We have just rerun our mortgage stress models, incorporating data to 1st March 2017. Household budgets remain under pressure, thanks to flat incomes and rising living costs – and some lifts in mortgage rates. You can read more about our approach to measuring mortgage stress here. Our current analysis concentrates on owner occupied mortgages.

Overall, 21.78% of households are in some degree of mortgage stress. We look at mild stress, meaning they are managing to meet repayments, but are doing so by cutting back on other expenditure, putting more on credit cards, and seeking to refinance or restructure to reduce monthly payments. 19.08% of households fall into this group. An additional 2.7% of households are in severe stress, meaning they are likely to miss repayments, or are in default, or are looking to sell. We look at household cash flow, not a set percentage of income going on the mortgage.

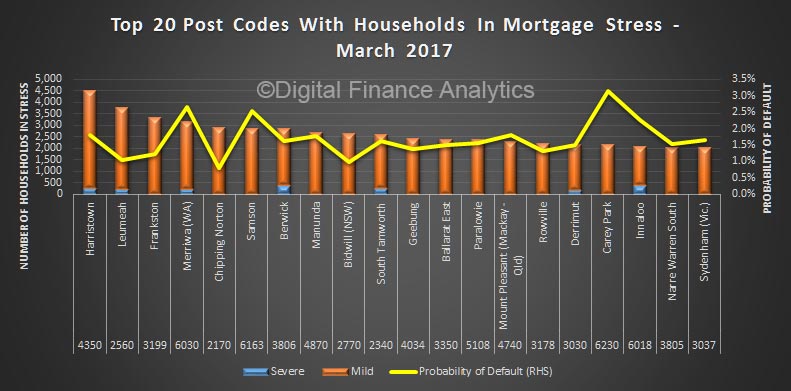

Here are the postcodes across Australia with the highest levels of stress.

Harristown, QLD 4350, which was the highest count in December 2016, still is first, followed by Leumeah NSW 2560. Leumeah is a suburb of Sydney, Macarthur/Camden, about 40 kms from the CBD. The average age of the people in Leumeah is 35 years of age. Around 37% of households there have a home loan mortgage.

Third is Frankston VIC 3199, which is a suburb of Melbourne, Bayside, It is about 39 kms from Melbourne. Frankston is in the federal electorate of Dunkley. The median/average age of the people in Frankston is 38 years of age. Around 30% of households here have a mortgage.

Third is Frankston VIC 3199, which is a suburb of Melbourne, Bayside, It is about 39 kms from Melbourne. Frankston is in the federal electorate of Dunkley. The median/average age of the people in Frankston is 38 years of age. Around 30% of households here have a mortgage.

Fourth highest is Merriwa 6030, a suburb of South Western, Heartlands, WA. It is about 35 kms from Perth in the electorate of Pearce. 41% of homes here are mortgaged. The average age of the people in Merriwa is 35 years of age.

Once again, remember interest rates are very low, and are expected to rise, so the OECD warning about the risks in the housing sector seem well placed.

Editors Note. We updated this post to reflect the total of mild and stress, when it first appeared, we sorted only on mild stress, which changed the results slightly – and we also added back the latest probability of default metrics as well.

2 thoughts on “Mortgage Stress Grinds Higher”