Today we start a series on the results from our latest SME surveys. We have data from our statistically representative cross sections of 26,000 businesses, from small part-time businesses up to well established firms. This data feeds our SME reports, and we are working on the next edition, though the 2015 version is still available and is available on demand. This is a top-level summary of our findings, the detailed analysis is available for our paying clients.

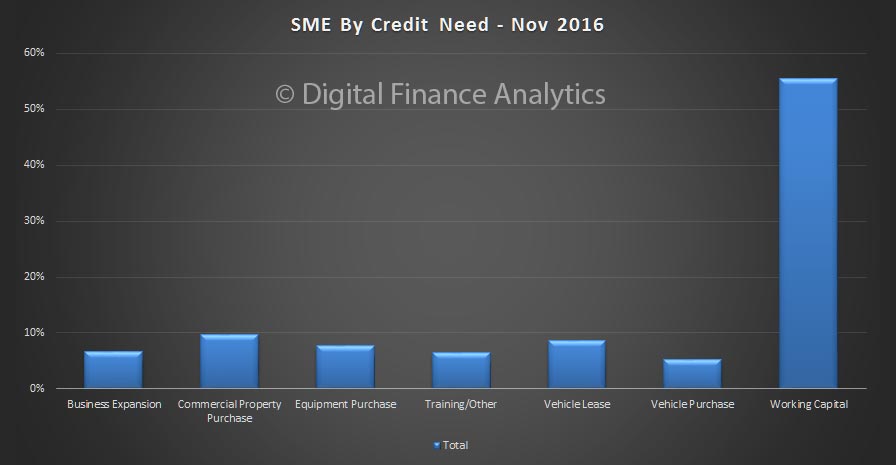

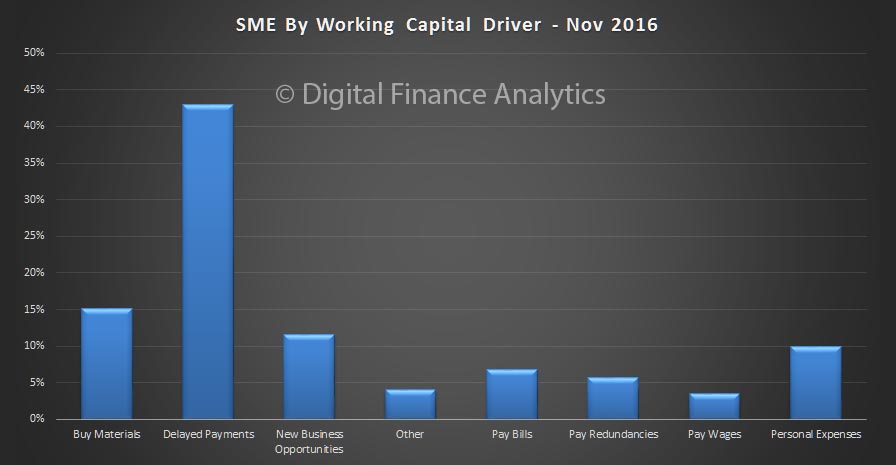

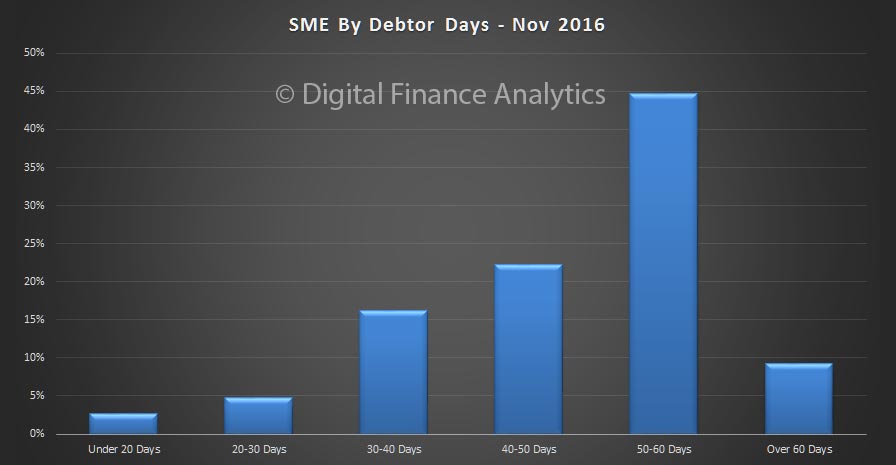

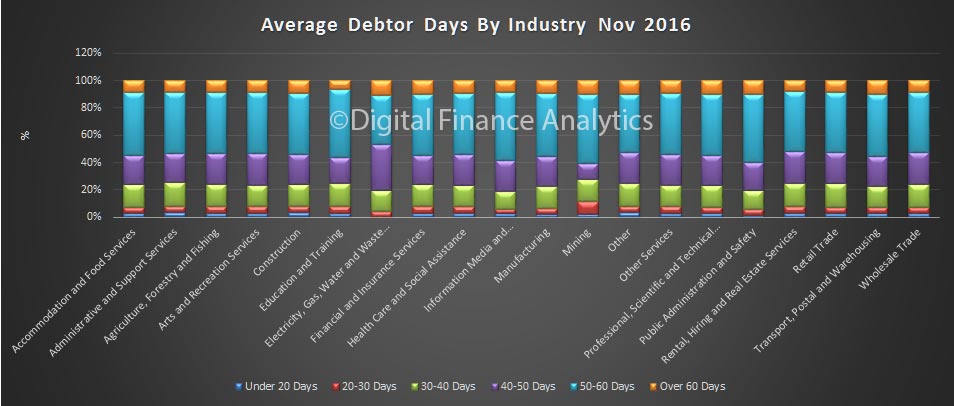

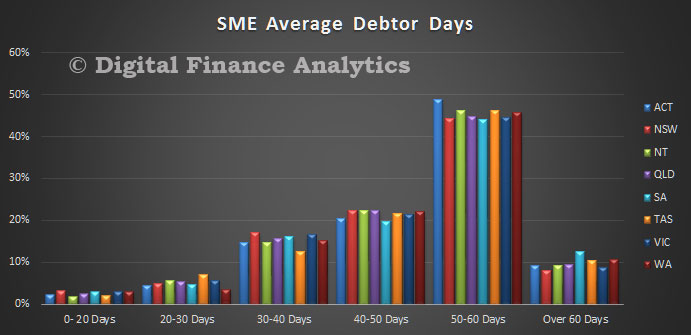

We begin today with some basic facts about the sector, before we look at their levels of confidence, use of technology, borrowing needs and propensity; and hiring plans. We find that many businesses continue to struggle with tight cash-flows and are unable or unwilling to borrow more to help grow their businesses. Debtor days are increasing for many, as larger firms, and government departments are settling their invoices on more extended terms. Switching between banks is still relatively rare.

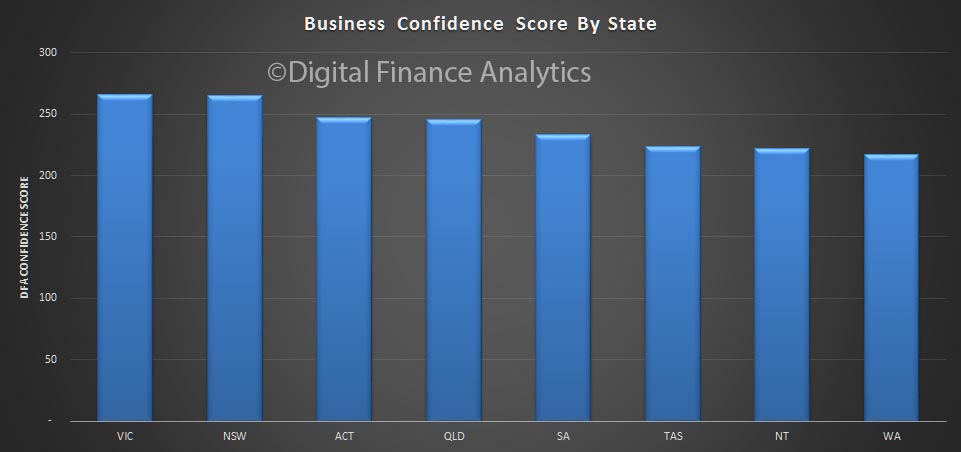

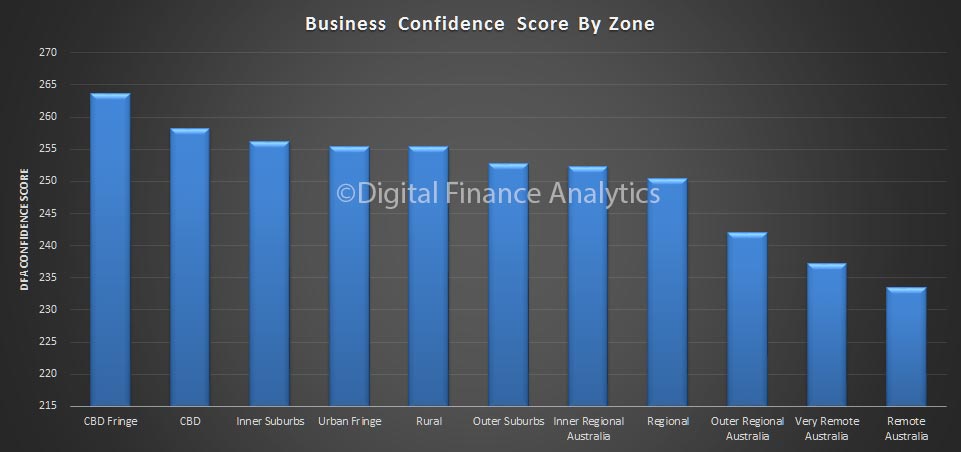

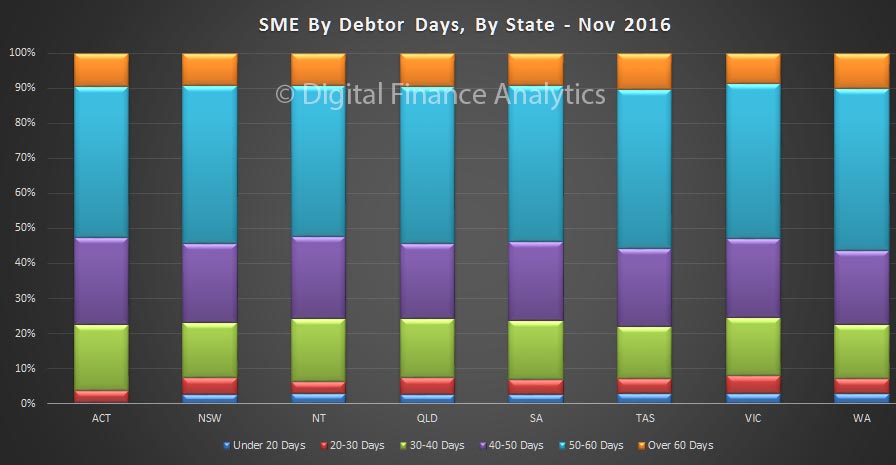

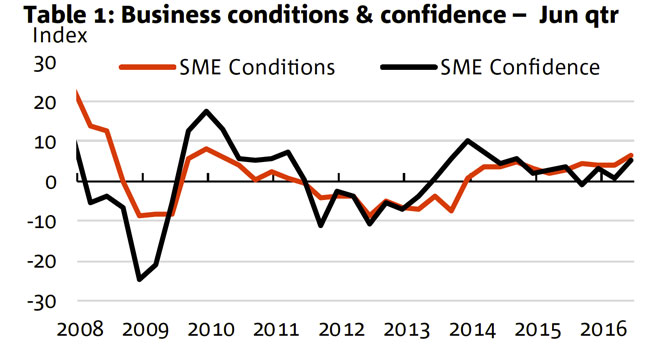

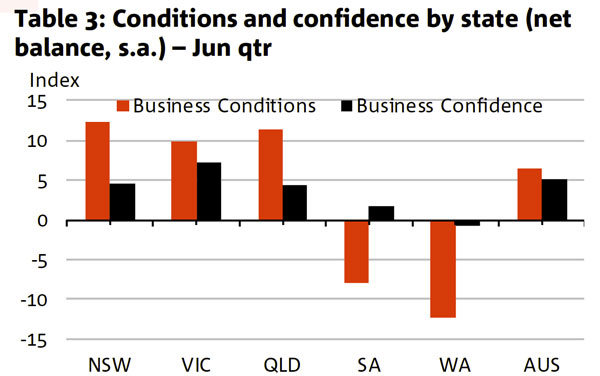

The state of SME’s are important because around 5 million households are reliant in income from them, and when they fire, they can become a significant growth engine. We will also, later, discuss the state by state variations, which are significant.

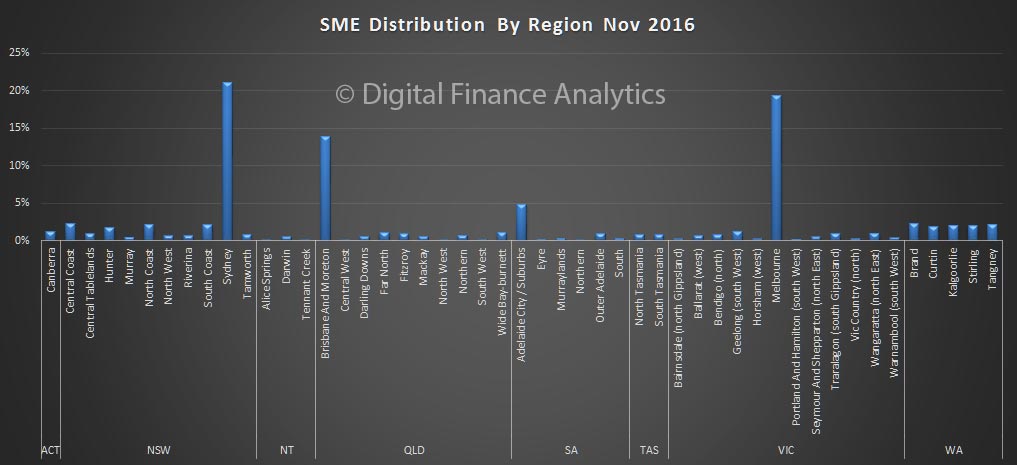

So to begin. There are more than 2.2 million small and medium businesses. Many are located in the main urban centres, but there is also a smattering across the regions as well.

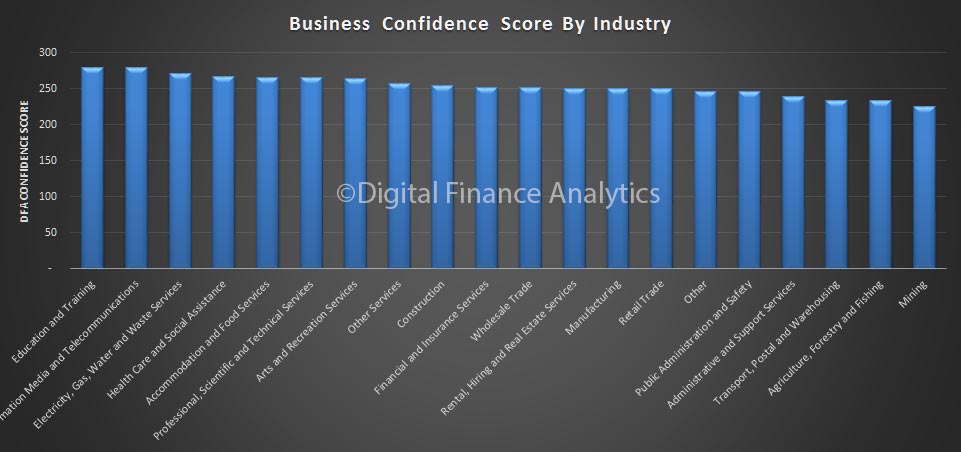

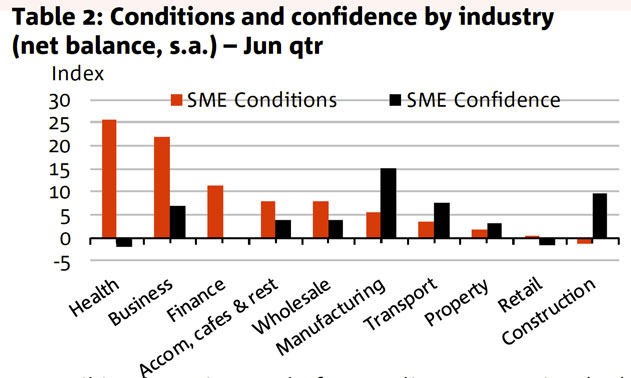

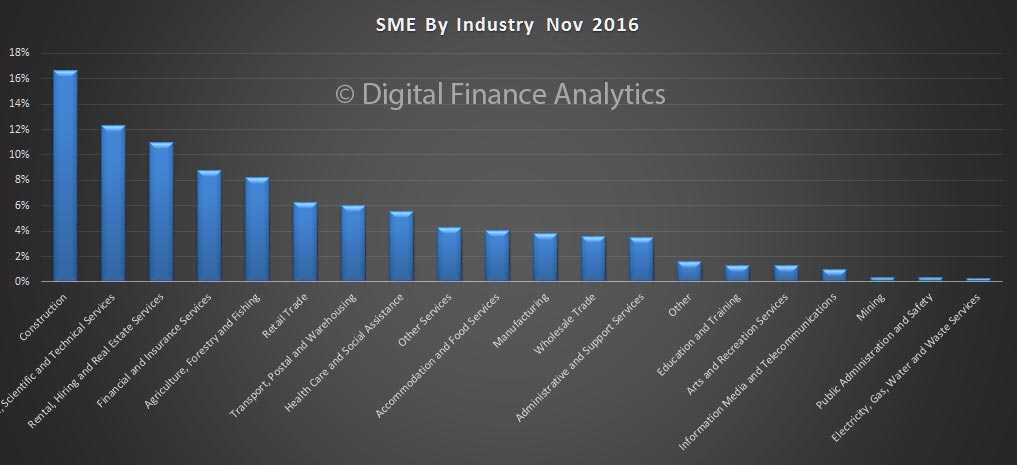

When we look across an industry classification, we see that the largest segment of the market is construction, then technical, and then real estate and rentals. Property and construction related activity provides employment to more than one third of businesses, directly or indirectly.

When we look across an industry classification, we see that the largest segment of the market is construction, then technical, and then real estate and rentals. Property and construction related activity provides employment to more than one third of businesses, directly or indirectly.

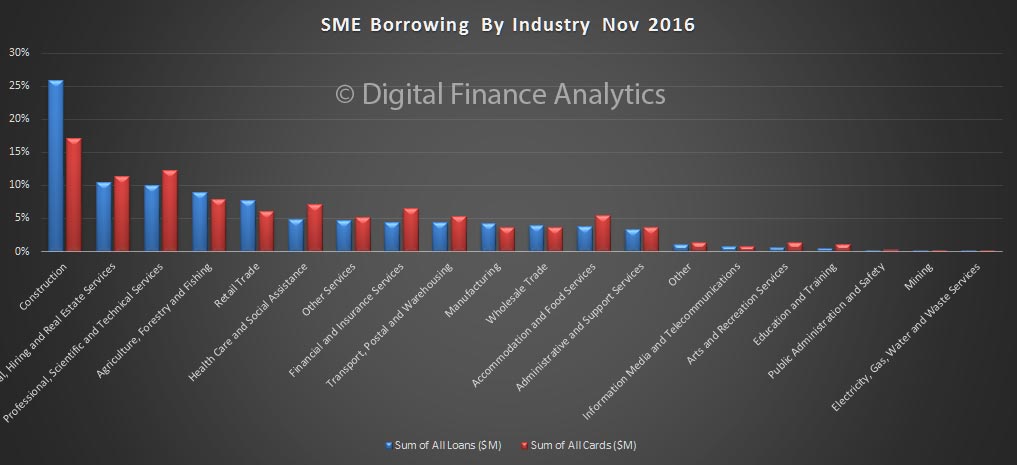

Borrowing is strongest in the construction sector, whether we look at secured and unsecured loans, or credit card debt (which may be either on a business card, or a personal credit card).

Borrowing is strongest in the construction sector, whether we look at secured and unsecured loans, or credit card debt (which may be either on a business card, or a personal credit card).

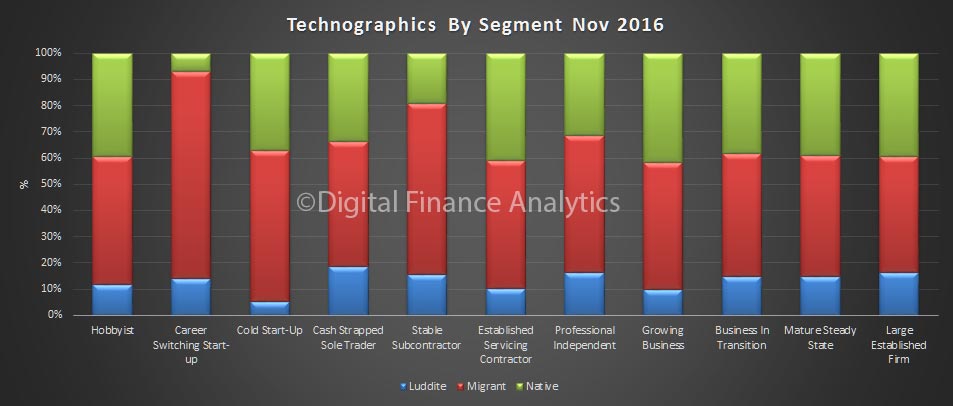

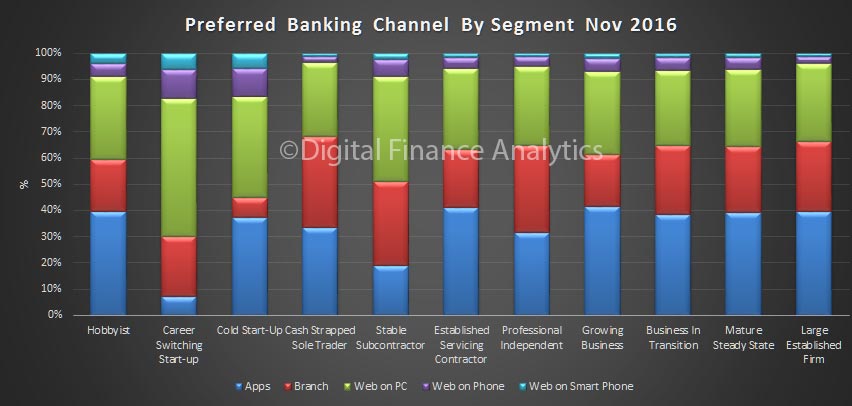

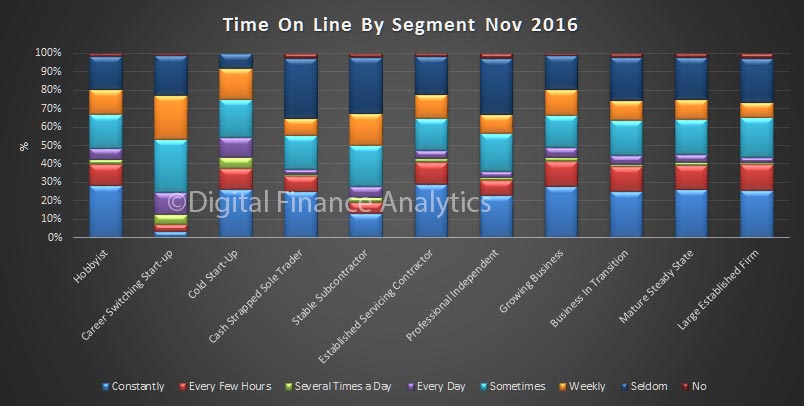

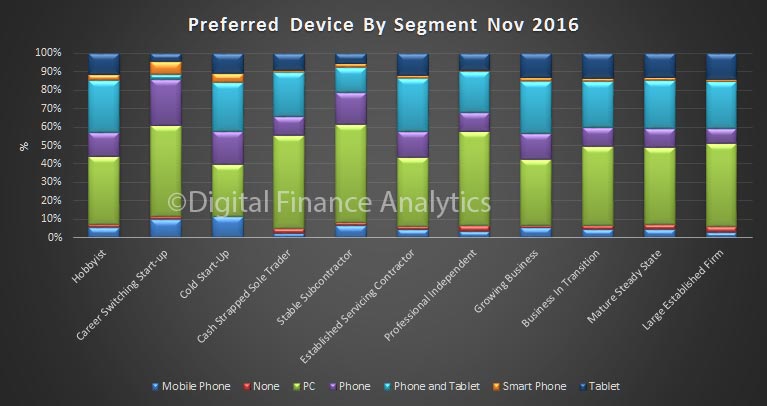

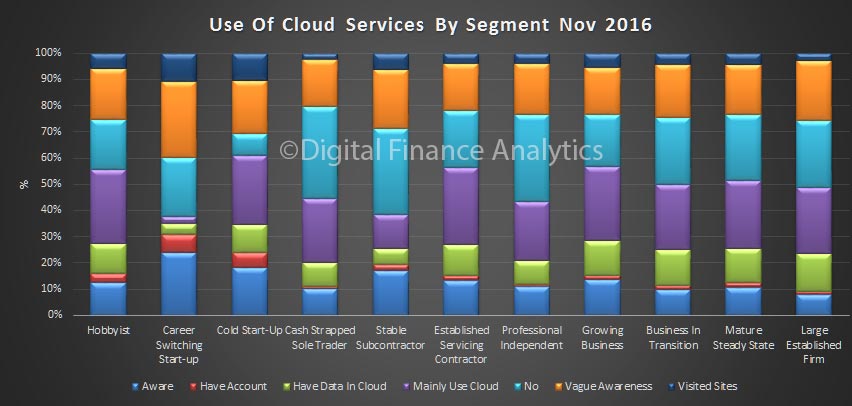

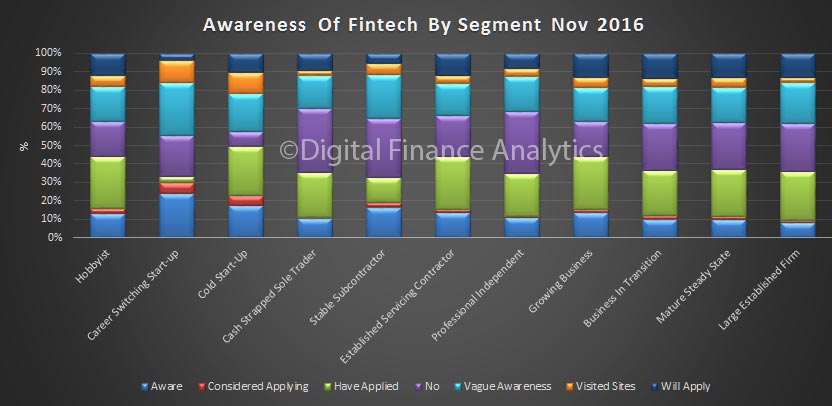

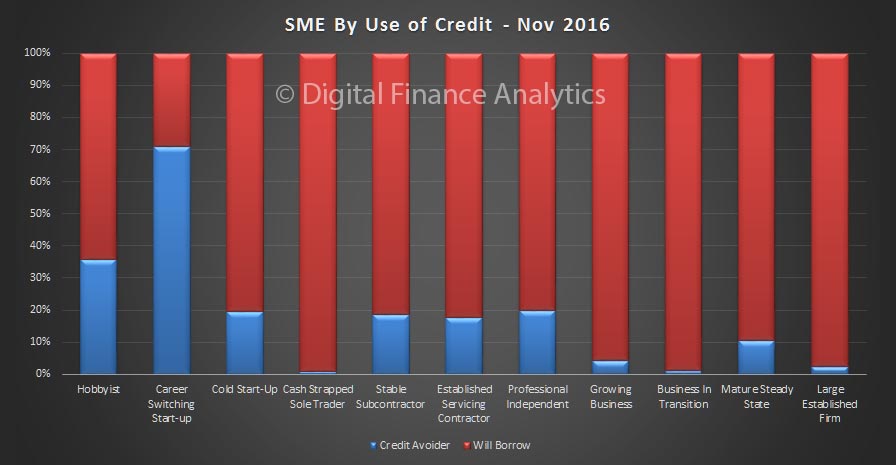

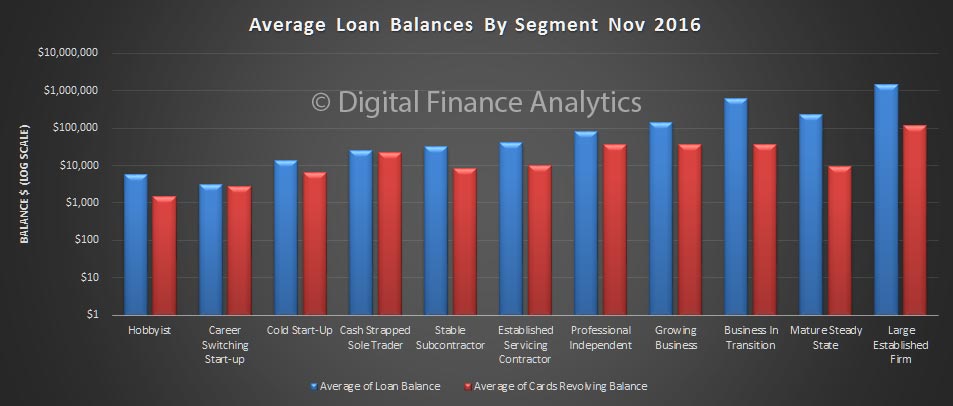

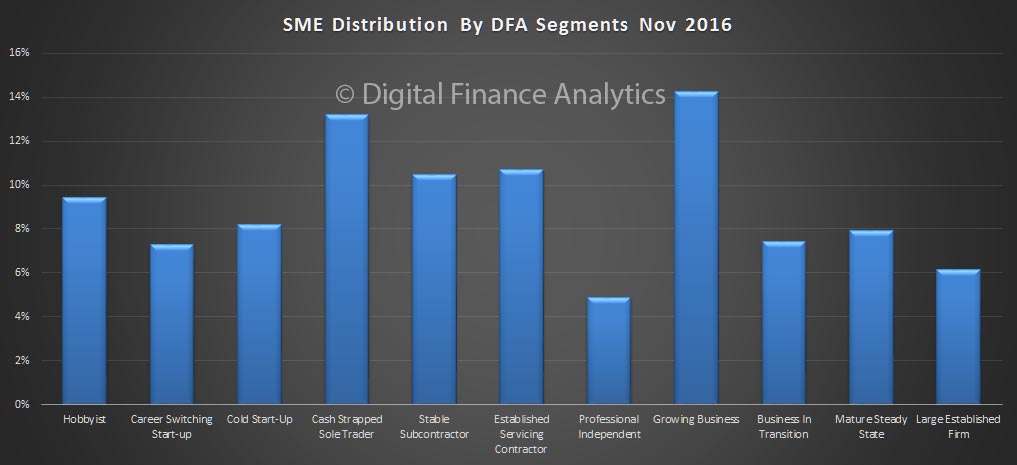

At this point we introduce our SME segmentation model. Segmentation is essential when looking at the SME sector, because the businesses are so varied. Our model takes account of a number of elements, including purpose of the business, length of time trading, history of the principle and number of employees. Here is a brief summary.

At this point we introduce our SME segmentation model. Segmentation is essential when looking at the SME sector, because the businesses are so varied. Our model takes account of a number of elements, including purpose of the business, length of time trading, history of the principle and number of employees. Here is a brief summary.

Hobbyists are running part-time businesses, for example trading on eBay, doing a few hours in the “gig” economy, or doing it just for fun.

Career Switching Start-ups are new businesses created by people who, either from choice, or redundancy have decided to start their own business.

Cold Start-ups are new businesses, starting from scratch, with limited experience and funds.

Cash-strapped Sole Traders are businesses who have been trading for some time, but are finding it difficult to maintain a balance of selling and delivering to customers. Many are in the construction sector.

Stable Contractors are businesses who have been trading for longer and are in a more stable condition. Many will be sole-traders.

Established Service Contractors are more resilient, and often employing business, with a track record, and established customer base.

Professional Independents are self-employed qualified individuals, working in a number of professions, from medicine, law, financial services to vets.

Growing Business, are on the move, seeking to expand and extend. They are mainly employing businesses.

Business in Transition are those seeking to change, from for example, sole trader to a company, or commence international trading.

Mature Steady State businesses are well established firms, where the focus is not on growth, but on keeping the business running efficiently.

Finally, Large Established Firms are those with large number of employees, a successful track record of trading, and an established brand.

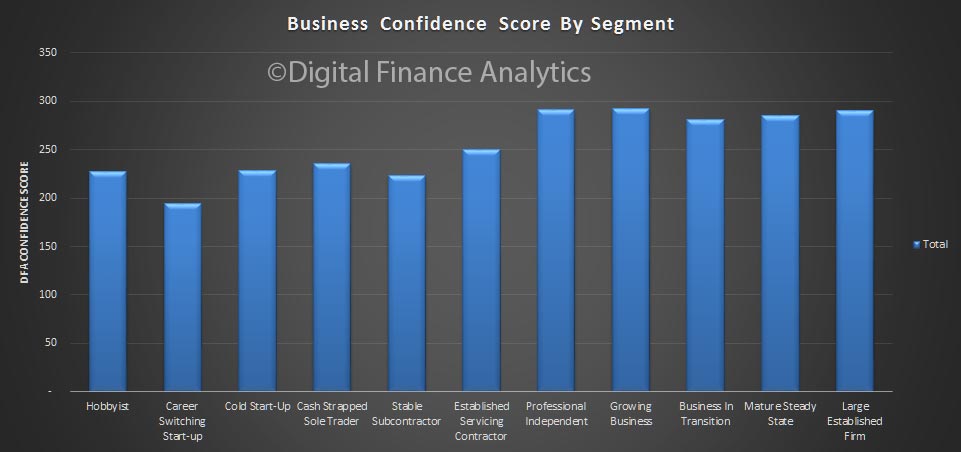

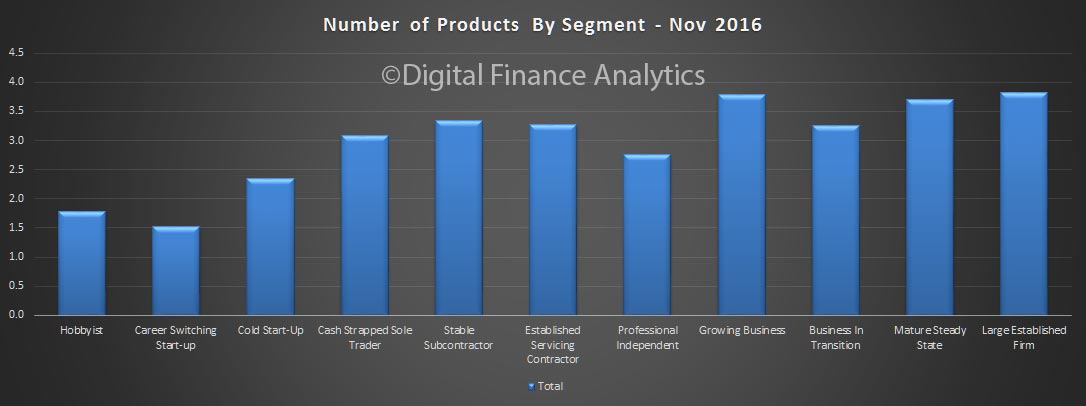

The relative distribution across these segments is shown below. This highlights the effectiveness of the segmentation.

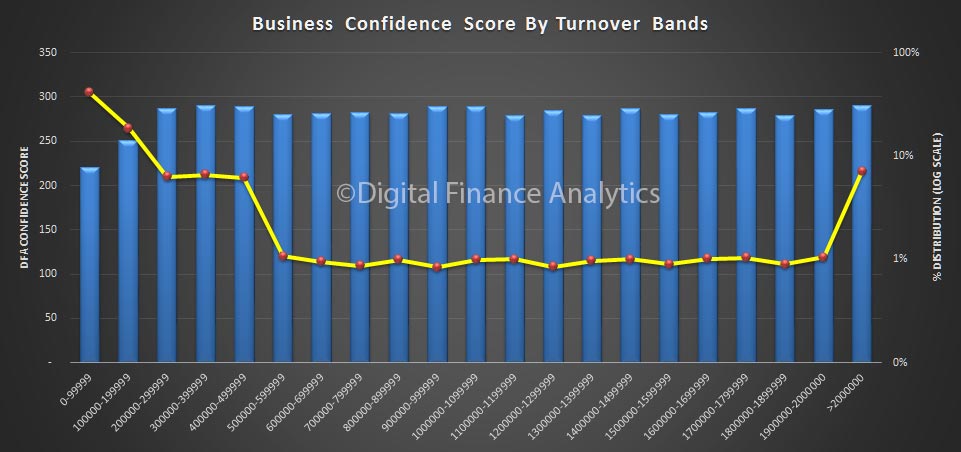

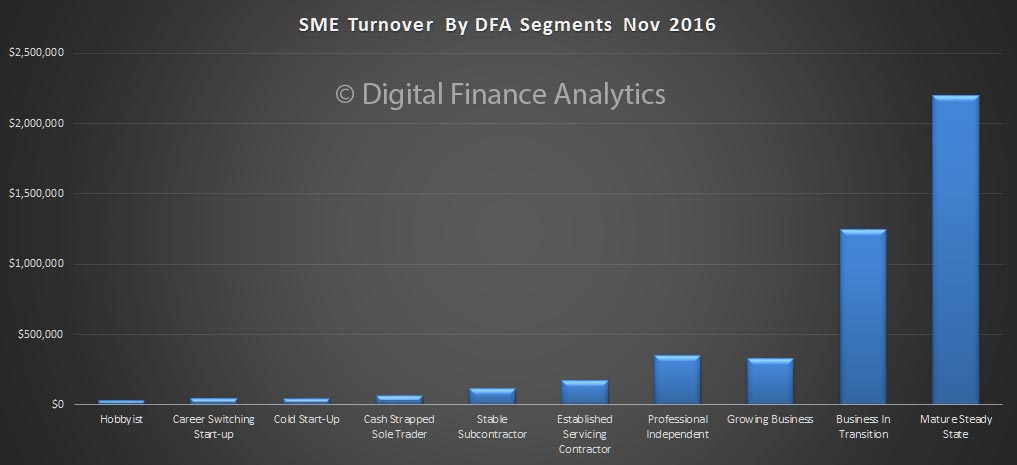

We do not use turnover as a primary segmentation element, though turnover tends to increase as we move from simple part-time businesses to more complex trading entities.

We do not use turnover as a primary segmentation element, though turnover tends to increase as we move from simple part-time businesses to more complex trading entities.

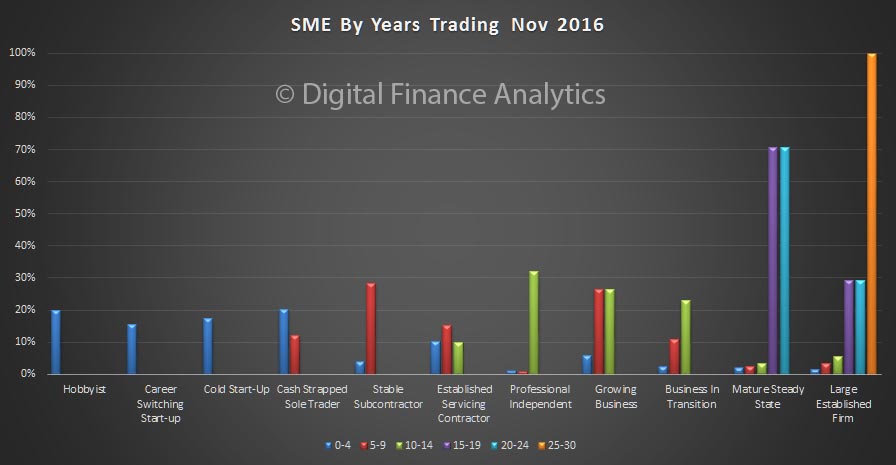

The time trading has a significant impact on the segmentation, as you might expect.

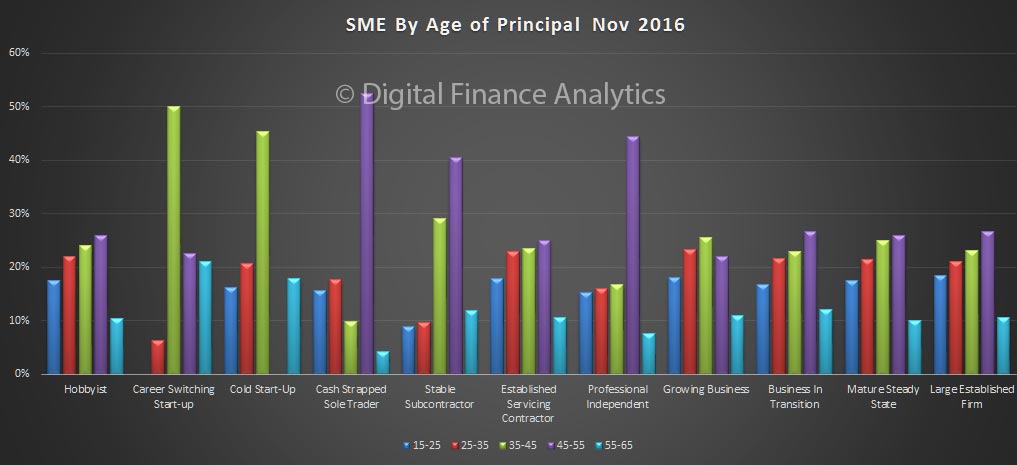

We also find the age of the principal varies across the segments.

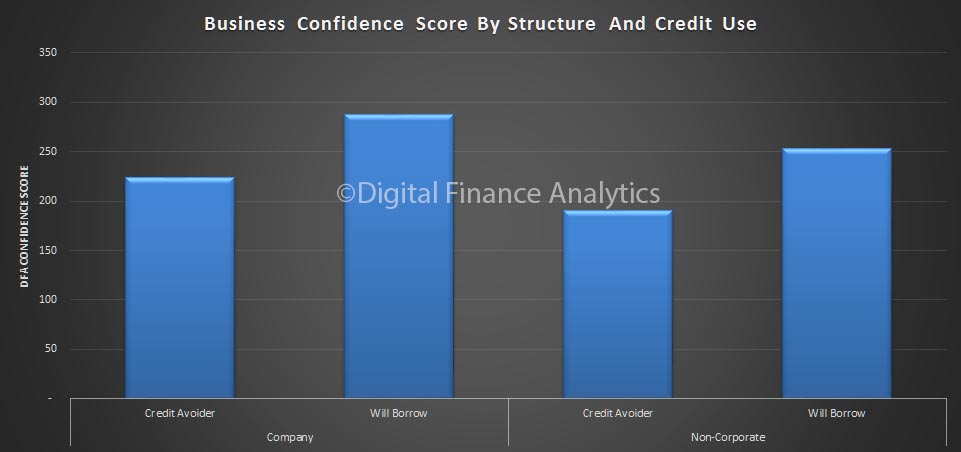

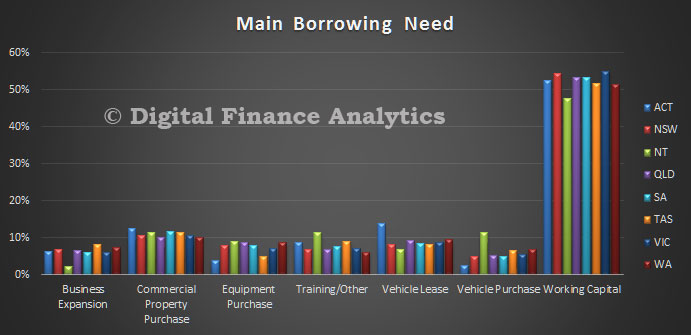

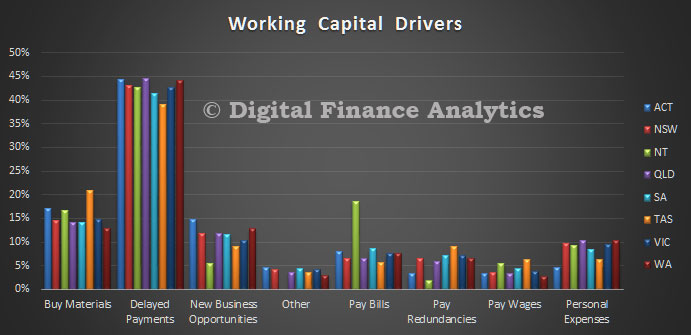

So having painted an overall picture, next time we will look at business confidence, then borrowing propensity.

So having painted an overall picture, next time we will look at business confidence, then borrowing propensity.

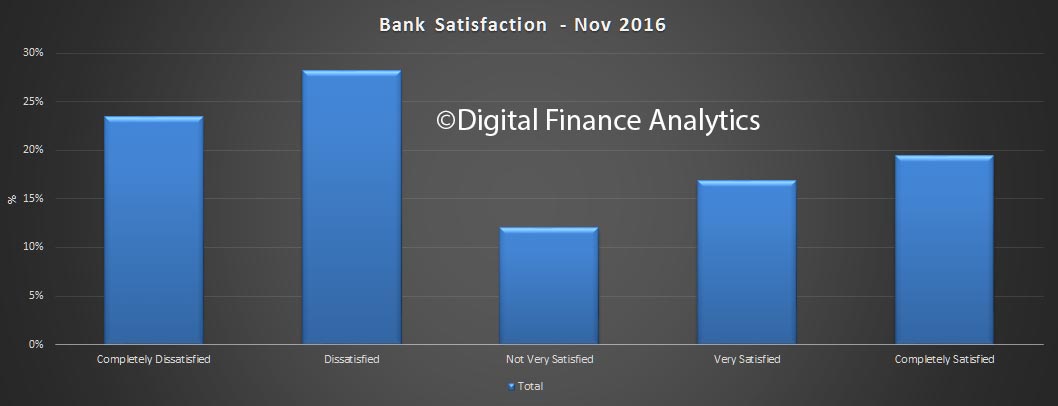

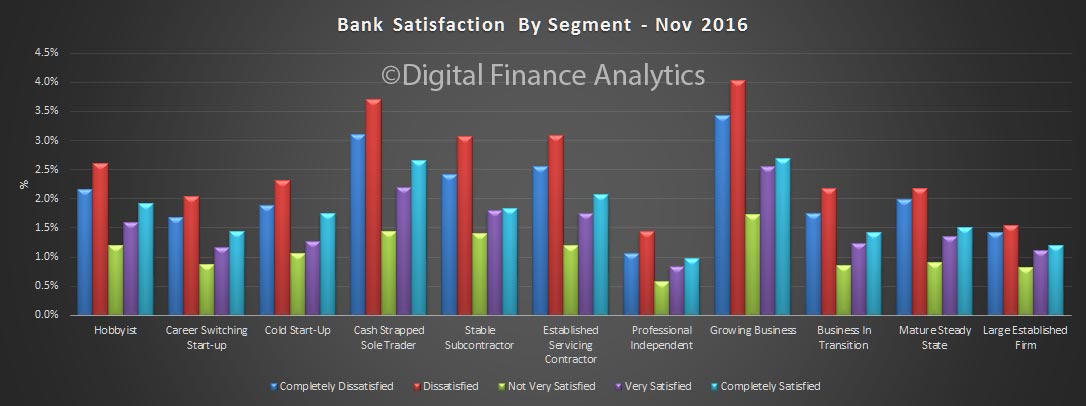

An analysis at the segment level reveals that more established, larger businesses tend to be more satisfied, whilst smaller and growing businesses are generally less satisfied. Those borrowing are less satisfied.

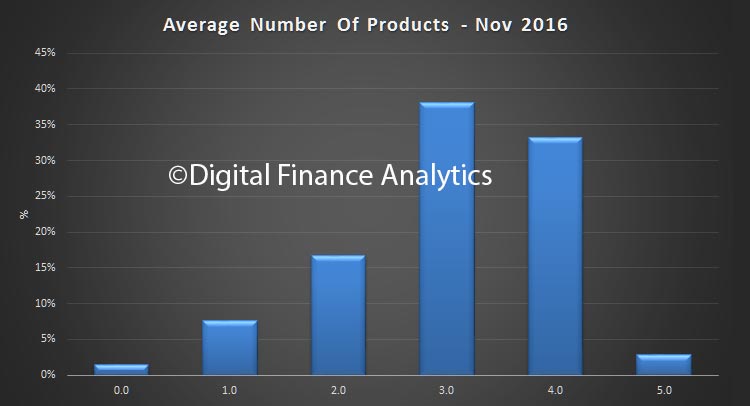

An analysis at the segment level reveals that more established, larger businesses tend to be more satisfied, whilst smaller and growing businesses are generally less satisfied. Those borrowing are less satisfied. The average number of bank products varies across the SME base.

The average number of bank products varies across the SME base. However, on a segmented basis, larger businesses tend to have a greater number of products.

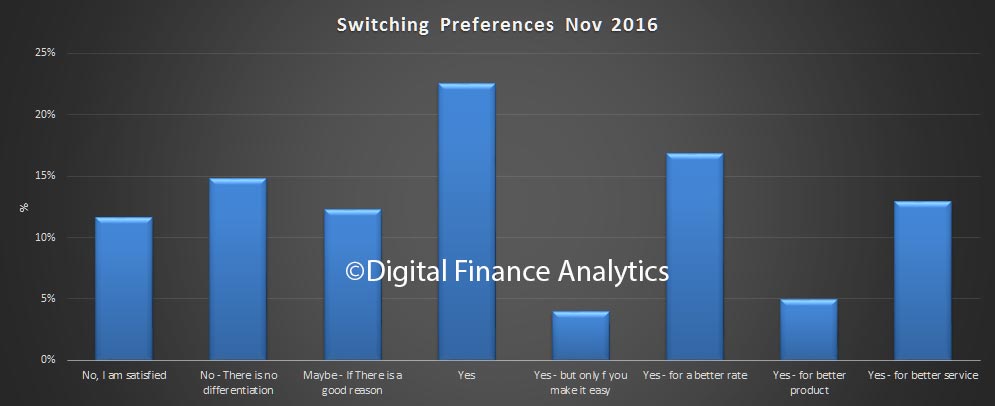

However, on a segmented basis, larger businesses tend to have a greater number of products. Around three quarters of SME’s said they would consider switching.

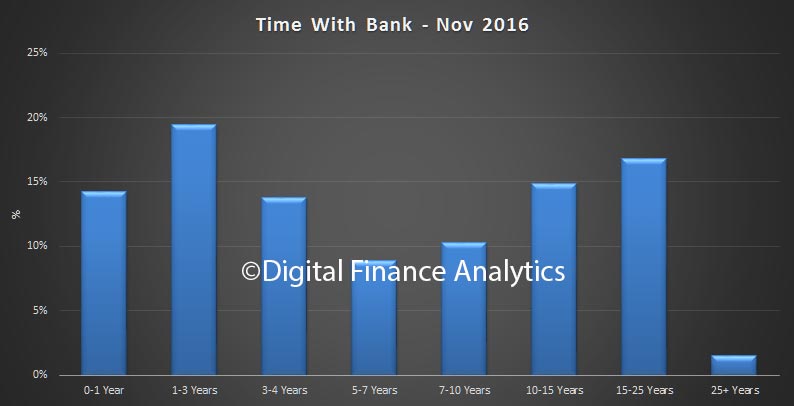

Around three quarters of SME’s said they would consider switching. However, from the time with bank data, we see that most stick with their existing relationships.

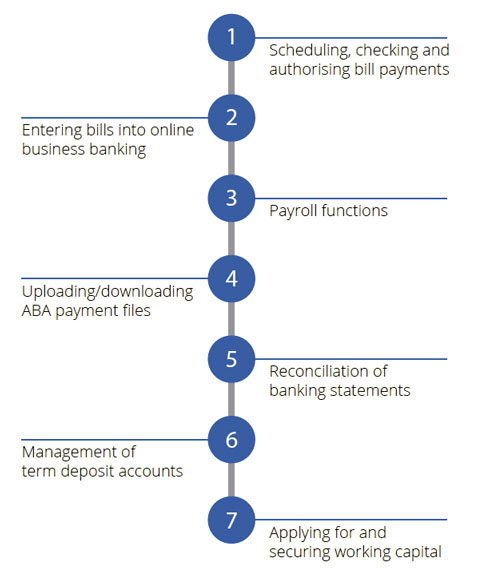

However, from the time with bank data, we see that most stick with their existing relationships. Our analysis suggests three reasons for this. First, many perceive little or no differentiation between banks, so there is no point in switching. Second, their current bank has provided facilities which make it hard to switch, including secured loans, credit cards and payrole services. Third, some have sought to switch, but have been unable to replicate the current facilities they have from their current bank.

Our analysis suggests three reasons for this. First, many perceive little or no differentiation between banks, so there is no point in switching. Second, their current bank has provided facilities which make it hard to switch, including secured loans, credit cards and payrole services. Third, some have sought to switch, but have been unable to replicate the current facilities they have from their current bank.