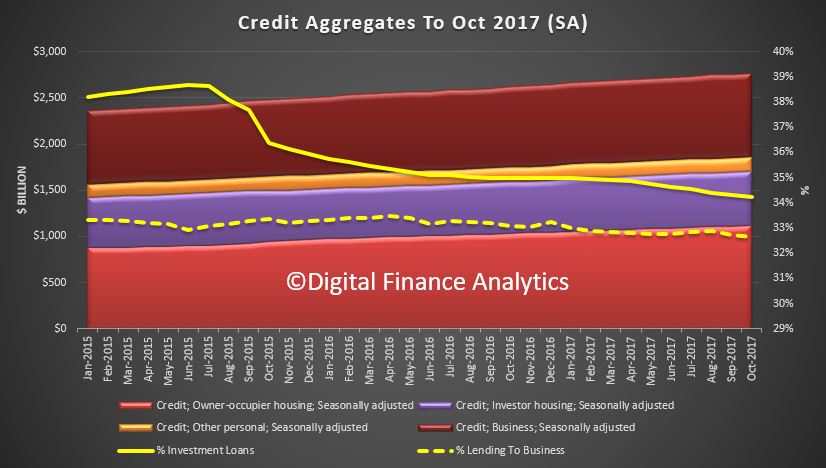

The latest data from the RBA, to end October 2017 , shows that lending for housing rose 0.5% in the month, and 6.5% for the past year (three times inflation!). Lending to business rose 0.3% to 4% over the past year and personal credit was flat, and fell 0.9% over the past year. Another $1.2 billion of housing loans were reclassified in the month, making $60 billion in total, this is more than 10% of the total investment loan book! The proportion of investor loans fell slightly again, down to 34.2% of portfolio

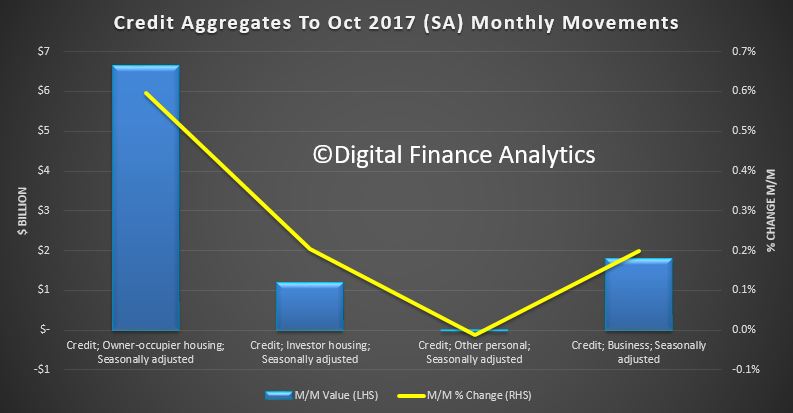

Total mortgage lending is now above $1,7 trillion, with owner occupied loans up 0.6% or $6.6 billion to $1.12 trillion, and investor loans up 0.2% or $1.2 billion to $584 billion. Comparing this with the APRA data, out today, we see continued relative growth in the non-bank sector.

Total mortgage lending is now above $1,7 trillion, with owner occupied loans up 0.6% or $6.6 billion to $1.12 trillion, and investor loans up 0.2% or $1.2 billion to $584 billion. Comparing this with the APRA data, out today, we see continued relative growth in the non-bank sector.

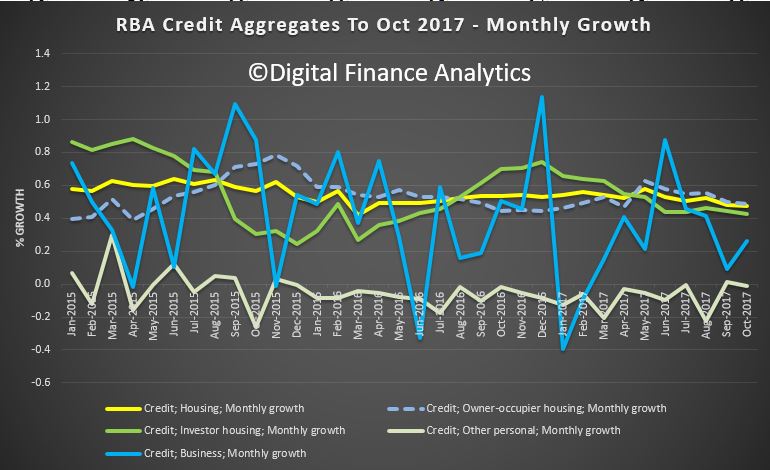

Here is the monthly growth plots, which even seasonally adjusted are noisy.

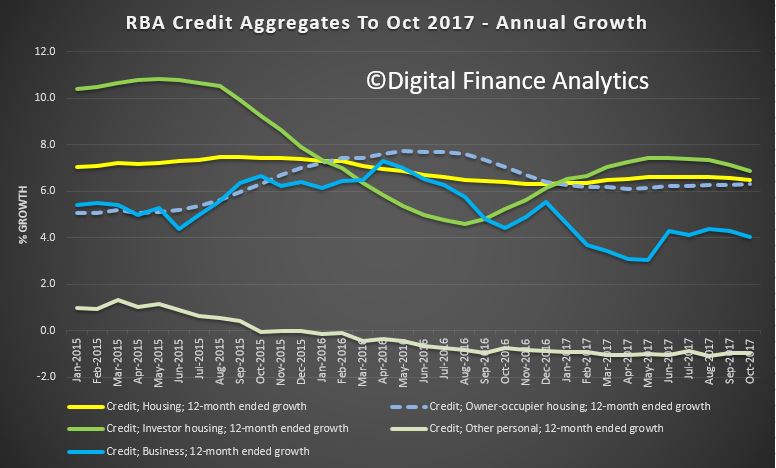

Here is the monthly growth plots, which even seasonally adjusted are noisy.  The smoother annual plots shows a slowing trend across the mortgage sector, but with investor sector still growth at 6.9%, ahead of the owner occupied sector at 6.5%, or business at 4%. Further evidence the settings are wrong.

The smoother annual plots shows a slowing trend across the mortgage sector, but with investor sector still growth at 6.9%, ahead of the owner occupied sector at 6.5%, or business at 4%. Further evidence the settings are wrong.

There is simply no excuse to allow home lending to be running at more than three times inflation or wage growth at the current dizzy price and leverage levels. Still too much focus on home lending and not enough on productive growth enabling business lending. This is something which the Royal Commission is unlikely to touch, as it is a policy, not a behaviourial issue.

There is simply no excuse to allow home lending to be running at more than three times inflation or wage growth at the current dizzy price and leverage levels. Still too much focus on home lending and not enough on productive growth enabling business lending. This is something which the Royal Commission is unlikely to touch, as it is a policy, not a behaviourial issue.

The RBA says:

Following the introduction of an interest rate differential between housing loans to investors and owner-occupiers in mid-2015, a number of borrowers have changed the purpose of their existing loan; the net value of switching of loan purpose from investor to owner-occupier is estimated to have been $60 billion over the period of July 2015 to October 2017, of which $1.2 billion occurred in October 2017. These changes are reflected in the level of owner-occupier and investor credit outstanding. However, growth rates for these series have been adjusted to remove the effect of loan purpose changes.