There were several well publicised Government bail-out’s of banks which got into problems after the GFC. For example, the UK’s Royal Bank of Scotland was nationalised. This costs tax payers dear, so there were measures put in place to try to manage a more orderly transition when a bank gets into difficulty.

In October 2011, the Financial Stability Board (FSB) issued its Key Attributes

of Effective Resolution Regimes for Financial Institutions (Key Attributes). These Key Attributes set out the ‘core elements that the FSB considers to be necessary for an effective resolution regime. There followed legislation in a number of jurisdictions.

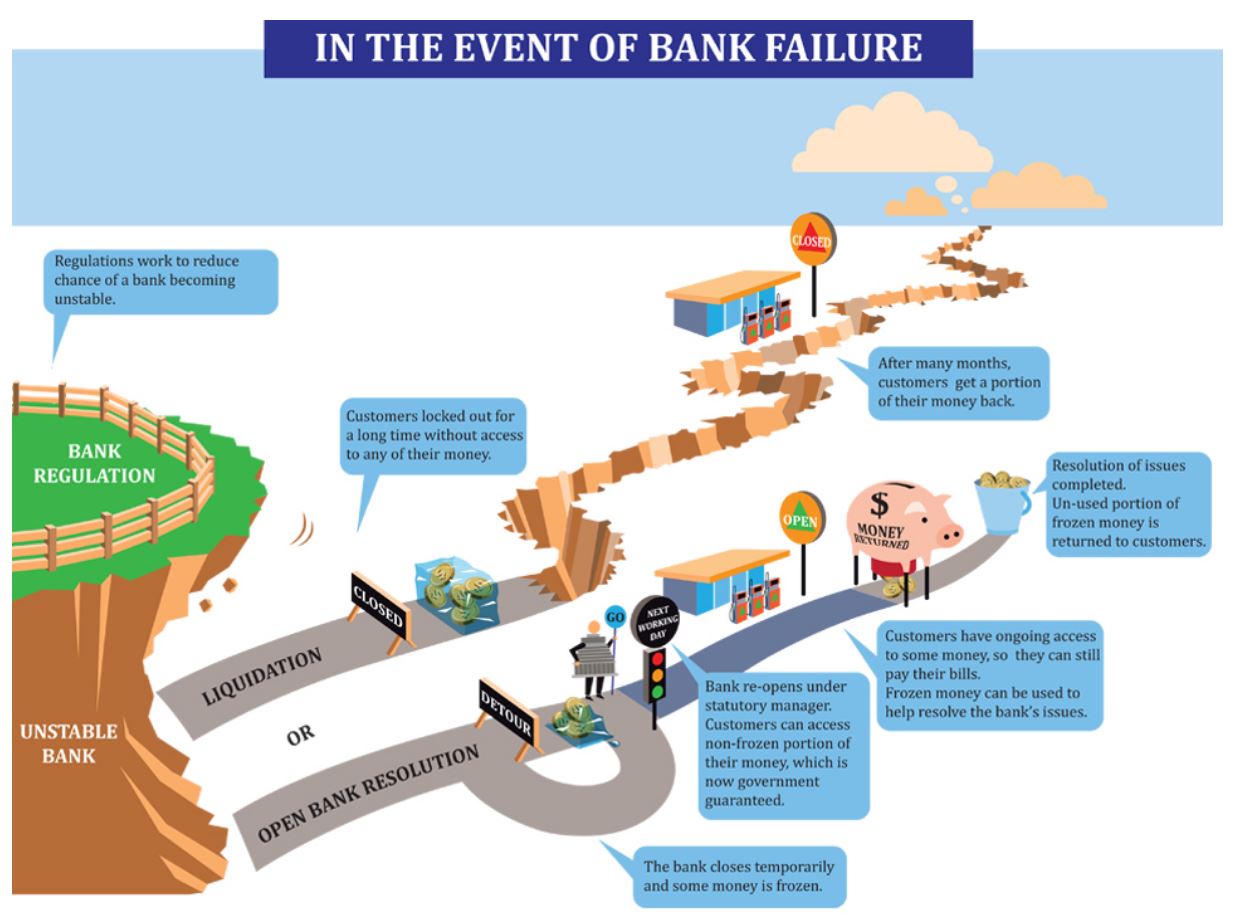

For example, the EU introduced the Bank recovery and resolution – Directive 2014/59/EU, the US The Dodd-Frank Title II Overview: Orderly Liquidation Authority and in New Zealand the Open Bank Resolution (not to be confused with Open Banking, which we discussed last week). This is a summary from New Zealand.

But note the chilling words “the bank closes temporarily and some money is frozen. Bank re-opens under statutory manager. Customers can access non-frozen portion of their money, which is now Government protected. Frozen money can be used to help resolve the bank’s issues. Resolution of issues completed. Un-used portion of frozen money is returned to customers”.

But note the chilling words “the bank closes temporarily and some money is frozen. Bank re-opens under statutory manager. Customers can access non-frozen portion of their money, which is now Government protected. Frozen money can be used to help resolve the bank’s issues. Resolution of issues completed. Un-used portion of frozen money is returned to customers”.

Or in other words, customers money, held as savings in the bank are able to be grabbed to assist in the resolution. This is of course what happened to people with bank deposits in Cyprus a few years back.

The thinking behind it is simple. Banks need an exit strategy in case of a problem, and Government bail-outs should not be an option. So a manager can be appointed to manage through the crisis. They can use bank capital, other instruments, like hybrid bonds and deposits to create a bail-in. This approach to rescuing a financial institution on the brink of failure makes its creditors and depositors take a loss on their holdings. This is the opposite of a bail-out, which involves the rescue of a financial institution by external parties, typically governments using taxpayers money.

So, given the New Zealand position (and the tight relationship between banking regulators in Australia and New Zealand), we should look at the position in Australia. Are deposit funds in Australia likely to be “bailed-in”?

As it happens there has been a long running discussion on this in Australia, and on 16 November 2017, the Senate referred the Financial Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Bill 2017 [Provisions] to the Economics Legislation Committee for inquiry and report by 9 February 2018. They just reported back.

It all centered on the powers which were to be given to APRA to deal with a banking collapse. “The bill seeks to strengthen the powers of the Australian Prudential Regulation Authority (APRA) to facilitate the orderly resolution of an authorised deposit-taking institution (ADI) or insurer so as to protect the interests of depositors and policyholders, and to protect the stability of the financial system in case of crisis”. The Treasurer had argued that by “affording APRA the power to work with ADIs and insurers in order to plan for economic stress events, the cost to the taxpayer will be significantly

reduced in the event of a financial crisis”.

The Senate review and consultation elicited a significant number of submissions, and they made two main points in opposition to the bill: firstly, they believed that this bill gives APRA the power to ‘bail-in’ depositors’ savings to stabilise a failing financial institution; secondly, in place of the bill, the Australian Parliament should legislate a Glass-Steagall style separation of the banks.

Specifically, Dr Wilson Sy, a former analyst with APRA, considered that the bill was not clear enough on the topic of depositors’ savings. Dr Sy suggested that deposit protection is to be balanced against financial system stability, without the law clearly stating which has higher priority’. Dr Sy claimed that the bill is ‘designed to confiscate bank deposits to ‘bail-in’ insolvent banks to save the financial system.

It came down to the meaning of “any other instrument” in the draft bill. Treasury said, “the use of the word ‘instrument’ in paragraph (b) is intended to be wide enough to capture any type of security or debt instrument that could be included within the capital framework in the future. It is not the intention that a bank deposit would be an ‘instrument’ for these purposes”. Treasury confirmed that because deposits are not classified as capital instruments, and do not include terms that allow for their conversion or write-off, they cannot be ‘bailed-in’.

The committee concluded:

The committee believes that the protection of depositors’ interests is paramount and does not consider that the bill would allow the ‘bail-in’ of Australians’ savings and deposits. The stability of the financial system depends on its depositors having confidence in its financial institutions. By ensuring the security of depositors’ savings, the overall protection of the financial system can be ensured.

But there are a few questions to consider.

- Why not expressly exclude deposits from the bill, the current vague wording appears to leave the door open for a deposit grab in case of financial instability? We may have some reassuring words from the regulators, but is it enough?

- How does this fit with the NZ model, where deposits can be targeted, especially, as the regulators in the two countries are closely aligned, and in fact most banking in New Zealand is provided by Australian Bankers. In case of failure would customers of a bank operating in both countries be different?

And two wider questions.

- The NZ model expressly says depositors should weight up the risks of placing money with specific lenders but can savers really do this?

- The issue of hybrid bonds needs more careful consideration, in that in Australia (unlike some other countries) these bonds have been sold to retail investors, people looking to savings with good returns, and who probably do not understand the bail-in risks they may face. So even if deposits are excluded there is a risk that investors in hybrids will get a nasty shock.

Seems to me this is a messy area, and I for one cannot be 100% convinced savings will never be bailed-in. And that’s a worry!

I recall the Productivity Commission comment last week, that financial stability had taken prime place compared with competition (and so customer value) in financial services. The issue of bail-in of deposits appears to be shaping the same way.