CBA just released their FY17 results, with statutory NPAT $9,928m, up 7.6% on FY16. The cash NPAT was up 4.6% to $9,881m. Much of the lift is explained by a fall in loan impairment expense, down 12.8% to $1,095m, plus a one off from the Visa transaction.

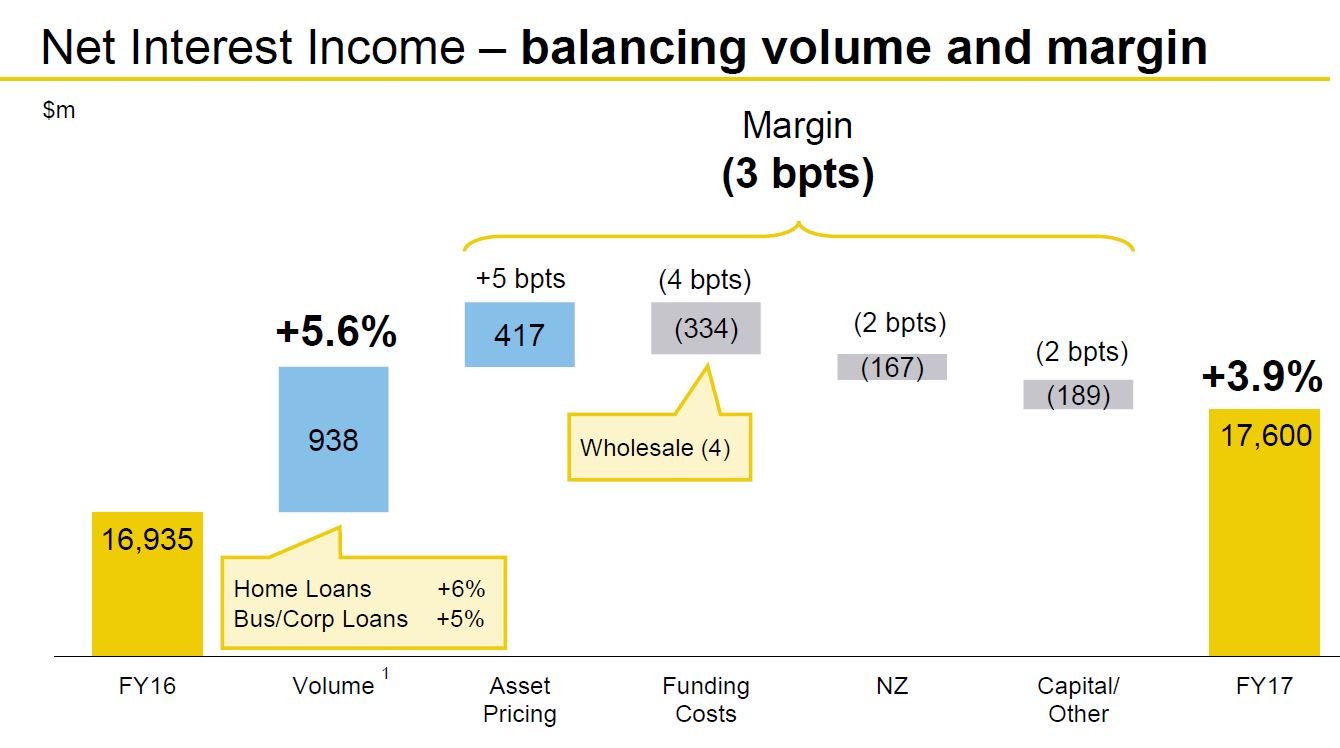

However their net interest margin fell 3 basis points to 2.11%, despite recent mortgage book repricing. The underlying cost income ratio fell 60 basis points to 41.8%.

As a result, return on equity overall fell 0.5% to 16%, earnings per share was $5.74 (compared with $5.55 in FY16) and the dividend per share was $4.29, compared with $4.20 last year.

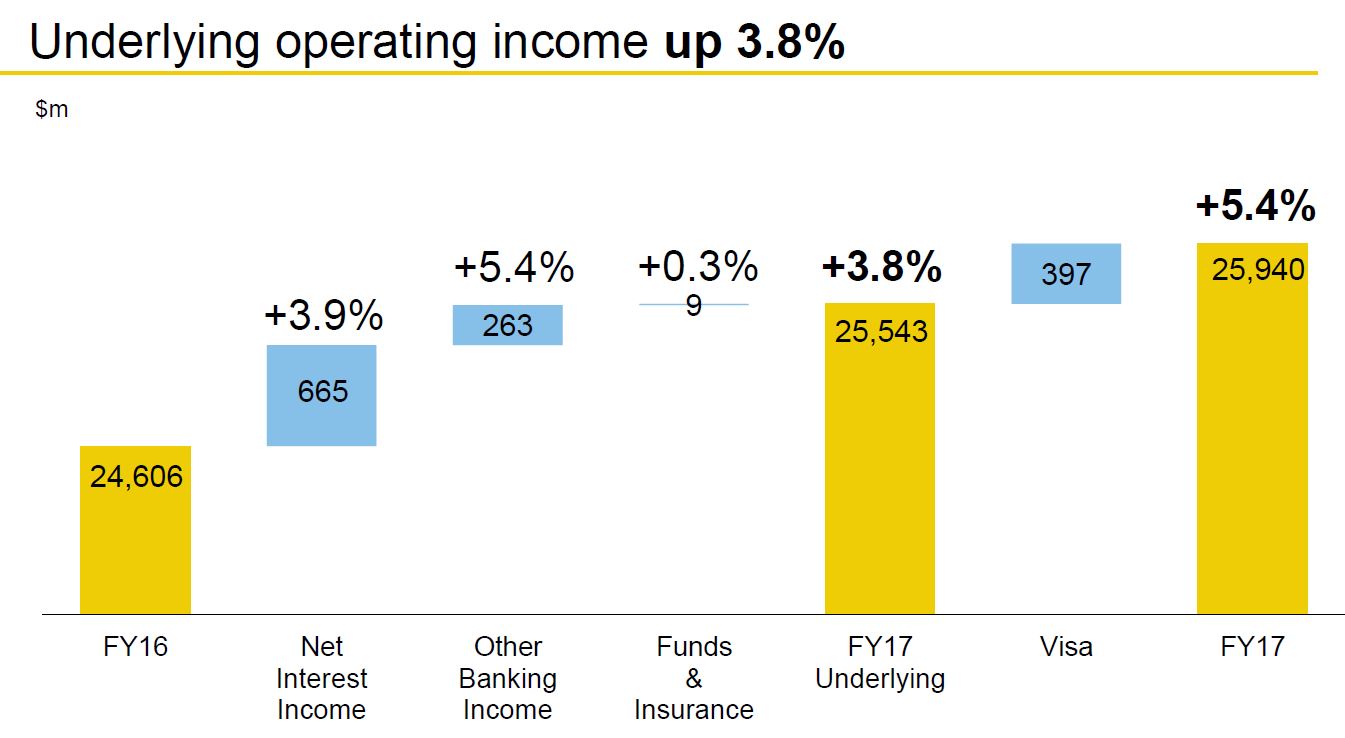

Operating income increased by 3.8%, ahead of operating expense growth of 2.4%, delivering positive jaws on an underlying basis.

Banking income grew 4.3% due to volume growth in home lending, business lending and deposits. Insurance income fell 1.1% due to loss recognition of $143 million.

Banking income grew 4.3% due to volume growth in home lending, business lending and deposits. Insurance income fell 1.1% due to loss recognition of $143 million.

CBA Invested almost $1.3 billion whilst maintaining underlying expense growth to 2.4%.

Higher wholesale funding costs and increased competition in home and business lending more than offset asset repricing, resulting in a 3 basis point decline in the net interest margin to 2.11%. In calculating the Group’s NIM, mortgage offset balances are now being deducted from average interest earning assets to reflect their non-interest earning nature, and to align with peers and industry practice. This results in changes to Group’s NIM for current and prior periods.

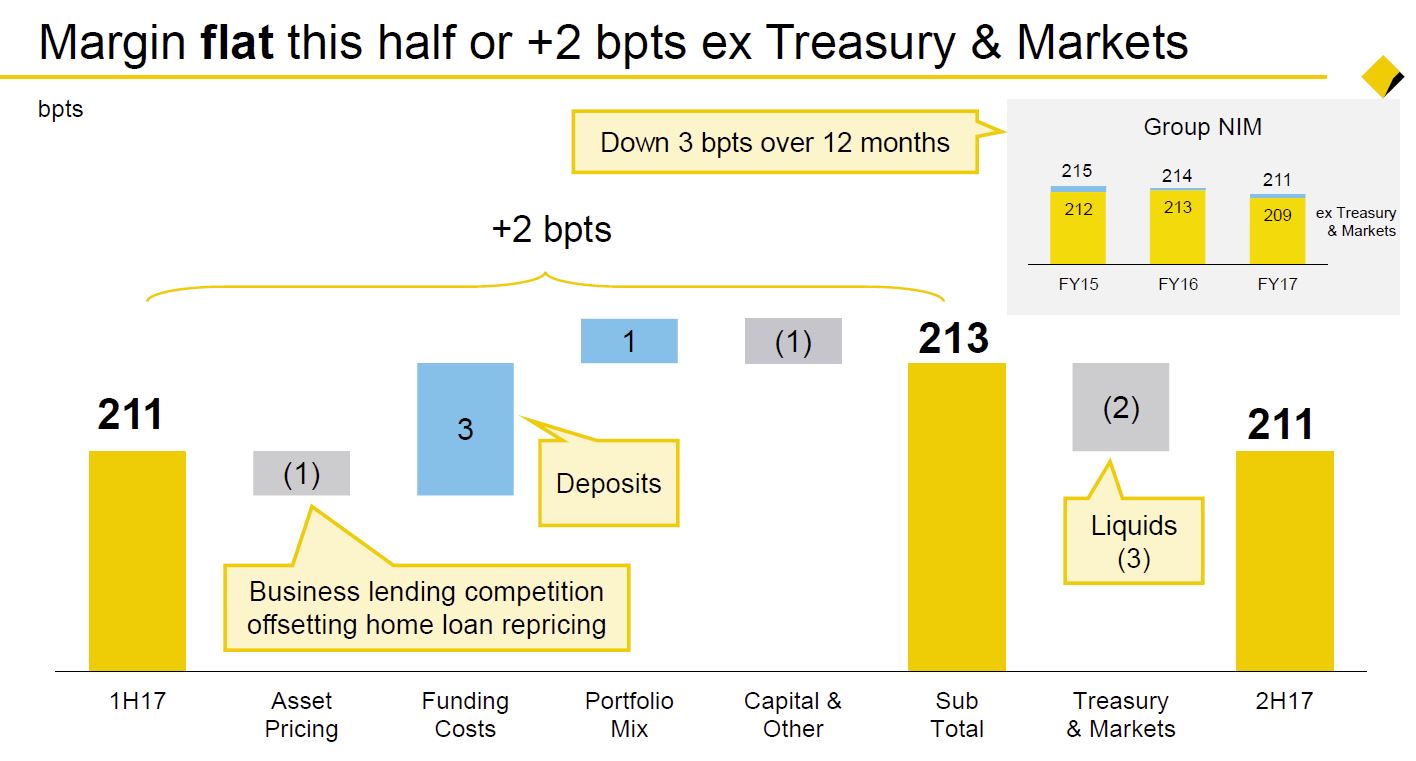

It was flat second half thanks to home loan repricing.

It was flat second half thanks to home loan repricing.

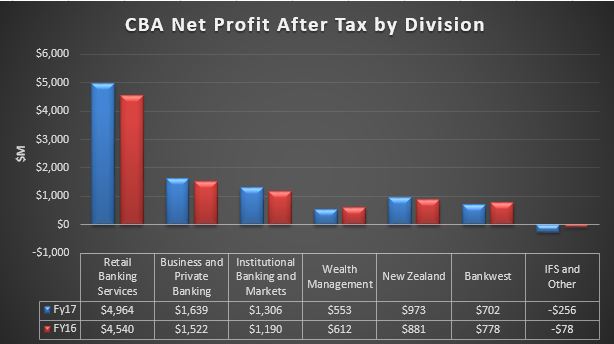

Looking across the divisions, the Retail Bank again contributed the lions share of the result, but with positive growth at the NPAT level in all divisions, other that IFS; all on a cash basis.

Looking across the divisions, the Retail Bank again contributed the lions share of the result, but with positive growth at the NPAT level in all divisions, other that IFS; all on a cash basis.

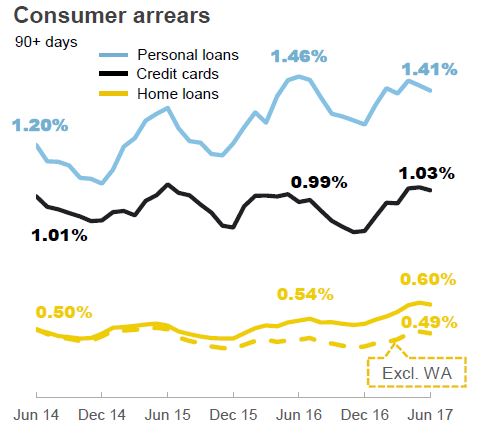

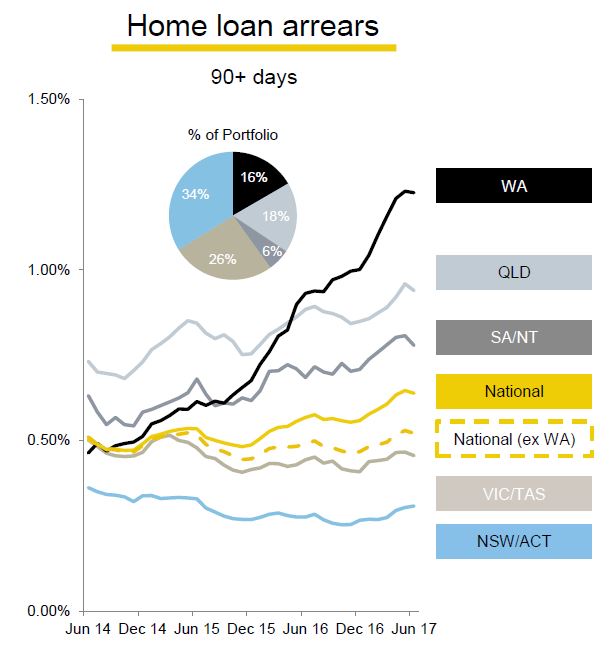

In the Retail bank, consumer arrears were controlled, though losses in WA climbed again, with 90+ days at 1.23%.

In the Retail bank, consumer arrears were controlled, though losses in WA climbed again, with 90+ days at 1.23%.

Some interesting mortgage related information was contained in the announcement.

Some interesting mortgage related information was contained in the announcement.

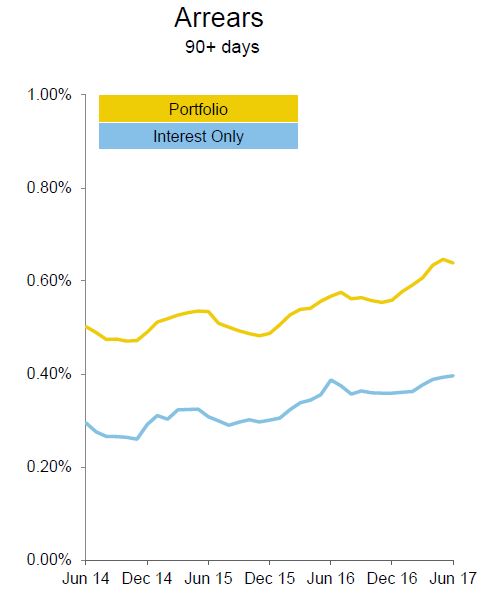

The FY17 losses on their home loan book is 3 bpts. The portfolio dynamic LVR is 50%. Investment loans make up 33%, with new investment loans falling from 37% in Dec 16 to 32% in Jun 17. 77% of customers are paying in advance – this includes any amount ahead of monthly minimum repayment and includes offset facilities. They have a loan serviceability buffer of 2.25% above the customer rate, with a minimum floor rate (RBS: 7.25% pa, Bankwest: 7.35%). They have a maximum LVR of 80% for IO loans now. Interest Only loans have lower arrears.

The FY17 losses on their home loan book is 3 bpts. The portfolio dynamic LVR is 50%. Investment loans make up 33%, with new investment loans falling from 37% in Dec 16 to 32% in Jun 17. 77% of customers are paying in advance – this includes any amount ahead of monthly minimum repayment and includes offset facilities. They have a loan serviceability buffer of 2.25% above the customer rate, with a minimum floor rate (RBS: 7.25% pa, Bankwest: 7.35%). They have a maximum LVR of 80% for IO loans now. Interest Only loans have lower arrears.

John Symond exercised his put option which will require CBA to acquire the remaining 20% interest in Aussie Home Loans (AHL). The purchase price will be determined in accordance with the terms agreed in 2012 and the purchase consideration will be paid in the issue of CBA shares. They will consolidate AHL from completion of the acquisition which is currently expected to be in late August 2017.

John Symond exercised his put option which will require CBA to acquire the remaining 20% interest in Aussie Home Loans (AHL). The purchase price will be determined in accordance with the terms agreed in 2012 and the purchase consideration will be paid in the issue of CBA shares. They will consolidate AHL from completion of the acquisition which is currently expected to be in late August 2017.

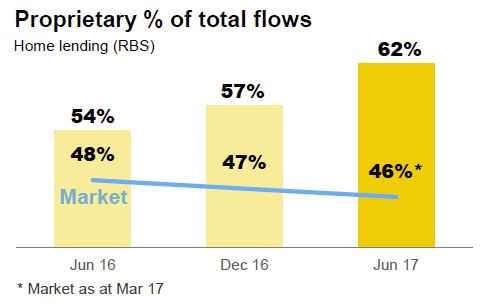

Their focus on propitiatory loan origination has led to a fall in the proportion of loans via brokers.

More broadly, CommBank research on financial wellbeing shows one in three Australian households would struggle to access $500 in an emergency, and more than a third of Australians are spending more than they earn each month.

More broadly, CommBank research on financial wellbeing shows one in three Australian households would struggle to access $500 in an emergency, and more than a third of Australians are spending more than they earn each month.

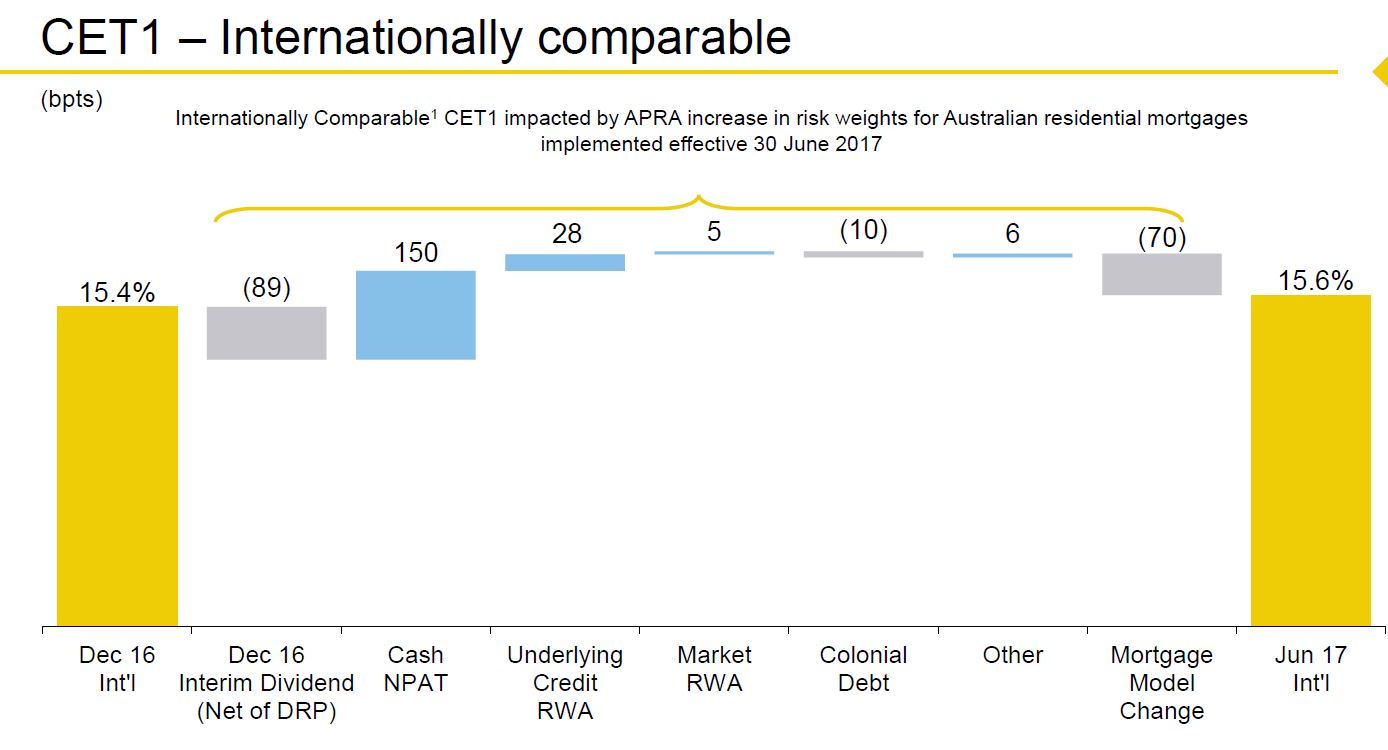

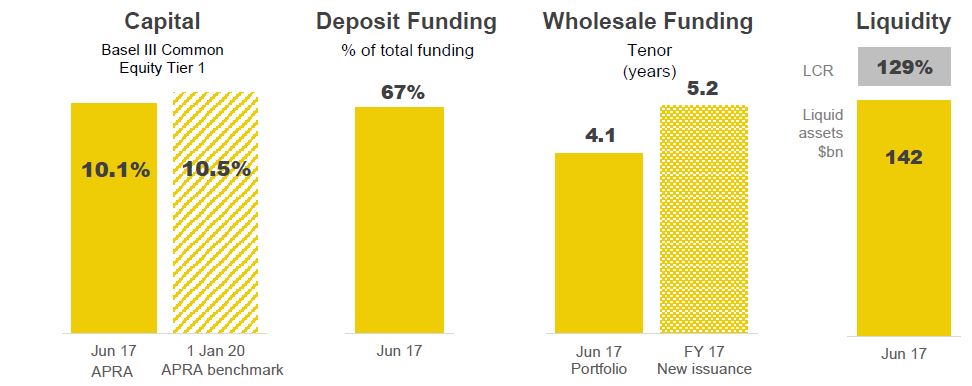

The Group’s Common Equity Tier 1 (CET1) ratio was 10.1% on an APRA basis, and 15.6% on an internationally comparable basis, maintaining CBA’s position in the top quartile of international peer banks for CET1.

CBA are confident they will meet APRA’s‘unquestionably strong’ CET1 ratio average benchmark of 10.5% or more by 1 January 2020.

CBA are confident they will meet APRA’s‘unquestionably strong’ CET1 ratio average benchmark of 10.5% or more by 1 January 2020.

Customer deposits contributed 67% of total funding and the Net Stable Funding Ratio (NSFR) was 107%.

The average tenor of the wholesale funding portfolio was 4.1 years and the average tenor of new issuance was 5.2 years.

Liquid assets increased from $134 billion in 2016 to $142 billion, and the Liquidity Coverage Ratio was 129%.

The Leverage Ratio was 5.1% on an APRA basis and 5.8% on an internationally comparable basis.

The banking levy is estimated at $258m (post tax), first payment due March 2018. The Group effective tax rate will be 30.3% after the levy.