Given the rise in the number of Fintechs targetting the SME unsecured lending sector, it is timely to consider the potential addressable size of the market in Australia. To do that we have taken data from the Digital Finance Analytics SME survey of 26,000 businesses, and used this data to estimate the current size of the market. The latest data is from August 2016.

First, we need to focus in on smaller SME’s, so we set a turnover ceiling of $500k. In fact though there are more than 1 million businesses in this category, many SME’s have much smaller turnovers than that. Then we remove from the analysis secured loans (either against property or other assets), leases, factoring and credit card debt. This gives us a read of the level of unsecured debt. We also excluded businesses who prefer not to borrow at all.

First, we need to focus in on smaller SME’s, so we set a turnover ceiling of $500k. In fact though there are more than 1 million businesses in this category, many SME’s have much smaller turnovers than that. Then we remove from the analysis secured loans (either against property or other assets), leases, factoring and credit card debt. This gives us a read of the level of unsecured debt. We also excluded businesses who prefer not to borrow at all.

So, we estimate that currently, the stock of unsecured loans to these small businesses is around $8.2 billion. Of this, $5.3 billion would show up as a business loan, either as an overdraft, structured loan or term loan in the RBA data. The rest is classified as personal debt, meaning it is a personal loan or overdraft, but it will still be used for business purposes. So, $2.9 billion relates to loans which would be classified as personal finance in the RBA data. This also highlights the significant “twilight zone” between business and personal finances.

Next, we need to estimate the annual flow of these loans, and also overlay those businesses with the potential to access a Fintech loan. At very least they need to be comfortable with using online services, and tools. So we excluded the “digital luddites” and those not tech savvy.

We estimate that $3.6 billion of unsecured lending was written by lenders, of all sorts, to our target businesses, in the past 12 months. Of this $2.1 billion was a business loan, and $1.5 billion was a personal loan. This includes refinancing of existing loans, and new loans.

Most Fintech SME lenders will only lend to a business, with an ABN. So, we should discount the $1.5 billion of personal loans. That leaves a current annual addressable market of around $2.1 billion. We also expect this to grow strongly in coming years.

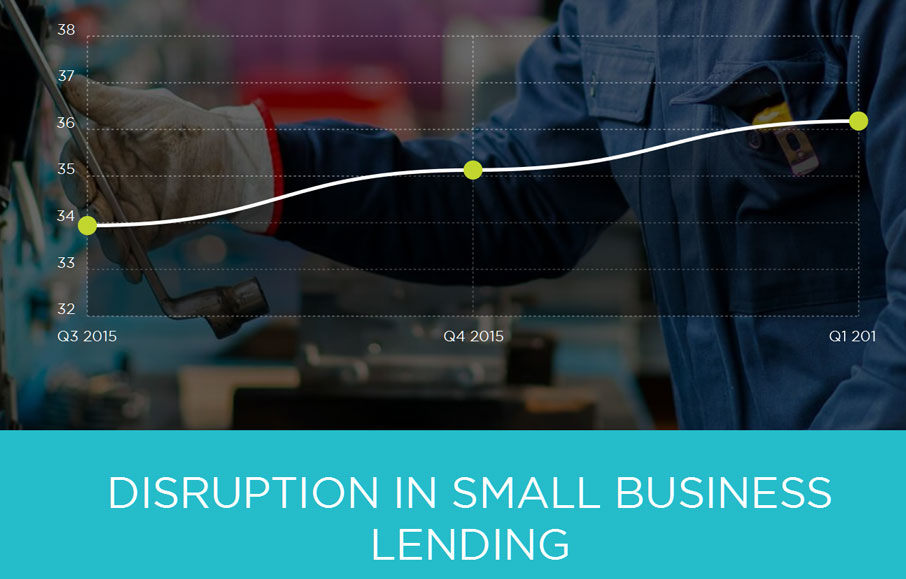

We are already seeing a strong trend in the growing awareness of Fintech among businesses. The joint DFA and Moula Disruption Index is tracking this momentum.

Increased digital penetration, and greater awareness of Fintech alternatives will increase the addressable market quite considerably. In addition, new lenders may offer loans to businesses which today cannot obtain credit.

Increased digital penetration, and greater awareness of Fintech alternatives will increase the addressable market quite considerably. In addition, new lenders may offer loans to businesses which today cannot obtain credit.

So, in conclusion, despite the relatively early history of the sector, there is an addressable market which is significant, and interesting and north of $2 billion annually. Whilst the market is small compared with the $40 billion consumer credit card industry or the $140 billion total consumer credit market, it is set to grow.

Finally, it is also worth considering our post from yesterday, which looked at some Fintechs charging very high rates of interest. Will increased competition drive rates lower and create a still larger market?