A somewhat obscure fact about the marching orders for Australia’s Reserve Bank is that, usually, when a government is elected or re-elected or a new governor takes office, the official agreement between the government and the Reserve Bank changes.

There have been seven such agreements so far, each signed by the

federal treasurer and bank governor of the time, and each entitled “Statement on the Conduct of Monetary Policy”.

The first was signed by treasurer Peter Costello and incoming

governor Ian Macfarlane in 1996, the second when Costello reappointed

Macfarlane in 2003, and the third when Costello appointed Glenn Stevens

in 2006.

The fourth was between new treasurer Wayne Swan and Stevens on

Labor’s election in 2007, and the fifth between Swan and Stevens on

Labor’s reelection in 2010.

The sixth was between incoming treasurer Joe Hockey and Stevens on

the Coaition’s election in 2013, and the most recent one between

treasurer Scott Morrison and incoming governor Philip Lowe in 2016.

The Statement on the Conduct of Monetary Policy (the Statement) has

recorded the common understanding of the Governor, as Chair of the

Reserve Bank Board, and the Government on key aspects of Australia’s

monetary and central banking policy framework since 1996.

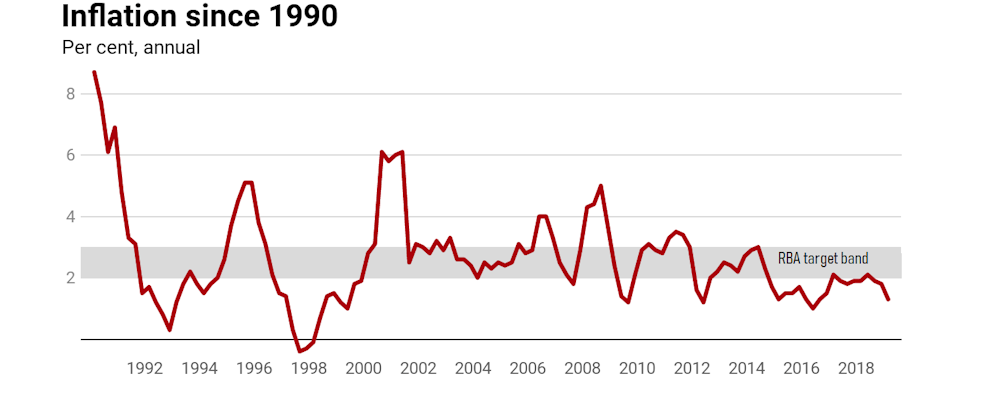

For nearly a quarter of a century, as the statement goes on to note,

there has been a core component of how monetary policy is conducted:

The centrepiece of the Statement is the inflation targeting

framework, which has formed the basis of Australia’s monetary policy

framework since the early 1990s.

But over the years, there have been tweaks. One was this change between the 2013 and 2016 statements.

Effective management of inflation to provide greater certainty and to

guide expectations assists businesses and households in making sound

investment decisions…

The change from “low inflation” to “effective management of

inflation” sounds subtle, but was no accident. It gave the Reserve Bank

extra wiggle room around the inflation target.

And boy, did it come in handy.

The target that’s rarely met

The big question about the agreement is whether the next one (between

Frydenberg and Lowe on the Coalition’s reelection) will tweak the

target again, change it completely, or do something in between.

Because it presumably can’t remain the same.

One reason to think it will change, perhaps significantly, is the

bank’s utter inability to even get particularly close to its target

inflation band of 2-3%, let alone to get within tit, “on average, over time” as required by the agreement.

For years now, inflation has mostly been below the band.

ABS 6401.0

You might not think this matters too much. But it does.

The inflation target is crucial in setting stable expectations for consumers, businesses and markets.

Don’t just take my word for it.

Here is what the previous Reserve Bank governor, Glenn Stevens, said in his last official speech before handing over to Philip Lowe in August 2016:

From 1993 to 2016, a period of 23 years, the average rate of

inflation has been 2.5% – as measured by the CPI, and adjusting for the

introduction of the goods and services tax in 2000. When we began to

articulate the target in the early 1990s and talked about achieving

“2–3%, on average, over the cycle”, this is the sort of thing we meant. I

recall very well how much scepticism we encountered at the time. But

the objective has been delivered.

As I pointed out last month, expectations about price movements depend on Australians believing that the bank will do what it says it will do.

Once people lose faith in the bank’s commitment to or ability to

achieve the target, inflation expectations become unmoored. People react

to what they think what might happen rather than what they are told

will happen. This is what led to Australia’s wage-price spirals in the

1970s and 1980s, and to Japan’s lost decades of deflation.

Three possible outcomes

One possibility is the same statement, word for word. It would be

meant to signal that the bank and the government think things are under

control.

A second possibility is a tweak that further emphasises the “flexible” nature of the target, along the lines Lowe mentioned in his speech at this month’s Reserve Bank board board dinner in Sydney. It would provide more cover for the bank’s inability to hit its target.

A third option would be to add some discussion of the importance of

fiscal policy – government spending and tax policy – as a complement to

the Reserve Bank’s work on monetary policy. Lowe is keen to mention that

he is keen on it, every chance he gets.

But that would put the government under implicit pressure to run

budget deficits at times like those we are in rather than surpluses.

It’s hard to see the Morrison government signing up for that, given its

repeated talk during the election about the importance of being

“responsible”.

Or something more

At the more radical end of the spectrum would be a genuinely new framework for monetary policy.

In the United States, which has also missed its inflation target,

though by not as much as Australia, there has been much discussion of

moving to a “nominal GDP target”. The range mentioned is 5-6% a year.

Advocates of this include former US Treasury secretary Larry Summers, who outlined his rationale in a Brookings Institution report in mid-2018.

ANU economist and former Reserve Bank board member Warwick McKibbin

championed the idea along with economists John Quiggin, Danny Price and

then Senator Nick Xenophon in the leadup to the 2016 agreement between Morrison and Lowe.

Nominal GDP is gross domestic product before adjustment for prices.

In countries subject to big changes in export prices such as Australia,

it can provide a better guide to changes in income.

When nominal GDP is strong (as it is when minerals prices are high)

consumer spending is likely to be strong – perhaps too strong. When it

is weak (as it is when minerals prices collapse) consumer spending is

likely to be weak and in need of support.

But don’t get your hopes up

Given the natural caution of the bank and of this government, we

should probably expect something at the modest end of the spectrum –

even if something like a nominal GDP target would make sense.

Perhaps what’s most important isn’t what the statement says, but that

it says something and that the Reserve Bank sticks to it. It will lose

an awful lot of credibility if it sticks to nothing.

Property expect Joe Wilkes and I discuss the latest New Zealand data, and consider the drive to attract first time buyers in both NZ and Australia. What does the data say?

The number of home loan applications received by the major bank in the week following the federal election hit a six-month high, according to CEO Matt Comyn, via The Adviser.

Following

his address to the Trans-Tasman Business Circle, CEO of the

Commonwealth Bank of Australia (CBA) Matt Comyn revealed that the bank

experienced a surge in home loan applications via both the proprietary

and broker channel following the Coalition government’s election victory.

“I think, in particular at the moment, quite rightly, there is a strong interest in property,” Mr Comyn said.

“We

did have the strongest week in applications that we have seen in more

than six months. It did feel – certainly from a demand perspective –

there is quite a shift in sentiment.”

The election outcome

signalled the defeat of the Labor opposition’s proposed changes to

negative gearing and the capital gains tax, which some observers feared

would further dampen sentiment in the housing market.

Expectations

of a rate cut from the Reserve Bank of Australia (RBA) also heightened

following the election, after governor Philip Lowe conceded that the central bank would “consider the case for a rate cut” in June.

Mr

Comyn said the bank has revised its monetary policy forecast and now

expects an imminent rate cut from the RBA; however, Mr Comyn downplayed

its contribution to lifting market sentiment.

“It has an effect but there are other things that have a higher impact,” Mr Comyn added.

“Fiscal

stimulus, cuts to taxes, and increases in sentiment tend to have a much

bigger transmission effect to the broader economy.”

Further,

commenting on the fall in home values, Mr Comyn said that the

correction is an overall positive for the broader economy.

“It’s

painful for anyone who owns a house and sees the value of their asset

or any asset reduce, but I do think it’s a good thing,” he said.

“It’s in the interests of long-term financial stability.”

CBA launches new ‘green mortgage’

During his address, Mr Comyn unveiled a new “green mortgage” initiative, designed to reward “energy-efficient” mortgage holders.

Mr

Comyn said CBA plans to pass on the benefits of continued demand for

green bonds from investors, by offering $500 cashbacks to mortgage

holders who have solar panels installed in their homes.

Commenting

on the announcement, Daniel Huggins, CBA’s executive general manager,

home buying, said: “We are always looking for innovative ways to support

our customers, which is why we are launching this new initiative.”

He

added: “We understand many of our home loan customers could reduce

their energy volume and usage and pay less or become net positive for

energy by investing in energy efficient devices.”

Mr Huggins said the bank is in the process of introducing other initiatives to encourage home owners to make “greener choices”.

“We

want to support more of our customers who wish to install small scale

renewables by reducing their installation costs and payback periods,” Mr

Huggins added.

CBA stated that the green mortgage initiative will be formally launched in the coming weeks.

We look at the latest credit stats from the RBA and APRA. The credit impulse is slowing. Its at the slowest rate since 1974. So what does that really mean?

ANZ today released its scheduled APRA APS330 report covering the quarter to 31 December 2018. Credit Quality remains stable with a Provision Charge of $156 million tracking below the FY2018 quarterly average.

The Group loss rate was 10 basis points1 (14 bps 1Q18). Group Common Equity Tier 1 (CET1) was 11.3% at the end of the quarter.Consistent with usual practice, ANZ also released a chart pack to accompany the Pillar 3 disclosure.

The chart pack once again includes an update on Australian housing mortgage flows and credit quality. Australia home loan system growth was 4.2%2 in the 12 months to end December 2018. ANZ’s Australian home loan portfolio grew 1.0% ($2.7 billion) in the same period with the Owner Occupier portfolio up 3.5% ($6.1billion) and the Investor portfolio down 3.8% ($3.2 billion). In the 12 months to the end of January 2019, ANZ’s home loan portfolio grew 0.4%.

ANZ’s home lending growth trends are attributable to lower system growth, ANZ’s preference for Owner Occupier/Principal and Interest lending which drives faster amortisation, together with policy and process changes implemented in the second half of calendar year 2018.

ANZ Chief Executive Officer Shayne Elliott said: “Consumer sentiment has remained generally subdued with uncertainty around regulation and house prices impacting confidence. While we are maintaining our focus on the Owner Occupier segment, we acknowledge we may have been overly conservative in our implementation of some policy and process changes. We are also taking steps to prudently increase volumes in the investor space”.

Switching volumes for those moving from Interest Only to Principal and Interest during the quarter was $6 billion, of which $4 billion was contractual. The total amount of contractual switching scheduled for the reminder of FY19 is $12 billion. Customers choosing to convert ahead of schedule during the first quarter was in line with the quarterly average for FY18 ($2 billion). Total switching in FY18 was $24 billion.

Eurozone (EZ) GDP growth now looks likely to slow to just 1% this year according to a report published by Fitch Ratings‘ Economics team. The deterioration in growth prospects and declining inflation expectations will prompt the ECB to consider restarting asset purchases.

Economic activity data from the EZ has deteriorated more

sharply than other parts of the world in recent months and has delivered

the biggest negative surprise relative to market and Fitch’s own

expectations.

“While numerous transitory factors are partly to

blame, these cannot explain the breadth and depth of the slowdown.

Rather, we believe that the slowdown has been primarily the result of

deterioration in the external environment as net trade turned from a

tailwind to a headwind,” said Fitch’s Chief Economist, Brian Coulton.

The

domestic slowdown in China has, we believe, played a particularly

important role here. Germany’s greater trade openness and larger

exposure to China leave the largest European economy’s expansion more

vulnerable to China’s domestic cycle and import demand. This is

underlined by Germany having seen the biggest deterioration in activity

data among the EZ economies – despite a healthy domestic economy with

few of the imbalances that typically spark an abrupt downturn in

domestic demand. Furthermore, the deterioration in manufacturing

Purchasing Managers’ Indices (PMIs) since last summer has been greatest

in countries with a large auto export sector, dragged down by the first

decline in global car sales since 2009 and the first fall in vehicle

sales in China for several decades.

The weakening in EZ

external indicators has not been matched in the domestic economy. Labour

market performance remains strong supporting household income growth,

monetary policy remains supportive, bank lending conditions are easy and

credit to households and businesses continues to grow. Only in Italy

have we seen evidence of private sector borrowers reporting somewhat

tighter credit availability. Fiscal policy is also being eased in the EZ

and should be supportive of growth in 2019. Private sector debt ratios

have improved significantly since 2012 in Italy, Spain and Germany.

EZ

growth should recover through the course of 2019 as the policy response

in China helps to stabilise its economy from the middle of the year,

one-off impediments to growth in Germany unwind, and EZ macro policy is

eased. However, early indications for 1Q19 and the profile of our China

forecast mean that there will not be much of a pick-up in EZ quarterly

growth before 2H19.

This suggests that EZ growth in 2019 is

likely to be around 1% compared with our December 2018 GEO forecast of

1.7%, a substantial cut. Both Germany and Italy will see similar

revisions, with 2019 GDP growth now forecast at around 1% and 0.3%

respectively. Even with this lower forecast, downside risks remain from

an escalation in global trade tensions, a deeper slowdown in China, a

disorderly no-deal Brexit or increased uncertainty related to domestic

political tensions.

The sharp deterioration in growth prospects

and falling inflation expectations are likely to result in renewed

monetary stimulus measures from the ECB.

“We had already been

expecting the ECB to delay the start of its policy normalisation -both

interest rates and balance sheet reduction – but we now believe it will

seriously consider restarting QE asset purchases relatively soon,” added

Robert Sierra, Director in Fitch’s Economics team..

We also

foresee the ECB announcing a one- to two-year long-term refinancing

operation (LTRO) in March to replace the existing TLTRO2 programme,

which matures from June 2020. The rationale for a new targeted LTRO

(TLTRO) is less convincing in light of improved conditions in the

banking sector, but the ECB will want to avoid an unwarranted tightening

in credit conditions by abruptly withdrawing liquidity facilities.

Welcome to the Property Imperative weekly to the sixteenth of February 2019 – our digest of the latest finance and property news with a distinctively Australian flavour.

Watch the video, listen to the podcast, or read the transcript.

The data fest continued this week, with more evidence of weaknesses

appearing in the global economy, as Italy formally went into recession, Trump

declared an emergency to pay for his wall, trade talks progressed but Brexit

continues to wind into chaos. US retail figures were shockingly weak, a further

indicator that the current stock market rally is going to run out of steam.

Locally, more banks revealed margin compression, home prices continued to fall,

and the property spruikers fixated on the slightly higher auction clearance

results this past week, despite their continued weakness. Just another week in

paradise.

First to home prices. The latest index from CoreLogic shows more falls,

with Melbourne and Perth dropping 0.32% and 0.46% respectively. Sydney dropped

0.26%. As always, these averages only tell some of the story, but the falls

from peak are continuing to grow. Perth is now at 17.1% and Sydney 12.8%.

The impact of this is a reduction in the number of suburbs with a

million dollar plus price tag. CoreLogic data to the end of January 2019 showed

there were 649 suburbs across Australia that had a median house or unit value

at or in excess of $1 million. They said “Although this figure had increased

substantially from 123 suburbs a decade earlier, it has fallen from 741 suburbs

in January 2018. In fact, more suburb had a median of at least $1 million in

2017 (651) than do currently.” As at January 2019, there were 366 suburbs in

NSW that had a median house value of at least $1 million and 46 suburbs with a

median unit value of at least $1 million. In Vic, there were 129 suburbs that

had a median value of at least $1 million as at January 2019.

The negative wealth effect bites harder.

Australian auction clearance rates jumped noticeably last week, with the

final rate in Sydney at 54% and Melbourne 52.4%, whereas before Christmas we

were in the forties.

CoreLogic said that the combined capital city final auction clearance

rate remained above 50 per however volumes are still quite low across the

capitals with only 928 auctions held. The last time we saw the final weighted

average clearance above 50 per cent was back in late September 2018 when

volumes were significantly higher. One year ago, a higher 1,470 capital city

homes went to auction returning a final auction clearance rate of 63.7 per cent.

This weekend, CoreLogic is currently tracking 1,359 auctions across the

capital’s so volumes up by 46.4 per cent on last week. But the lower year on

year trend continues with volumes down 31.8 per cent when compared to the same

week last year (1,992).

In fact, we often get a small lift after the summer break, so this is in

my view not material. But the industry

is making the most of the higher results and not mentioning the painfully low

volumes.

This takes us to the question of whether there will be looser lending

ahead. Well ASIC came out this week with their thoughts for review on

responsible lending standards. Specifically, they refer to using the Household

Expenditure Measure as a guide, and the lenders need to make specific inquiry

to confirm affordability, not rely on a HEM without appropriate buffers. My view is that HEM 2.0 will used to

keep bank costs down but will keep credit standards much tighter than they

were. All this reinforces the focus on tighter lending standards

And remember that APRA recently confirmed the 7% hurdle affordability

rate and warned of risks in the system. And ASIC also benefited from the

passage of a bill this week to give the regulator powers to impose more fines.

ASIC is bearing its teeth. Corporate executives could face maximum jail terms

of 15 years for criminal offences and companies could cop fines of up to $525

million per civil violation. We are in a new lending environment, and as you

know by now, tighter credit means lower home prices.

HSBC made the point this week that

“The deceleration in the flow of

housing credit has been evident since at least early 2018 but has only recently

come into focus due to a flurry of weakness in indicators of domestic demand. This

includes a weaker-than-expected Q3 GDP print, the biggest monthly drop in

surveyed business conditions since the Global Financial Crisis, a 22.5%

year-ended fall in building approvals and monthly retail sales that turned

negative in December, confirming two soft quarters of consumer spending. In the ‘ugly contest’ of G10 Foreign Exchange,

we still think the AUD looks unattractive versus the higher carry and reserve

currency status of the USD. Our forecast remains for AUD/USD to trade down to

post-crisis lows of 66c by year-end.”

And another dampening factor to consider is that according to the AFR, China

has introduced jail terms for operators of “underground banks”

illegally helping tens of thousands of its citizens transfer money out of the

country to buy property overseas. This will reinforce the cooling demand we

have already seem from international buyers and will put more pressure on the

high-rise developers and , our real estate market more broadly. They took this

step to try and prop up the weakening Chinese economy, where home sales are

falling. Estimates by Gan Li, a

professor at Southwestern University of Finance and Economics in Chengdu

suggests that sales volumes in 24 cities tracked by China Real Estate

Index System fell by 44% in the first week of 2019 compared with a year

earlier, though the four largest cities including Shanghai and Beijing —

still saw a 12% increase.

Roughly 25% of China’s gross domestic product has been

created from property-related industries, according to CLSA. And housing is a crucial

means of asset formation in China, where ordinary citizens face restrictions to

overseas investment and have few domestic options besides local stock markets,

which lost 25% of their value last year. Prof. Gan’s striking estimate that 65

million urban residences — or 21.4% of housing — stand unoccupied was published

in a report in December. The proportion is up from 18.4% in 2011, driven by a

rise of vacancies in second- and third-tier cities, where demand is relatively

weaker and speculative activities are more prevalent. In other words, almost

half the bank loans are tied to housing assets that are neither being lived in

nor churning out rental income. According to the stress test conducted by the

professor, a 5% fall in housing prices would take away 7.8% of the actual asset

value of occupied houses, but 12.2% for unoccupied houses.

Back in Australia, the broker wars continue, with the industry mounting

a rear-guard action to try and reverse the Hayne recommendation to remove

conflicted remuneration by abolishing commission in favour of a buyers fee, as

well as bringing in a best interests obligation. They are however batting uphill, with

consumer groups claiming the mortgage broker industry is pretending to care

about reform, while vigorously lobbying politicians to protect their

commissions. The consumer groups said “Mortgage

broking lobbyists continue to swarm on Parliament House in an attempt to derail

crucial recommendations from the Royal Commission Final Report, showing the

sector cannot be trusted to stand up for everyday home owners when it comes to

reform”. As reported by SBS, They

are urging the government to implement the recommendations of the royal

commission into the financial services industry, including ending trail

commission payments to brokers for the life of a home loan and phasing out

commissions paid by lenders to brokers who push their loans.

And UBS added heat to the debate by reporting that 32 per

cent of customers who secured their mortgage via brokers stated they misrepresented

parts of their mortgage documentation compared to 22 per cent of customers who

used bank proprietary distribution. “In each category of factual accuracy (with

the exception of ‘would rather not say’) there was a statistically

significantly higher level of misrepresentation for customers who secured their

mortgage via a broker,” the report said.

Data from New Zealand also shows a weakening housing

market. According to the REINZ, outside of Auckland, seasonally adjusted house

prices rose by 2.3% in December, with prices up 9.7% year-on-year. But Auckland’s

seasonally adjusted median house price fell by 2.4% and was down 2.4%

year-on-year. The second year of falls. Christchurch’s (Canterbury) fell by

1.7% in January and was down 1.4% year-on-year. Whereas Wellington’s median

house price rose 0.9% in January but was up 11.6% year-on-year.

And in other New Zealand News, the Reserve Bank there has

gone coy on the next cash rate movement, it might be up, it might be down, as

some weaker economic indicators come through. I will be releasing a report from

Joe Wilkes on this tomorrow. And of course, RBNZ has also tabled a proposal to

lift bank capital much higher than APRA is proposing, Under the proposal, over

five years or so, banks’ Tier 1 capital ratios would rise from the current

industry average of around 12 percent of risk-weighted assets, to somewhere

above 16 percent for banks deemed systemically important.

RBNZ governor, Adrian Orr, defended the reforms, contending

that the proposed capital requirements are not excessive and would lead to a

more level playing field in the banking sector. He also attacked the excessive

returns of Australia’s Big Four banks as reported in the AFR saying “We have to

remember that the return on equity should be related to the risks they are

taking… At the moment, the return on equity for banking is incredibly strong

and we would even hazard to say over and above the risks they are holding

themselves as private banks, because there is an aspect in most OECD countries

of the ability to free ride — where returns can be privatised, and losses can

be socialised”. “More capital means sounder financial institutions… The capital

levels we are talking about are still well within the range of norms. We have

spent a lot of time trying to compare apples with apples”. A back of an

envelope calculation suggests Australian Banks would need an extra $100 billion

or so capital to get to the same level – so I guess you could call this the

price of Australia’s “too big to fail” policy. Tax payers may yet have to pick

up the bill. New Zealand is once again, way ahead on policy here.

The RBA had a couple of outings this week, but there was

little new. Still clinging to the wages growth will come mantra, and also

making again the point that the Aussie Dollar can go lower, to support the

economy. Despite the evidence. Expect a rate cut later, the question now is

whether it will be before or after the election, or both.

And just when you thought it was case to come out after the

Banking Royal Commission, The Treasurer noted that there will be a further

review in three years’ time to ensure they have improved their behaviour and

are treating customers better. And Josh Frydenberg wrote this week to the heads

of the Australian Banking Association, Australian Securities and Investments

Commission and Australian Prudential Regulation Authority directing them to

swiftly implement dozens of Commissioner Kenneth Hayne’s recommendations that

pertain to their bodies. This reform is not going away. For a Banker’s view see

our post “Beyond The Royal Commission” where I discuss what the banks should be

doing with Ex. ANZ Director John Dalhsen.

And talking of reform, post the Royal Commission, there was

progress on the Glass Steagall bill in Parliament this week. The question of

structural separation of the banks has been passed to a Senate Committee for a

review. Here is an extract from

Hansard:

The Hayne Royal Commission into Misconduct in the Banking,

Superannuation and Financial Services Industry has highlighted the necessity

for banks to be limited to their core industry.

The vertical integration of the banks providing additional

services including financial advice, insurance and superannuation have been

shown to be the root cause of rorts, over charging and profit gouging.

Australia’s best-known finance commentator Alan Kohler

wrote in The Australian on 3 December 2018 and I quote:

I have been opening a random sample of the 10,140

submissions — just short ones from individuals. Without exception they called

for the banks to be broken up and most of them, surprisingly, used the term

‘Glass-Steagall’ – suggesting that the now-repealed American law that used to

forcibly separate banking from insurance and investment banking be introduced

into Australia.

Alan Kohler stated further:

That would certainly be a fertile field for the Royal

Commissioner to plough, although most of the banks have already announced plans

to break themselves up along those lines so perhaps such a recommendation would

lack drama.

Unlike most commentators and politicians, however, Kohler

is not totally fooled by these moves from the banks that appear as if they are

separating voluntarily.

Continuing, he made the following very important point:

But Westpac says it will keep its insurance and wealth

management division and AMP and Macquarie have not announced any plans to get

rid of their banks, so an Australian version of Glass-Steagall would make it uniform

and would make sure they didn’t slide back into their bad old ‘one stop shop’

ways in future.

Kohler now joins the ranks of other notable Australian

experts who have endorsed the Glass-Steagall option.

In the aftermath of the global financial crisis, Don Argus,

former CEO of National Australia Bank and former Chairman of BHP, said in The

Australian on 17 September 2011 and I quote:

People are lashing out and creating all sorts of

regulation, but the issue is whether they’re creating the right regulation …

What has to be done is to separate commercial banking from investment banking.

Former ANZ director John Dahlsen wrote in the Australian

Financial Review on 21 August 2018 and I quote:-

Problems in banking will not be solved until the structure

is changed … With barriers removed it is possible that banks and the

investment market will move to unlock shareholder value in structural

separation, following the principle of the US Glass-Steagall Act, which kept

commercial and retail banking separate. Voluntary demergers would threaten the

gravy train of ‘coupon clipping’ for fee extraction, but enforced separation in

Australia seems inevitable…

Former ACCC chairman Professor Alan Fels was quoted in The

Australian on 9 August 2018 and again I quote:

There are a number of serious structural issues that need

to be considered, the first and most obvious is the separation of the activity

of creating financial products and then offering so-called independent advisory

services to customers on what are the best products. A second very important

one is whether there should be a structural separation between traditional

banking activities and the more risky investment activities … Banks benefit

from the implicit guarantee on their deposit liabilities which flows into their

trading activities.

Banking expert Martin North of Digital Finance Analytics

stated in his submission to the Interim Report of the Royal Commission:

The large players are too big to fail and too complex to

manage, and need to be broken apart. A modern Glass-Steagall separation would

achieve this, and is proven to reduce risk, and drive better customer outcomes

and right-size our finance sector.

Former APRA Principal Researcher Dr Wilson Sy recommended

in his submission to the Royal Commission:

The financial system should be structurally separated to

simplify regulation, increase competition and innovation, and better serve the

community.

The Banking System Reform (Separation of Banks) Bill 2018,

previously introduced by the Honourable Bob Katter MP in the House of

Representatives but since lapsed, is being introduced by Pauline Hanson’s One

Nation Party into the Senate due to my party’s ongoing commitment to overcome

the systemic failure in our banking system and, more importantly, in bank

management per se.

So, to the markets. The ASX 100 rose just 0.08% on Friday

to 4,989.20 and is now up 3.71% over the past year. The local volatility index was up a little to

12.73, and is down 30.09% from a year back, as market concerns continue to

ease. The ASX 200 Financials rose 0.15% on Friday to end at 5,779.80 and is

still down 7.58% from a year ago. The banks are a riskier proposition these

days as mortgage lending continues to slow.

ANZ was up 1.02% to 26.81, down 3.26% from last year. CBA

was up 0.31% to 70.81 and is down 4.33% from this time last year. NAB was down

a little to 24.22 and has fallen 16.11% over the past year. They are currently

the least trusted bank, according to recent Roy Morgan research, and the recent

leadership changes are clearly not helping. Westpac was up 0.19% to 26.24, down

13.8% from a year back, and of course the ASIC HEM case remains unresolved.

Bank of Queensland was up 0.3% to 9.95, down 17.2% from this time last year.

SunCorp who reported this week with a lower margin, and higher costs (including

a number of insurance claims events) was up 0.92% to 13.10, down 1.65% from

last year. Bendigo and Adelaide Bank who also reported again with margin down

and costs up, was up 0.1% to 9.87, down 9.38% from this time last year. Its tough being a regional bank in a slowing

and competitive mortgage market. AMP who also reported this week, with a

significant, if not signalled drop in profit following the Royal Commission,

fell 3.11% on Friday to end at 2.18, down 57.39% from a year ago. I find it

hard to know what the true value of the company is, given the remediation challenge

ahead.

Macquarie, who gave a bullish update, was down 0.98% to

124.22, up 21.42 since last year, and they remain confident of the outlook,

helped by their international footprint.

Genworth the lenders mortgage insurer fell 0.83% to 2.38,

down 8.75% over the year and Aggregator Mortgage Choice rose 0.63% to 79.5

cents, down 64.44% from last year, as the broker commissions question bites.

The Aussie was up 0.11% to 71.47, still down 10.61% from a

year ago. More falls ahead me thinks. The Aussie Gold cross was up 0.16% to

1,850.35, up 8.71% from last year. And the Aussie Bitcoin cross was down 0.5%

to 4,552.1 down 62.69% from a year ago.

In the US, headline nominal retail sales fell by 1.2% over the month, their

sharpest monthly decline since the financial crisis. Notwithstanding ongoing

strong job creation, consumption weakened on the back of low confidence and

market turbulence. Yet Wall Street rallied on Friday, with the Dow and the

Nasdaq posting their eighth consecutive weekly gains as investors grew hopeful

that the United States and China would hammer out an agreement resolving their

protracted trade war.

Talks between the United States and China will resume in Washington next

week, with both sides saying progress has been made toward resolving the two

countries’ contentious trade dispute. With just weeks to go until the March 1

deadline, President Donald Trump offered an optimistic update on the second

round of U.S.-China trade talks, prompting traders to turn bullish on stocks. Trump

said that trade talks “are going extremely well,” stressing that the

United States is closer than ever to “having a real trade deal” with

China. Without a trade deal secured by March 1, the U.S. could implement

further tariffs on China. Trump said, however, that he would be

“honored” to remove tariffs if an agreement can be reached.

This newfound optimism on trade pushed energy stocks sharply higher, as

traders had long feared a prolonged trade war would hurt economic growth in

China, the world’s largest oil consumer, denting oil demand.

The Dow Jones Industrial Average rose 1.74 percent, to 25,883.25, up 2.19% from last year, the S&P 500

gained 1.09 percent, to 2,775.6 up 1.76% on last year and all 11 major sectors

in the S&P 500 ended the session in the black. The SP 100 was up 1.09% to 1,217.96, up 0.97%

from last year. The Volatility index was

down 8.08% on Friday to 14.91, 15.78% lower than a year back, and well off its

nervous highs.

The S&P Financials index was down 0.55% to 425.53, still down 11.01%

from a year earlier reflecting concerns about future earnings. Goldman Sachs

was up 3.1% to 198.50, still 26.68% lower than last year.

The Nasdaq Composite was up 0.61 percent, to 7,472.41 and is 3.97%

higher than this time last year. Apple was down 0.22% to m170.42. Up 2% from a

year back. Google was down 0.85% to 1,119.63, up 5.27% while Amazon was down

0.91% to 1,607.95, up 11.83% after scrapping its plans for a New York

headquarters. Facebook was down 0.88% to 162.50, down 8.67% from a year back.

Intel was up 1.67% to 51.66, and 11.67% up from last year.

The Feds weaker stance continues to flow through to a lower 10-Year

treasury rate, and it was up 0.2% on Friday to 2.664. The 3 Month rate was also

down 0.13% to 2.427. As a result, funding costs are easing a little, taking

some of the risk pressure off, but of course leaving the US cash rate lower

than the FED would have liked to see – the economy has not escaped the QE bear

trap yet.

The US Index was down a little to 96.92 and is 8.91% higher than a year

back. Across the pond, the British Pound US Dollar was up a little, to 1.2897,

down 8.61% from a year ago. The UK Footsie was up 0.55% to 7,236.68, and is

slightly lower than a year back, which given the Brexit uncertainly says

something. Prime Minister May

suffered another humiliating defeat as Parliament voted against her amendment

to seek reaffirmation of support to see changes to her Brexit deal. The vote

only slightly raised the risk of a no-deal Brexit, but the base case still

remains Article 50 will need to be extended. The Footsie Financials index was up 0.37% to 656.38

and down 1.57% from a year back. The Royal Bank of Scotland, who reported this

week was up 2.44% to 247.50, but down 12.11% from last year. Its profits were

up, and it also reported making big loans to companies to allow them to forward

buy and hold goods ahead of Brexit. The RBS is till majority owned by the

Government following its bail-out a decade ago.

The Euro US Dollar was up a little to 1.1296, down 9.34% from last year,

Deutsche Bank was up 4.94% to 7.65 Euros, but still down 42.3% from this time

last year.

The Chinese Yuan US Dollar ended at 0.1476, down 6.29% from a year back, WTI Oil was up 2.57% to 55.81, down 9.65% from last year, Gold reversed earlier losses following the huge retail sales miss number and rose 0.83% to 1,324.75 down 5.43% over the year, Silver was up 1.46% to 15.755, down 7.78% over the past 12 months and Copper was up 1.51% to 2.816 down 14.22 % annually.

Finally, Bitcoin ended at 3,665.3, down 61.29% over the past year. It broke above the upper bound of a downside channel recently that was containing the price action since January 14th. On top of that, the rally brought the price above the 3500 mark, with the crypto hitting resistance near the key obstacle of 3700, before retreating somewhat. JPMorgan announced that they became the first U.S. bank to create and successfully test a digital coin representing a fiat currency. This is quite the pivot, as many will recall the CEO Dimon’s comments that bitcoin is a fraud and any employee trading it would be fired for being stupid. JPM Coin will run on the JPMorgan’s own blockchain, called Quoroum. This is the very early stages for JPMorgan’s digital coin and initial goal is to accelerate corporate payments. While cryptocurrency fans may love the announcement, this does not necessarily bode well for bitcoin, as JPM Coin could be the beginning of severe competition for the digital currency.

Now that nearly 80 percent of S&P 500 companies having reported, fourth-quarter earnings season is largely in the rearview mirror. Analysts now see a profit increase of 16.2 percent for the quarter, but going forward, however, the outlook continues to worsen. First quarter earnings are currently seen falling by 0.5 percent, the first year-on-year decline since mid-2016.