Moody’s says on 17 November, the European Banking Authority (EBA) set out its draft methodology for a new round of stress tests that the European Union’s 49 biggest banks must undergo next year. The inclusion of IFRS 9 will lower Tier 1 equity, under stress by an estimated 50-60 basis point.

Similar to the 2016 stress tests, the 2018 exercise will examine banks’ resilience to both base-case and stressed-case scenarios over a three-year horizon, based on a common methodology and prescribed macro-economic scenario parameters. The EBA test will again abstain from setting a minimum capital threshold below which a bank would fail, as in 2014. However, even without set hurdles, the market will benchmark the adverse scenario results, expressed in stressed capital ratios, against banks’ minimum capital requirements, and thereby single out the weaker performers.

The first-time inclusion of International Financial Reporting Standard 9 (IFRS 9), a new accounting rule that takes effect 1 January 2018, will make next year’s stress test tougher than the last one and will likely translate into greater provisioning needs and therefore lower common equity Tier 1 ratios in the prescribed stress-case scenario. The new rules demand that banks set aside higher loan-loss provisions further in advance of default, which is credit positive for banks. While we expect that the initial effect of IFRS 9 will be limited, and therefore digestible for most EU banks, risk provisioning requirements under simulated stressed market conditions will likely be greater using the IFRS 9 rules. However, the size of provisioning will also strongly depend on the macroeconomic scenario assumptions that have yet to be published.

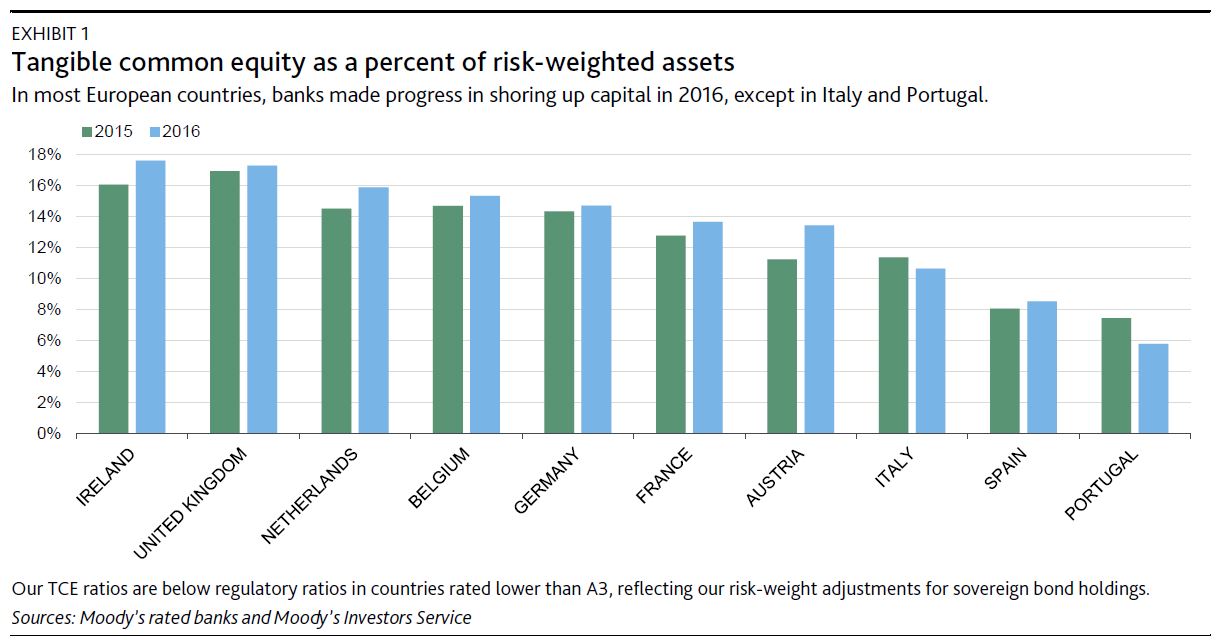

Our expectation of a limited initial effect of IFRS 9 is based on our projection of a 50-60 basis point decline in the ratio of common equity Tier 1 to risk-weighted assets for many European banks. However, we also expect that the initial effect will vary across regions. When additionally taking into account varying stating-point capital levels, capital ratios of banking systems starting from a weak position, including Italy and Portugal, are more at risk of stressed capital ratios falling closer to (or even below) the applicable minimum requirements (see Exhibit 1).

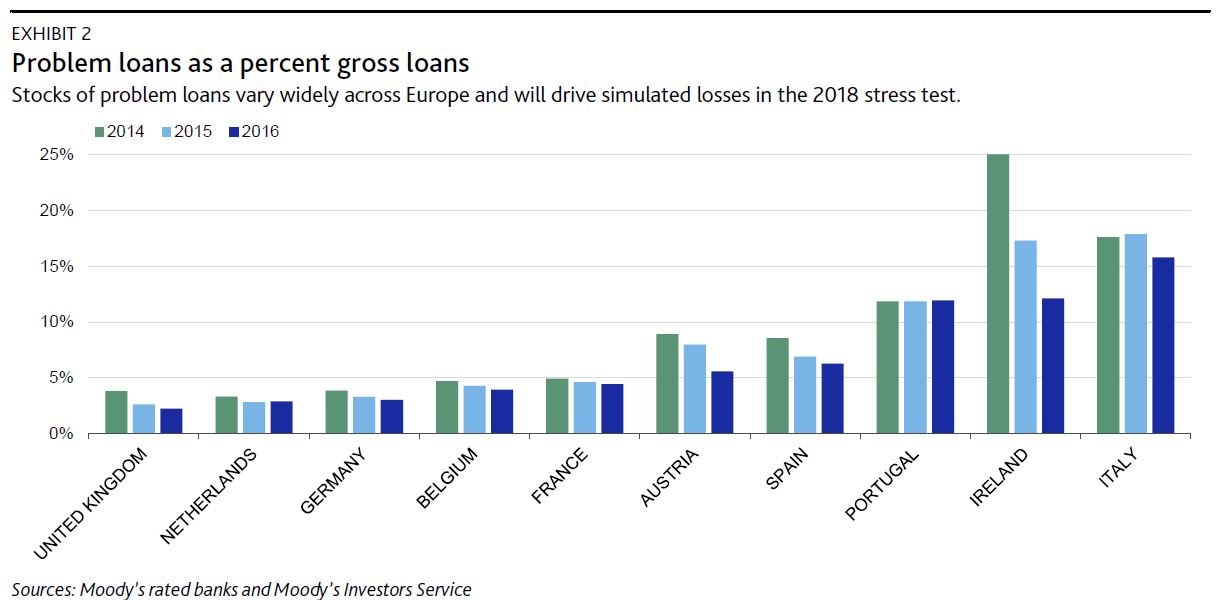

In the EBA’s 2018 stress test, the initial effect on capital ratios will likely be amplified when simulating stressed economic conditions. Europe’s weaker banking systems with relatively large but still performing portfolios that have deteriorated over time will experience greater capital effects under the new rules than banks that benefitted from systemwide asset quality improvements amid benign credit conditions in recent years. Such quality improvements have resulted in low nonperforming exposures in a number or European countries, including France, Germany and the UK (see Exhibit 2).

The objective of the 2018 stress test is to assess the resilience of EU banks and banking systems to shocks. The results will inform the supervisory review and evaluation process, the European Central Bank’s annual in-depth evaluation of each bank’s risk exposure. This evaluation forms the basis of the regulators’ decisions on bank-specific minimum capital requirements for the subsequent year