NAB gave their June 17 quarter update today. There were no surprises, with an unaudited statutory net profit of $1.6 billion and unaudited cash earnings of $1.7 billion, up 2% versus March 2017 Half Year quarterly average and 5% versus prior corresponding period.

Andrew Thorburn, Group CEO said:

The major bank levy became effective from 1 July 2017 and is estimated to cost NAB approximately $375 million annually, or $265 million post tax, based on our 30 June 2017 liabilities.

Separately, in July, the Australian Prudential Regulation Authority (APRA) announced a CET1 ratio target of at least 10.5% by January 2020 for major banks to be viewed as ‘unquestionably strong’, with finalisation of international capital reforms not expected to require any further increases to Australian requirements. NAB expects to meet APRA’s new capital requirements in an orderly fashion given the existing capital position and the timelines involved.

Revenue was up 2%, with growth in lending and improved Group net interest margin (NIM) partly offset by lower Markets and Treasury income. They reported a higher Group NIM largely reflects loan repricing and more favourable funding conditions. Expenses were up 2%, or 1% excluding redundancies, due to increased investment spend.

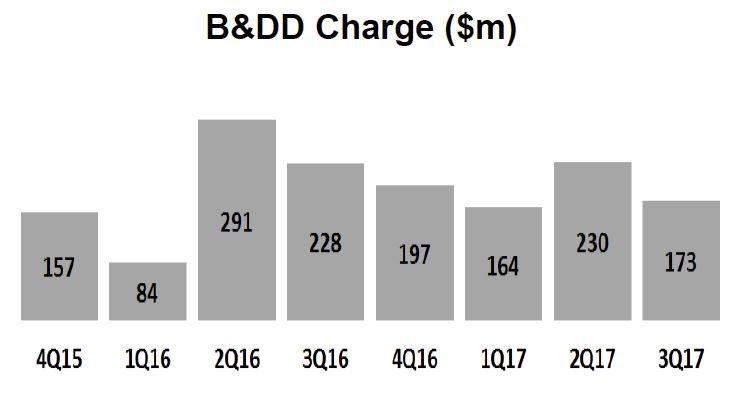

The biggest impact was a reduction in the bad debt charges. Bad and doubtful debt charges (B&DDs) fell 12% to $173 million, reflecting improved asset quality trends and non-repeat of the collective provision overlay for commercial real estate raised in the March 2017 Half Year.

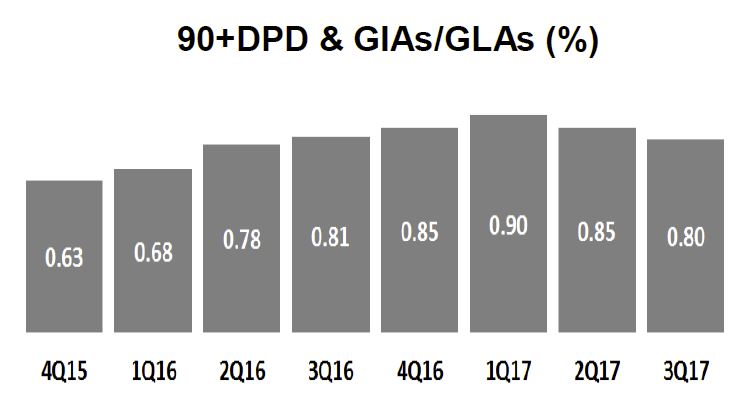

The ratio of 90+ days past due (DPD) and gross impaired assets (GIAs) to gross loans and advances (GLAs) of 0.80% declined 5 basis points (bps) from March 2017 mainly reflecting improved conditions for New Zealand dairy customers.

The ratio of 90+ days past due (DPD) and gross impaired assets (GIAs) to gross loans and advances (GLAs) of 0.80% declined 5 basis points (bps) from March 2017 mainly reflecting improved conditions for New Zealand dairy customers.

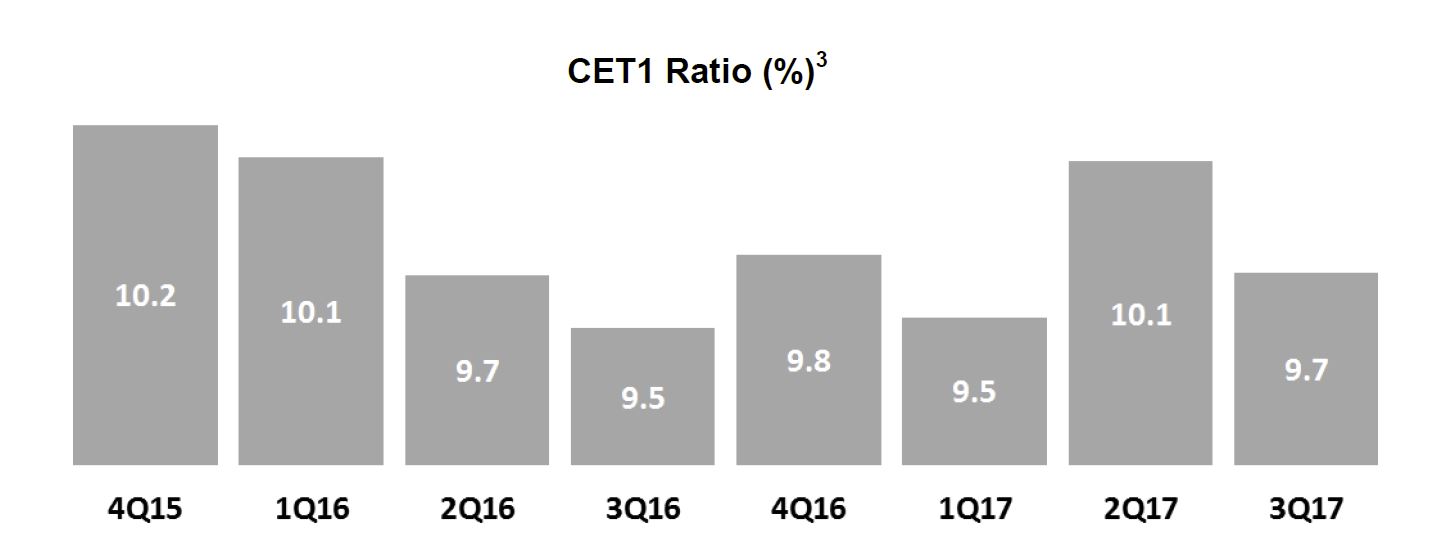

The Group Common Equity Tier 1 (CET1) ratio of 9.7%, compared to 10.1% at March 2017 mainly reflecting the impact of the interim 2017 dividend declaration and 17 bps for higher risk weights due to previously advised mortgage model changes.

The Group Common Equity Tier 1 (CET1) ratio of 9.7%, compared to 10.1% at March 2017 mainly reflecting the impact of the interim 2017 dividend declaration and 17 bps for higher risk weights due to previously advised mortgage model changes.

The Leverage ratio was 5.3% (APRA basis), the Liquidity coverage ratio (LCR) quarterly average was 127% and the Net Stable Funding Ratio (NSFR) was 108%.

The Leverage ratio was 5.3% (APRA basis), the Liquidity coverage ratio (LCR) quarterly average was 127% and the Net Stable Funding Ratio (NSFR) was 108%.

For this full year they remain confident of achieving more than $200 million in productivity savings and, excluding the impact of the bank levy, expect to deliver positive ‘jaws’.