A progress report (the ninth) on adoption of the Basel regulatory framework was issued today by BIS. This report sets out the adoption status of Basel III regulations for each Basel Committee on Banking Supervision (BCBS) member jurisdiction as of end-September 2015. It updates the Committee’s previous progress reports, which have been published on a semiannual basis since October 2011.

Regarding the consistency of regulatory implementation, the Committee has published its assessment reports on 22 members – Australia, Brazil, Canada, China, nine members of the European Union, Hong Kong SAR, India, Japan, Saudi Arabia, Mexico, Singapore, South Africa, Switzerland and the United States – regarding their implementation of Basel III risk-based capital regulations, which are available on the Committee’s website. This includes all members that are home jurisdictions of global systemically important banks (G-SIBs). The Committee has also published five assessment reports (Hong Kong SAR, India, Saudi Arabia, Mexico and South Africa) on the domestic adoption of the Basel LCR standards. The assessments of Russia, Turkey, South Korea and Indonesia are under way, including consistency of implementation of both risk-based capital and LCR standards. Further, preparatory work for the assessment of G-SIB standards has already started in mid-2015 and its assessment work will start later this year. By September 2016, the Committee aims to have assessed the consistency of risk-based capital standards of all 27 member jurisdictions and the consistency of G-SIB standards of all five member jurisdictions that are home jurisdictions of G-SIBs.

The Basel III framework builds on and enhances the regulatory framework set out under Basel II and Basel 2.5. The structure of the attached table has been revamped (effective from October 2015) to monitor the adoption progress of all Basel III standards, which will come into effect by 2019. The monitoring table no longer includes the reporting columns for Basel II and 2.5, as almost all BCBS member jurisdictions have completed their regulatory adoption. The attached table therefore reviews members’ regulatory adoption of the following standards:

- Basel III Capital: In December 2010, the Committee released Basel III, which set higher levels for capital requirements and introduced a new global liquidity framework. Committee members agreed to implement Basel III from 1 January 2013, subject to transitional and phase-in arrangements.

- Capital conservation buffer: The capital conservation buffer will be phased in between 1 January 2016 and year-end 2018, becoming fully effective on 1 January 2019.

- Countercyclical buffer: The countercyclical buffer will be phased in parallel to the capital conservation buffer between 1 January 2016 and year-end 2018, becoming fully effective on 1 January 2019.

- Capital requirements for equity investment in funds: In December 2013, the Committee issued the final standard for the treatment of banks’ investments in the equity of funds that are held in the banking book, which will take effect from 1 January 2017.

- Standardised approach for measuring counterparty credit risk exposures (SA-CCR): In March 2014, the Committee issued the final standard on SA-CCR, which will take effect from 1 January 2017. It will replace both the Current Exposure Method (CEM) and the Standardised Method (SM) in the capital adequacy framework, while the IMM (Internal Model Method) shortcut method will be eliminated from the framework.

- Securitisation framework: The Committee issued revisions to the securitisation framework in December 2014 to strengthen the capital standards for securitisation exposures held in the banking book, which will come into effect in January 2018.

- Capital requirements for bank exposures to central counterparties: In April 2014, the Committee issued the final standard for the capital treatment of bank exposures to central counterparties, which will come into effect on 1 January 2017.

- Basel III leverage ratio: In January 2014, the Basel Committee issued the Basel III leverage ratio framework and disclosure requirements. Implementation of the leverage ratio requirements began with bank-level reporting to national supervisors until 1 January 2015, while public disclosure started on 1 January 2015. The Committee will carefully monitor the impact of these disclosure requirements. Any final adjustments to the definition and calibration of the leverage ratio will be made by 2017, with a view to migrating to a Pillar 1 (minimum capital requirements) treatment on 1 January 2018 based on appropriate review and calibration.

- Basel III liquidity coverage ratio (LCR): In January 2013, the Basel Committee issued the revised LCR. It came into effect on 1 January 2015 and is subject to a transitional arrangement before reaching full implementation on 1 January 2019.

- Basel III net stable funding ratio (NSFR): In October 2014, the Basel Committee issued the final standard for the NSFR. In line with the timeline specified in the 2010 publication of the liquidity risk framework, the NSFR will become a minimum standard by 1 January 2018.

- G-SIB framework: In July 2013, the Committee published an updated framework for the assessment methodology and higher loss absorbency requirements for G-SIBs. The requirements will be introduced on 1 January 2016 and become fully effective on 1 January 2019. To enable their timely implementation, national jurisdictions agreed to implement by 1 January 2014 the official regulations/legislation that establish the reporting and disclosure requirements.

- D-SIB framework: In October 2012, the Committee issued a set of principles on the assessment methodology and the higher loss absorbency requirement for domestic systemically important banks (D-SIBs). Given that the D-SIB framework complements the G-SIB framework, the Committee believes it would be appropriate if banks identified as D-SIBs by their national authorities were required to comply with the principles in line with the phase-in arrangements for the G-SIB framework, ie from January 2016.

- Pillar 3 disclosure requirements: In January 2015, the Basel Committee issued the final standard for revised Pillar 3 disclosure requirements, which will take effect from end-2016 (ie banks will be required to publish their first Pillar 3 report under the revised framework concurrently with their year-end 2016 financial report). The standard supersedes the existing Pillar 3 disclosure requirements first issued as part of the Basel II framework in 2004 and the Basel 2.5 revisions and enhancements introduced in 2009.

- Large exposures framework: In April 2014, the Committee issued the final standard that sets out a supervisory framework for measuring and controlling large exposures, which will take effect from 1 January 2019.

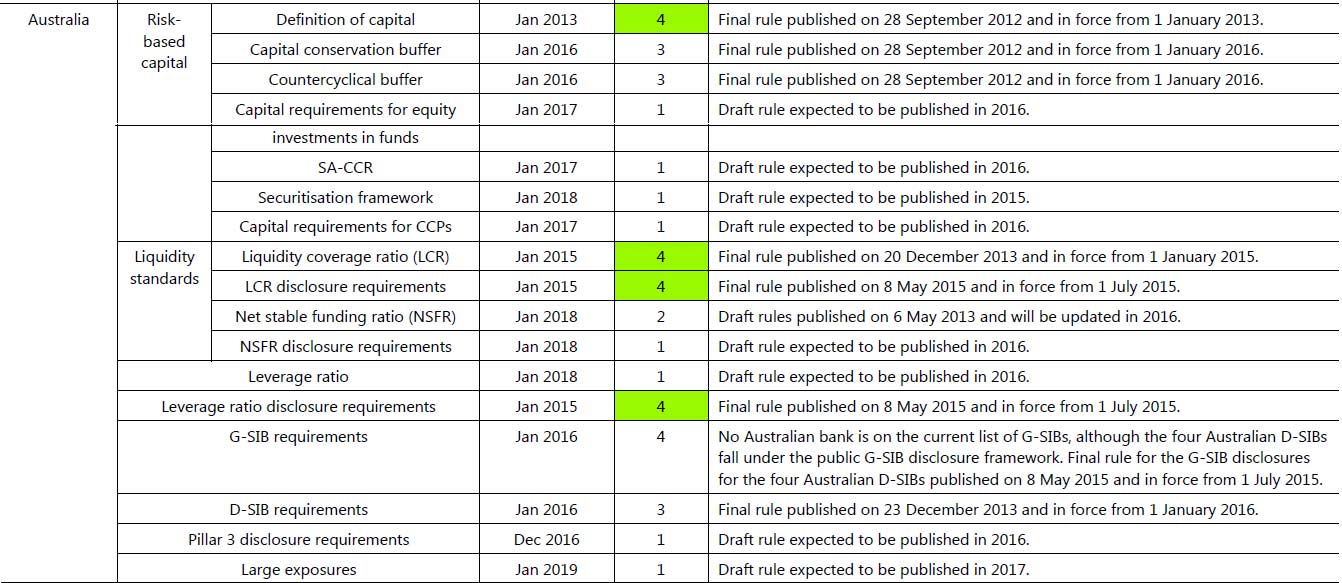

They published an assessment of Australia’s progress:

Still a long way to go; highly complex, and this is before Basel IV arrives. Is more complexity better?

Still a long way to go; highly complex, and this is before Basel IV arrives. Is more complexity better?