We recently released the latest data on mortgage stress. We said “of the 3.1 million mortgaged households, latest results from the DFA surveys of 52,000 households reveals an estimated 669,000 are now experiencing mortgage stress. This is a 1.5% rise from the previous month and maintains the trends we have observed in the past 12 months”.

Within our household data we have information on the drivers of mortgage stress, the symptoms of stress and how households are mitigating mortgage stress. Today we explore this data.

As described in our earlier post, we look for a range of leading indicators which signal mortgage stress, as well as comparing disposable income with outgoings. We do not use a “30% of gross income” measure because this is too general (there are some household not in stress with much higher proportions of income going on the mortgage, whilst others are paying lower proportions, but are in stress).

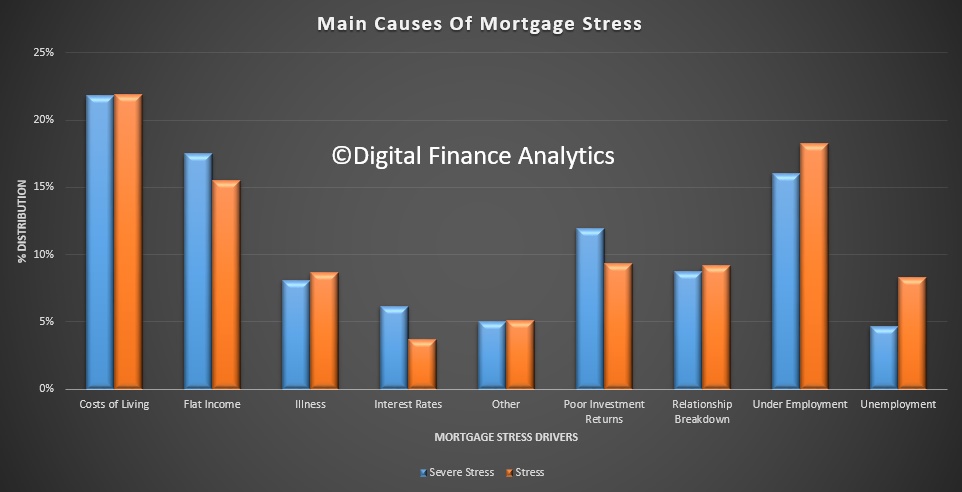

Mortgage stress is caused by a range of factors, including rising costs of living, flat incomes, underemployment, as well as unemployment, relationship breakdown and rising interest rates. There are some differences between those stressed and those in severe stress, but the portfolio of drivers are similar. Over time those stressed are more likely to turn into distressed, typically over 18-24 months.

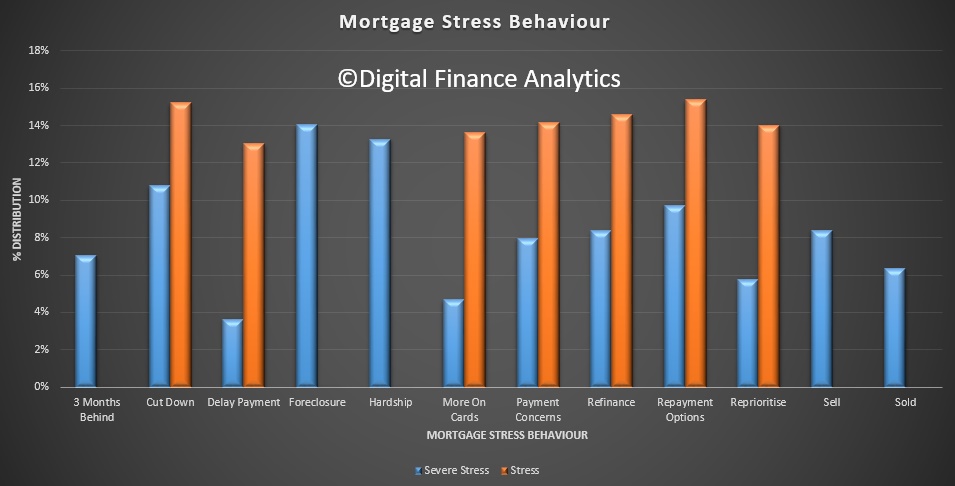

Here is a plot of the various behavioural mortgage stress drivers, separated by those in mild stress (stress) and those in severe stress. Those in stress are actively reviewing their spending priorities, looking at alternative mortgage repayment options to reduce outgoings, seeking to refinance, are putting more on credit cards and generally cutting back on spending; all to alleviate concerns about being able to meet mortgage repayments. Meantime they may well delay making payments.

Here is a plot of the various behavioural mortgage stress drivers, separated by those in mild stress (stress) and those in severe stress. Those in stress are actively reviewing their spending priorities, looking at alternative mortgage repayment options to reduce outgoings, seeking to refinance, are putting more on credit cards and generally cutting back on spending; all to alleviate concerns about being able to meet mortgage repayments. Meantime they may well delay making payments.

Severely stressed households are more likely to already be behind with their repayments, are seeking to sell, seeking hardship assistance, may already be involved in foreclosure, as well as the more normal activities of cutting back spending, re-prioritising, and putting more on cards.

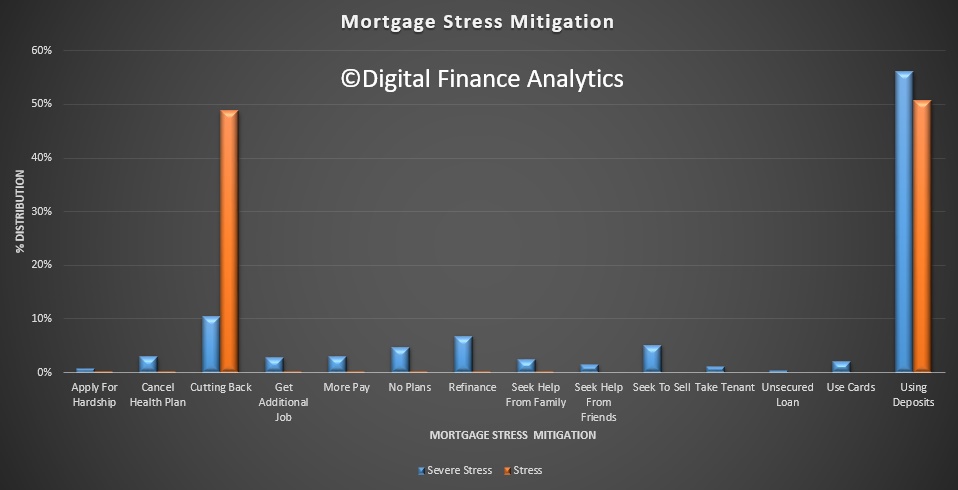

In terms of mitigation, those in mild stress are mainly using two strategies. First drawing on existing savings (which of course are finite) and second cutting back on other spending. Most do not expect to add to their credit cards as they are often already at their limit.

In terms of mitigation, those in mild stress are mainly using two strategies. First drawing on existing savings (which of course are finite) and second cutting back on other spending. Most do not expect to add to their credit cards as they are often already at their limit.

However, those in serve stress, whilst they will also do the same; a wider range of activities are on the cards, including seeking to sell or refinance, putting even more are cards (often getting additional credit), cancelling health insurance, and seeking help from friends, family and even unsecured loans (like pay day loans). This is again an indication of the complexity of the situation these households are facing.

Dealing with mortgage stress is difficult, especially when incomes are static or falling in real terms and when interest rates are likely to rise further. Yet we note that about half of those we identify as in stress do not recognise they are in difficulty. The first step to solving a problem is to recognise you have one.

Dealing with mortgage stress is difficult, especially when incomes are static or falling in real terms and when interest rates are likely to rise further. Yet we note that about half of those we identify as in stress do not recognise they are in difficulty. The first step to solving a problem is to recognise you have one.

Many stressed households would benefit from some objective financial advice, as dealing with this is complex. There are not many independent sources of advice available. Whilst there is some information of ASIC’s Money Smart site, we think ASIC should put up more detailed guidance about spotting the symptoms and dealing with mortgage stress.

Many mortgage brokers and financial advisors would jump to selling more products, which is not the right solution in the majority of cases.

One thought on “Getting To Grips With Mortgage Stress”