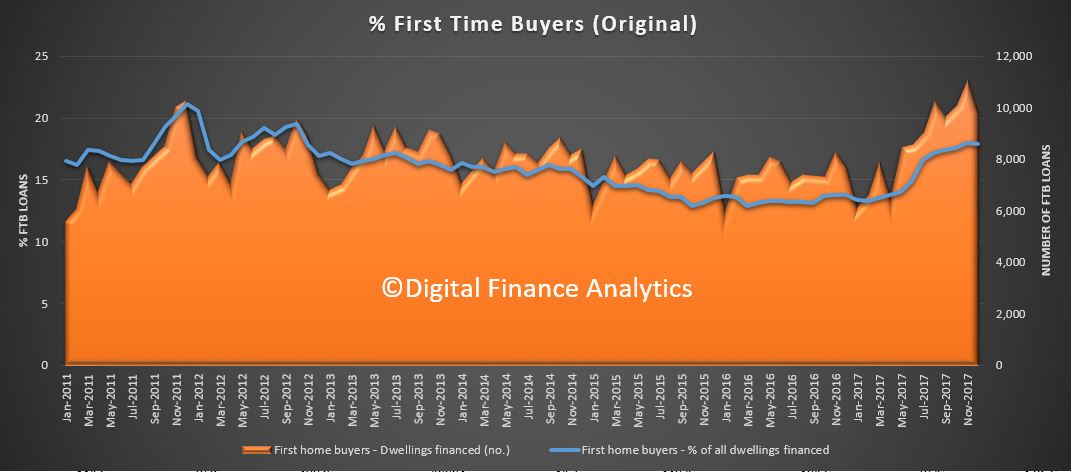

The latest Housing Finance Data from the ABS shows a fall in flows in December. In trend terms, the total value of dwelling finance commitments excluding alterations and additions fell 0.1% or $31 million. Owner occupied housing commitments rose 0.1% while investment housing commitments fell 0.5%. Owner occupied flows were worth $14.8 billion, and down 0.3% last month, while owner occupied refinancing was $6.2 billion, up 1.2% or $73 million. Investment flows were worth 11.9 billion, and fell 0.5% or $62 million. The percentage of loans for investment, excluding refinancing was 45%, down from 49% in Dec 2016. Refinancing was 29.5% of OO transactions, up from 29.2% last month. Momentum fell in NSW and VIC, the two major states. In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 17.9% in December 2017 from 18.0% in November 2017 – the number of transactions fell by 1,300 compared with last month. But the ABS warns that the First Time Buyer data may be revised and users should take care when interpreting recent ABS first home buyer statistics. The ABS plans to release a new publication which will see Housing Finance, Australia (5609.0) and Lending Finance, Australia (5671.0) combined into a single, simpler publication called Lending to Households and Businesses, Australia (5601.0).

We continue to have data issues with mortgage lending, with the RBA in their new Statement on Monetary Policy saying it now appears unnecessary to adjust the published growth rates to undo the effect of regular switching flows between owner occupied and investment loans as they have been doing for the past couple of years. So now investor loan growth on a 6-month basis has been restated to just 2%. More fluff in the numbers! Additionally, the RBA will publish data on aggregate switching flows to assist with the understanding of this switching behaviour.

More data this week highlighting the pressures on households. National Australia Bank’s latest Consumer Behaviour Survey, shows the degree of anxiety being caused by not only cost of living pressures but also health, job security, retirement funding as well as Australian politics. Of all the things bothering Australian households in early 2018, nothing surpasses cost of living pressures. Over 50% of low income earners reported some form of hardship, with almost one in two 18 to 49-year-olds being effected.

Despite improved job conditions and households reporting healthier financial buffers, the overall financial comfort of Australians is not advancing, according to ME’s latest Household Financial Comfort Report. In its latest survey, ME’s Household Financial Comfort Index remained stuck at 5.49 out of 10, with improvements in some measures of financial comfort linked to better employment conditions – e.g. a greater ability to maintain a lifestyle if income was lost for three months – offset by a fall in comfort with living expenses.

We released the January 2018 update of our Household Financial Confidence Index, using data from our rolling 52,000 household surveys. The news is not good, with a further fall in the composite index to 95.1, compared with 95.7 last month. This is below the neutral setting, and is the eighth consecutive monthly fall below 100. Costs of living pressures are very real, with 73% of households recording a rise, up 1.5% from last month, and only 3% a fall in their living costs. A litany of costs, from school fees, child care, fuel, electricity and rates all hit home. You can watch our separate video on this.

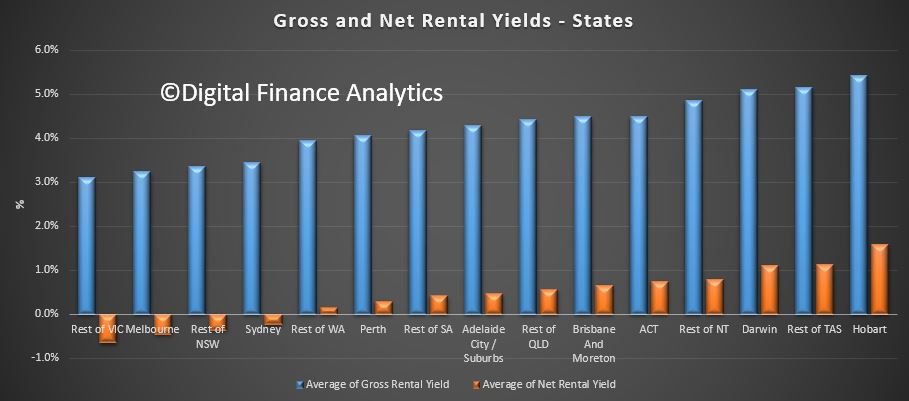

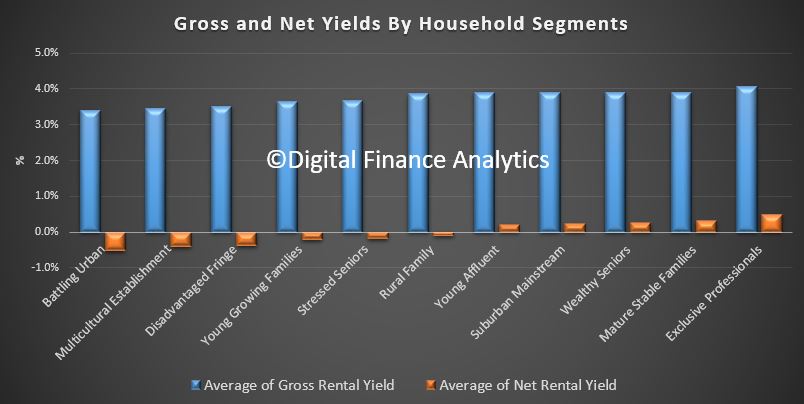

We also published updated data on net rental yields this week, using data from our household surveys. Gross yield is the actual rental stream to property value, net rental is rental payments less the costs of funding the mortgage, management fees and other expenses. This is calculated before any tax offsets or rebates. The latest results were featured in an AFR article. The results are pretty stark, and shows that many property investors are underwater in cash flow terms – not good when capital values are also sliding in some places. Looking at rental returns by states – Hobart and Darwin are the winners; Melbourne, and the rest of Victoria, then Sydney and the rest of NSW the losers. The returns vary between units and houses, with units doing somewhat better, and we find some significant variations at a post code level. But we found that more affluent households are doing significantly better in terms of net rental returns, compared with those in more financially pressured household groups. Batting Urban households, those who live in the urban fringe on the edge of our cities are doing the worst. This is explained by the types of properties people are buying, and their ability to select the right proposition. Running an investment property well takes skill and experience, especially in the current rising interest rate and low capital growth environment. Another reason why prospective property investors need to be careful just now.

Finally, we saw market volatility surge, as markets around the world gyrated following the “good news” on US Jobs last week, which signalled higher interest rates. In our recent video blog we discussed whether this is a blip, or something more substantive. We believe it points to structural issues which will take time to play out, so expect more uncertainly, on top of the correction which we have already had. This will put more upward pressure on interest rates, and also on bank funding here.

Overall then, a week which underscores the uncertainly across the finance sector, and households. This will not abate anytime soon, so brace for a bumpy ride. And those managing our large banks will need to adapt to a fundamentally different, more competitive landscape, so they are in for some sleepless nights.

If you found this useful, do like the post, add a comment and subscribe to receive future updates. Many thanks for taking the time to watch.

An ABC segment on the issues facing the Royal Commission, with reference to poor lending practice, including comments from DFA.

The royal commission — the one the Government still doesn’t want — opens its doors on Monday, February 12, and is sure to hear more harrowing stories of bad behaviour by banks.

It’s officially known as the Royal Commission into Misconduct in the Banking, Superannuation, and Financial Services Industry. Given the big banks dominate the sector, it is really a royal commission into banks.

Even as the banks tell everyone who will listen they have lifted their game — and in some areas they have — the bad news stories keep on coming.

Treasurer Morrison has release the report by King & Wood Mallesons partner Scott Farrell today in to open banking which aims to give consumers greater access to, and control over, their data. It mirrors recent UK developments, and is another nail in the competitive advantage the large players currently have. Later the scheme could be widened to other industry sectors, such as energy or telecommunications.

This “open banking” regime mean that customers, including small businesses, can opt to instruct their bank to send data to a competitor, so it can be used to price or offer an alternative product or service.

The report recommends that the open banking regime should apply to all banks, though with the major banks to join it first. For non-banks and fintechs, the report wants a “graduated, risk-based accreditation standard”. Superannuation funds and insurers are not included for now.

In fact, all authorised deposit-taking institutions (ADIs) will automatically be accredited to receive data.

There are exclusions. For example, value added data which is created by banks as a result of their analysis will not be included in the regime. Know your customer data though should be sharable. De-identified aggregate data would not be sharable.

Data provided under the regime will initially be “read only”, but the successful adoption of open banking “could also lead to ‘write access’ reforms” in the future. The following products are called out as in scope.

Transfer of data should be made free of charge, the report says.

Safeguards will be important, including under the Privacy Act, and a customer’s consent under Open Banking must be explicit, fully informed and able to be permitted or constrained according to the customer’s instructions. Joint accounts will need some special considerations in terms of authority, and advice.

An appropriate data standard will need to be agreed, and a clear and comprehensive framework for the allocation of liability between participants in Open Banking should be implemented. This framework should make it clear that participants in Open Banking are liable for their own conduct, but not the conduct of other participants. To the extent possible, the liability framework should be consistent with existing legal frameworks to ensure that there is no uncertainty about the rights of customers or liability of data holders.

In terms of implementation, data holders should be required to allow customers to share information with eligible parties via a dedicated application programming interface, not screen scraping.

The starting point for the Standards for the data transfer mechanism should be the UK Open Banking technical specification.

A period of approximately 12 months between the announcement of a final Government decision on Open Banking and the Commencement Date should be allowed for implementation. From theCommencement Date, the four major Australian banks should be obliged tocomply with a direction to share data under Open Banking. The remaining AuthorisedDeposit-taking Institutions should be obliged to share data from 12 months after the

Commencement Date, unless the ACCC determines that a later date is more appropriate.

The ACCC as lead regulator should coordinate the development and implementation of a timely consumer education programme for Open Banking. Participants, industry groups and consumer advocacy groups should lead and participate, as appropriate, in consumer awareness and education activities.

The ABA welcomed the report:

Banks are excited to enter the Open Banking age that will spark new innovations and deliver cutting edge products, with customers the big winner.

The Farrell Report into Open Banking released by the Treasurer today recognises both the opportunities and challenges that data sharing will bring. While the Australian Bankers’ Association has some concerns surrounding the implementation, the report lays out a broadly sensible path to Open Banking. Mr Farrell’s report should be commended for its focus on customers and its commitment to work with stakeholders to design a safe and secure data sharing framework.

Giving customers greater access to their own data will boost choice in banking and further simplify the application process for a financial product.

Australians have one of the most innovative and technologically advanced banking systems in the world. Examples of this is 24-hour banking, payWave and the soon to be launched PayID and New Payments Platform.

As the Productivity Commission affirmed this week, Australian banks are at the forefront of global innovation which has delivered a superior customer experience. Investments in how banks use data are already leading to new innovations that are improving the customer experience and this is set to continue under Open Banking.

A reform as large as Open Banking must be carefully considered and properly implemented.

Research shows that Australians trust their banks with personal information, more than online retailers, social media companies and even governments. It’s important that banks maintain this trust and ensure that the open data reforms don’t place personal information at risk.

Banks will continue to work with stakeholders like consumer groups, FinTech’s, regulators and government to get this right so it is a good model for all industries and customers are protected.

The ABA looks forward to carefully analysing Mr Farrell’s report and working with members and stakeholders to address any challenges to ensure its success. Banks would also like to thank Mr Farrell for his thorough and thoughtful inquiry

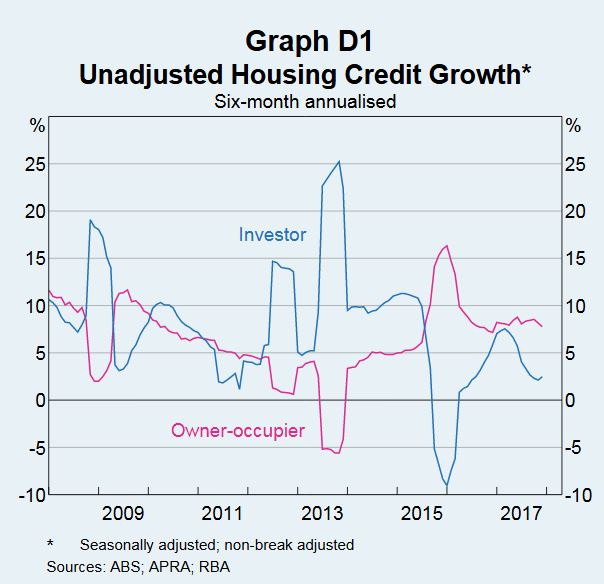

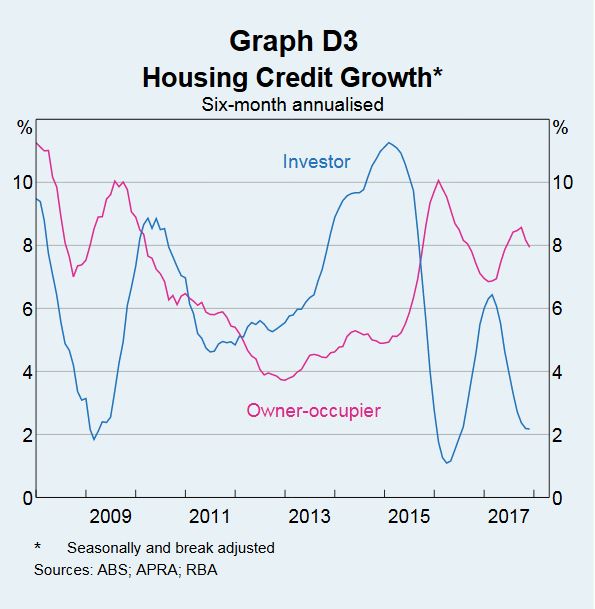

The RBA published their Statement on Monetary Policy today. The key themes were foreshadowed yesterday, but there was in interesting side discussion on the housing loans data. They says it now appears unnecessary to adjust the published growth rates to undo the effect of regular switching flows between owner occupied and investment loans. So now investor loan growth on a 6 month basis has been restated to just 2%. More fluff in the numbers!

Developments in investor and owner-occupier housing credit have attracted considerable attention in recent years. The RBA publishes these data as part of Australia’s Financial Aggregates on a monthly basis.

Measuring the Level and Growth Rate of Housing Credit

The Financial Aggregates statistical release contains data on the levels of credit extended by financial intermediaries to Australian businesses and households, including the levels of investor and owner-occupier housing credit. Sometimes, factors other than demand and supply can affect the growth of these series (Graph D1). Examples include changes in the availability of data from lenders, or changes arising from lenders reporting a reclassification of investor and owner occupier loans at a particular time. Each month, based on information provided by institutions, the RBA makes an assessment about whether any of the changes in the unadjusted data are being driven by such reporting changes. The RBA publishes growth rates adjusted to remove the effect of these breaks in order to aid the interpretation of the underlying growth in credit.

Switching Between Investor and Owner-occupier Housing Loans

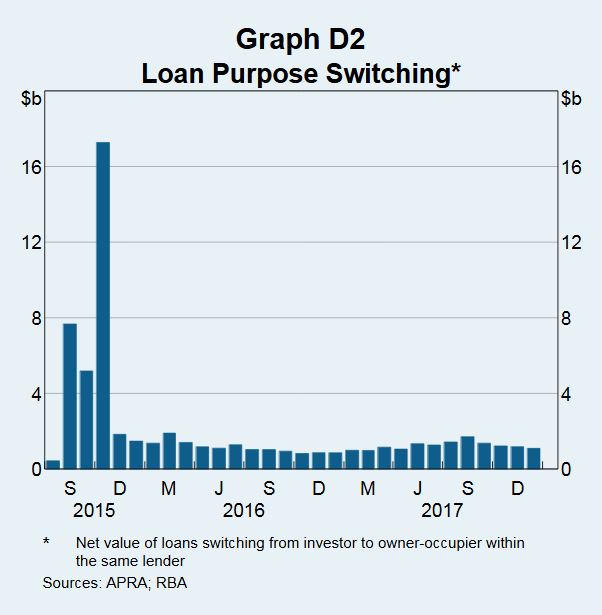

In mid 2015, some banks decided to introduce interest rate differentials between investor and owner-occupier housing loans in response to regulatory measures. For a few months thereafter, a large amount of outstanding housing credit was reported as having switched from investor to owner-occupier (Graph D2).

While the published growth rates for total housing credit were not affected by this switching, it had a substantial effect on the unadjusted growth rates of investor and owner-occupier credit. It was considered likely that many of these loans had switched purpose at some earlier date. But there was a greater incentive to report such switches after the pricing differential came into effect. So a decision was made to adjust the published growth rates for investor and owner-occupier credit to remove the effect of this switching.

Following the large amount of switching that initially occurred around the second half of 2015, the amount of switching each month has decreased significantly and appears to have been relatively stable for some time now. Indeed, these flows appear to reflect consistent behaviour that occurs from month to month. As a result, it now appears unnecessary to adjust the published growth rates to undo the effect of these regular switching flows. Accordingly, henceforth, adjustments for switching flows will only be applied to the growth figures over the period from mid to late 2015 when reported switching was unusually large, but not thereafter. The resulting break-adjusted growth rates are shown in Graph D3. Additionally, the RBA will publish data on aggregate switching flows to assist with the understanding of this switching behaviour.

In trend terms, the total value of dwelling finance commitments excluding alterations and additions fell 0.1% or $31 million. Owner occupied housing commitments rose 0.1% while investment housing commitments fell 0.5%.

Owner occupied flows were worth $14.8 billion, and down 0.3% last month, while owner occupied refinancing was was $6.2 billion, up 1.2% or $73 million. Investment flows were worth 11.9 billion, and fell 0.5% or $62 million. The percentage of loans for investment, excluding refinancing was 45%, down from 49% in Dec 2016. Refinancing was 29.5% of OO transactions, up from 29.2% last month.

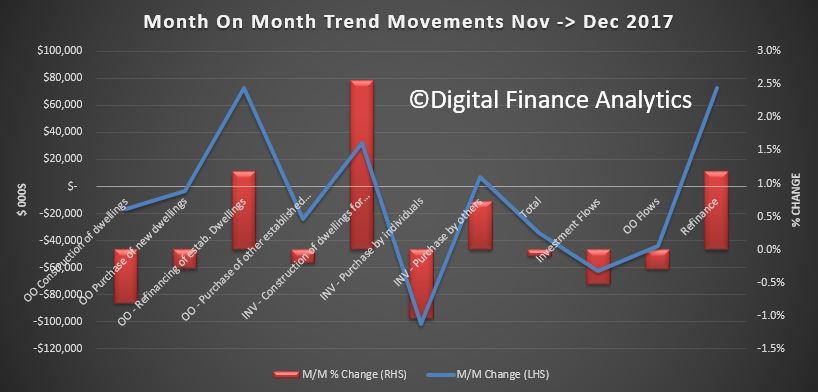

The number of commitments for owner occupied housing finance fell 0.3% in December 2017.

The number of commitments for the construction of dwellings fell 0.8%, the number of commitments for the purchase of established dwellings fell 0.3% and the number of commitments for the purchase of new dwellings fell 0.1%.

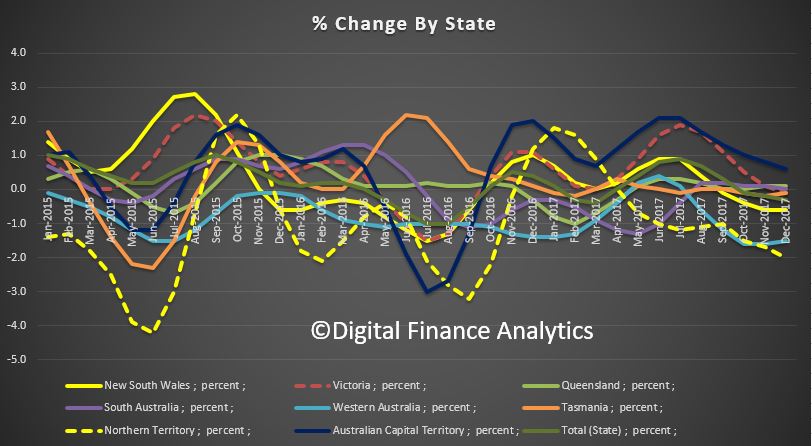

Momentum fell in NSW and VIC, the two major states.

In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments fell to 17.9% in December 2017 from 18.0% in November 2017.

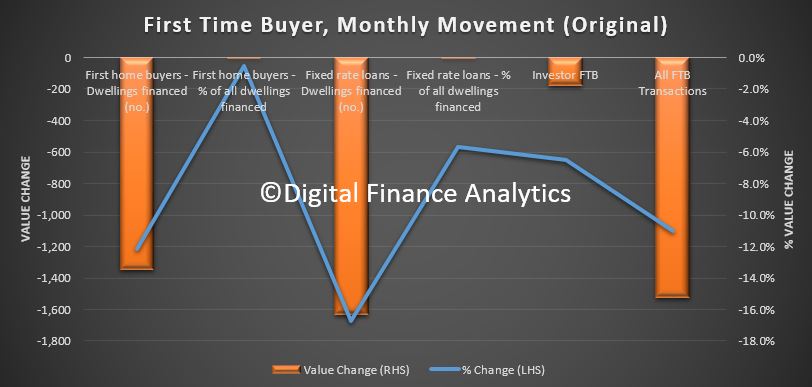

The number of transactions fell by 1,300 compared with last month. The proportion of fixed rate loans also fell.

We also saw a fall in first time buyer investors, from our own surveys.

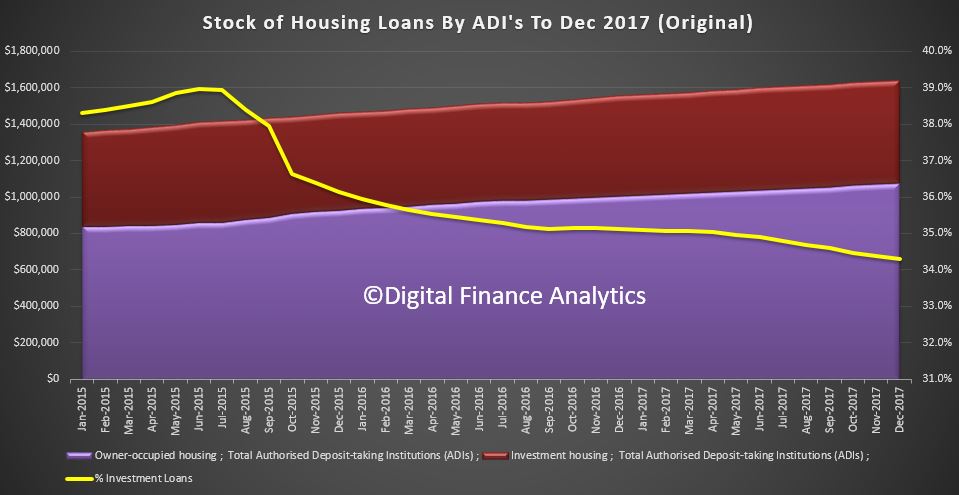

In original terms the stock of housing loans with ADI’s rose 0.5% in the month to $1.68 trillion. 34.3% of loans are for property investment purposes.

The ABS pointed out that the First Time Buyer data is under review, and new housing datasets are on their way.

The number of loans to first home buyers has recorded strong growth in recent months. The increase has been driven mainly by changes to first home buyer incentives made in July by the New South Wales and Victorian governments. The ABS is working with APRA and the financial institutions to establish the size of the increase in first home buyer lending in recent months and improve the quality of first home buyer statistics more broadly. These numbers may be revised and users should take care when interpreting recent ABS first home buyer statistics.

FORTHCOMING CHANGES

A new publication will soon be released which will see Housing Finance, Australia (5609.0) and Lending Finance, Australia (5671.0) combined into a single, simpler publication called Lending to Households and Businesses, Australia (5601.0).

To enable users to prepare for the new publication, tables of data in the new publication format will be released no less than one month prior to the first release of Lending to Households and Businesses, Australia (5601.0).

Significantly, he says the temporary measures taken to address too-free mortgage lending will morph into the more permanent focus on amongst other things, further strengthening of borrower serviceability assessments by lenders, strengthened capital requirements for mortgage lending imposed by us, and comprehensive credit reporting being mandated by the Government.

Bank capital

One area that was of interest to this audience last year was the strengthening of banking system capital. On that front, I’m pleased to say we are getting close to the end of the journey.

As some of you would know, the Australian Government conducted a broad-ranging inquiry into the Australian Financial System in 2014. Amongst other things, that inquiry tasked us with ensuring that Australian banks had ‘unquestionably strong’ capital ratios. In July last year, we published a paper setting out the benchmarks that we considered to be consistent with that goal. At a headline level, this required the four major Australian banks to strengthen their capital ratios, relative to end 2016 levels, by around 100 basis points on average to target CET1 ratio of 10.5 per cent (or about 16 per cent on an internationally comparable basis). We also said we expected that strengthening should be achieved by 2020 at the latest.

As things stand, the major banks haven’t quite hit this target yet, but are well on the way to doing so in an orderly fashion. We set a smaller task for the smaller institutions, and they by and large have it covered already.

That capital build-up is important because, as you’re all no doubt aware, we received a Christmas present from the Basel Committee in the form of the long-awaited package of reforms to finalise Basel III. The changes, in total, represent a significant overhaul of many components of the capital framework1.

We have, however, committed to ensure that changes in capital requirements emanating from Basel will be accommodated within the unquestionably strong target we have set. In other words, given the banking system has largely built the necessary capital, the recent Basel announcement does not have any real impact on the aggregate capital needs of the Australian banks. They will change the relative allocation of capital within the system, but not add to the aggregate requirement beyond what has already been announced.

We’ll begin consultation on the proposed approach to implementing Basel III changes in the next week or two. Our initial public release will include indicative risk weights, but these will be subject to further analysis and an impact study to calibrate the final proposed risk weights and ensure we end up with a capital requirement that is consistent with our assessment of unquestionably strong capital levels. We also have some recent input from the Productivity Commission to feed into our deliberations, which we’ll give consideration to as we work through the consultation process.

In terms of timelines, the Basel Committee has agreed to an implementation timetable commencing in 2022, with further phase-ins after that. As I said earlier, we expect banks to be planning to increase their capital strength to exceed the ‘unquestionably strong’ benchmarks by the beginning of 2020. Whether we implement our risk weight changes in line with Basel timeframes or modify that timeline somewhat, it’s unlikely there will be any need for additional phase-in and transitional arrangements given the industry will be well placed to meet the new requirements.

And just quickly on the other key components of the Basel reforms, we instituted the Basel liquidity and funding requirements in line with the internationally agreed timetable – the Liquidity Coverage Ratio (LCR) from 2015, and the Net Stable Funding Ratio (NSFR) from the beginning of this year – in full and without any transition. So the adjustment process to the post-crisis international reforms in Australia has the finish line well in sight.

Housing

The other topic that generated some questions last year concerned housing, and so I thought I should say a few words about our actions in that area.

The broad environment – high house prices, high household debt, low interest rates, and subdued household income growth – hasn’t changed greatly over the past 12 months (although in more recent times house price appreciation has certainly slowed in the largest cities – Sydney and Melbourne). Those conditions are not unique to Australia – a number of other jurisdictions continue to battle with somewhat similar conditions and imbalances. What’s notable for Australia, however, is the relatively high proportion of mortgage lending on the banking system’s balance sheet.

Against that backdrop, and amidst strong competitive pressures among lenders, the quality of new mortgage lending and the re-establishment of sound lending standards have been a major focus of APRA for the past few years now. We introduced industry-wide benchmarks on (in 2014) lending to investors and (in 2017) lending on interest-only terms. As I have spoken about many times previously, these are temporary measures we have put in place to deliberately temper competitive pressures, which were having a negative impact on lending practices throughout the industry, and help to moderate the volume of new lending with higher risk characteristics. Left unchecked, the drive for growth and market share was producing an adverse outcome as lenders sought ways to accommodate higher risk propositions to grow new lending volumes. Instead of prudently trimming their sails to reflect an environment of heightened risk, lenders were pressured to sail closer to the wind.

Over time, our interventions have served their purpose and we have seen lending standards improve. Our most recent intervention was in relation to interest-only lending. Imposing quantitative limits is not our preferred modus operandi, but over many years we’d seen interest-only loans become easily available, and options for extending or refinancing on interest-only terms allowed borrowers to avoid paying down debt for prolonged periods. Those loans do, however, provide less protection to borrower and lender when house prices soften, and expose borrowers to ‘repayment shock’ when the loan begins amortising (made worse if it occurs at a time when interest rates are rising from a low base).

Our benchmark of no more than 30 per cent of new lending being on interest-only terms is not overly restrictive for borrowers who genuinely need this form of finance – roughly 1-in-3 loans granted can still be on an interest-only basis – but it has required the major interest-only lenders to establish strategies that incentivise more borrowers to repay their principal. The industry has been quite successful in doing so: recent data for the last quarter of 2017 shows that only about 1-in-5 loans were interest-only, and the number of interest-only loans with high LVRs continued to fall to quite low levels. All of that is positive for the quality of loan portfolios.

While the direction in asset quality is positive, we’re not declaring victory just yet. We still want to see that the improvements the industry has made are truly embedded into industry practice. And we can modify our interventions as more permanent measures come into play. That will include, amongst other things, further strengthening of borrower serviceability assessments by lenders, strengthened capital requirements for mortgage lending imposed by us, and comprehensive credit reporting being mandated by the Government. Through these initiatives, we are laying the platform to make sure prudent lending is maintained on an ongoing basis.

Governance and culture

In addition to improvements in financial strength and asset quality, it’s also critical to the long run health of the financial system that the Australian community has a high degree of confidence that individual financial institutions are well governed and prudently managed. What has become more apparent and pronounced over the past year is that – despite their financial health and profitability – community faith in financial institutions in Australia, as has been the case elsewhere, has been eroded due to too many incidences of poor behaviour and poor customer outcomes. None of these have thus far threatened the viability of any institution, but they have certainly not been without commercial and reputational damage.

While most matters of conduct are primarily the responsibility of our colleagues at ASIC, these issues are nevertheless of great interest to a prudential regulator for what they say about an organisation’s attitudes towards risk. So as with the balance sheet strengthening of the financial system over the past few years, we have also taken a greater interest in efforts to strengthen behaviours and cultures. We can’t regulate these into existence, but we have been working to ensure Australian financial institutions have been giving greater attention to these matters than may have traditionally been the case. On these issues, it’s fair to say the journey continues.

We track gross and net rental yields on investment properties via our household surveys. Gross yield is the actual rental stream to property value, net rental is rental payments less the costs of funding the mortgage, management fees and other expenses. This is calculated before any tax offsets or rebates. The latest results were featured in an AFR article today.

The results are pretty stark, and shows that many property investors are underwater in cash flow terms – not good when capital values are also sliding in some places.

This shows the gross and net rental returns by states – Hobart and Darwin are the winners, Melbourne, and the rest of Victoria, then Sydney and the rest of NSW the loosers.

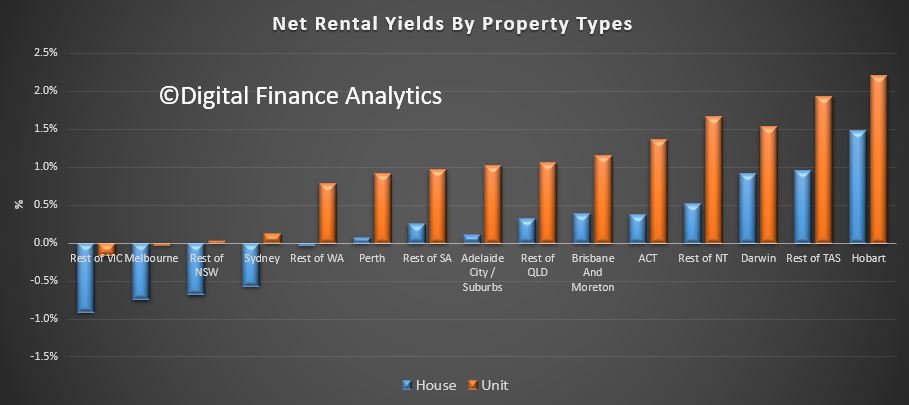

The returns vary between units and houses, with units doing somewhat better.

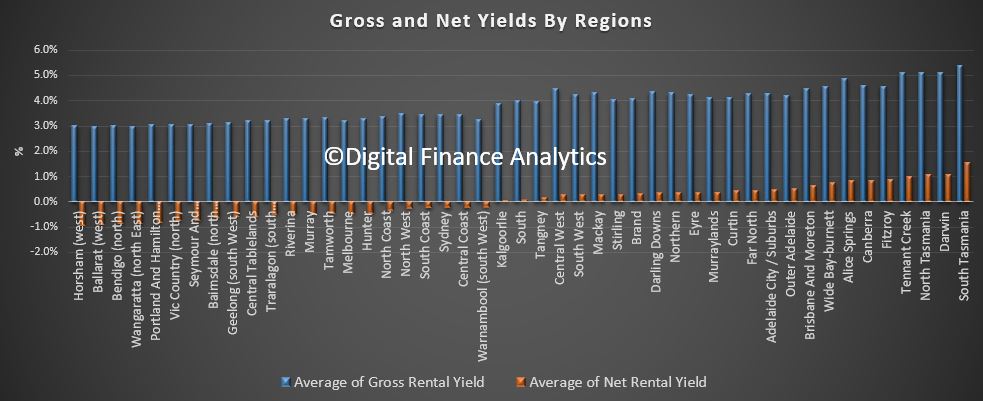

Here is a view by regions.

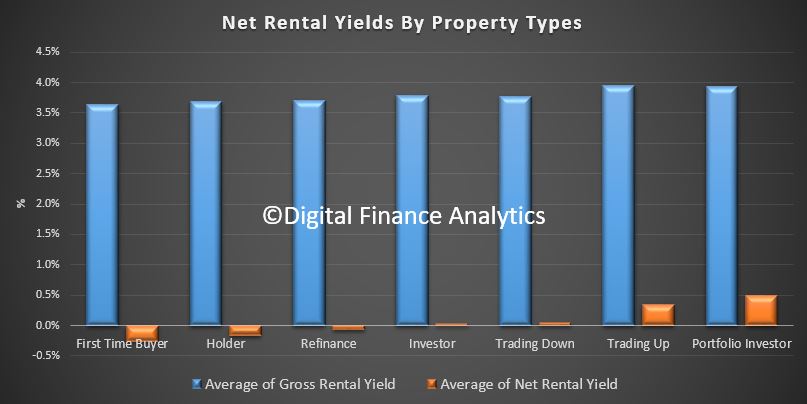

We find that portfolio property investors (those with multiple investment properties) are doing the best, whilst new investor buyers are doing the worse, not least because they have larger mortgages to service, and interest rates are higher, and no capital growth.

Finally, here is the killer slide. More affluent households are doing significantly better in terms of net rental returns, compared with those in more financially pressured household groups. Batting Urban households, those who live in the urban fringe on the edge of our cities are doing the worst. This is explained by the types of properties people are buying, and their ability to select the right proposition. Running an investment property well takes skill and experience, especially in the current rising interest rate and low capital growth environment. Another reason why prospective property investors need to be careful just now.

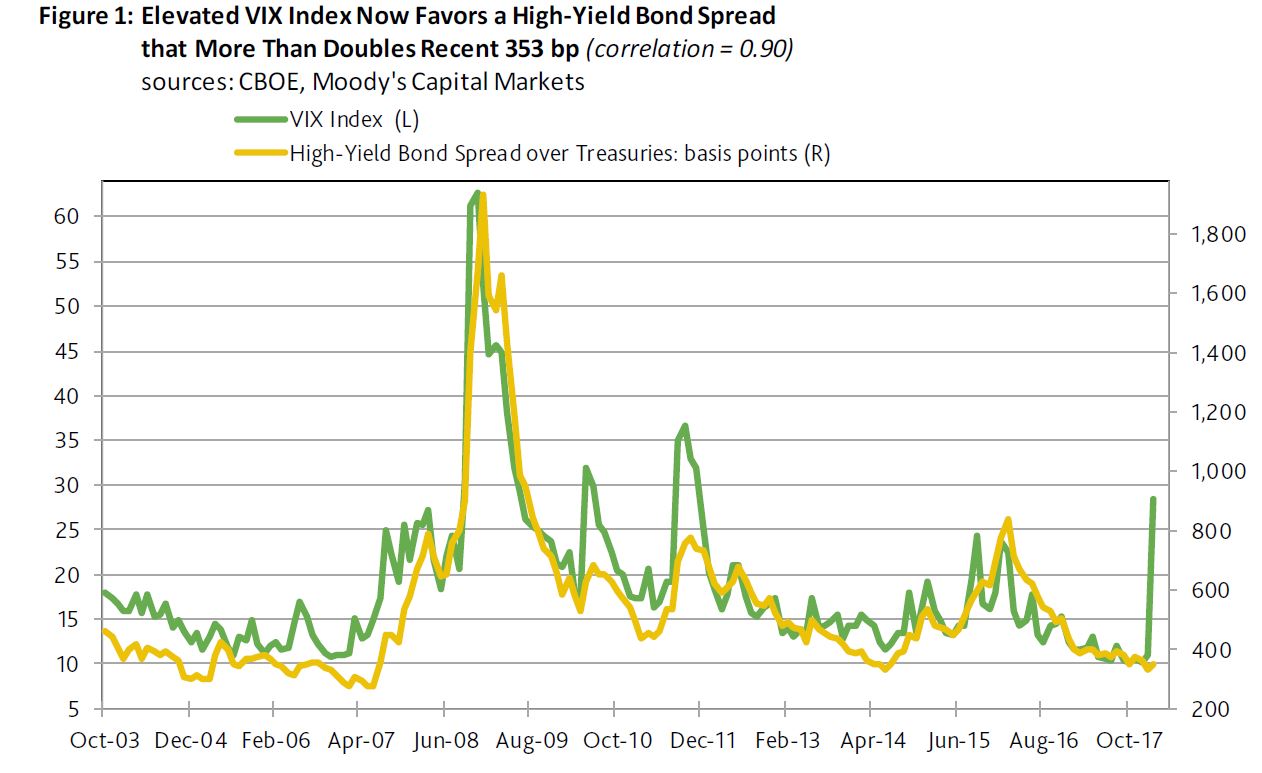

Thus far, the corporate credit market has been relatively steady amid equity market turmoil. Corporate credit’s comparative calm stems from expectations of continued profit growth that underpins a still likely slide by the high-yield default rate. The record shows that 90% of the year-to-year declines by the default rate were joined by year-to-year growth for the market value of U.S. common stock.

Today’s positive outlooks for business sales and operating profits suggest that equities will recover once issues pertaining to interest rates are sufficiently resolved. For now, equities may be paying dearly for having been more richly priced vis-a-vis fundamentals when compared to corporate bonds.

Since the VIX index’s current estimation methodology took effect in September 2003, the high-yield bond spread has generated a strong correlation of 0.90 with the VIX index. However, for now that ordinarily tight relationship has broken down. Never before has the high-yield bond spread been so unresponsive to a skyrocketing VIX index.

The VIX index’s 28.5-point average of February-to-date has been statistically associated with an 832-basis-point midpoint for the high-yield bond spread. Instead, the high-yield bond spread recently approximated 353 bp. Thus, the high-yield spread predicted by the VIX index now exceeds the actual spread by a record 479 bp.

The old record high gap was the 364 bp of October 2008, or when the actual spread of 1,398 bp would eventually surpass the 1,762 bp predicted by the VIX index. Not long thereafter, the actual high-yield spread would peak at the 1,932 bp of December 2008.

More recently, or during the euro zone crisis of 2011, the 1,018 bp high-yield spread predicted by the VIX index was as much as 323 bp above August 2011’s actual spread of 695 bp. After eventually peaking at October 2011’s 775 bp, the spread narrowed to 590 bp by August 2012.

What transpired following August 2011 and October 2008 warns against being too quick to dismiss the possibility of at least a 100 bp widening by the latest high-yield spread. Nevertheless, high-yield spreads would be significantly thinner one year after the gap between the predicted and actual spreads peaked.

For example, by August 2012, the high-yield spread had narrowed to 590 bp, while the spread had thinned to 737 bp by October 2009.

Something appears to be very wrong with risk management at the Commonwealth Bank (CBA), that cuts right across the bank. There have been risk management problems in the retail (money laundering), institutional banking (foreign exchange and bank bill swap rate benchmark manipulation) and wealth management (Comminsure scandal) arms of the bank.

And the responsibility, the accountability for risk management stops, and starts, with the bank’s board.

In presenting its 2018 half yearly profits, the CBA board announced that the bank had set aside provisions of A$375 million in anticipation of a penalty resulting from failures to properly implement anti-money laundering controls.

In the media conference following the appointment of Matt Comyn as the new CEO of CBA, the chair of the banks’ board Catherine Livingstone, admitted, while it was:

…entirely appropriate to share a collective accountability for the issues that we have had… [that] the processes around operational risk management and compliance risk management…is where we have not performed as we should have.

In his first media conference as CEO, Mr Comyn, not surprisingly, concurred with his new boss.

And it became unanimous, when a few days later the progress report of the Australian Prudential Regulation Authority’s Prudential Inquiry Panel into the culture at CBA, reported that investigations were being focused on “capabilities and accountabilities for risk management in the organisation, particularly for operational, compliance and reputational risk”.

How the CBA manages risk

CBA’s latest annual report describes in some detail the risk management framework that is supposed to direct risk management across the bank. The framework, which incorporates the requirements of APRA’s prudential standard for risk management, comprises three main components: a risk appetite statement (which describes the types and maximum levels of risk that the board is willing to accept), a three year rolling group business plan and a risk management strategy.

The bank’s risk appetite is formulated by the Board Risk Committee, approved by the board, and dictates the levels of risk-taking in each business line.

In practise the bank actually follows what is called a Three Lines of Defence model. The so-called first line of defence is business management, which is responsible for the effective implementation of the board-approved risk management framework.

The second line is a separate group of staff with specific risk management skills to develop and monitor the risk management process. The third and last line is an independent group that acts as an internal audit function.

CBA is a large and complex organisation, and naturally there is a large, complex risk bureaucracy. This is detailed in the bank’s latest risk report.

However, APRA is clear that the board should take ultimate responsibility.

The lines of defence are clearly broken. If there had been one single, or maybe two, risk management failures at CBA, you could put it down to complexity, teething problems or just bad luck. But over the last decade, there has been a catalogue of bad risk decisions affecting the bank’s customers, shareholders and the Australian financial system.

After the first few times, surely the effectiveness of the risk framework and the three lines of defence should have been questioned and remedial action taken? But apparently it was not, and there is now frantic action by the people responsible – the CBA board – to do something (anything) about it.

In the media conference, Catherine Livingstone and the new CEO repeatedly talked about “collective accountability” and tried to diffuse the severity of the situation by talking about “organisation wide” and “culture” issues, as if even the staff in the bank’s branches were somehow to blame.

In fact, in the case of money laundering through ATMs that has drawn the ire of AUSTRAC, it was the first line business staff in the branches who raised the alarm. Their warnings were not taken seriously. To claim that the lower-level staff are somehow “collectively accountable” is bordering on the bizarre.

The accountability for the risk management failures is indeed spread far and wide but by far and away it is the joint responsibility of the board and executive committee. The knee-jerk reaction to cut a few bonuses is insufficient.

Someone in the board of the bank has to resign or be fired. Where failures are detected, bonuses already paid out, for example to recently retired board members, should be retrieved.

And going forward, the three lines of defence must become a real protection for customers rather than a convenient pretence, and APRA must ensure, for customers’ sakes, that the three lines are operating effectively in all large financial institutions.

Author: Pat McConnell, Visiting Fellow, Macquarie University Applied Finance Centre, Macquarie University