Malcolm Edey, RBA Assistant Governor (Financial System) spoke at the Australian Financial Review Retail Summit and discussed the changing face of payments, including the relative volume and costs of various payment methods. Cheques are well out of favour.

A good place to start is an observation that will not be lost on anyone here. That is that the nature of the payments we use is changing, and changing quite rapidly at the moment. Probably the clearest example to most people has been the take-up of contactless, or tap-and-go, card payments. These have taken off extraordinarily quickly in Australia, to the point where Australia is thought of as the leading contactless market in the world. This is a technology that offers a benefit to both consumers and merchants in terms of the time taken to process a payment, and as a result it has been embraced – but many merchants might also notice that their payments costs have risen because of the resulting change in their payments mix. This is a good example of the complex dynamics of competition in the retail payments system.

But the rise of contactless payments is only one of a range of changes that have been occurring to the payments system over time – some of which you might have noticed, some of which you have probably never thought about.

Possibly the most important trend we are seeing is the steady decline in the use of traditionally paper-based payments. Think of when was the last time you wrote or received a cheque. In 2000 the average Australian wrote around 35 cheques per year. In 2015/16 that was down to six. What is more, while cheque use has been declining for two decades, the decline if anything is accelerating; after falling by an average of about 13 per cent per year in the preceding five years, the number of cheques written fell by 17 per cent in 2015/16.

We have been observing the decline in cheques for many years, but more recently it has been a decline in the use of that other traditionally paper instrument – cash – that has been attracting attention. The only real way to adequately measure the use of cash is to survey the users – something the Reserve Bank does via a consumer diary once every three years. We ran the first of these surveys in 2007, when a large majority of consumer payments – 69 per cent – were made with cash. By 2010, that percentage had fallen to 62 per cent and by 2013, 47 per cent, with the decline occurring across all payment values. We will run the survey again this year, but it seems a safe bet that there will be a further, probably quite large, decline in cash use.

This trend is not all about people falling out of love with cash; a significant factor is the rapid rise in online commerce, where of course cash is not an option.

So what has filled the gap left by our paper instruments? In the retail space it is largely cards, which have grown by an average of 11 per cent per year over the past five years. This reflects cards’ large share in online commerce, as well as their having gained ground at the retail point of sale. Based on the Bank’s consumer survey, card payments made up 43 per cent of all consumer payments in 2013, and 55 per cent of those over 50 dollars. The ubiquity of card payments is one reason we care a lot about how those systems operate, as I will discuss more a bit later.

It is also worth noting that in the period measured by our survey, BPAY also gained an increasing share of the market, while the relative newcomer, PayPal showed strong growth from a low base.

The Cost of Payments

Of equal interest to these broader trends in payments usage is the cost of payments. The retail sector clearly has a strong interest in the cost of payments to merchants, and while the Reserve Bank is also interested in this, its principal focus when evaluating the efficiency of the payments system is the resource cost of payments – that is, how much it costs the economy in total to produce a payment – abstracting from the various fees that determine the cost to any single party or sector. Determining resource costs is a large job, requiring detailed information on financial institutions’ costs and things like the cost of processing time for merchants.

The Reserve Bank last went through this exercise in 2014. The most comforting news from that study was that the resource cost of consumer to business payments had declined as a percentage of GDP since the previous cost study in 2006, from 0.80 per cent to 0.54 per cent, even though the number of transactions had risen. Despite the favourable trend overall, the mix of payments within the total acted in the direction of increasing costs.

Looking across the main non-cash retail systems, we see that, unsurprisingly, the highest per-transaction resource costs were generated by the cheque system, with each cheque written costing the economy about $5.12, if account overheads are ignored. This is not surprising given the cost of shipping and processing physical cheques, although there have been some efficiency improvements in the cheque system since the time of the study.

Perhaps of more current interest to the retail sector is the cost of our card systems. Credit cards are quite costly at around 94 cents for the average sized transaction, while MasterCard and Visa debit are less costly and eftpos uses the fewest resources of any of the card systems, at around 45 cents per transaction.

The broad relativities between the resource costs of these systems is similar to those faced by merchants. Another way to think about that is that it is merchants who, by and large, bear the cost of payments. This is largely achieved by the way fees are used in these systems. I think the most telling illustration of that is to compare the actual costs faced by merchants to the costs faced by consumers once fees and benefits to consumers, like interest-free periods and reward points, are taken into account. What you will see is that, despite being more expensive to produce and more costly to merchants, on average a credit card transaction costs a consumer slightly less than a debit card transaction. These are the incentives that shape payment choices by consumers.

“Where consumers see a card surcharge, they should check to see what non-surcharged methods of payment are available. Before paying a surcharge, they should think about whether any benefits from using that payment method outweigh the cost of the surcharge; if not they should consider switching to an alternative payment method. This will not only save them money, it will help keep costs down for businesses and will put pressure on card schemes to keep their charges low”. This was Tony Richards, Head of Payments Policy Department RBA, conclusion when he spoke at the 26th Annual Credit Law Conference and discussed the revised card payment surcharging regime.

In his speech he started by looking at data on average merchant service fees (or MSFs) show that there are very large differences in the cost of different card systems for merchants. These costs ranged from an average of just 0.14 per cent of transaction value for eftpos in the June quarter to about 2 per cent of transaction value for Diners Club. For MasterCard and Visa transactions, the average cost to merchants of debit cards was 0.55 per cent of transaction value, while the average cost of credit card transactions was 0.81 per cent. The average cost of American Express cards was 1.66 per cent of transaction value.

But these averages mask significant variation across different merchants. Many merchants pay up to 1–1½ per cent on average for MasterCard and Visa credit card transactions. And it is not unusual for merchants to pay 2–3 per cent to receive an American Express card payment.

Then he discussed five key elements of the new framework contained in the Bank’s new surcharging standard and the Government’s amendments to the Competition and Consumer Act.

First, the new framework preserves the right of merchants to surcharge for more expensive cards, but it does not require them to do so. Under the framework, a merchant that decides to surcharge a particular type of card may not surcharge above their average cost of acceptance for that card type.

For example, if on average it costs a merchant 1 per cent of the value of a transaction to receive a Visa credit card payment, the merchant may apply a surcharge of up to 1 per cent for that type of card. The merchant would not, however, be able to apply the same 1 per cent surcharge if the customer chose instead to pay with a debit card that was less costly to the merchant.

Second, the definition of card acceptance costs that can be included in a card surcharge has been narrowed. Acceptable costs will be limited to fees paid to the merchant’s card acquirer (or other payments facilitator) and a limited number of other documented costs paid to third parties for services directly related to accepting the particular type of card. A merchant’s internal costs cannot be included in a surcharge.

Third, a merchant that wishes to surcharge will typically have to do so in percentage terms rather than as a fixed-dollar amount. In the airline industry, this means that surcharges on lower-value airfares have been reduced significantly.

Fourth, the Government has given the ACCC investigation and enforcement powers over cases of possible excessive surcharging.

The Bank’s standard and the ACCC’s enforcement powers apply to payment surcharges in six card systems that have been designated by the Reserve Bank – eftpos, the MasterCard debit and credit systems, Visa’s debit and credit systems, and the American Express companion card system. However, Reserve Bank staff have been in discussions with other card systems that have not been designated and we expect that those systems will all be including conditions in their merchant agreements that are similar to the limits on surcharges under the Bank’s standard. This will mean that merchants that wish to surcharge on payments in these other systems will be contractually bound to similar surcharging caps to those that apply to the regulated systems.

Fifth, surcharging in the taxi industry – which is subject to significant regulation in many other aspects – will remain the responsibility of state taxi regulators. Until recently, surcharges of 10 per cent were typical in that industry. However, authorities in five of the eight states and territories have now taken decisions to limit surcharges to no more than 5 per cent. As new payment methods and technologies emerge, the Bank expects that it will be appropriate for caps on surcharges to be reduced below 5 per cent. The Government and the Bank will continue to monitor developments in the taxi industry with a view to assessing whether further measures are appropriate.

The first stage of implementation of the surcharging reforms took effect on 1 September and covers surcharging of card payments by large merchants. Merchants are defined as large if they meet certain tests in terms of their consolidated turnover, balance-sheet size or number of employees. The framework will take effect for other, smaller merchants in September 2017.

There are a few reasons for the delayed implementation for smaller merchants. Most importantly, these merchants are less likely to have a detailed understanding of their payment costs. Since the new framework involves enforcement by the ACCC, the Bank considered it important to ensure that such merchants have simple, easy-to-understand monthly and annual statements that show their average payment costs for each of the card systems subject to the Bank’s standard. Accordingly, as part of the new regulatory framework, acquirers and other payment providers must provide merchants with such statements by mid 2017. All merchants will be required to comply with the new surcharging framework from September 2017 and ACCC enforcement will apply also to smaller merchants from that point.

Given the new framework has only been effective for two weeks, it is too early to be definitive about how the new surcharging regime applying to large merchants has affected the surcharging behaviour of those merchants. However, based on some corporate announcements and an initial survey of some websites, I think it is possible to make six initial observations.

First, and most prominently, the major domestic airlines have moved away from fixed-dollar surcharges to percentage-based surcharging. This will result in a very significant reduction in surcharges payable on lower-value airfares. The two full-service airlines have introduced surcharges for on-line payments of 1.3 per cent for credit cards and 0.6 per cent for debit cards. A passenger wishing to pay for a $100 domestic airfare by card will now pay a surcharge of $1.30 or 60 cents, as opposed to a surcharge of up to $7-8 previously. Surcharges on some high-value airfares may rise with the shift to percentage-based surcharges. However, the airlines have implemented caps on surcharges of $11 for domestic fares and $70 for international fares, indicating that they continue to prefer to not pass on their full payment costs on purchases of more expensive tickets.

Second, there does not appear to have been any increase in the prevalence of surcharging. It remains the case that companies that face relatively low merchant service fees are tending not to surcharge, while those businesses which receive a high proportion of expensive cards are more likely to surcharge.

Third, the surcharge rates for credit cards that have been announced show significant variation, which is consistent with other evidence that there is a lot of variation in the merchant service fees faced by different businesses. In the case of the Qantas group, for example, Qantas is charging a credit card surcharge of 1.3 per cent while Jetstar – which presumably receives fewer high-cost cards – is charging a surcharge of 1.06 per cent.

Fourth, as required by the Australian Consumer Law, merchants that have announced changes to their surcharges are continuing to offer non-surcharged means of payment. In the face-to-face environment, this typically includes cash, eftpos and sometimes MasterCard and Visa debit cards. In the on-line environment, it typically includes payments via BPAY, POLi or direct debit, which are typically low-cost for merchants.

Fifth, while there are still many instances of ‘blended’ credit card surcharges, there are some early signs of greater discrimination in surcharges. Blending refers to the practice of charging the same surcharge across a number of systems regardless of their cost – say across the MasterCard, Visa and American Express credit systems.

The new framework allows merchants to set the same surcharge for a number of different payment systems, provided that the surcharge is no greater than the average cost of acceptance of the lowest-cost of those systems. For example, if a merchant accepts cards from two credit card systems, which have average costs of acceptance of 1 per cent and 1.5 per cent, it can set separate surcharges of up to 1 per cent and 1.5 per cent, respectively. If it wishes to set a single surcharge, it cannot average the costs and set a 1.25 per cent surcharge for both systems, since it would be surcharging one of those systems excessively. In this example, the maximum common surcharge that could be charged would be 1 per cent.

While I think we are already seeing some reduction in the practice of blended surcharging, it is likely that we will see this trend continue from mid 2017 when new rules on the interchange fees exchanged between banks for card transactions take effect. Without wishing to go into details, the Bank will for the first time be placing a cap on the maximum interchange fee that can be paid on any card transaction. This will significantly reduce the cost of MasterCard and Visa payments for those merchants which currently receive a high proportion of high-interchange cards.

The sixth change has been in the event ticketing industry, where it was previously very difficult to avoid a card surcharge in the on-line environment. Given this, the ACCC had already required the major ticketing companies to show their surcharges as a separate component within their headline, up-front pricing. Effective 1 September, the two major companies have now removed their card surcharges and are now quoting a simple, single price for all payment methods.

According to Computerworld, Financial institutions that fail to make their APIs openly available are “doomed”, says Visa’s ANZ head of product Rob Walls.

“Anyone that stands still in the current environment of technology change is doomed. We have to continue to evolve – because consumers are expecting it,” he said.

In February, the payments giant published more than 40 APIs “for every payment need” on its Visa Developer platform. The web portal also provides access to sandboxes, documentation and test data.

“We came to the view that there isn’t a single entity that can own all of the innovation in payments,” Walls said. “We’ve been operating as a payment network for almost 60 years. Previously our network was fairly closed, only those who were financial institutions or merchants or tech companies, that were authorised to access it, were able to engage with us.

“Over the past couple of years we’ve seen disruption in many industries, we’ve seen organisations change the way they’re using technology. With with millions of developers around the world today, which is forecast to grow, the value really is going to come from co-creation.”

Walls said that there were around 140 services within Visa that could be made available and there was a push internally to post more.

“There’s now a bit of internal competition around how quickly can I get my product or service into the API set. You want more people using it.”

APIs already published were selected based on client demand and the ease at which they could be securely extracted and made available for external consumption, Walls said.

Australian financial bodies have been cautious in making APIs openly available, citing cost and security concerns.

“If Australia does not mandate an Open Financial Data model that is in line with global standards, or leaves banks to implement Open Banking APIs at their own pace, we will deny consumers the benefits of greater competition and improved financial services, and risk our banks becoming less agile and less competitive than their international peers,” the peak body wrote.

European regulation – the Payment Services Directive (PSD2) – requires that EU banks make it easier to share customer transaction and account data with third-party providers. Last year the UK government established the Open Banking Working Group with a remit to design a framework for an open API standard.

Open minds

Financial institutions were increasingly coming round to the potential of sharing APIs and drawing on the developer community, Walls said.

ANZ bank has made a limited number available via its Developer Hub and CIO Scott Collary announced in July that: “We want to be a more open bank”. NAB ran a hackathon at the end of last year, with monitored access to a number of its APIs.

“I think what’s really driving it is the fear of disruption. But that language is changing amongst financial institutions in Australia. Instead of being disrupted how can we work with the disruptors to improve the overall service?” Walls said

“The banks and Visa are of the view that innovation is able to come from anywhere and if it’s able to be integrated into my business in a fast, simple, viable way – then I don’t necessarily have to build it.”

Later this month, Aussie and Kiwi start-ups will pitch business ideas that make use of Visa services in a competition, ‘The Everywhere Initiative’.

Successful startups that can develop innovative applications using Visa APIs ‘to solve business challenges and bring new ideas to payments’ in three categories stand to win cash prizes and the chance to run a pilot with Visa.

ASIC says Westpac Banking Corporation (Westpac) has recently refunded approximately $20 million to around 820,000 customers for not clearly disclosing the types of credit card transactions that attract foreign transaction fees.

Following a customer complaint, Westpac notified ASIC that customers may have been incorrectly charged foreign transaction fees for Australian dollar transactions processed by overseas merchants. Because Westpac’s terms and conditions did not clearly state that foreign transaction fees would be charged for such Australian dollar transactions, Westpac commenced a process to identify impacted customers and provide refunds with interest.

Westpac has updated its disclosure to clarify that Australian dollar transactions – when they are processed by overseas merchants – will also attract a foreign transaction fee.

ASIC Deputy Chairman Peter Kell said, ‘It is essential for consumers to know when fees will be charged, so that they can make an informed decision when using financial products and services.’

ASIC acknowledges the cooperative approach taken by Westpac in its handling of this matter, and its appropriate reporting of the matter to ASIC.

ASIC warning to consumers

ASIC is also issuing a warning to consumers about unanticipated credit card foreign transaction fees.

It may come as a surprise to consumers that transactions made in Australian dollars with overseas merchants, or processed by a business outside Australia, can attract a foreign transaction fee. This may even occur where the merchant’s website has an Australian address (domain name) or where a foreign business advertises and invoices prices in Australian dollars.

‘It may not always be clear to the consumer that the merchant or entity is located outside Australia, particularly in an online environment where the website uses an Australian domain name,’ said ASIC Deputy Chairman Peter Kell. ‘We urge consumers to check whether the transaction they make is with an overseas-based merchant or processed outside Australia, especially when they shop online.

‘Equally, credit card issuers need to ensure that the disclosure of such fees is clear so customers understand the fees that they are charged when using their cards.’

‘Not all cards impose foreign transaction fees. For consumers who make frequent overseas purchases, it is worth shopping around for a card that offers no foreign transaction fees,’ he said.

ASIC is working with other industry participants on this issue, including by requiring improved disclosure by a number of credit card issuers.

Overseas merchants who display prices to Australian consumers in Australian dollars will usually give consumers the choice to pay in the applicable foreign currency or in the Australian dollar equivalent, as converted by the merchant at their own exchange rate (using a process known as ‘dynamic currency conversion’). As consumers may be unable to avoid paying international transaction fees for Australian dollar transactions with overseas merchants, consumers may wish to pay in the applicable foreign currency if they expect the exchange rate to be applied by their card issuer to be more competitive than the exchange rate used by the merchant.

Customers with queries or concerns about the charging of credit card foreign transaction fees should contact their credit card issuer. ASIC has published specific information and guidance for consumers about the charging of international transaction fees by credit card issuers on its MoneySmart website.

Background

A foreign transaction fee (also known as an international transaction fee) is a fee charged by many credit card providers for transactions – including purchases and cash advances:

that are converted from a foreign currency to the Australian dollar; or

that are made in Australian dollars with merchants and financial institutions located overseas; or

that are made in Australian dollars (or other currencies) that are processed outside Australia.

A foreign transaction fee is generally calculated as a percentage of the Australian dollar value of the transaction (typically up to 3.5%). Credit card schemes (such as Visa, MasterCard and American Express) have different rules about foreign transaction fees and the percentage fees will vary depending on the card scheme.

Debit cards may also attract a foreign transaction fee, and consumers are encouraged to check the terms and conditions to find out whether this fee will be imposed by debit card issuers.

From March 2014, Westpac’s credit card terms and conditions did not clearly state that a ‘foreign transaction fee’ would be charged for transactions:

for ‘card-not-present’ transactions in Australian dollars with merchants located overseas;

in Australian dollars with financial institutions located overseas; or

in Australian dollars (or any other currency) that is processed by an entity outside Australia (together referred to as Overseas Transactions in Australian Dollars).

This may have led customers to believe that a foreign transaction fee would be charged only when a transaction was made in a foreign currency that required a conversion into Australian dollars at the time of the transaction.

Affected customers have been provided compensation, including:

a refund of the foreign transaction fee charged on the transaction;

where any credit card interest was charged on the foreign transaction fee amount, a refund of the interest component; and

an additional interest payment on the refund amount from the date the foreign transaction fee was charged until the date of refund.

The company formed by the payments industry to build and operate the New Payments Platform, NPP Australia Limited, has a new CEO, with the commencement today of Adrian Lovney as its inaugural Chief Executive Officer.

The New Payments Platform is a major industry initiative to develop new national infrastructure for fast, flexible, data rich payments in Australia. The Program proceeded to the fourth phase, “build and internal test” in August 2015. The NPP is on track to being operational in the second half of 2017.

The Program reached a historic milestone in December 2014 when 12 leading authorised deposit-taking institutions (ADIs) committed funding for the build and operation of the NPP. These institutions became the founding members of NPP Australia Limited.

NPP Australia also signed a 12-year contract with global provider of secure financial messaging services Society for Worldwide Interbank Financial Telecommunication (SWIFT) to design, build and operate the basic infrastructure. The establishment of NPP Australia and the appointment of SWIFT marked the launch of the Program’s “design and elaborate” stage, which was then successfully completed in July 2015. The current “build and internal test” stage is scheduled for completion in early-mid 2017.

In October 2015, NPP Australia reached agreement with Australia’s premier bill payment system provider -BPAY – to deliver the first overlay service to use the NPP once it is operational in the second half of 2017.

The NPP will be open access infrastructure for Australian payments. The intention is that all ADIs will connect to the NPP, either directly or indirectly through another member, so they can process a wide variety of fast data-rich payments for their account holders. ADIs can choose to join the NPP at any point in its development and operation.

Core members are Australia and New Zealand Banking Group Limited, Australian Settlements Limited, Bendigo and Adelaide Bank Limited, Citigroup Pty Ltd, Commonwealth Bank of Australia, Cuscal Limited, HSBC Bank Australia Limited, Indue Ltd, ING DIRECT, Macquarie Bank Limited, National Australia Bank Limited, Reserve Bank of Australia and Westpac Banking Corporation.

NPP Australia Chairman Paul Lahiff said in June, “Adrian is an energetic leader with a passion for leading large-scale transition programs and is well-equipped to head up the commercialisation of the NPP.”

“Adrian emerged as the outstanding candidate from an extensive domestic and global search process and the NPPA Board is delighted to have secured his services,” Mr Lahiff said.

Mr Lovney was the General Manager of Product & Service at Cuscal Ltd with responsibility for product, services, and customers across the business, including leading the organisation’s work in NPP. Previously, he was Cuscal’s General Manager Strategy & Communications, responsible for leading the evolution of Cuscal’s business over the last five years as well as the successful migration and transition of customers to a new and innovative payments platform.

Mr Lovney said in June , “I am honoured to be taking on this important role at this critical stage in the development of Australia’s New Payments Platform. The NPP is a uniquely Australian take on the real time payments infrastructure being implemented overseas. Its layered business architecture will deliver scale and efficiency, while supporting a diverse range of fast payments well into the future.

“These are exciting times and I am thrilled to be able to work with the NPP Australia Board and shareholders of NPP to help them realise the benefits of the investment they have made in this new payments system for Australia,” Mr Lovney said.

Small to medium enterprises (SME) are increasingly relying on commercial credit cards to finance their operations, because payment terms for the businesses they supply are stretching out. But if the Reserve Bank of Australia (RBA) goes ahead with plans to include commercial cards in the new caps on interchange fees, SMEs will be even more hard pressed to make ends meet.

These interchange fees are a major component of the Merchant Service Fees that all Merchants pay on accepting payment cards. Commercial cards are however operated on a different business model to consumer credit cards. For example, commercial cards have much higher credit limits than consumer cards and the flow of interchange revenue from spending on these cards, to the card issuers (usually banks) enables them to take more credit risk and hence extend more credit to SME’s.

The Australian Small Business and Family Enterprise Ombudsman, Kate Carnell has said that, “the majority of small business failures are by far a result of poor cash flow, with slow payments from customers or clients, a leading factor”. She claimed that “the big end of town are delaying payments to those that can least afford it; small-to-medium sized enterprises”.

One example of this is major food businesses Fonterra and Kellogg’s stretching payment terms for suppliers from 90 days to 120 days. The consequences of this are twofold; firstly the large corporations will hold onto money for longer and get positive returns on that, while the SME’s are forced to use expensive overdrafts at banks to fund their ongoing business.

A survey by a UK company MarketInvoice earlier this year, found Australia was the worst offender for late payments, ranking even below countries such as Mexico. Some jurisdictions have however been moving in the other direction; since March 2013 the maximum payment terms in the European Union have been 30 days, unless an agreement is made in writing by both parties, in which case the maximum is 60 days.

To overcome the cash flow challenges that go on along with longer payment terms, many SME’s use commercial credit cards to pay their suppliers and hence take advantage of the up to 55 interest free days (all the major Australian banks issue commercial cards and the interest free periods are up to 55 days) on these cards. SME’s are using commercial credit cards for more than just their cash flow.

These cards can be used to partly finance payments to suppliers, particularly where an SME has struggled to get finance from a bank. SME’s are hence more likely to rely on commercial cards as a source of finance than are larger businesses, which typically can raise capital through a variety of means like bank loans, share issues or corporate bonds.

The reduction in interchange which the RBA is imposing may cause issuers, including banks, to cut costs by reducing credit risk, which would mean less credit extended to SME’s, via commercial cards. Issuers could also find this segment of the credit card market less attractive and hence be less willing to offer this type of credit card to SME’s.

The RBA’s reasoning for including commercial cards ín the proposed maximum 0.80% interchange cap, is there’s not enough evidence to suggest that issuers will stop providing these cards under the cap. The RBA however accepts that “this may involve the introduction of fees on these cards and/or the reduction of the interest free period”.

According to the Australian Bureau of Statistics, as of June 2015, the SME sector employed 68% of Australians and it generated 55% of total income from industry. As larger businesses look to increase the number of days before they settle their invoices from SME suppliers and these businesses face pressure to pay their employee’s wages and utility bills on time, the value of commercial payment cards is all the more obvious.

Less commercial payment cards; with less credit offered on them, at higher interest rates, could well be another unintended consequence of the RBA’s intervention into the payments system.

Author: Steve Worthington, Adjunct Professor, Swinburne University of Technology

The Australian Competition and Consumer Commission is reminding large businesses of a new ban on charging consumers excessive payment surcharges, which commences today.

“The new law limits the amount a large business can charge customers for use of payment methods such as most credit and debit cards. Businesses can only pass on the permitted costs of the payment method such as bank fees and terminal costs,” ACCC Chairman Rod Sims said.

“The new law has caused many large businesses to review their pricing practices. We expect to see a move from flat-fee surcharges for purchasing items like flights, towards percentage-based or capped surcharges. The ACCC is aware that some event ticketing companies are intending to change their pricing practices from 1 September such that consumers will no longer be charged fees based on the payment method chosen.”

The RBA has indicated, as a guide, that the costs to merchants of accepting payments by debit cards is in the order of 0.5%, by credit card is 1-1.5%, and for American Express cards it is 2-3%. Some merchants’ costs might be higher than these indicative figures.

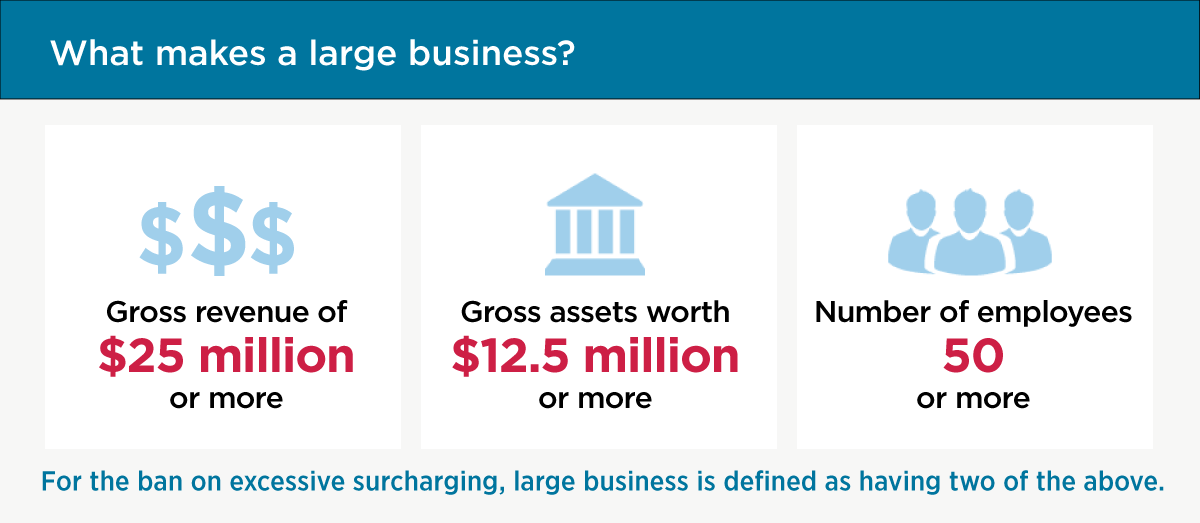

For the first year the law only applies to large businesses, defined as having two of the following: gross revenue of $25 million or more, gross assets worth $12.5 million or more, or with 50 or more employees. It will apply to all businesses from 1 September 2017.

The ACCC has been raising awareness of the ban in the lead up to 1 September, including engaging with many large businesses to ensure they are aware of their obligations.

Consumers who believe they have been charged an excessive surcharge can contact the ACCC via our website.

“We will be enforcing these new rules from today, and the ACCC encourages all large businesses that haven’t already to ensure their payment charging methods are in line with the new law,” Mr Sims said.

It is important to note that businesses can still charge other fees, such as ‘booking fees’ or ‘service fees’ which apply regardless of the method of payment. In doing so, those businesses must still comply with the Australian Consumer Law in terms of ensuring the disclosure of any such fees is upfront and clear.

Passing on the cost of processing debit and credit card payments is not mandatory for businesses. Indeed, the ban has no effect on businesses that choose not to impose a payment surcharge.

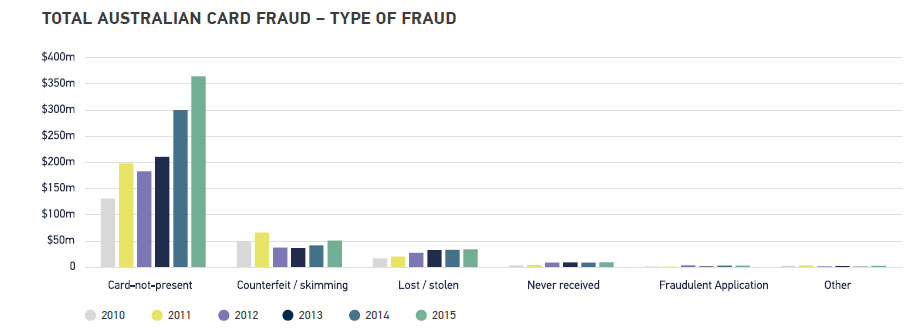

The Australian Payments Clearing Association (APCA) have released their 2016 Payments Fraud Report. The rate of fraud across all Australian cheques and cards increased from 20.8 cents in 2014 to 24.5 cents in 2015.

In 2015, Australians spent $1.92 trillion using their cards and cheques; of this overall total, 0.025%, or $469 million, worth of transactions were fraudulent. While some areas of card fraud have declined, overall card fraud has risen due to a significant increase in CNP fraud. Card-not-present (CNP) fraud occurs when valid card details are stolen and then used to make purchases or other payments without the card, mainly online or by phone.

Australian payment cards fraud

Australians are spending more than ever on their cards and the rate of fraud is increasing. The total amount spent on cards in 2015 increased 5% to $689,470 million. The rate of card fraud increased to 66.8 cents per $1,000, up from 58.8 cents in 2014. This compares to the UK’s 2015 card fraud rate of 83 pence per £1000. CNP fraud increased to $363 million, with 62% or $226.3 million occurring overseas. Most of this fraud is likely due to sophisticated malware and phishing attacks and large-scale data breaches. It reflects the growth in cyber-crime generally.

Domestically, CNP fraud increased 38% to $136.7 million. This channel is increasingly attractive to criminals as Australians spend more online and as measures to tighten up card present channels, both in Australia and overseas, take positive effect.

As the US transitions to chip technology – the last significant economy to upgrade from magnetic stripe – criminals are increasing their focus to online domains. Similar to the cards of other jurisdictions such as the UK, this is impacting Australian cards, which are often captured by data breaches occurring in the US.3 Counterfeit / skimming fraud on Australian cards domestically dropped 10% to $22.9 million.

However, knowing the window of opportunity is closing, fraudsters are rushing to use fake cards at US merchants where the magnetic stripe is still accepted. This largely explains the 77% increase in counterfeit / skimming fraud on Australian cards overseas.

Fraud on Australian cards domestically

With chip technology providing strong protection against counterfeit cards in Australia, fraud is increasingly migrating online. Counterfeit / skimming fraud dropped 10% in 2015 to $22.9 million, down from $25.4 million in 2014. Card-not-present (CNP) fraud increased 38% to $136.7 million, up from $99 million in 2014.

Fraud on Australian cards overseas

Fraud on Australian cards is occurring in the US and other countries at terminals that haven’t yet been upgraded to chip technology. Counterfeit / skimming fraud increased 77% to $28.1 million, up from $15.8 million in 2014. Australian cards have been caught up in large scale data-breaches overseas. CNP fraud increased 13% to $226.3 million, up from $200.9 million in 2014.

Overseas payment cards used in Australia

Chip technology is protecting overseas cards used for card present transactions in Australia. Counterfeit / skimming fraud dropped 14% to $8 million, down from $9.3 million in 2014. However CNP fraud on overseas cards in Australia is increasing. CNP fraud increased 7% to $47.8 million, up from $44.7 million in 2014

Cheques used in Australia

Cheque use has dropped more than 70% in Australia over the past 10 years. The total rate of cheque fraud increased to 0.7 cents per $1,000 in 2015, up from 0.5 cents in 2014 – remaining under 1 cent per $1,000.

The rate of fraud increased to 66.8 cents per $1000 spent, up from 58.8 cents in 2014.

APCA is the self- regulatory body for Australia’s payments industry and has 100 members including Australia’s leading financial institutions, major retailers, payments system operators and other payments service providers.

According to Computerworld, Heritage Bank has endorsed an application by some of the nation’s biggest banks lodged with the Australian Competition and Consumer Commission that seeks the right to form a cartel to collectively negotiate with, and engage in a boycott of, mobile wallet providers including Apple, Google and Samsung.

The Toowoomba-headquartered mutual bank is the biggest issuer of prepaid cards in Australia.

Last month the Commonwealth Bank of Australia, National Australia Bank, Westpac, and Bendigo and Adelaide Bank submitted the application to Australia’s competition watchdog.

In its submission to the ACCC Heritage argued that the restrictions imposed by Apple on third-party mobile payment apps for the iPhone reduce competition. Apple does not allow services other than its own Apple Pay offering to use the iPhone’s Near Field Communication antenna for contactless transactions.

In the ACCC application the banks indicate that one of the issues they would seek to collectively bargain over is access to the iPhone’s NFC capabilities. For its part, Apple has argued opening up access to NFC would undermine the security of mobile payments on the iPhone.

So far, in Australia only American Express and ANZ customers are able to use Apple Pay after the two companies struck agreements with the iPhone maker, Heritage Bank’s submission notes.

“Those with NFC enabled Android phones can choose from a broad range of issuers who support mobile payments,” Heritage argues. “iPhone users are consequently disadvantaged by the lack of access provided by Apple to issuers who offer their customers the option of a mobile payment wallet other than Apple Pay.”

Heritage adds that currently the industry “is not able to develop and enact agreed Australian standards relating to the safety, security and stability of mobile payments systems for which issuers, not Third Party Wallet Providers, primarily hold the risk.”

Finally, the submission adds, “Fees and other charges levied by Third Party Wallet Providers on issuers may not be able to be passed through to users of the service. This reduces competition since the decision to pass fees to customers of issuers (or not) and the level of those fees may not be negotiable when contracting with Third Party Wallet Providers who control mobile devices.”

EFTPOS provider Tyro has also indicated it backs the banks’ application.

“It is in the Australian public interest to maintain choice for consumers, merchants and banks as to mobile wallet solutions and the applications that they enable,” a submission from the company argues.

“While Apple allows third parties to connect free of charge via Wi-Fi, 3G, Bluetooth and other network protocols to its phone product range, it does not do so for NFC.

“Eliminating third party access to the Apple NFC function is particularly effective in stifling innovation and competition, because it is the only available and highly secure connectivity option that is ubiquitously available across the entire card payment infrastructure and terminal fleet.”

ANZ and Amex the winners in Australia’s banks’ fight with Apple over payment apps

However, South Australia’s Small Business Commissioner, John Chapman, expressed a different opinion: “In my view, this is simply a case whereby powerful banks are simply not used to having to accede to another, more powerful organisation — Apple — a global company that has the smarts and the resources to be able to simply ignore the banks’ demands.”

Apple says it “strongly urges” the Australian Competition and Consumer Commission (ACCC) to reject an application from three of the four major banks that would see them able to band together in order to negotiate access to the company’s digital wallet system.

Last month the Commonwealth Bank of Australia, National Australia Bank and Westpac, as well as Bendigo and Adelaide Bank, applied to the ACCC for the right to engage in collective negotiations over, and potentially boycott, third-party digital wallets including Apple Pay, Google Pay and Samsung Pay.

One bugbear of the banks outlined in their application is the refusal of Apple to open up access to the iPhone’s NFC antenna in order for third party iOS applications to be used for contactless payments.

So far ANZ is the only one of Australia’s big four banks to strike a deal to offer Apple Pay to its customers. “Apple has struggled to negotiate agreements with the Australian Banks and only recently signed an agreement with ANZ,” Apple said in a response lodged with the ACCC that was first noted by the AFR.

The other banks “based on their limited understanding of the offering… perceive Apple Pay as a competitive threat”, Apple argued.

The goal of the banks banding together “is to force Apple and other third party providers to accept their terms, allow them to charge consumers that choose to use Apple Pay, and force Apple to undermine the security of its mobile payment service by opening access to the NFC antenna, placing at risk the consumer experience of a simple, secure, and private way to make payments in store, within applications or on the web.”

Apple said it could not identify any public benefits that could arise from the banks being authorised to engage in a collective boycott.

The banks’ application to the ACCC notes: “Some issuers in other countries have expressed concern that Apple has not allowed other mobile payment apps to use the iPhone’s NFC payment functionality…”

“Providing simple access to the NFC antenna by banking applications would fundamentally diminish the high level of security Apple aims to have on our devices,” Apple argued in response.