Digital Finance Analytics (DFA) has released the February 2018 mortgage stress and default analysis update. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Across Australia, more than 924,500 households are estimated to be now in mortgage stress (last month 924,000). This equates to 29.8% of households. In addition, more than 21,000 of these are in severe stress, up 1,000 from last month. We estimate that more than 55,000 households risk 30-day default in the next 12 months, up 5,000 from last month.

We expect bank portfolio losses to be around 2.8 basis points, though with losses in WA are higher at 4.9 basis points. Some households continue to benefit from refinancing to cheaper owner occupied loans, giving them a little more wriggle room in terms of cash flow. The typical transaction has saved up to 45 basis points or $187 each month on a $500,000 repayment mortgage. Enough to make a real difference.

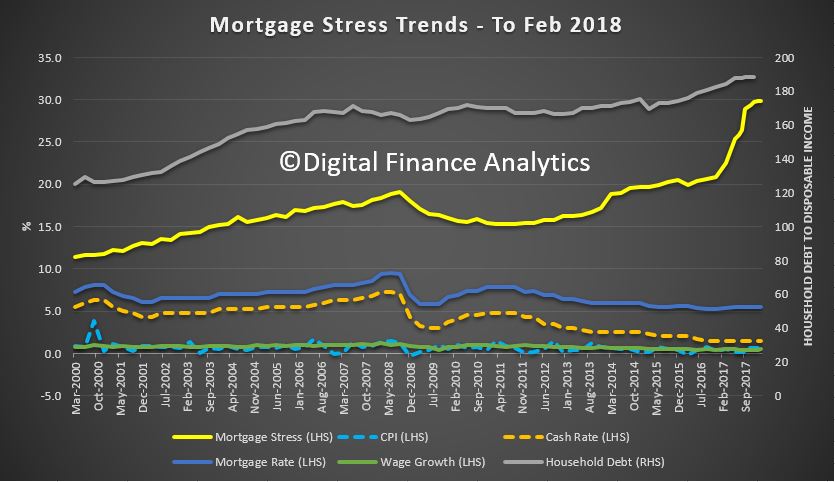

Martin North, Principal of Digital Finance Analytics said “the number of households impacted are economically significant, especially as household debt continues to climb to new record levels. Mortgage lending is still growing at two to three times income. This is not sustainable and we are expecting lending growth to continue to moderate in the months ahead”. The latest household debt to income ratio is now at a record, if revised 188.4.[1]

Martin North, Principal of Digital Finance Analytics said “the number of households impacted are economically significant, especially as household debt continues to climb to new record levels. Mortgage lending is still growing at two to three times income. This is not sustainable and we are expecting lending growth to continue to moderate in the months ahead”. The latest household debt to income ratio is now at a record, if revised 188.4.[1]

In our report last month, Gill North, a professor of law at Deakin University and a DFA Principal, indicated that “when external conditions in Australia deteriorate and or levels of financial stress and loan defaults rise acutely, a wave of responsible lending actions seems inevitable.”

Last week, the findings of an important case imitated by the Australian Securities and Investments Commission (ASIC) against the ANZ banking group were published: Australian Securities and Investments Commission v Australia and New Zealand Banking Group Limited [2018] FCA 155. ANZ was found to have breached its responsible lending obligations when providing car loans through its former car finance business, Esanda, and was ordered to pay a civil penalty of $5 million. The legal principles established in this case are broadly relevant, as all credit assistance providers (including brokers) and credit providers are subject to responsible lending obligations.

The Court found that in respect of 12 car loan applications from three brokers, ANZ failed to take reasonable steps to verify the income of the consumer because it relied solely on consumer payslips provided by the loan broker in circumstances where ANZ:

- knew that payslips were a type of document that was easily falsified;

- received the document from a broker who sent the loan application to Esanda; and

- had reason to doubt the reliability of information received from that broker;

- income is one of the most important parts of information about the consumer’s financial situation in the assessment of unsuitability, as it will govern the consumer’s ability to repay the loan;

- while ANZ did not completely fail to take steps to verify the consumers’ financial situation, it inappropriately relied entirely on payslips received from these brokers; and

- ANZ management did not ensure that relevant policies were complied with and, in the case of the contraventions involving one broker, no action was taken despite management personnel having become aware of the issues about the broker.

ANZ will be remediating approximately 320 car loan customers for loans taken out through the three broker businesses from 2013 to 2015 which are likely to have been affected by fraud. ASIC has separately taken action against the broker businesses that were involved in submitting false documents to ANZ.

Gill and a co-author (Associate Professor Therese Wilson from the law school at Griffiths University) have just had a paper entitled “Supervision of the Responsible Lending Regimes: Theory, Evidence, Analysis & Reforms” accepted for publication by the prestigious and highly ranked journal of the ANU University, the Federal Law Review. This co-authored paper includes an empirical study and analysis on the responsible lending actions taken by ASIC between 2014 and mid-2017.

Finally, Gill commends the Financial Services Royal Commission for its initial focus on consumer credit related misconduct and “predicts that consumer credit will be at the heart of the next significant banking scandal or financial crisis in Australia.”

Standing back, risks in the system continue to rise, and while recent strengthening of lending standards will help protect new borrowers, there are many households currently holding loans which would not now be approved. This is a significant sleeping problem and the risks in the system are higher than many recognise.

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end February 2018. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Households are defined as “stressed” when net income (or cash flow) does not cover ongoing costs. They may or may not have access to other available assets, and some have paid ahead, but households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell.

The forces which are lifting mortgage stress levels remain largely the same. In cash flow terms, we see households having to cope with rising living costs – notably child care, school fees and fuel – whilst real incomes continue to fall and underemployment remains high. Households have larger mortgages, thanks to the strong rise in home prices, especially in the main eastern state centres, but now prices are slipping. While mortgage rates remain quite low for owner occupied borrowers, those with interest only loans or investment loans have seen significant rises. We expect some upward pressure on real mortgage rates in the next year as international funding pressures mount, a potential for local rate rises and margin pressure on the banks.

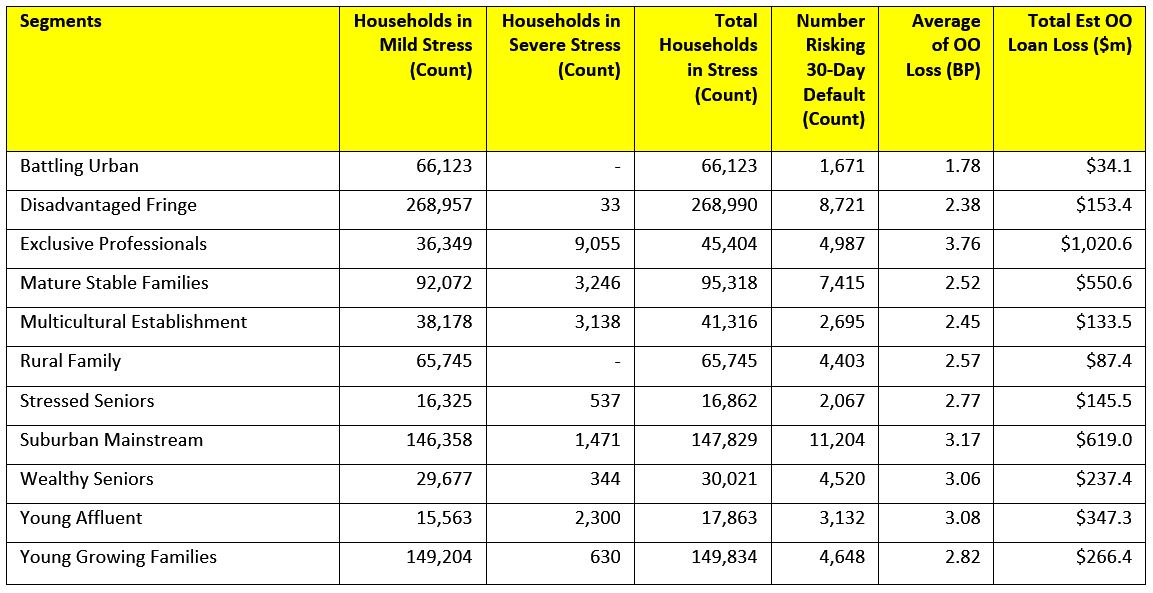

Probability of default extends our mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes. Our Core Market Model also examines the potential of portfolio risk of loss in basis point and value terms. Losses are likely to be higher among more affluent households, contrary to the popular belief that affluent households are well protected.

Stress by The Numbers.

Stress by The Numbers.

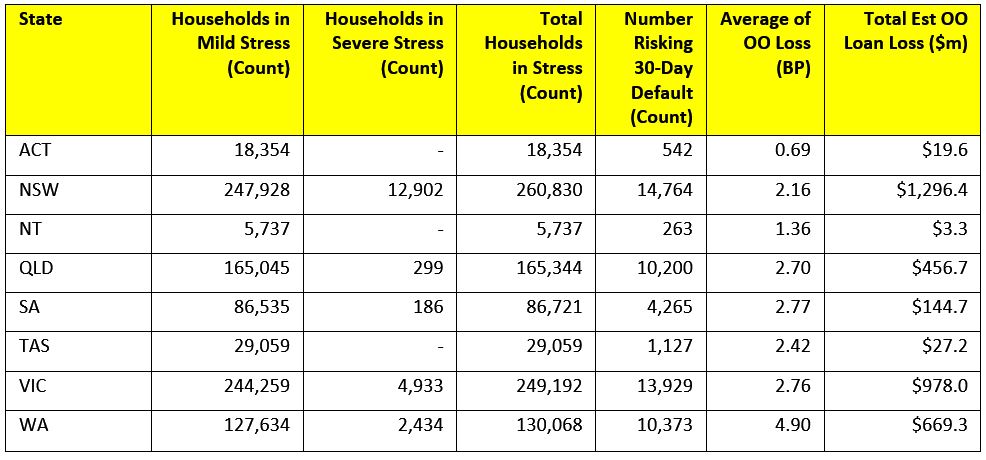

Regional analysis shows that NSW has 260,830 households in stress (254,343 last month), VIC 249,192 (254,028 last month), QLD 165,344 (158,534 last month) and WA has 130,068 (125,994 last month). The probability of default over the next 12 months rose, with around 10,373 in WA, around 10,200 in QLD, 13,929 in VIC and 14,764 in NSW.

The largest financial losses relating to bank write-offs reside in NSW ($1.3 billion) from Owner Occupied borrowers) and VIC ($978 million) from Owner Occupied Borrowers, which equates to 2.16 and 2.76 basis points respectively. Losses are likely to be highest in WA at 4.9 basis points, which equates to $669 million from Owner Occupied borrowers.

The largest financial losses relating to bank write-offs reside in NSW ($1.3 billion) from Owner Occupied borrowers) and VIC ($978 million) from Owner Occupied Borrowers, which equates to 2.16 and 2.76 basis points respectively. Losses are likely to be highest in WA at 4.9 basis points, which equates to $669 million from Owner Occupied borrowers.

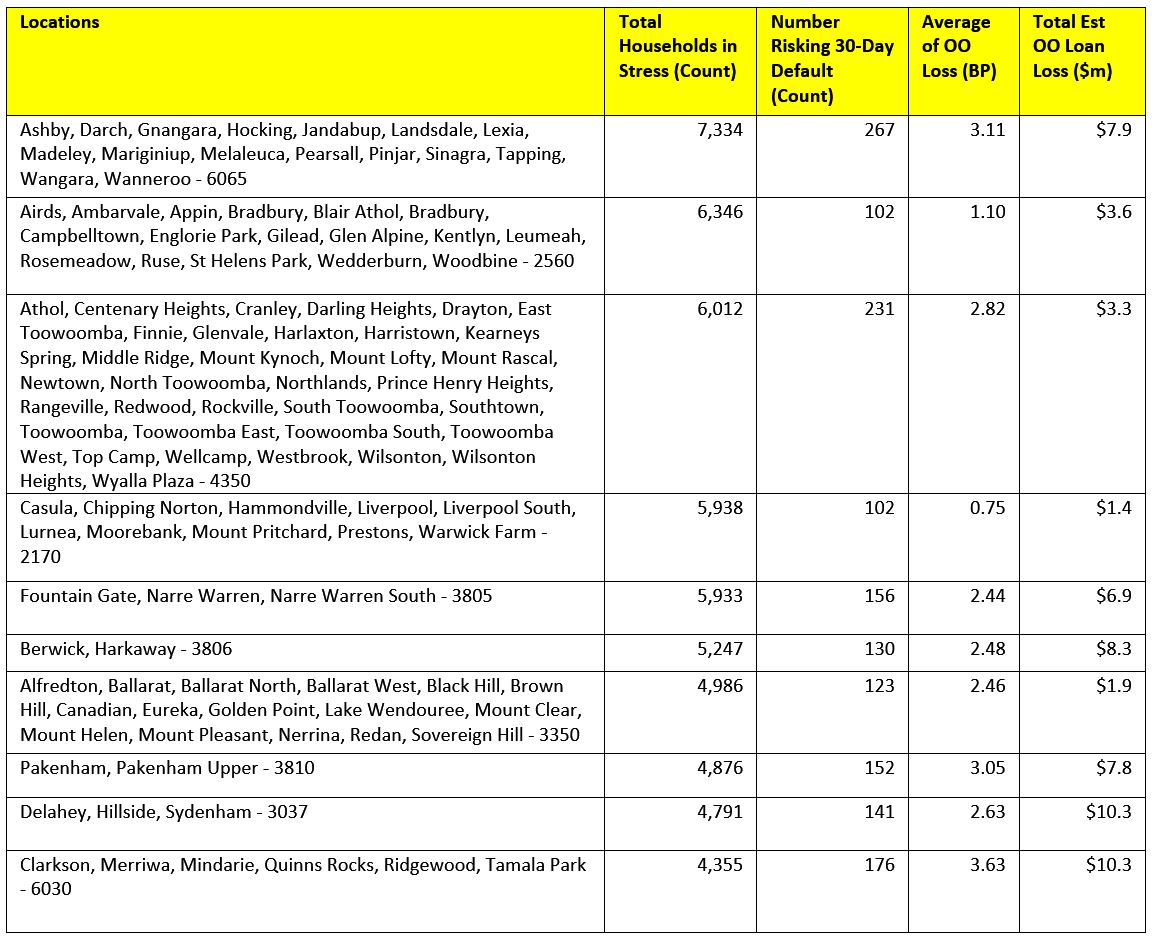

Here are the top post codes sorted by the highest number of households in mortgage stress.

[1] RBA E2 Household Finances – Selected Ratios September 2017 (Revised 2nd Feb 2018). The Bank has recently restated these ratios, taking them on average 10 points lower.

[1] RBA E2 Household Finances – Selected Ratios September 2017 (Revised 2nd Feb 2018). The Bank has recently restated these ratios, taking them on average 10 points lower.

You can request our media release. Note this will NOT automatically send you our research updates, for that register here.

[contact-form to=’mnorth@digitalfinanceanalytics.com’ subject=’Request The February 2018 Stress Release’][contact-field label=’Name’ type=’name’ required=’1’/][contact-field label=’Email’ type=’email’ required=’1’/][contact-field label=’Email Me The February 2018 Media Release’ type=’radio’ required=’1′ options=’Yes Please’/][contact-field label=”Comment If You Like” type=”textarea”/][/contact-form]

Note that the detailed results from our surveys and analysis are made available to our paying clients.

The UK will have a lot of home owners in mortgage stress should interest rates rise continue to rise.