The RBA released their credit aggregate data to end December 2017 today. $1.1 billion of loans were reclassified in the month (we guess AMP).

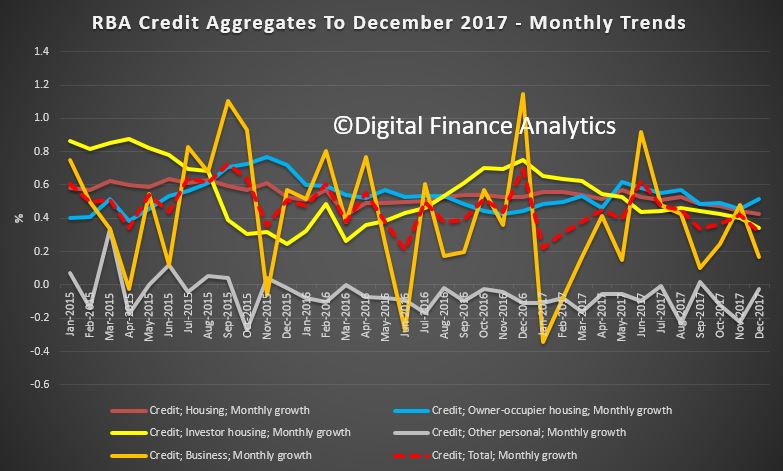

They report that lending for housing grew 6.3% for the 12 months to December 2017, the same as the previous year, and the monthly growth was 0.4%. Business lending was just 0.2% in December and 3.2% for the year, down on the 5.6% the previous year. Personal credit was flat in December, but down 1.1% over the past year, compared with a fall of 0.9% last year. This is in stark contrast to the Pay Day Loan sector, which is growing fast, as we discussed yesterday (and not in the RBA data).

Total credit grew 0.3% in the month, and 4.8% for the year, so mortgage lending is still supporting overall growth, lifting the record household debt even higher. We need still tighter regulatory controls – especially as the costs of living continue to outstrip wage growth.

The annual trends show that investor lending is slowing a little, but still stands at 6.1% seasonally adjusted. Owner occupied lending is running at 6.4% over the last year. 34.1% of loans are for investment purposes.

The monthly data is very noisy as usual.

The monthly data is very noisy as usual.

The value of owner occupied loans was $1.13 trillion, up $6.3 billion or 0.6%, seasonally adjusted; investment loans were $587 billion up $2 billion or 0.3%, seasonally adjusted; other personal credit $151 billion, down 0.2% or 0.3 billion and business lending was $908 billion, up $0.8 billion or 0.1%.

The data contains various health warnings:

The data contains various health warnings:

All growth rates for the financial aggregates are seasonally adjusted, and adjusted for the effects of breaks in the series as recorded in the notes to the tables listed below. Data for the levels of financial aggregates are not adjusted for series breaks. Historical levels and growth rates for the financial aggregates have been revised owing to the resubmission of data by some financial intermediaries, the re-estimation of seasonal factors and the incorporation of securitisation data. The RBA credit aggregates measure credit provided by financial institutions operating domestically. They do not capture cross-border or non-intermediated lending.

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $62 billion over the period of July 2015 to December 2017, of which $1.1 billion occurred in December 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.