Last night DFA was involved in a flurry of tweets about the relationship between our rolling mortgage stress data and mortgage non-performance over time. The core questions revolved around our method of assessing mortgage stress, and the strength, or otherwise of the correlation.

We were also asked about our expectations as to when non-performing mortgage loans will more above 1% of portfolio, given the uptick in stress we are seeing at the moment.

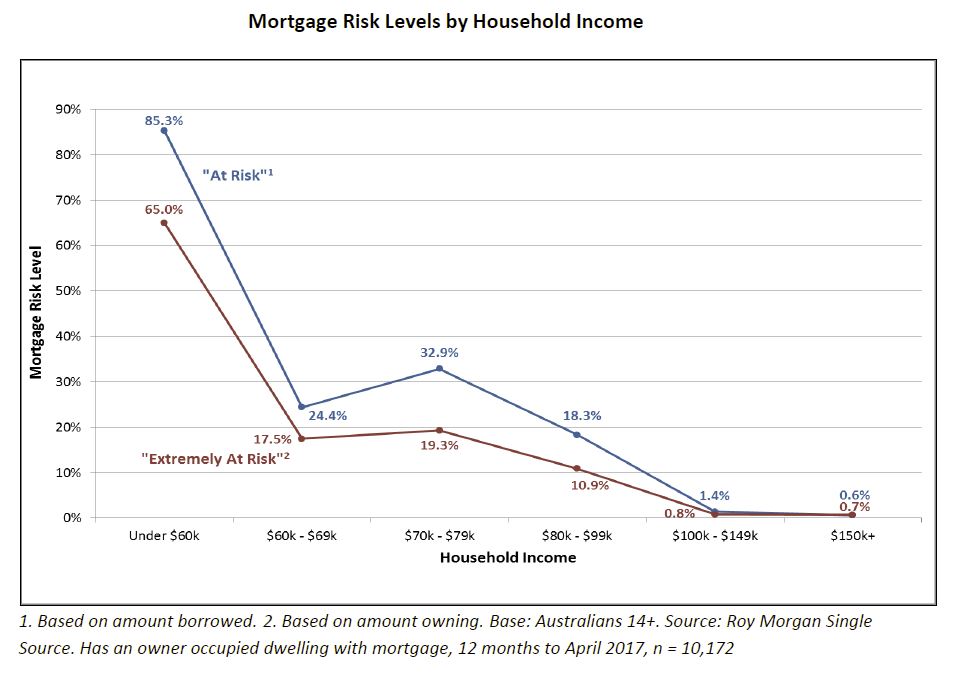

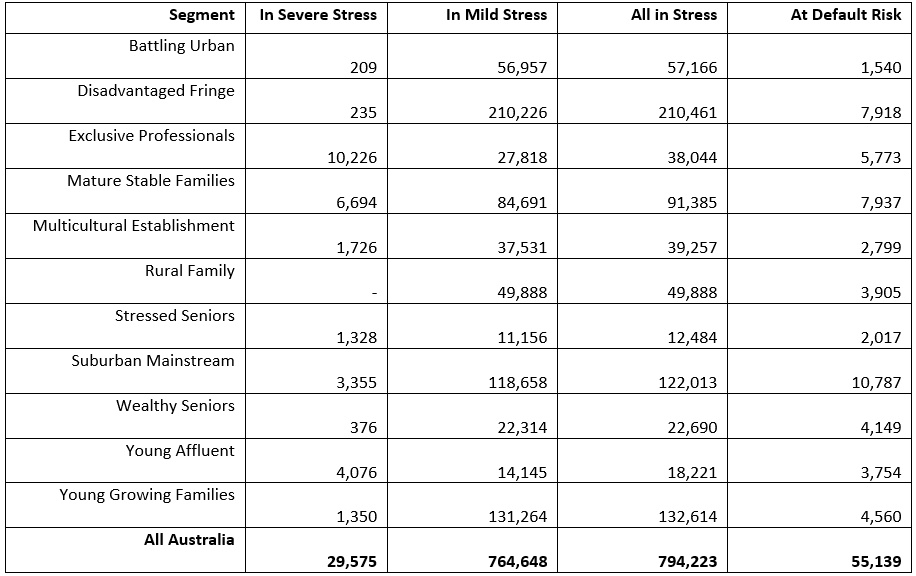

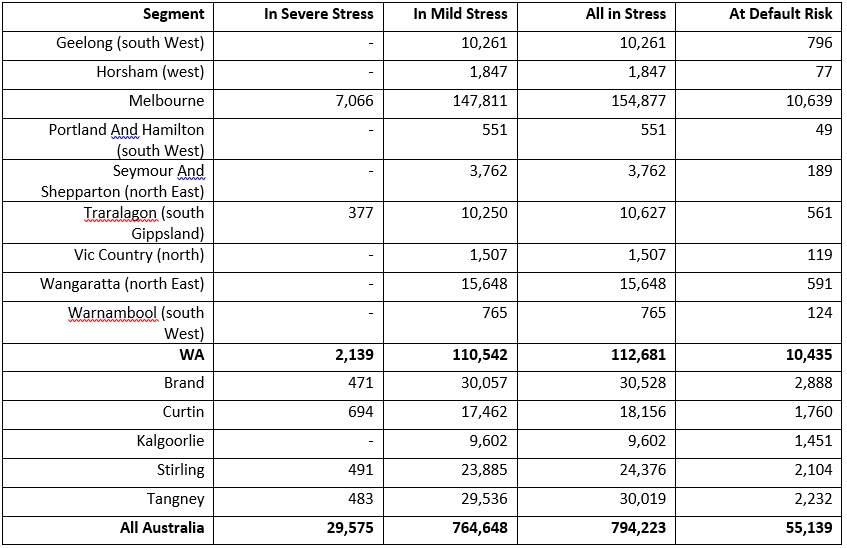

Our May 2017 data showed that across the nation, more than 794,000 households are now in mortgage stress (last month 767,000) with 30,000 of these in severe stress. This equates to 24.8% of households, up from 23.4% last month. We also estimate that nearly 55,000 households risk default in the next 12 months.

However, it got too late last night to try and explain our analysis in 140 characters. So here is more detail on our approach to mortgage stress, and importantly a chart which slows the relationship between stress data and mortgage non-performance.

Our analysis uses our core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end May 2017.

We analyse household cash flow based on real incomes, outgoings and mortgage repayments. Households are “stressed” when income does not cover ongoing costs, rather than identifying a set proportion of income, (such as 30%) going on the mortgage.

Those households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell.

We also make an estimate of predicated 30 day defaults in the year ahead (PD30) based on our stress data, and an economic overlay including expected mortgage rates, inflation, income growth and underemployment, at a post code level.

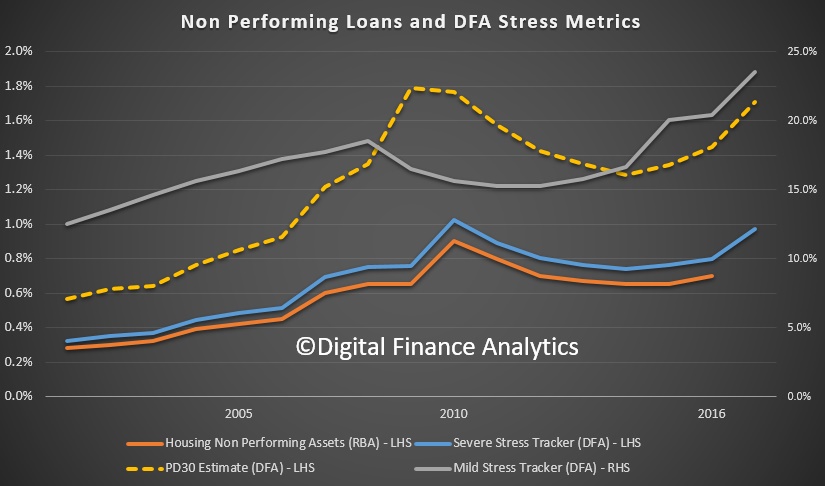

Here is the mapping between stress and non-performance of loans.

The red line is the data from the regulators on non-performing mortgage loans. In 2016 it sat around 0.7%. There was a peak following the 2007/8 financial crisis, after which interest rates and mortgage rates came down.

The red line is the data from the regulators on non-performing mortgage loans. In 2016 it sat around 0.7%. There was a peak following the 2007/8 financial crisis, after which interest rates and mortgage rates came down.

We show three additional lines on the chart. The first is our severe stress measure, the blue line, which is higher than the default rate, but follows the non-performance line quite well. The second line is the PD30 estimate, our prediction at the time of the expected level of default, in the year ahead. This is shown by the dotted yellow line, and tends to lead the actual level of defaults. Again there is a reasonable correlation.

The final line shows the mild stress household data. This is plotted on the right hand scale, and has a lower level of correlation, but nevertheless a reasonable level of shaping. After the GFC, rates cuts, plus the cash splash, helped households get out of trouble by in large, but since then the size of mortgages have grown, income in real terms is falling, living cost are rising as is underemployment. Plus mortgage rates have been rising, and the net impact in the past six months, with the RBA cash rate cut on one hand, and out of cycle rises by the banks on the other, is that mortgage repayments are higher today, than they were, for both owner occupied borrowers and investors. Interest only investors are the hardest hit.

Households are responding by cutting back on their spending, seeking to refinance and restructure their loans, and generally hunkering down. All not good for broader economic growth!

So, given the severe stress, mild stress and our PD30 estimates are all currently rising, we expect non-performing loans to rise above 1% of portfolio during 2018. Unless the RBA cuts, and the mortgage rates follow.

So, given the severe stress, mild stress and our PD30 estimates are all currently rising, we expect non-performing loans to rise above 1% of portfolio during 2018. Unless the RBA cuts, and the mortgage rates follow.