The Bank for International Settlements has featured the issues arising from high household debt in its December 2017 Quarterly Review. They call out the risks from high mortgage lending, high debt servicing ratios, and the risks to financial stability and economic growth. All themes we have already explored on the DFA Blog, but it is a well argued summary. Also note Australia figures as a higher risk case study. Here is a summary of their analysis.

Central banks are increasingly concerned that high household debt may pose a threat to macroeconomic and financial stability. This special feature seeks to highlight some of the mechanisms through which household debt may threaten both macroeconomic and financial stability.

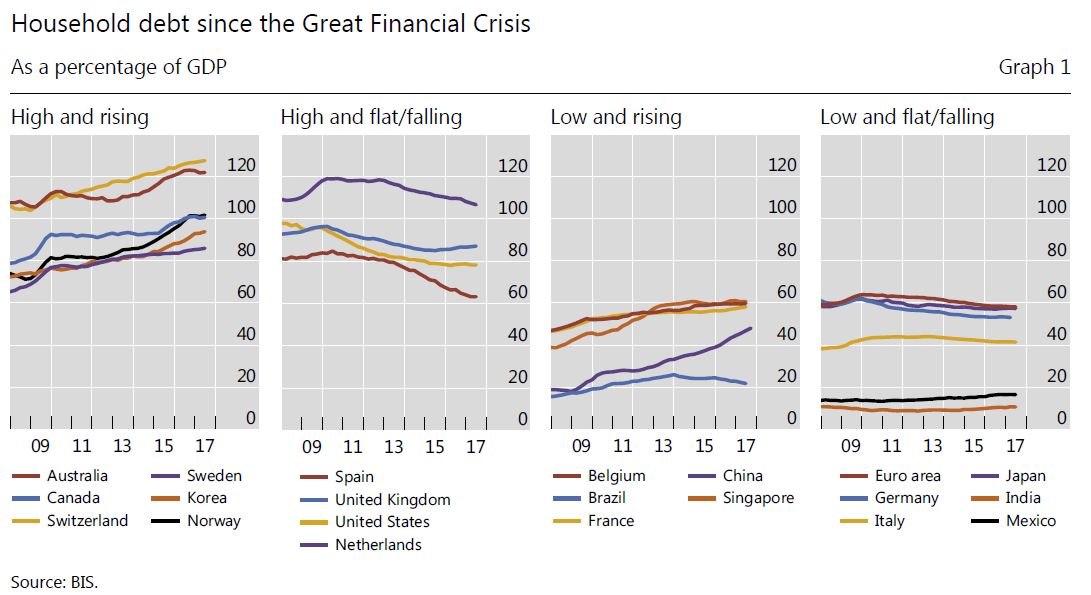

Australia is put in the “High and rising” category. The debt ratio now exceeds 120% in both Australia and Switzerland. Mortgages make up the lion’s share of debt (between 62 and 97%). In Australia mortgage debt has risen from 86% of household debt in 2007 to 92% in 2017.

High household debt can make the economy more vulnerable to disruptions, potentially harming growth. As aggregate consumption and output shrink, the likelihood of systemic banking distress could increase, since banks hold both direct and indirect credit risk exposures to the household sector.

High household debt can make the economy more vulnerable to disruptions, potentially harming growth. As aggregate consumption and output shrink, the likelihood of systemic banking distress could increase, since banks hold both direct and indirect credit risk exposures to the household sector.

They say the size of household debt burdens matters too. This is best measured by the ratio of interest payments and amortisation to income – the debt service ratio (DSR). They say that rising household debt can reflect either stronger credit demand or an increased supply of credit from lenders, or some combination of the two. In Australia, for instance, heightened

competition among lenders seems to have resulted in a relaxation of lending standards. In addition, the interest rate sensitivity of a household’s debt service burden is likely to matter. High debt (relative to assets) can make a household less mobile, and hence less able to adjust by finding a new or better job in another town or region. Homeowners may be tied down by mortgages on properties that have depreciated in value, especially those that are underwater (ie worth less than the loan balance).

These household-level observations have implications for aggregate demand and aggregate supply. From an aggregate demand perspective, the distribution of debt across households can amplify any drop in consumption. Notable examples include high debt concentration among households with limited access to credit (ie close to borrowing constraints) or less scope for self-insurance (ie low liquid balances).

Since poorer households are more likely to face these credit and liquidity

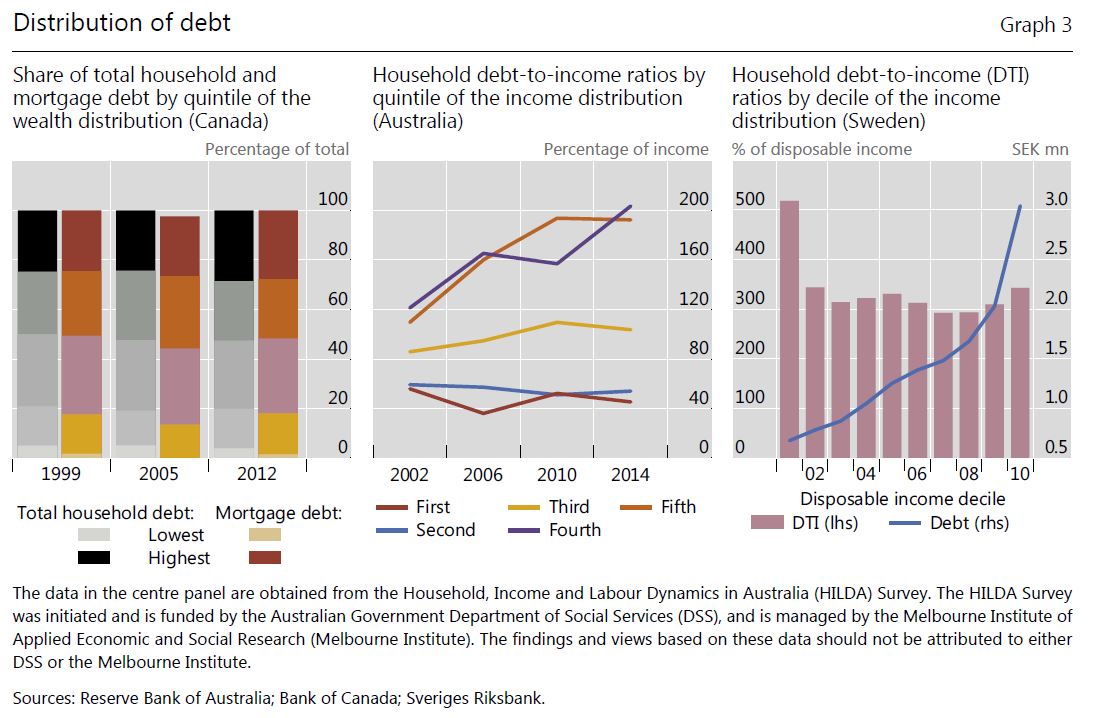

constraints, an economy’s vulnerability to amplification can be assessed by looking at the distribution of debt by income and wealth. In Australia, households in the top income brackets tend to have substantially higher debt ratios than those at the bottom of the distribution (eg in 2014, the top two quintiles had debt ratios of about 200%, while the bottom two had ratios of about 50%. [Note this is based on OLD 2014 HILDA data, and debt to higher income households has risen further since then!]

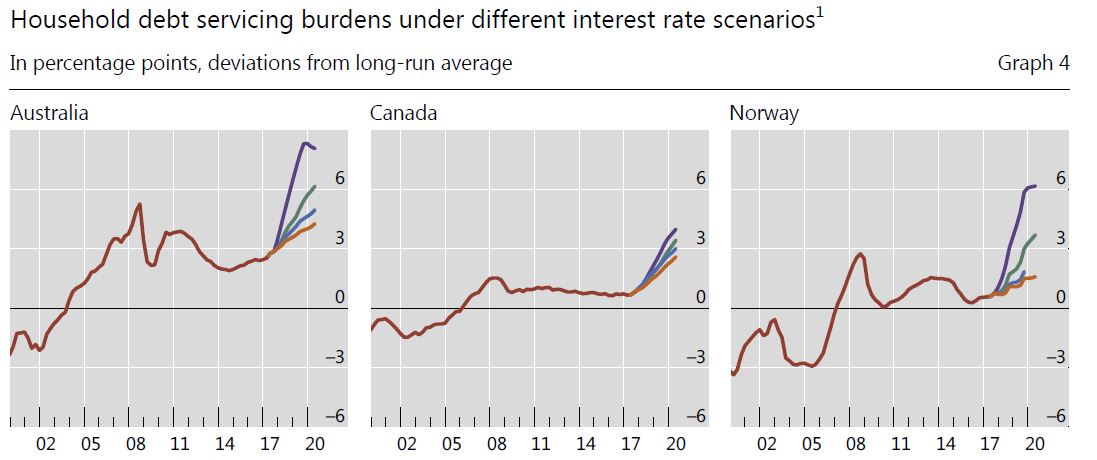

In countries where household debt has risen rapidly since the crisis, and where the majority of mortgages are adjustable rate, DSRs are already above their historical average, and would be pushed yet further away by higher interest rates.

In countries where household debt has risen rapidly since the crisis, and where the majority of mortgages are adjustable rate, DSRs are already above their historical average, and would be pushed yet further away by higher interest rates.

From an aggregate supply perspective, an economy’s ability to adjust via labour reallocation across different regions can weaken if household leverage grows over time. In such an economy, a fall in house prices – as may be associated with interest rate hikes – would saddle a number of households with mortgages worth less than the underlying property. A share of these “underwater” homeowners might also lose their jobs in the ensuing contraction. In turn, their unwillingness to realise losses by selling their property at depressed prices may prolong their spell of unemployment by preventing them from taking jobs in locations that would require a house move.

Elevated levels of household debt could pose a threat to financial stability, defined here as distress among financial institutions. These exposures relate not only to direct and indirect credit risks, but also to funding risks. There is some evidence that this may be occurring in Australia, where high-DSR households are more likely to miss mortgage payments.

Elevated levels of household debt could pose a threat to financial stability, defined here as distress among financial institutions. These exposures relate not only to direct and indirect credit risks, but also to funding risks. There is some evidence that this may be occurring in Australia, where high-DSR households are more likely to miss mortgage payments.

The indirect exposure to household debt arises from any increase in credit risk linked to households’ expenditure cuts. These are bound to have a broader impact on output and hence on credit risk more generally. Deleveraging by highly indebted households could induce a recession so that banks’ non-household loan assets are likely to suffer. Financial stability may also be threatened by funding risks . The network of counterparty relationships could become a channel for the transmission of stress, as any decline in the value of one bank’s cover pool could rapidly affect that of all the others.

They conclude:

Central banks and other authorities need to monitor developments in household debt. Several features of household indebtedness help to shape the behaviour of aggregate expenditure, especially after economic shocks. The level of debt and its duration – as well as whether debt has financed the acquisition of illiquid assets such as housing – all play a role in determining how far an individual household will cut back its consumption. Aggregating up, the distribution of debt across households can amplify these adjustments. In turn, such amplification is more likely if debt is concentrated among households with limited access to credit or less scope for selfinsurance. Since these households are also likely to be poorer households, keeping track of the distribution of debt by income and wealth can help indicate an economy’s vulnerability to amplification.

One thought on “BIS Special Feature On Household Debt”