We have updated our bank fee analysis, to take account of the 2013 data from the RBA. They collect fees data from 17 banks operating in Australia, covering over 90 per cent of total banking sector assets. Each bank provides data on income received over the financial year that is used as the basis for their public annual accounts. All fees are net of rebates and other concessions granted.

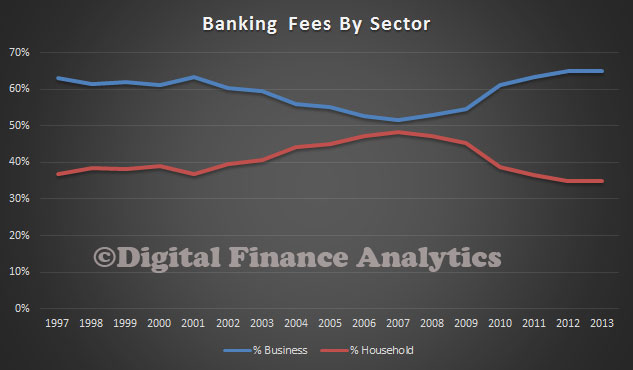

It does not include wealth management, broker, loan mortgage insurance, or other fees across financial services and the non-bank sector. The total reported in more than $11.6 bn, up 2.6% from 2012. Business fees grew at 2.8%, and Household fees at 2.3%. Business contributed around 65% of all fees in 2013.

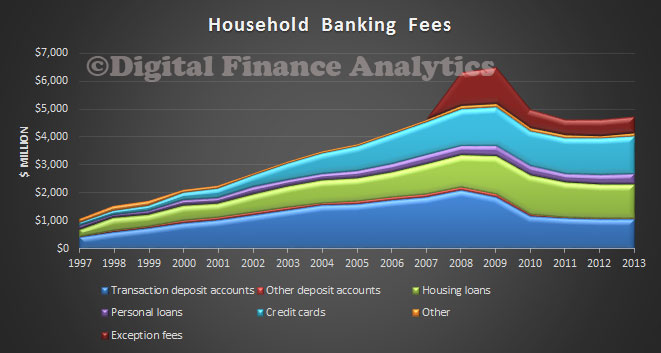

Looking at fees charged to households, we see total fees are below their 2009 peaks, when exception fees reach their highs, and before banking competition, led by nab initially, forced some fees down.

Looking at fees charged to households, we see total fees are below their 2009 peaks, when exception fees reach their highs, and before banking competition, led by nab initially, forced some fees down.

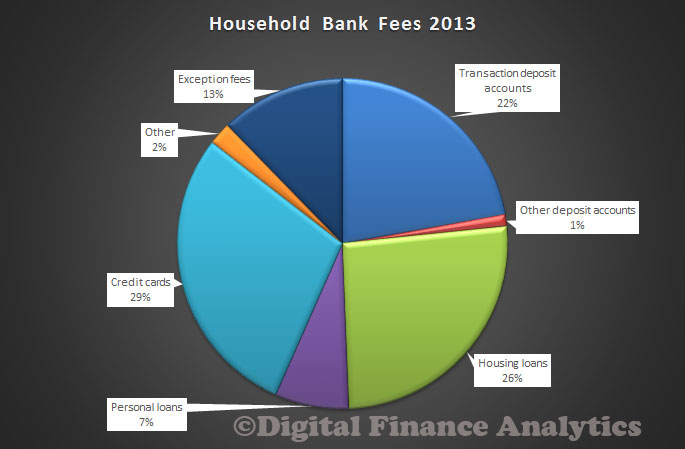

In 2013, credit cards remains the single largest source of fees at 29%, with housing loans at 26% and transaction deposit accounts 22%.

In 2013, credit cards remains the single largest source of fees at 29%, with housing loans at 26% and transaction deposit accounts 22%.

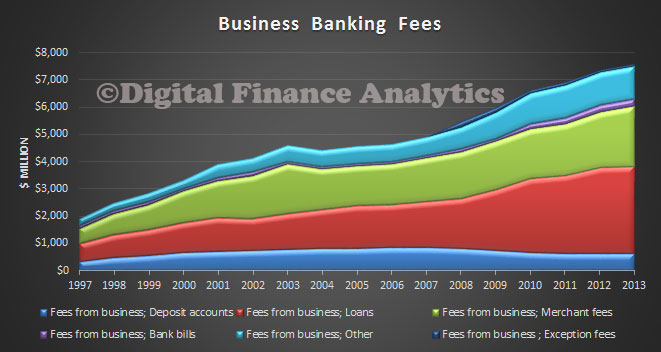

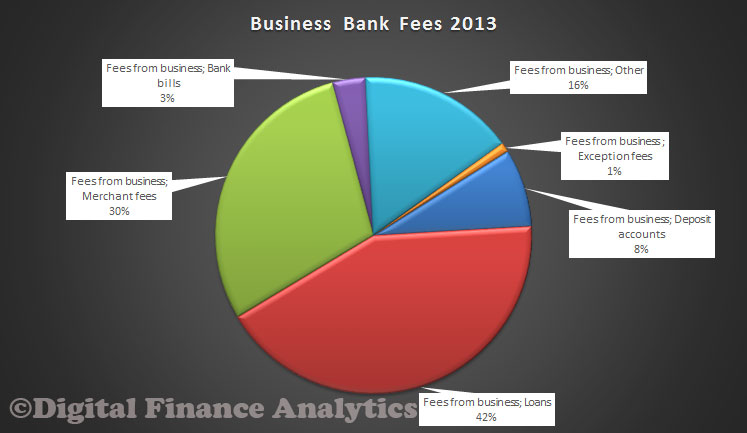

Looking at fees charged to businesses, we see a consistent rise. This is one reason why many small businesses continue to struggle.

Looking at fees charged to businesses, we see a consistent rise. This is one reason why many small businesses continue to struggle.

In 2013, 42% of fee income came from business loans, 30% from merchant service fees and 16% from other categories. Exception fees were around 1% of total business fees.

In 2013, 42% of fee income came from business loans, 30% from merchant service fees and 16% from other categories. Exception fees were around 1% of total business fees.

The RBA definitions are included below:

- Deposit account fees comprise mainly account-servicing and transaction fees, but also fees for overdrawing the account.

- Loans are either direct loans or accounts that have a facility to become overdrawn without penalty (particularly in the case of business loans). Loan account fees comprise mainly establishment and loan servicing fees.

- ‘Credit card’ fees comprise mainly annual fees, but also include late payment, over-limit, cash advance and foreign-currency conversion fees.

- ‘Other’ fees paid by households include fees from items such as travellers’ cheques, foreign currency transactions, and custodial services.

- Fees from business also include fees and charges collected from government entities, including statutory authorities and corporatised bodies.

- ‘Merchant fees’ include credit card and debit card fees charged to merchants, as well as non-transaction fees associated with the provision of terminal facilities.

- ‘Bank bills’ fees include activation, application, commitment, drawdown, facility, late presentation, and line fees.

- ‘Other’ business fees include export collections, foreign exchange guarantees, payroll service, safe custody and special clearance fees.

- ‘Exception fees’ are those charged by the bank when the customer breaches the terms of a banking product, typically by making a late payment or exceeding a credit limit on a credit card or by overdrawing a deposit account.

A few observations. First the data is likely to understate the total fees being paid, as it relates to 90% of bank assets, and does not include the non bank sector, and other financial services categories. The average household will be paying more than $500 each year. We ran our international fee benchmarks, and discovered that total fee take is line ball with other similar markets, but we still have more fees active in Australia – more than 200 fee categories for households!

So banking fees is a nice little earner for the banks. The class action on late payment fees continues with attention being directed to nine banks – Westpac, Citibank, ANZ, CBA, NAB, St.George, BankSA, BankWest and AmericanExpress.

For comparison purposes, more than $18.6bn is charged by the wealth management sector, and $1.5bn by mortgage brokers.

One thought on “Banking Fees Cost $11.6 bn”