Robo-advice is just as important to the future of Australian banks as the integration of superannuation platforms was in the 1990s, argues robo-adviser Clover. We agree, but cannibalisation and effective segmentation are the key issues yet to be addressed, as shown in results from our surveys.

Speaking to InvestorDaily, Clover chief executive Harry Chemay said the major Australian banks will have to address automated advice sooner rather than later.

“Robo-advice is as important to the future as superannuation was to the banks in the 1990s, when every bank started to buy a superannuation fund or platform to gain entry into the market,” Mr Chemay said.

“Now we’re seeing that the next stage is the technological implementation of wealth advice and wealth management.”

Mr Chemay predicted that many banks will attempt to build a robo-advice platform in-house, with Macquarie Bank “the first cab off the rank” with the launch of automated advice service Owners Advisory in 2015.

However, it will be “fundamentally difficult” for a bank to build out an automated advice solution for two reasons, he said: “You do need a very customer-centric approach, which is very user experience-driven design, and you need to be fairly agile,” Mr Chemay said.

“There’s no doubt that banks could do it, but if they adopt the traditional method of product development it will be slower to market and it will require substantial resources.”

The alternative is for banks to look at third parties such as Decimal or Ignition Wealth to provide an ‘out of the box’ white-label solution, he said.

That could, however, create compliance headaches down the track, Mr Chemay said, noting that ASIC has made it clear that the operation of advice algorithms is the responsibility of the wealth management firm, not the robo-adviser.

“Unlike a human-to-human interaction across a table, robo-advice is running 24/7 – it can potentially be generating advice all the time around the clock,” he said.

“And if something goes wrong with an algorithm, there is the potential for many people to get incorrect advice.”

Concerns such as these prompted Clover to apply for its own managed discretionary account licence from ASIC, with the licence approved by the regulator last week, according to Mr Chemay.

Clover will be moving a select few of its clients into a beta testing environment in the next few weeks, with a full launch targeted for July or early August 2016, he said.

Clover also has a relationship with industry fund Equipsuper, which is in the process of rolling out an automated advice solution to its members.

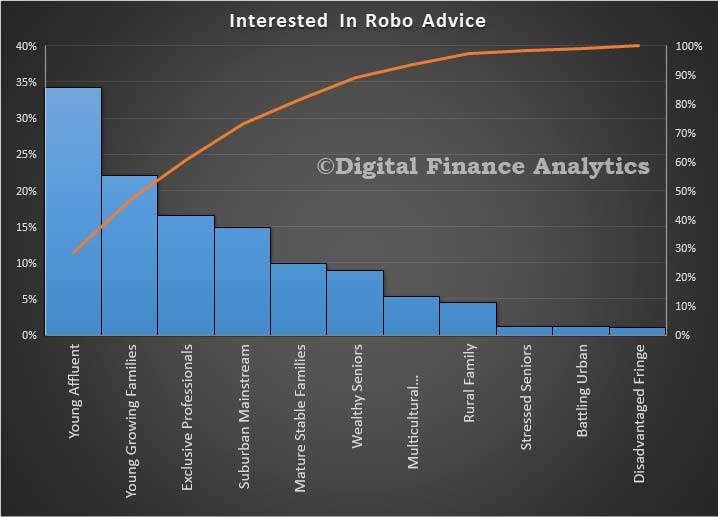

The additional point we would make is the potential cannibalisation of existing customers. Analysis we completed earlier in the year showed that those with existing advice relationships AND high digital alignment were most likely to consider Robo-Advice. Those who are digitally aligned, but not seeking advice showed no propensity to use such a service – at this point in time.

So two observations, first there are many different potential offerings which should be constructed on a Robo-Advice basis, as the needs, of young affluent, and very different from say exclusive professionals. So effective segmentation of the offers will be essential, and different personas will need to be incorporated into the systems being developed.

Second, the bulk of the interest lays with those who have had advice, so it may not, in the short term grow the advice pie. Indeed there appears to be strong evidence that existing advisors may find their business being cannabalised as existing clients switch to Robo-Advice. This is especially true if the range of options are greater, and the price point lower.

We therefore question the assumption expressed within the industry that Robo-Advice is not a threat, as it will simply expand the pie to segments which today do not seek advice. In fact, we suggest the clever play is to make it a tool, and aligned to Advisors, rather than a substitute for them. In addition, the marketing/education strategies need to be developed carefully. There is a lot in play here.