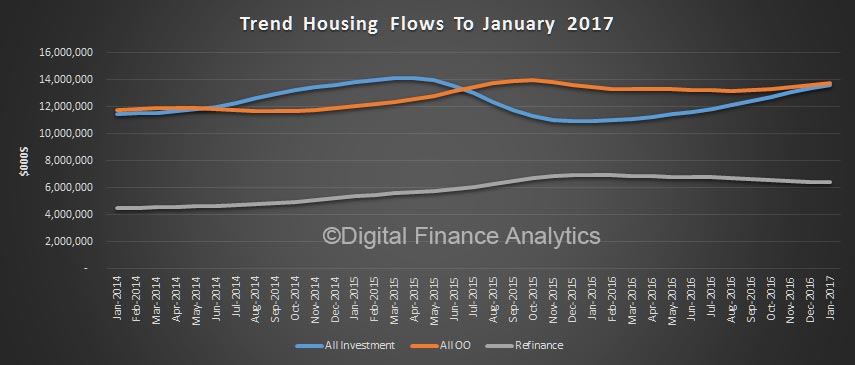

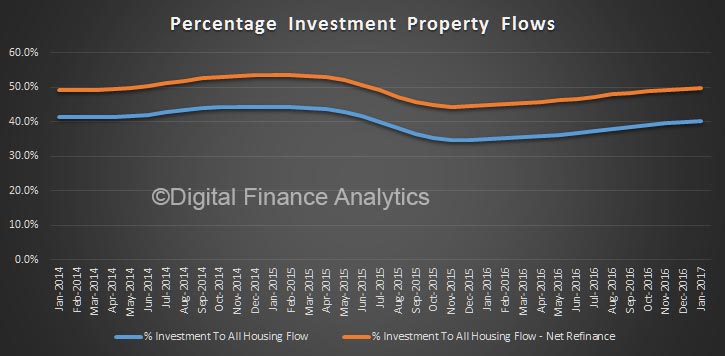

The ABS released their Housing Finance data today, showing the flows of loans in January 2017. Those following the blog will not be surprised to see investor loans growing strongly, whilst first time buyers fell away. The trajectory has been so clear for several months now, and the regulator – APRA – has just not been effective in cooling things down. Investor demand remains strong, based on our surveys. Half of loans were for investment purposes, net of refinance, and the total book grew 0.4%.

In January, $33.3 billion in home loans were written up 1.1%, of which $6.4 billion were refinancing of existing loans, $13.6 billion owner occupied loans and $13.5 billion investor loans, up 1.9%. These are trend readings which iron out the worst of the monthly swings.

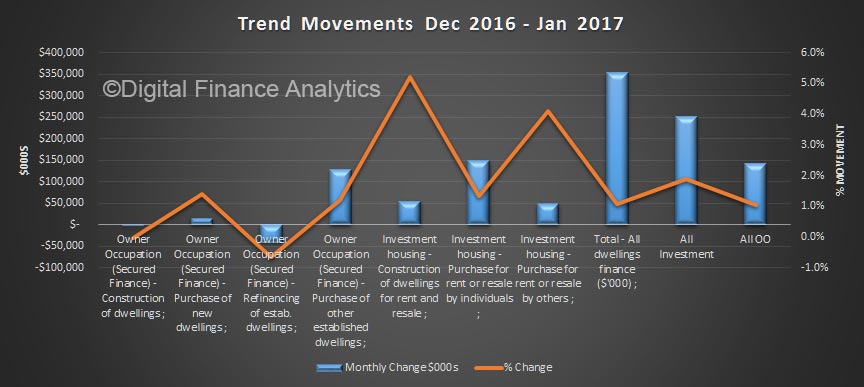

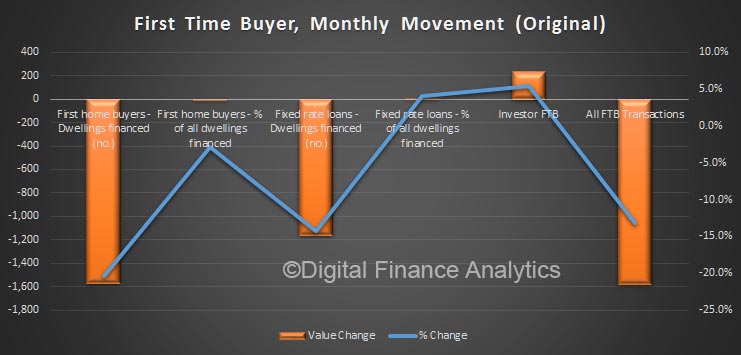

Looking at individual movements, momentum was strong, very strong across the investor categories, whilst the only category in owner occupied lending land was new dwellings. Construction for investment purposes was up around 5% on the previous month.

Stripping out refinance, half of new lending was for investment purposes.

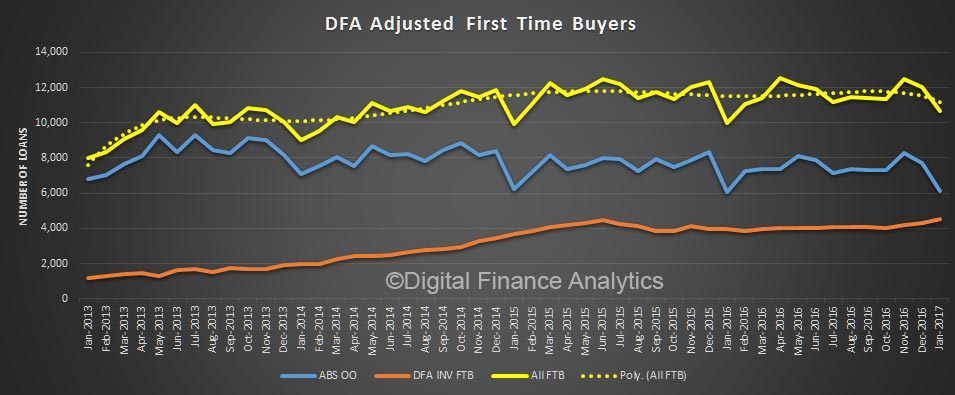

First time buyers fell 20% in the month, whilst using the DFA surveys, we detected a further rise in first time buyers going to the investment sector, up 5% in the month.

Total first time buyer activity fell, highlighting the affordability issues.

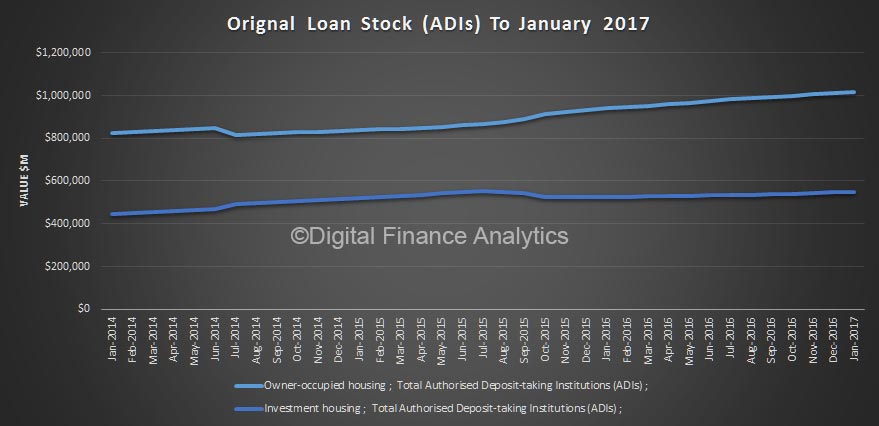

In original terms, total loan stock was higher, up 0.4% to $1.54 trillion.

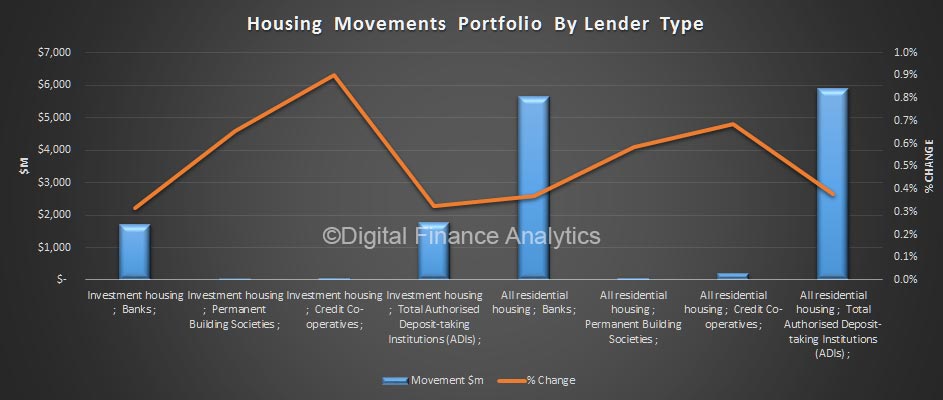

Looking at the movements across lender types, we see a bigger upswing from credit unions and building societies, compared with the banks, across both owner occupied and investment loans. Perhaps as banks tighten their lending criteria, some borrowers are going to smaller lenders, as well as non-banks.

We think APRA should immediately impose a lower speed limit on investor loans but also apply other macro-prudential measures. At very least they should be imposing a counter-cyclical buffer charge on investment lending, relative to owner occupied loans, as the relative risks are significantly higher in a down turn.

The budget has to address investment housing with a focus on trimming capital gain and negative gearing perks. The current settings will drive household debt and home prices significantly higher again.

Politicians and the powerful property lobby continue to argue that building more houses is the solution to Australia’s chronic affordability problems.

But a “supply-side solution” – as propounded by NSW Premier Gladys Berejiklian as well as Prime Minister Malcolm Turnbull and Treasurer Scott Morrison – will only work if affordability is just a supply-side problem. Evidence suggests this is not the case. In fact, our analysis shows that Australia is almost a world leader in rates of new housing production.

How Australia compares

One way to assess Australia’s supply performance is to compare it with other developed countries. The graph below compares the number of dwelling completions per 1,000 persons across 13 countries, for the years 2010 and 2015. On this measure, Australia’s new housing production is second only to South Korea’s.

Australia delivers two-thirds more homes per 1,000 persons than the US and four times more than the UK. When we measure supply as a proportion of existing stock, Australia again ranks second with a rate double that of the US.

OECD questionnaire on affordable and social housing; World Bank population growth and total population figures, Author provided

A slightly different approach takes into account population growth. This involves measuring dwelling completions per head of new population. Here Australia’s performance sits in the middle of the pack.

We are delivering just over 0.5 dwellings per head of new population compared to more than 2 in South Korea. This rate is, however, still ahead of the UK and comparable to the US. Again, that suggests inadequate supply is not the major cause of the affordability crisis.

OECD questionnaire on affordable and social housing, World Bank population growth and total population figures, Author provided

State comparisons of supply

At a national level, supply seems pretty healthy. But there are significant state variations. This might, on the surface, be used to explain different patterns of price growth.

The table below shows that New South Wales has produced fewer new homes per 1,000 people than Australia overall over a 30-year period. The difference was particularly marked between 2005 and 2015.

State comparisons of new housing supply.ABS building activity Australia cat. 8152; ABS Australian Demographic statistics Cat 3101, Author provided

However, higher supply output in the other states has certainly not created affordable markets. In NSW, the last two years have delivered significant supply growth yet prices have continued to rise just as fast. So why do prices rise with supply growth?

Demand drives supply

In a market-driven housing system, price stimulates new housing supply. In Australia new supply has responded relatively quickly to price rises (despite the continuous rhetoric from the property lobby about planning).

But there is always some lag due to the time it takes to secure necessary approvals and physically construct property. There is no such lag with demand meaning there is often a sustained mismatch between the two – positive or negative.

In a rising market, development becomes more profitable and land values rise, meaning greater returns for all concerned. Potential future capital gains stimulate investment activity. Price rises also allow owner-occupiers to trade up as the equity in their own dwelling increases.

In such circumstances, increased levels of housing supply do little to satiate demand created by population growth and the appetite of investors.

Western Australia has had an incredible level of housing completions over the last 30 years, as shown in the table, with 2014 and 2015 particularly strong. In the last 12 months, dwelling commencements have collapsed by more than 25%. Prices have been falling slowly for almost three years driven by the contraction in the resources sector and strong levels of new supply.

However, even under these conditions, WA housing affordability shows little sign of improving for those on low incomes. The market still cannot deliver housing for those at the bottom end of the market.

The housing market is simply unable to deliver housing that is affordable to those on lower (and, increasingly, moderate) incomes because there is a minimum cost of delivering housing that meets minimum community standards. This is made up of the land price, the physical construction costs of the dwelling, and the profit required for taking on the development risk.

This is why market intervention and subsidy are essential to deliver options for those on low incomes.

Targeted interventions are needed

Two strategies are needed to deliver affordable housing to the lower end of the market.

First, demand-side measures need to be better targeted to stimulate investment in new supply, particularly affordable rental housing, rather than simply fuelling demand.

Second, any government serious about improving affordability needs to put more resources into the community housing sector. This could be funded in two ways: partly by taxing the windfall gains from development and partly by reallocating existing demand-side subsidies.

The community housing sector can operate counter-cyclically. This means it can maintain housing supply even when house prices stagnate or fall – which is good for the economy.

Targeting supply to deliver housing for those on low incomes and reining in demand-side incentives that fuel prices will make some difference to affordability for those most affected.

There was some encouragement over the weekend. Scott Morrison discussed the rental market and social housing as part of the affordability solution. This was a welcome change from trotting out the tired old supply arguments and threatening to fuel demand through more home ownership incentives.

Let’s hope the treasurer follows through and delivers some much-needed “whole of housing market” thinking in the May budget.

Authors: Steven Rowley, Director, Australian Housing and Urban Research Institute, Curtin Research Centre, Curtin University; Nicole Gurran, Professor – Urban and Regional Planning, University of Sydney; Peter Phibbs, Chair of Urban Planning and Policy, University of Sydney

While 3D-printing may have been faded away in recent years from the spotlight of core “disruptive” technologies, that may soon change again after a company managed to 3D-print an entire house in just 24 hours. Located in Russia, the following 400-square-foot home, or 37 square meters, was built in just a day, at a cost of slightly over $10,000.

As profiled in the Telegraph, the company Apis Cor, 3D-printing specialists based in Russia and San Francisco, built the house using a mobile printer on-site. According to the company, the walls of the building were printed and painted in just 24 hours.

What makes Apis’ process unique is that while 3D-printing a home usually involves creating the parts off-site and constructing the building later, Apis Cor uses a mobile printer to print their apartments on-site. As profiled here, in 2015 the world’s first 3D-printed apartment building was constructed in China, with the structures printed off-site.

However, the Apis process is unique in that it eliminates the need to transfer the printed blocks to the construction site.

“Printing of self-bearing walls, partitions and building envelope were done in less than a day: pure machine time of printing amounted to 24 hours,” the company said.

The main components of the house, including the walls, partitions and building envelope are printed solely with a concrete mixture. Once the house has been completed, the printer is removed with a crane-manipulator and the roof is then added, followed by the interior fixtures and furnishings, as is a layer of paint to the exterior of the house.

The total construction cost of the house: $10,134.

The initial house consists of a hallway, bathroom, living room and kitchen and is located in one of Apis Cor’s facilities in Russia. The company has claimed that the house can last up to 175 years.

Nikita Chen-yun-tai, the inventor of the mobile printer and founder of Apis Cor, explained his desire is “to automate everything”.

“When I first thought about creating my machine the world has already knew about the construction 3D printing,” he explained. “But all printers created before shared one thing in common – they were portal type. I am sure that such a design doesn’t have a future due to its bulkiness. So I took care of this limitation and decided to upgrade a construction crane design.”

He adds: “We want to help people around the world to improve their living conditions. That’s why the construction process needs to become fast, efficient and high-quality as well. For this to happen we need to delegate all the hard work to smart machines.”

Apis Cor has claimed to be the first company to have developed a 3D printer than can print whole buildings on-site.

For now the technology is in its infancy, however in a few years, the deflationary pressures unleashed by Apis-Cor and its competitors could results in a huge deflationary wave across the construction space, and would mean that a house that recently cost in the hundreds of thousands, or millions, could be built for a fraction of the cost, providing cheap, accessible housing to millions, perhaps in the process revolutionizing and upending the multi trillion-dollar mortgage business that is the bedrock of the US banking industry.

The Victorian Government has announced the First Home Owner Grant will be doubled in regional Victoria. The Grant will increase from $10,000 to $20,000, commencing 1 July 2017. The Government expects up to 6,000 first home buyers will receive extra assistance.

The increased grant will be available to first home buyers building new homes valued up to $750,000, and is an additional $50 million investment in regional Victoria over the next three years.

The grant will be applicable to contracts signed from 1 July 2017 to 30 June 2020, at which time, the Government will review the benefits for first home buyers and businesses in regional Victoria.

However, our analysis of such grants, not only here but overseas is that they simply lifts prices by the same amount. It is a zero sum game.

Whilst we understand the political agenda, this move is unlikely to improve housing affordability and access to property.

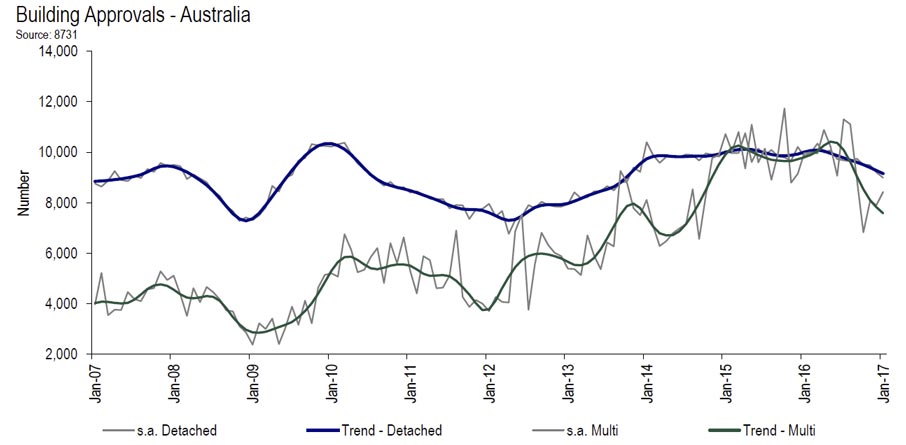

The number of dwellings approved fell 2.1 per cent in January 2017, in trend terms, and has fallen for eight months, according to data released by the Australian Bureau of Statistics (ABS) today.

Here is the data charted by the HIA. They say “new dwelling approvals have been falling back over the past year, particularly due to a reduced inflow of new multi-unit projects”.

In trend terms, dwelling approvals decreased in January in the Australian Capital Territory (19.4 per cent), Queensland (6.8 per cent), New South Wales (4.8 per cent), Northern Territory (1.7 per cent) and Western Australia (0.3 per cent). Dwelling approvals increased, in trend terms, in Tasmania (3.0 per cent), Victoria (2.9 per cent) and South Australia (1.1 per cent).

In trend terms, approvals for private sector houses fell 1.2 per cent in January. Private sector house approvals fell in New South Wales (2.2 per cent), South Australia (1.4 per cent), Western Australia (1.4 per cent), Queensland (1.0 per cent) and Victoria (0.3 per cent).

In seasonally adjusted terms, dwelling approvals increased by 1.8 per cent in January, driven by a rise in total dwellings excluding houses (6.6 per cent). Total house approvals fell 2.2 per cent

The value of total building approved fell 2.9 per cent in January, in trend terms, and has fallen for six months. The value of residential building fell 0.9 per cent while non-residential building fell 6.8 per cent.

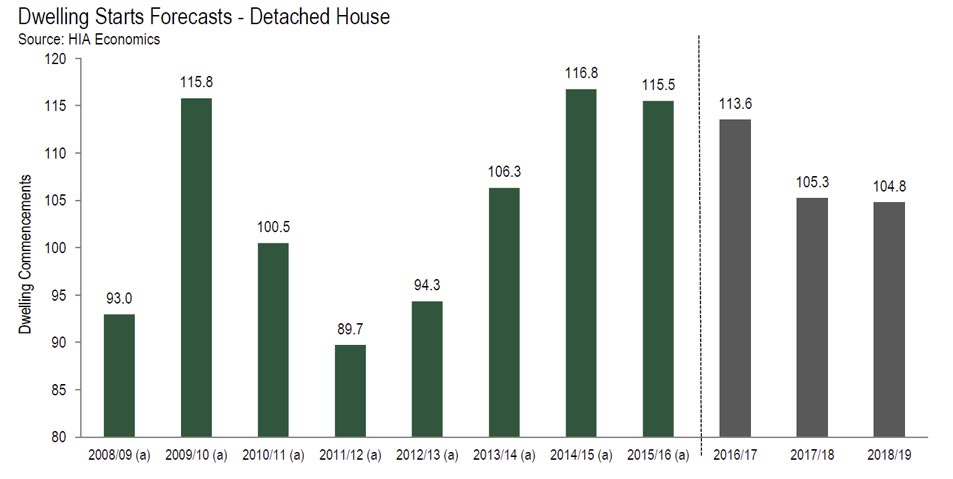

According to the Housing Industry Association, during the year ended September 2016, there were over 229,000 dwellings that commenced construction. While this is still an exceptionally high level of activity based on historical experience, the annualised level of commencements has eased since peaking at over 231,000 in the year ending in the March 2016 quarter. This is supportive of HIA’s view that the current new residential building cycle is likely to have peaked in 2016.

Detached houses

Despite the decline in the total number of commencements, the detached house segment of the market has proven resilient.

There were 29,634 detached houses commenced during the September 2016 quarter, which makes a total of 115,953 commencements in the year up to this point.

The prevailing dynamics in the detached house market during 2015/16 were a marked contraction in the level of activity in Western Australia counter balancing the ongoing resurgence in the Victorian and New South Wales markets. While there were variations in other state and territory markets, when we take a national perspective these two factors eclipsed the rest. However, we are now well into 2016/17 and approaching a new phase of the cycle which will have a fresh dynamic. The headwinds afflicting WA may soon subside and Sydney and Melbourne’s time in the sun may be drawing to a close.

From a national perspective, detached house commencements are forecast to ease by 1.7 per cent in 2016/17 ahead of a further decline of 7.3 per cent in 2017/18. After falling to a low of 104,800 starts in the 2018/19 year, the level of detached house building is forecast to gradually improve across the out years of the forecast horizon.

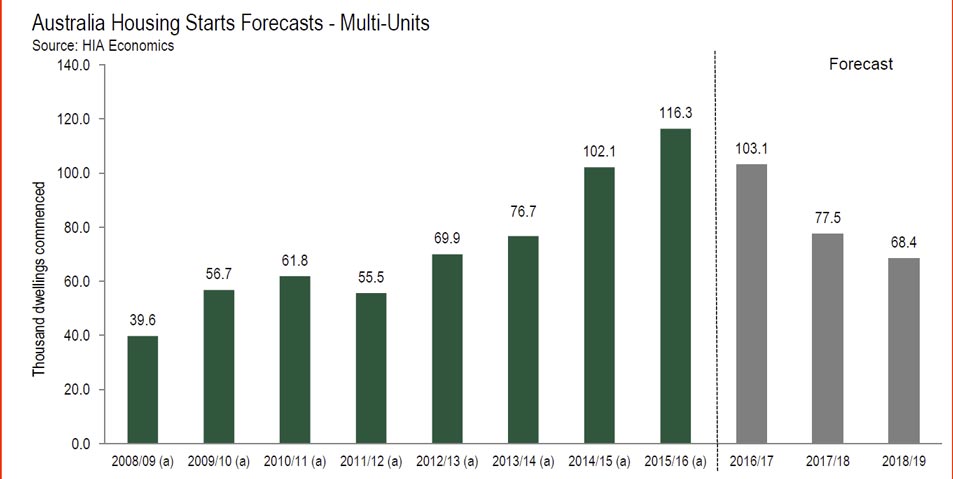

Multi-unit dwellings

The ‘multi-unit’ market has weakened overall. After a very strong result in the March 2016 quarter, the number of multi-unit commencements fell away quite sharply throughout the middle of the year.

However, there are markedly different trajectories for the semi-detached market (including townhouses, row and terrace type dwellings) and the market for apartments in buildings of four or more storeys.

The number of commencements for semi-detached dwellings continued to grow throughout the year. In contrast, the number of commencements for apartments in high-rise developments slowed as activity in Victoria and Queensland eased. The flow of new apartment projects getting underway in New South Wales has remained more buoyant and there is a record level of apartments in developments awaiting commencement.

In aggregate, there were a total of 25,202 multi-unit dwellings commenced in the September 2016 quarter, which is equivalent to 113,383 across the full year. HIA is forecasting that multi-unit dwelling commencements will remain at quite a high level in the 2016/17 financial year, albeit with an annual decline of 11.3 per cent. Looking beyond 2016/17 is when we anticipate commencements will post more significant declines. Multi-unit commencements are forecast to decline by around 25 per cent in 2017/18, and then by a further 12 per cent in 2018/19. The 2018/19 year is projected to be the low point of the cycle for multi-unit commencements, when 68,400 starts are forecast to occur.

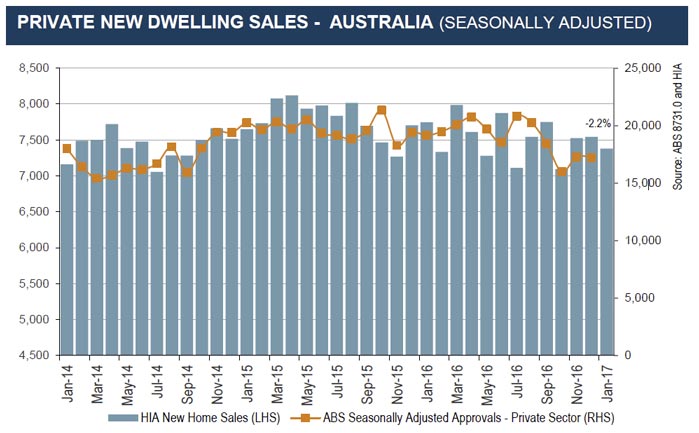

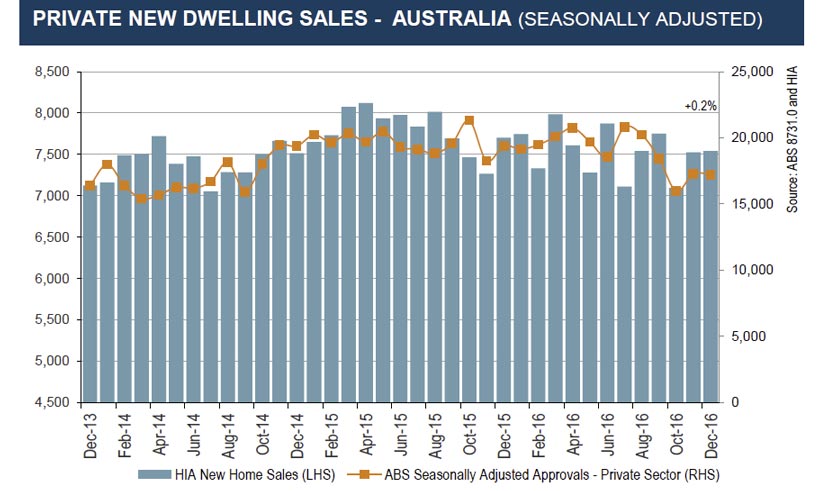

The first key new housing update for 2017 provides a softer update, said the Housing Industry Association.

The January 2017 update for the HIA’s monthly New Home Sales survey reveals a decline of 1.5 per cent in detached house sales following a similar fall of 1.6 per cent in December last year. Detached house sales fell by a very modest 1.1 per cent over the three months to January 2017 to be down by 4.0 per cent when compared to the same period 12 months previously. The sale of ‘multi-units’ dropped by 4.3 per cent in January following an increase of 6.4 per cent in December 2016. Over the three months to January 2017 multi-unit sales increased by 4.8 per cent to a level 9.0 per cent higher than the comparable period a year earlier.

Seasonally adjusted new detached house sales increased by 12.1 per cent in Western Australia in January 2017 following a sharp dip of 9.1 per cent last December. In the month of January 2017 detached house sales fell by 6.8 per cent in New South Wales, 4.1 per cent in Victoria, 2.0 per cent in Queensland, and 1.4 per cent in South Australia.

“The HIA New Homes Sales Report – a survey of Australia’s largest home builders showed a moderate decline of 2.2 per cent in January 2017,” said HIA Chief Economist, Dr Harley Dale. “This weaker update does follow a relatively decent run home for new home sales in late 2016.”

“Given that Australia is tailing off from the largest and longest new home building cycle in history, both the total and sub-component profiles for new home sales are still in very good shape,” said Harley Dale.

“There aren’t many sectors punching above their weight in the nation’s economy right now, so the profile for new home sales is also good news for Australia as a whole.”

“HIA’s latest forecasts for new dwelling commencements will be released on Thursday and they will paint a healthy short term picture for residential construction. There is nothing to be seen in this latest update for new home sales or from any other recent leading indicator results to deter us from this outlook,” concluded Harley Dale.

Property giant Lendlease is seeing longer settlement periods and higher cash buying as apartment buyers respond to a recent clampdown on mortgage lending by banks.

The company said residential pre-sales remained steady but customers are taking longer – between 28 to 30 days – to complete settlements at Australian apartment buildings.

“In Australia, we are working with buyers who need more time for settlement. We are also seeing increased use of non-banking sources of finance and also more cash buying,” chief financial officer Tarun Gupta said.

Australia’s major banks have tightened lending criteria for property investors over the past year – particularly for foreign investors, in response to the regulator’s cap on lending growth in the investor market.

“We are seeing an uptick in cash settlements, which are now 30 to 35 per cent. We are also seeing more non-banking finance entities writing loans for our customers,” Mr Gupta said.

Lendlease booked residential pre-sales of $5.7 billion, with 2,037 units settled, including 628 apartments.

Apartment defaults continued to be minimal, at less than one per cent.

The company delivered a 12 per cent lift in first-half profit, leveraging on its strength in the construction and office building space.

It reported net profit of $394.8 million for the six months to December 31, as margins jumped at its US construction business and sales were stronger at a number of its Australian office buildings.

Revenue rose 7.6 per cent to $7.95 billion.

Lendlease lifted earnings for the development division by 10 per cent, in part because of the completion of the last of the three Barangaroo office towers in Sydney.

“Commercial development, in particular the Australian office sector, was a highlight of the first half result,” chief executive Steve McCann said over an investor call.

The company made forward sales for three office buildings in Brisbane and Melbourne, and sold down a majority stake in the Circular Quay Tower development in Sydney.

The office segment is expected to be a major contributor to future growth at the company, with 13 major commercial buildings now in delivery phase across the globe, with estimated value of $7 billion.

Total development pipeline grew to $49 billion, up five per cent from a year earlier.

“We remain well placed for future success given earnings visibility and a targeted and disciplined approach to delivering on our strategy,” Mr McCann said.

But the main contributor to profits was the construction division, where half year earnings jumped 45 per cent, mostly on the back of a rebound in margins at the American business as a number of projects were completed.

Construction margins were weaker in Australia, but were offset by increased engineering activity.

The company declared an unfranked interim distribution of 33 cents per security, up 3.0 cents from a year earlier.

Residential land sales increased for the second consecutive quarter as prices reached a new high during the three months to September 2016 according to the latest HIA-CoreLogic Residential Land Report published today by Housing Industry Association and CoreLogic.

Today’s HIA-CoreLogic Residential Land Report shows that the land lot price nationally rose by 3.3 per cent during the September 2016 quarter to another record high of $243,585. During the quarter, 18,510 land lot transactions are estimated to have occurred across Australia, 6.4 per cent higher than the previous quarter but 7.3 per cent lower than a year earlier. During the six months to September 2016, land transactions experienced the largest increase in Perth (+5.5 per cent) compared with the same period year earlier. Land turnover also increased in Hobart (+2.1 per cent) over the same period. Land sales saw the largest reduction in Sydney (-29.9 per cent) over the same period. Turnover also fell back in Melbourne (-13.5 per cent), Adelaide (-5.1 per cent) and Brisbane (-3.3 per cent).

“During the September 2016 quarter, the volume of land sales increased by 1,121 lots compared with the June 2016 quarter,” said HIA Senior Economist, Shane Garrett.

“However, the number and size of government taxes, fees, levies and charges on new residential land needed to accommodate our growing population continues to weigh down on our national housing affordability challenges,” explained Shane Garrett.

“In addition to removing the excessive taxes on new land, long term commitment from all levels government in the areas of planning, land release and infrastructure funding is necessary.”

“Price pressures in the residential land market are greatest in the capital cities, with Sydney prices now approaching $1,000 per square metre,” concluded Shane Garrett.

According to CoreLogic research director Tim Lawless, “with median land prices rising consistently since mid-2013 it is clear that one of the primary drivers of broader housing market growth has been the underlying appreciation of land values, which is pushing the overall value of housing higher. The median dollar value per square metre of vacant land was recorded at $927 in Sydney, which is 32 per cent higher than the next most expensive capital city, which is Perth where the rate per square metre is $701. The high land costs are a significant contributor to the unaffordability of housing across Australia’s largest capital city.”

“With housing affordability one of the most topical housing market issues, the underlying drivers of high land costs need further scrutiny. Government policies around land release and headworks costs are central to the debate around housing affordability and the cost of vacant land,” continued Tim Lawless.

“The trend towards a larger number of land sales over the September and June quarters of last year is very welcome, however land sales remain more than 7 per cent lower than their previous 2015 peak. With capital city transactions rising by almost 10 per cent over the September quarter compared with a 1.1 per cent rise across the combined regional markets, it is clear that demand for vacant land is most concentrated across the capital city markets where economic conditions are generally stronger,” concluded Tim Lawless.

The HIA New Homes Sales Report – a survey of Australia’s largest home builders – highlights a relatively healthy end to 2016, said the Housing Industry Association.

New detached house sales fell by 2.3 per cent in the December 2016 quarter, while the sale of multi-units grew by 3.2 per cent.

The December update for the HIA’s monthly New Home Sales survey shows growth of 0.2 per cent in total seasonally adjusted new home sales in December 2016. This result follows faster growth of 6.1 per cent in November. Multi-unit sales increased by 6.4 per cent in December 2016. Detached house sales fell by 1.6 per cent, within which there was strong gains for New South Wales and Victoria.

Seasonally adjusted new detached house sales increased in two out of five mainland states in December 2016, compared to four out of five states in November. Detached house sales increased in the month of December by 2.4 per cent in New South Wales and by 5.8 per cent in Victoria. The monthly fall in detached house sales was 9.1 per cent in Queensland, 1.9 per cent in South Australia, and 9.0 per cent in Western Australia.

“New home sales hit a two year low in October last year, but recovered well in November and December,” said HIA Chief Economist, Dr Harley Dale. “The late 2016 results were strong for the sales of ‘multi-units’, while detached house sales remained in reasonable shape.”

“The strong finish to 2016 for new home sales admittedly follows a very weak month in October,” said Harley Dale. “Obviously it is better that new home sales bounced back rather than kept falling!”

“The overall profile for both HIA New Home Sales and ABS Building Approvals is consistent with the first stage of the down cycle in new home commencements being a mild one. We expect this down cycle to begin in 2017.”

“As has been the case all cycle, new home sales (and building approvals) highlights the large differences in new home building conditions between the five mainland states,” concluded Harley Dale.

Looking at individual movements, momentum was strong, very strong across the investor categories, whilst the only category in owner occupied lending land was new dwellings. Construction for investment purposes was up around 5% on the previous month.

Looking at individual movements, momentum was strong, very strong across the investor categories, whilst the only category in owner occupied lending land was new dwellings. Construction for investment purposes was up around 5% on the previous month. Stripping out refinance, half of new lending was for investment purposes.

Stripping out refinance, half of new lending was for investment purposes. First time buyers fell 20% in the month, whilst using the DFA surveys, we detected a further rise in first time buyers going to the investment sector, up 5% in the month.

First time buyers fell 20% in the month, whilst using the DFA surveys, we detected a further rise in first time buyers going to the investment sector, up 5% in the month. Total first time buyer activity fell, highlighting the affordability issues.

Total first time buyer activity fell, highlighting the affordability issues. In original terms, total loan stock was higher, up 0.4% to $1.54 trillion.

In original terms, total loan stock was higher, up 0.4% to $1.54 trillion. Looking at the movements across lender types, we see a bigger upswing from credit unions and building societies, compared with the banks, across both owner occupied and investment loans. Perhaps as banks tighten their lending criteria, some borrowers are going to smaller lenders, as well as non-banks.

Looking at the movements across lender types, we see a bigger upswing from credit unions and building societies, compared with the banks, across both owner occupied and investment loans. Perhaps as banks tighten their lending criteria, some borrowers are going to smaller lenders, as well as non-banks. We think APRA should immediately impose a lower speed limit on investor loans but also apply other macro-prudential measures. At very least they should be imposing a counter-cyclical buffer charge on investment lending, relative to owner occupied loans, as the relative risks are significantly higher in a down turn.

We think APRA should immediately impose a lower speed limit on investor loans but also apply other macro-prudential measures. At very least they should be imposing a counter-cyclical buffer charge on investment lending, relative to owner occupied loans, as the relative risks are significantly higher in a down turn.