In a keynote address by ASIC Chair, James Shipton at Committee for Economic Development of Australia (CEDA) event in Melbourne yesterday, it appears the regulator will hold public hearings about responsible lending practices.

He said that ASIC was updating its responsible lending guidance, and as part of its consultation, public hearings would be held to “robustly test some of the issues and views that have been raised in submissions”.

This is a follow-up to ASIC’s consultation paper on updating its guidance on responsible lending, which was issued in mid-February 2019.

Interestingly, ASIC has discretion as to whether such hearings would take place privately or publicly. However the regulator is required to have regard to whether it is in the public interest for a hearing to take place in public.

In addition, ASIC also has power to summon witnesses and require the production of documents for the purposes of a public hearing. It may also refer to a court any questions of law arising at a hearing.

To date ASIC has hardly used it hearings powers but is does appear they intend to utilise these as an aspect of its renewed approach to enforcement in the wake of the Hayne Royal Commission.

We are embedding and expanding new supervisory approaches and promoting best practice and innovation in regulation – particularly through our Close & Continuous Monitoring program (or CCM) and our corporate governance review that is aimed at improving governance practices at the board level.

We are also implementing new and existing reforms and working towards our new obligations and responsibilities in response to the Royal Commission. This includes an expanded role for ASIC to become the primary conduct regulator in superannuation.

The Australian Information Commissioner (Commissioner) has accepted an Enforceable Undertaking (EU) offered by Commonwealth Bank of Australia (CBA).

The EU underpins

execution of further enhancements to the management and retention of

customer personal information within CBA and certain of its

subsidiaries.

The EU follows CBA’s ongoing work to address two incidents; one

relating to the disposal of magnetic data tapes containing historical

customer statements; and the other relating to internal user access to

certain systems and applications containing customer personal

information. CBA reported both incidents to the Office of the Australian

Information Commissioner (OAIC) in 2016 and 2018 respectively and has

since been working to address these incidents.

As previously announced, CBA has found no evidence to date, as a

result of these incidents, that our customers’ personal information was

compromised, or that there have been any instances of unauthorised

access by CBA employees or third parties.

CBA’s commitments in the EU announced today include reviewing and implementing further enhancements to:

internal privacy policies, procedures and record retention standards;

internal user access controls on systems and applications that hold personal information; and

the privacy risk management and monitoring processes that apply to service providers to CBA and certain subsidiaries.

The EU provides CBA with 90 days to develop and submit to the OAIC a

work plan, and timetable of work that CBA will complete to meet its

obligations under the EU.

Commonwealth Bank Group Chief Risk Officer, Nigel Williams, said: “We

have offered this EU as a demonstration of our continued commitment to

appropriately managing the privacy of customer personal information, and

addressing any concerns identified by the Commissioner.

“We continue to take action to address issues, earn trust and be a

better bank for our customers. This includes proactively engaging with

our regulators to ensure we continue to build better systems, processes

and controls to manage the personal information of our customers.”

Slater and Gordon has today filed a class action against AMP on behalf of over two million Australians, via InverstorDaily.

The

class action is the second to be filed by Slater and Gordon as part of

its Get Your Super Back campaign that kicked off following the Royal

Commission.

The first class action launched by Slater and Gordon as part of their Get Your Super Back campaign was against Colonial First State.

The

case alleges that through arrangements with related parties, trustees

AMP Super and NM Super paid too much to related AMP entities for

administration services.

The case also alleges that they failed to secure an appropriate return on cash-only investment options.

Senior

Associate Nathan Rapoport at Slater and Gordon said super members

trusted that AMP would act in their best interests but instead were

charged exorbitant fees.

“Both AMP Super and NM Super, as

trustees of the funds, should have taken steps to secure the best deal

for members on a commercial arms-length basis,” said Mr Rapoport.

Mr

Rapoport said that the Royal Commission head evidence of a group of AMP

cash option members who received negative returns due to un-competitive

interest rates and excessive fees and not even the trustee was aware of

it.

“These customers would have been better off keeping their retirement savings under their bed,” Mr Rapoport said.

An AMP spokesperson said that the group acknowledged the class action proceeds and would vigorously defend the proceedings.

“The

action relates to fees charged to members, and the low interest rate

received and fees charged on cash-only fund options. The proceedings

will be vigorously defended.

“AMP and the trustees of its

superannuation funds are firmly committed to acting in the best

interests of their superannuation members and acting in accordance with

legal and regulatory obligations. We encourage any customers who have

concerns to contact AMP directly or their financial adviser,” an AMP

spokesperson said.

This is the latest class action to hit AMP after Maurice Blackburn Lawyers also

filed a class action against AMP seeking compensation for shareholders

alleging it breached the Corporations Act for failed to disclose its

practice of charging fees for no service and for its interactions with

ASIC.

Slater and Gordon were one of the five law firms to compete for the shareholder class action but Maurice Blackburn eventually won the right to continue on the case due to its funding model.

A professional indemnity (PI) specialist has expressed grave concern over new requirements for brokers to confirm that there are no signs of financial abuse when they assist clients in securing a loan; via Australian Broker.

The action has been taken by the banks in response to the Australian

Banking Association’s updated code of practice requiring a higher

standard for dealing with vulnerable customers. However, Darren Loades,

the FBAA’s dedicated PI insurance specialist for Queensland and the

Northern Territory, has questioned the sudden announcement, the lack of

clarity as to what the agreement entails, and the days-long timeframe

before the 1 July implementation.

“Do you think that’s by accident? I sure don’t,” said Loades.

“The main point is that it’s been rushed through, no one has actually

seen the details, and it could have very far-reaching and onerous

implications for brokers. Do not sign anything for the moment.”

Loades highlighted the serious liability concerns of signing an

agreement that could likely take brokers out of their current coverage

and leave them “entirely exposed.”

“Professional indemnity policies only respond to claims made under

common law. Signing one of these declarations could incur contractual

liabilities, over and above the liabilities a broker would owe at common

law,” he explained.

“The standard PI policy out there on the market will not pick up any

liabilities owed under contract. Brokers could potentially be left

exposed and not insured at all.”

Last week, FBAA managing director Peter White expressed concern that

“PI insurance could increase tenfold to cover a declaration like this.”

“To try and ram this through with little notice is not only

ridiculous and ill-conceived, but creates massive risks for brokers with

almost no benefit to borrowers,” he added.

As White expressed last week, Loades finds it suspect that the

agreements the banks are asking brokers to sign have yet to be made

accessible.

He continued, “But knowing the banking industry, the documents are

going to be pretty far-reaching with some nasty little clauses in there

along the lines of, ‘If you drop the ball in this area, you agree to

indemnify the bank against any losses.’ Otherwise, why would they be

going to this trouble?

“This seems to be a push from the banks to transfer their liability onto the broker, which isn’t all that fair or realistic.”

While Loades does acknowledge that brokers are the ones to have

face-to-face interaction with the borrower, he has serious doubts that a

set of written guidelines provided by the bank could translate to

brokers being able to identify signs of abuse in real life stations.

“That’s a whole different ballgame. Brokers aren’t qualified or

licenced to provide advice in this area of financial abuse,” he said.

“What happens if the broker happens to innocently miss a situation

where there is financial abuse? The bank is going to rely on this

document to say, ‘Well, you signed off. You’re the one who is liable.’”

The New Zealand Reserve Bank is requesting two reports from ANZ New Zealand to provide assurance it is operating in a prudent manner.

They say, that section 95 of the Reserve Bank of New Zealand Act 1989 gives the Reserve Bank the power to require a bank to provide a report by a Reserve Bank-approved, independent person. These reviews can investigate such issues as risk management, corporate or financial matters, and operational systems.

The first report will cover ANZ New Zealand’s

compliance with the Reserve Bank’s current and historic capital adequacy

requirements.

The second report will assess the

effectiveness of ANZ New Zealand’s Director’s Attestation and Assurance

framework, focussing on internal governance, risk management and internal

controls.

Reserve Bank Governor Adrian Orr said ANZ

remains sound and well capitalised.

“We continue to engage constructively with

ANZ New Zealand’s board, and they remain focussed on these important issues.

These formal reviews will allow us to work with the bank to ensure the public,

and we as regulator, can have continued confidence in the bank and that it is

operating in a prudent manner.”

“Section 95 reports are part of our

supervisory toolkit and provide independent assurance and insight about banks’

systems and practices. We have used them effectively in the past, and we will

continue to do so.”

The latest from the UK suggests inflation will fall below the 2% lower bounds as downside risks to growth build and the Brexit issue still haunts the halls. The Bank held the current rate, and will continue its market operations to stimulate the economy.

The Bank of England’s Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. At its meeting ending on 19 June 2019, the MPC voted unanimously to maintain Bank Rate at 0.75%.

The Committee voted unanimously to maintain the stock of sterling

non-financial investment-grade corporate bond purchases, financed by the

issuance of central bank reserves, at £10 billion. The Committee also

voted unanimously to maintain the stock of UK government bond purchases,

financed by the issuance of central bank reserves, at £435 billion.

The MPC’s most recent economic projections, set out in the May Inflation Report,

assumed a smooth adjustment to the average of a range of possible

outcomes for the United Kingdom’s eventual trading relationship with the

European Union and were conditioned on a path for Bank Rate that rose

to around 1% by the end of the forecast period. In those projections,

GDP growth was a little below potential during 2019 as a whole,

reflecting subdued global growth and ongoing Brexit uncertainties.

Growth then picked up above the subdued pace of potential supply growth,

such that excess demand rose above 1% of potential output by the end of

the forecast period. As excess demand emerged, domestic inflationary

pressures firmed, such that CPI inflation picked up to above the 2%

target in two years’ time and was still rising at the end of the

three-year forecast period.

Since the Committee’s previous meeting, the near-term data have been

broadly in line with the May Report, but downside risks to growth have

increased. Globally, trade tensions have intensified. Domestically, the

perceived likelihood of a no-deal Brexit has risen. Trade concerns have

contributed to volatility in global equity prices and corporate bond

spreads, as well as falls in industrial metals prices. Forward interest

rates in major economies have fallen materially further. Increased

Brexit uncertainties have put additional downward pressure on UK forward

interest rates and led to a decline in the sterling exchange rate.

As expected, recent UK data have been volatile, in large part due to

Brexit-related effects on financial markets and businesses. After

growing by 0.5% in 2019 Q1, GDP is now expected to be flat in Q2. That

in part reflects an unwind of the positive contribution to GDP in the

first quarter from companies in the United Kingdom and the European

Union building stocks significantly ahead of recent Brexit deadlines.

Looking through recent volatility, underlying growth in the United

Kingdom appears to have weakened slightly in the first half of the year

relative to 2018 to a rate a little below its potential. The underlying

pattern of relatively strong household consumption growth but weak

business investment has persisted.

CPI inflation was 2.0% in May. It is likely to fall below the 2%

target later this year, reflecting recent falls in energy prices. Core

CPI inflation was 1.7% in May, and core services CPI inflation has

remained slightly below levels consistent with meeting the inflation

target in the medium term. The labour market remains tight, with recent

data on employment, unemployment and regular pay in line with

expectations at the time of the May Report. Growth in unit wage costs

has remained at target-consistent levels.

The Committee continues to judge that, were the economy to develop

broadly in line with its May Inflation Report projections that included

an assumption of a smooth Brexit, an ongoing tightening of monetary

policy over the forecast period, at a gradual pace and to a limited

extent, would be appropriate to return inflation sustainably to the 2%

target at a conventional horizon. The MPC judges at this meeting that

the existing stance of monetary policy is appropriate.

The economic outlook will continue to depend significantly on the

nature and timing of EU withdrawal, in particular: the new trading

arrangements between the European Union and the United Kingdom; whether

the transition to them is abrupt or smooth; and how households,

businesses and financial markets respond. The appropriate path of

monetary policy will depend on the balance of these effects on demand,

supply and the exchange rate. The monetary policy response to Brexit,

whatever form it takes, will not be automatic and could be in either

direction. The Committee will always act to achieve the 2% inflation

target.

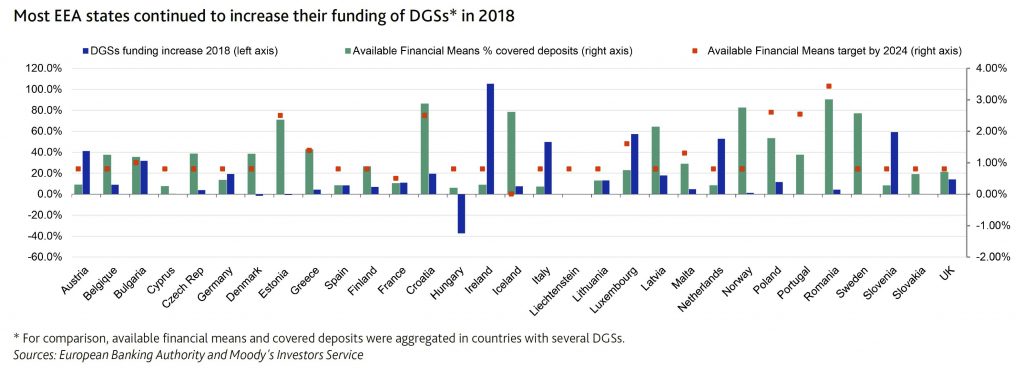

On 17 June, the European Banking Authority (EBA), published 2018 data on national Deposit Guarantee Schemes (DGSs) across the European Economic Area (EEA), which show that 32 of 43 DGSs increased their funds available to cover deposits in 2018 by levying banks.

Here of course the $250k deposit scheme is unfunded and currently inactive.

Moody’s says that the target of 0.8% of covered deposits by 2024 set out in the Deposit Guarantee Schemes Directive (DGSD) has already been achieved in 17 of the 43 DGSs in the EEA. The gradually increasing harmonisation of DGSs in Europe is credit positive for European banks because it improves European banking systems’ financial stability by better protecting depositors against the consequences of credit institution insolvency. As DGS funding increases and exceeds the 0.8% threshold, they also expect banks’ levies to moderate, which will benefit their profitability.

Since the 2009 financial crisis, European authorities developed policies and tools to buttress financial systems’ resiliency and help authorities prevent and, if needed, tackle bank distress without having to resort to taxpayers’ support. DGSs form one of these tools.

Under current EU legislation, depositors are protected by their national DGS up to €100,000 (or the equivalent in local currency). This protection applies regardless of whether ex ante funding has been accrued by DGS. Under the DGSD, all EEA banks are required to contribute to national DGSs so that at least 0.8% of covered deposits are funded by 2024 (and by exception, no less than 0.5% of the covered deposits, like in France2).

Nine member states have set up DGSs with higher funding targets such as Romania (3.43%) and Poland (2.6%). Some countries, such as Iceland, have not yet defined their national funding target, while others have defined numerous DGSs for different categories of banks and depositors, as in Germany for private, public, savings or cooperative banks, hence there are more DGS than there are EU countries.

As of year-end 2018, 16 countries had already reached the DGSD’s 0.8% minimum funding ratio for 2024, and 10 countries exceeded their national target. The levies banks paid increased by around 12% in 2018, while covered deposits grew only by 3.6%. As of year-end 2018, EEA member states had reached in aggregate a funding ratio of 0.65% of covered deposits, up from 0.6% in 2017.

Out of the 31 banking systems addressed in the EBA report, 25 increased the funding for the DGSs in 2018, with very large increases in Ireland (+105.2%), Slovenia (+59.2%) or Luxembourg (+57.3%). The diversity in funding efforts reflects different starting points since some countries did not have DGS or limited ex-ante funding when the DGSD was adopted. For instance Luxembourg had no funding in 2015 and a target of 1.6% of covered deposits.

Despite progress, the third pillar of the banking union – the European deposit insurance scheme (EDIS) proposal adopted in 2015 – is not yet in sight due to a lack of political consensus. The EDIS proposal builds on the system of national DGSs and would provide a stronger and more uniform degree of insurance cover in the euro area. This framework would reduce the vulnerability of national DGSs to large local shocks.

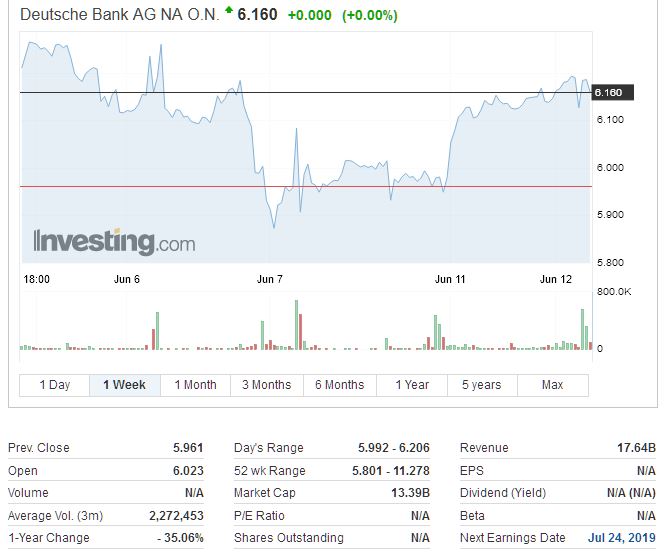

A New York Times report suggests that Deutsche Bank, the embattled banking titan faces an investigation by Federal Authorities.

The investigation includes a review of Deutsche Bank’s handling of so-called suspicious activity reports that its employees prepared about possibly problematic transactions, including some linked to President Trump’s son-in-law and senior adviser, Jared Kushner, according to people close to the bank and others familiar with the matter.

This is part of a criminal investigation into wider examinations into how illicit funds flow through the American financial system.

Deutsche Banks shares were down after the report.

The Justice Department has been investigating Deutsche Bank since 2015, when agents were examining its role in laundering billions of dollars for wealthy Russians through a scheme known as mirror trading. Customers would use the bank to convert Russian rubles into dollars and euros via a complicated series of stock trades in Europe and the United States.

Westpac says a former HSBC wealth management boss will lead its new Business division, the result of the bank’s restructure and merging of the wealth businesses.

Guilherme

(Guil) Lima has come to the role of business chief executive from HSBC

in Hong Kong, where he was group head of wealth management.

Prior to his last role, he also led the retail and wealth management businesses of HSBC for the Latin American region.

In March, Westpac restructured its business following the royal commission in an effort to simplify the company, merging its private wealth, platforms & investments and superannuation businesses into the new Business segment.

The bank revealed in its half year results that its wealth remediation and restructure was costing it $620 million.

Mr

Lima has 22 years’ experience in banking and consulting in Asia,

Europe, Latin America and the US and is a former McKinsey and Co

partner.

At McKinsey and Co’s financial services

practice, Mr Lima led a number of engagements across a variety of

commercial and retail banking businesses.

“His

background in leading strategic change on a global basis, as well as his

domain expertise in banking and wealth, will be particularly valuable

as we seek to grow the breadth of our customer relationships across the

new Business division,” Brian Hartzer, group chief executive, Westpac

said.

“I’d also like to thank Alastair Welsh,

general manager, commercial banking, for his contribution as acting

chief executive, business. Al is doing a great job managing the

transition and ensuring the division continues to run smoothly.”

Subject to regulatory and visa approvals, Mr Lima will commence in the role later in the year.

The RBA released their minutes today which clearly signals further rate cuts ahead as they drive toward to goal of 4.5% unemployment – the latest magic figure when wages will start to rise. Savers be dammed, to try and get household spending up.

International Economic Conditions

Members commenced their discussion by noting that the data on the global economy released since the

previous meeting had been mixed. GDP growth outcomes for the March quarter in some economies had been

slightly stronger than the second half of 2018, while labour markets had remained tight. However, global

trade and conditions in the global manufacturing sector had remained weak. New export orders had been

little changed at subdued levels and growth in industrial production had slowed in many economies,

including those economies in east Asia that are closely integrated with global supply chains.

The US–China trade dispute had escalated in May, intensifying the downside risk posed to the

global economic outlook from this source. The United States had proceeded to increase tariffs from

10 per cent to 25 per cent on US$200 billion of imports from China, and China had

responded by announcing that tariffs would increase by 5–25 per cent on

US$60 billion of US imports from 1 June 2019. In the days leading up to the meeting, the

US administration had also announced tariff measures affecting Mexico and India.

In the major advanced economies, GDP growth for the March quarter had been somewhat stronger than in

the second half of 2018. However, in both Japan and the United States the contribution from domestic

demand had declined, and investment intentions in Japan pointed to only moderate investment growth over

the period to early 2020. Nevertheless, labour markets in the advanced economies had remained tight. As

a result, wages growth had continued to increase, reaching around the highest rates recorded during the

current expansion in the three major advanced economies. Moreover, firms’ employment intentions

had remained positive at high levels and firms had continued to report widespread difficulties in

filling jobs.

Inflation had remained subdued globally despite tight labour markets and rising wages growth in many

advanced economies. Core inflation had been below target in the three major advanced economies,

following the decline in core inflation in the United States in recent months. Members noted that

temporary factors had been contributing to the decline in the US core inflation measure, with the

trimmed mean underlying inflation measure close to 2 per cent over recent months.

In China, indicators of activity had moderated in April. The moderation had partly reversed the

unusually strong results in March, which had included activity brought forward ahead of tax changes that

came into effect on 1 April 2019. Growth in fixed asset investment had slowed in April, driven by a

sharp fall in manufacturing investment, while infrastructure investment had been supported by increased

government spending. Industrial production had slowed across a wide range of products in April, although

production of construction-related materials – such as steel, plate glass and cement – had

remained strong.

Elsewhere in east Asia, growth had slowed further in the March quarter, mainly because of weaker growth

in exports and investment. Growth in India had been at the lower end of the range of recent experience,

with members noting that the recent tariff announcements by the US administration could adversely affect

Indian exports of goods.

Commodity price movements had been mixed since the previous meeting. Iron ore and rural prices had

increased. The increase in iron ore prices had been underpinned by supply constraints, strong demand

from China and an increase in steel production. On the other hand, the prices of coal, oil and base

metals had declined. Members noted that the decline in oil prices had mainly reflected renewed concerns

around the outlook for global oil demand.

Domestic Economic Conditions

Members noted that national accounts data for GDP growth in the March quarter would be released the day

after the meeting. GDP growth was expected to have been a little firmer than in the preceding two

quarters, supported by growth in exports, non-mining business investment and public spending. Growth in

consumption, however, was expected to continue to be sluggish and dwelling investment was expected to

have declined further in the March quarter.

Information received for the June quarter and indicators of future economic activity had been mixed.

Business conditions and consumer sentiment had been broadly stable at or slightly above average levels.

Information from the ABS capital expenditure survey and the Bank’s business liaison contacts

suggested that mining investment was close to its trough, while the available information pointed to

ongoing modest growth in non-residential building investment. Members noted that the low- and

middle-income tax offset, including the increase announced in the Australian Government Budget for

2019/20, would boost household disposable income and could support household

consumption in the second half of 2019.

Members also discussed the distributional implications of low interest rates on household incomes. Lower interest rates lead to a decline in the interest that households pay on their debt, but also lead to a decline in the interest income that households receive from interest-bearing assets, such as term deposits. As such, changes in interest rates have different effects on different groups of households. In particular, members recognised that many older Australians rely on interest income, which would decline with lower interest rates. The overall net effect of lower interest rates was nevertheless expected to boost aggregate household disposable income and thus spending capacity.

Conditions in established housing markets had remained weak. Housing prices had continued to decline in

Sydney and Melbourne during May, although the pace of decline had eased from earlier in the year.

Housing prices had continued to decline markedly in Perth. Members noted that the housing market was

likely to be affected by the removal of uncertainty around possible changes to taxation arrangements

relating to housing. They also considered the effects of the Australian Prudential Regulation

Authority’s (APRA’s) proposal to amend its requirement for banks to determine the

borrowing capacity of loan applicants using a specified minimum interest rate. While it remained too

early to determine the overall effects, auction clearance rates had increased noticeably in Sydney the

weekend following these developments. Building approvals had declined further in April, however, to be

more than 20 per cent lower over the preceding 12 months. This suggested that, even if

there were a marked turnaround in housing sentiment, given the lags involved it would take some time for

this to translate into higher residential construction activity.

Several key domestic data series relating to the labour market had been released over the previous

month. The wage price index had increased by 0.5 per cent in the March quarter to be

2.3 per cent higher over the year. While wages growth had been higher than a year earlier in

most industries and states, the low rate of wages growth provided further evidence of spare capacity in

the labour market. Wages growth in the private sector had been unchanged in the March quarter, and had

increased to 2.4 per cent over the year (2.7 per cent including bonuses). The Fair

Work Commission had recently granted a 3.0 per cent increase in the national minimum and award

classification wages, which would take effect from 1 July 2019. Members noted that this decision

directly affected the wages of around one-fifth of workers in Australia. Public sector wages growth had

been little changed in recent years because of caps on salary increases for public sector employees.

Members also noted that an increasing proportion of business liaison contacts were expecting wages

growth to be stable in the year ahead, although the proportion of contacts expecting wages growth to

decline had continued to fall.

The data on conditions in the labour market in April had been mixed. The unemployment rate had

increased to 5.2 per cent in April from (an upwardly revised) 5.1 per cent in March.

This followed a six-month period during which the unemployment rate had remained at around

5 per cent. The increase in the unemployment rate had been accompanied by an increase in the

participation rate to its highest level on record. The underemployment rate had also increased in April.

While the unemployment rate in both New South Wales and Victoria remained historically low, in both

states it had increased since the beginning of 2019. Employment growth nationwide had moderated in 2019,

but had remained above growth in the working-age population. Employment growth had been robust in most

states in preceding months; the exceptions were Western Australia and Tasmania, where the level of

employment had been roughly unchanged since mid 2018.

Forward-looking indicators of labour demand pointed to a moderation in employment growth in the near

term, to around the rate of growth in the working-age population. Measures of job advertisements had

declined over recent months. Employment intentions reported by the Bank’s business liaison

contacts had been lower than in mid 2018, but these intentions were still generally positive.

Members had a detailed discussion of spare capacity in the labour market. Although difficult to measure

directly, the extent of spare capacity in the labour market is an important factor that affects wages

growth and price inflation. On a number of measures, it was apparent that the labour market still had

significant spare capacity. The main approach to measuring spare capacity is to compare the current

unemployment rate with an estimate of the unemployment rate associated with full employment, which is

the rate of unemployment consistent with stable inflation. The Bank’s estimate of this

unemployment rate had declined gradually over recent years, to be around 4½ per cent

currently.

Members noted the significant uncertainty around modelled estimates of the unemployment rate consistent

with full employment. They also discussed other measures of spare capacity, including underemployment of

part-time workers, recognising that the supply side of the labour market had been quite flexible. Strong

employment growth over recent years had encouraged more people to join the labour force, allowing the

economy to absorb increased activity without generating inflationary pressure. Notwithstanding the

uncertainties involved, members revised their assessment of labour market capacity, acknowledging the

accumulation of evidence that there was now more capacity for the labour market to absorb additional

labour demand before inflation concerns would emerge.

Financial Markets

Members commenced their discussion of financial market developments by noting that escalating trade

disputes had led to a rise in volatility in global financial markets over preceding weeks, most notably

in equity markets. Nevertheless, with central banks expected to maintain expansionary policy settings

and risk premiums generally low, global financial conditions remained accommodative.

The escalation in the trade dispute between the United States and China had resulted in declines in

global equity markets. The fall in equity prices had been particularly sharp in China, but substantial

declines had also been seen in the United States as well as in a range of other advanced economies.

Members observed that the declines in equity prices had been largest for sectors more directly exposed

to the announced and prospective tariff changes and/or deriving a larger share of revenue from

international trade.

By contrast, Australian equity prices were little changed at close to their highest level in a decade.

Members noted that a sharp increase in Australian banks’ share prices, following the federal

election, had partly offset a recent decline in resource stocks in the context of escalating trade

tensions.

Members noted that there had been only a modest tightening in financial conditions in emerging markets,

including in Mexico, where trade tensions with the United States had recently resurfaced. Equity prices

had declined and sovereign credit spreads had widened somewhat, and there had been modest outflows from

bond and equity funds in emerging markets. Currencies of emerging market economies had also generally

depreciated a little, although there had mostly been little change in yields on government bonds

denominated in local currencies.

In the advanced economies, there had been some widening in yield spreads between corporate and

sovereign debt, particularly for corporations rated below investment grade. Members observed that

financing costs for corporations remained low nonetheless, with government bond yields having declined

further over the preceding month, in some cases to historic lows. This had partly reflected a shift down

in market participants’ expectations of future policy interest rates in several advanced

economies, including Australia, in an environment of ongoing trade tensions and subdued inflation. In

the cases of the United States, Canada and New Zealand, members noted that market pricing implied a

lowering of policy rates in the period ahead, although central banks in these economies had not

indicated that a near-term change in policy rates was in prospect.

Volatility in foreign exchange markets had generally remained low, although the Japanese yen had

appreciated over recent weeks, as tends to be the case in periods of increased uncertainty. There had

been a moderate depreciation of the Chinese renminbi over the preceding month.

Members noted that the Australian dollar had depreciated a little over preceding months, remaining

around the lower end of its narrow range of the preceding few years. Members also noted that while the

strength in commodity prices had supported the exchange rate, the decline in Australian government bond

yields relative to those in the major markets over 2019 had worked in the opposite direction. Long-term

government bond yields in Australia remained noticeably below those in the United States, although this

gap had narrowed a little recently as market participants’ expectations for the future path of

the US federal funds rate were revised sharply lower.

Housing credit growth had stabilised in recent months, having slowed substantially over the preceding

year. Growth in housing lending to owner-occupiers was running at around 4½ per cent in

six-month-ended annualised terms, while the rate of growth in housing lending to investors had been

close to zero since early 2019. Although standard variable reference rates for housing loans had

increased since mid 2018, the average rate paid on outstanding loans had been little changed since

then, as banks had continued to compete for new borrowers by offering materially lower rates on new

loans. Borrowers shifting from interest-only to principal-and-interest loans had also put downward

pressure on average outstanding mortgage rates.

Members were briefed on the changes proposed by APRA to its requirement that banks determine the

borrowing capacity of loan applicants using a specified minimum interest rate. Members observed that the

proposed changes would be likely to result in a modest increase in borrowing capacity for those with

lower interest rate loans, typically owner-occupiers and borrowers with principal-and-interest loans.

However, some borrowers facing higher-than-average interest rates would not see an increase in their

borrowing capacity. Members observed that such a change to serviceability assessments would mean that

any reduction in actual interest rates paid would increase households’ borrowing capacity a

little. This would be in addition to the positive effect on the cash flow of the household sector

overall.

The pace of growth in business lending had slowed in recent months, with lending to large businesses

continuing to be the sole source of growth. Lending to small businesses had declined over the preceding

year. Members noted that the stricter verification of income and expenses required for consumer lending

was also being applied to many small businesses.

Members noted that financing conditions for both financial and non-financial corporations were highly

favourable, with Australian bond yields at historic lows. Yields on residential mortgage-backed

securities were also at low levels, having declined in line with the one-month bank bill swap rate

(BBSW), which is the reference rate for these securities. Members observed that the increase in BBSW and

other short-term money market rates in 2018 had been fully unwound. As a result, the major banks’

debt funding costs were now at a historic low. The major banks’ retail deposit rates were also

historically low, with deposit rates having continued to edge lower. The average interest rate paid on

retail deposits by banks was slightly below the cash rate, although only a small share of deposits by

value received a rate below 0.5 per cent (predominantly deposits on transaction

accounts).

Financial market pricing implied that the cash rate target was expected to be lowered by 25 basis

points at the present meeting, with a further 25 basis point reduction expected later in the

year.

Considerations for Monetary Policy

In considering the stance of monetary policy, members observed that the outlook for the global economy

remained reasonable, although the risks from the international trade disputes had increased. Members

noted that the associated uncertainty had been affecting investment intentions in a number of economies

and that international trade remained weak. At the same time, the Chinese authorities had continued to

provide targeted stimulus to support economic growth, and global financial conditions remained very

accommodative. In most advanced economies, labour markets had remained tight and wages growth had picked

up, while inflation had remained subdued.

Members observed that the outlook for the Australian economy also remained reasonable, with the

sustained low level of interest rates continuing to support economic activity. A pick-up in growth in

household disposable income, continued investment in infrastructure and a renewed expansion in the

resources sector were expected to contribute to growth in output over coming years. The unemployment

rate was expected to decline a little towards the end of the forecast period, and underlying inflation

was expected to pick up gradually, to be at the lower end of the target range in the next couple of

years. Members noted that this outlook was based on the usual technical assumption that the cash rate

followed the path implied by market pricing, which suggested interest rates would be lower in the period

ahead.

The most recent data on labour market conditions had shown that, despite ongoing strong growth in

employment, the unemployment rate had not declined any further in the preceding six months and had edged

up in the most recent two months. Reasonably strong demand for labour had been met partly by a rise in

labour force participation. Members observed that this increased flexibility on the supply side of the

labour market, together with ongoing subdued growth in wages and inflation, suggested that spare

capacity was likely to remain in the labour market for some time. While wages growth had picked up from

a year earlier, it had remained subdued and recent data suggested the pick-up was only very gradual.

Together, these data suggested that the Australian economy could sustain a lower rate of unemployment

than previously estimated, while achieving inflation consistent with the target.

Members observed that underlying inflation had been below the 2–3 per cent target

range for three years and that the lower-than-expected March quarter inflation data – at

1½ per cent in underlying terms – had pointed to ongoing subdued inflationary

pressures. In part, this reflected continued slow growth in wages. Members also observed that

competition in retailing, very weak growth in rents in the context of the housing market adjustment and

government initiatives to reduce cost-of-living pressures had been dampening inflation pressures. These

factors were likely to continue for some time. Members recognised that Australia’s flexible

inflation targeting framework did not require inflation to be within the target range at all times,

which allows the Board to set monetary policy so as best to achieve the Bank’s broad objectives.

However, they also agreed that the inflation target plays an important role as a strong medium-term

anchor for inflation expectations, to help deliver low and stable inflation, which in turn supports

sustainable growth in employment and incomes.

In these circumstances, members agreed that further improvement in the labour market would be required

for wages growth and inflation to rise to levels consistent with the medium-term inflation target.

Moreover, while the Bank’s central forecast scenario for growth and inflation was unchanged, the

accumulation of data on inflation and labour market conditions over recent months had led members to

revise their assessment of the extent of inflationary pressure in the economy and, relatedly, the extent

of spare capacity in the Australian labour market.

Given these considerations, members considered the case for a reduction in the cash rate at the current

meeting. A lower level of interest rates would support growth in the economy, thereby reducing

unemployment and contributing to inflation rising to a level consistent with the target.

Members recognised that, in the current environment, the main channels through which lower interest

rates would support the economy were a lower value of the exchange rate, reduced borrowing rates for

businesses, and lower required interest payments on borrowing by households, freeing up cash for other

expenditure. Although households are net borrowers in aggregate, members recognised that there are many

individual households that are net savers and whose interest income would be reduced by lower interest

rates. Carefully considering these different effects, members judged that a lower level of interest

rates was likely to support growth in employment and incomes, and promote stronger overall economic

conditions.

Members also considered the risks associated with a lower level of interest rates in the period ahead.

Given the high level of household debt, the adjustment under way in housing markets and the tightening

in lending practices, members judged that a decline in interest rates was unlikely to encourage a

material pick-up in borrowing by households that would add to medium-term risks in the economy. Members

continued to recognise that there were risks to the forecasts for growth and inflation in both

directions. However, given the extent of spare capacity in the economy and the subdued inflationary

pressures, they judged there was a low likelihood of a decline in interest rates resulting in an

unexpectedly strong pick-up in inflation. Members also observed that a lower level of interest rates

would stimulate activity and thereby improve the resilience of the Australian economy to any future

adverse shocks.

Taking into account all the available information, the Board decided that it was appropriate to lower the cash rate by 25 basis points at this meeting. A lower level of the cash rate would assist in reducing spare capacity in the labour market, providing more Australians with jobs and greater confidence that inflation will return to be comfortably within the medium-term target range in the period ahead. Given the amount of spare capacity in the labour market and the economy more broadly, members agreed that it was more likely than not that a further easing in monetary policy would be appropriate in the period ahead. They also recognised, however, that lower interest rates were not the only policy option available to assist in lowering the rate of unemployment, consistent with the medium-term inflation target. Members agreed that, in assessing whether further monetary easing was appropriate, developments in the labour market would be particularly important.

The Decision

The Board decided to lower the cash rate by 25 basis points to 1.25 per cent, effective 5 June.