Home prices are horribly high in Australia. I think we can all agree on that point. But what is really driving this? “Classic” economic theory is that supply and demand of property drives prices, so factors such a number of builds, population and migration, and planning controls are all to blame. Indeed, a recent paper from the RBA peddled the line, as does the property and real estate sector. State and Federal Governments also talk this up.

But, there is another factor which is, according to our simulations, is much more directly impacting home prices and affordability. That is availability of credit. And this is contentious, because classic economists (including those residing in most central banks) tend to argue that credit growth is a zero sum gain, in that if there is a loan on one side of the ledger, there is a creditor on the other side of the fence, so the net impact is zero.

Worse still, classic theory suggests that banks are limited in what they can lend by the availability of deposits. Neither of these statements is true, and it fundamentally changes the banking and banking supervision game.

Back in 2014 I discussed this, based on an insight from the Bank of England. Their Quarterly Bulletin (2014 Q1), was revolutionary and has the potential to rewrite economics. “Money Creation in the Modern Economy” turns things on their head, because rather than the normal assumption that money starts with deposits to banks, who lend them on at a turn, they argue that money is created mainly by commercial banks making loans; the demand for deposits follows. Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits.

More recently the Bank of Norway confirmed this, and said “The bank does not transfer the money from someone else’s bank account or from a vault full of money. The money lent to you by the bank has been created by the bank itself – out of nothing: fiat – let it become.”.

And even the arch conservative German Bundesbank said in 2017 recently “this means that banks can create book money just by making an accounting entry: according to the Bundesbank’s economists, “this refutes a popular misconception that banks act simply as intermediaries at the time of lending – ie that banks can only grant credit using funds placed with them previously as deposits by other customers

“.

Therefore the only limit on the amount of credit is peoples ability to service the loans – eventually.

With that in mind, we have built a scenario model, based on our core market model, which allows us to test the relationship between home prices, and a series of drivers, including population, migration, planning restrictions, the cash rate, income, tax incentives and credit. We are looking at national averages here, and we have smoothed the data from RBA and ABS to bring the trends out.

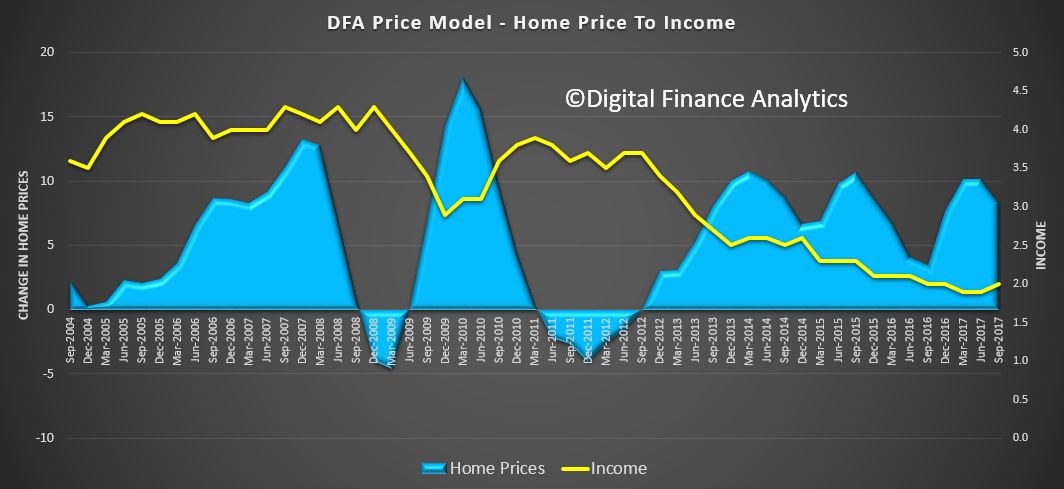

So first, lets walk through some of the relativity mapping. First we look at home prices relative to income growth. The blue area tracks changes in home prices since 2004, and the yellow line is the change in income. Most striking is that income growth and home prices are running in opposite directions, and have been especially since 2013. So income growth is not correlated to home price growth.

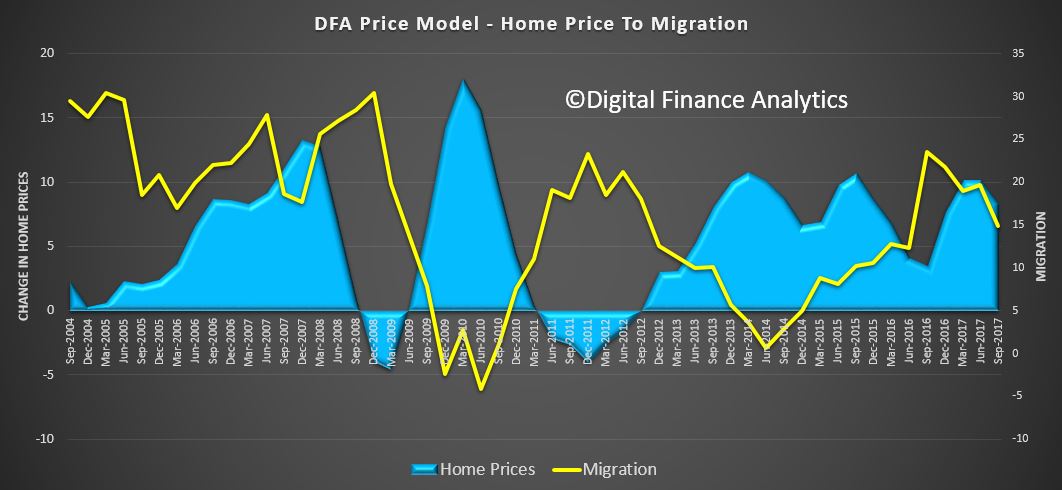

Next we look at home prices relative to migration and once again there is little alignment between home price growth and migration rates, this despite up to two thirds of population growth being fed from migration in recent years.

Next we look at home prices relative to migration and once again there is little alignment between home price growth and migration rates, this despite up to two thirds of population growth being fed from migration in recent years.

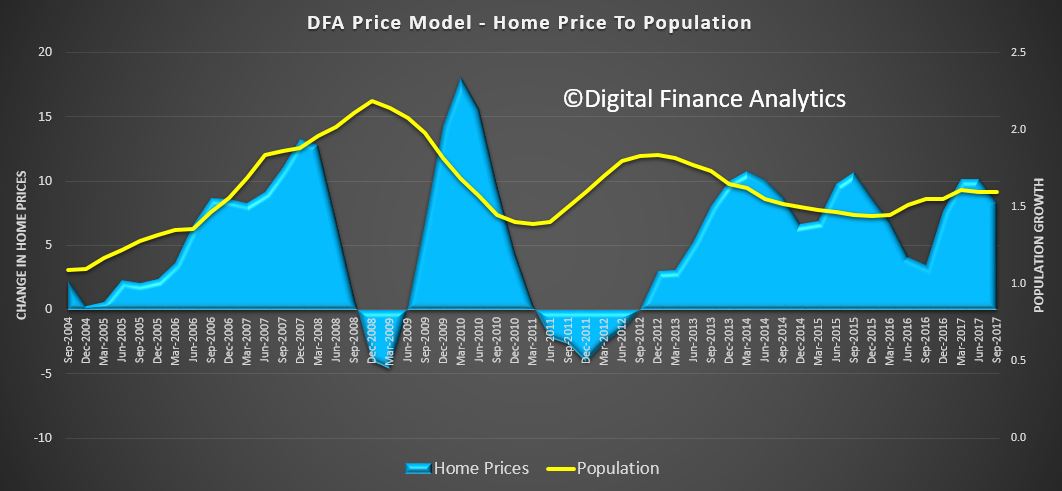

The relationship between overall population growth and home prices is equally disconnected. For example the rate of growth slowed from 2012 onward when we have had a large run up in home prices.

The relationship between overall population growth and home prices is equally disconnected. For example the rate of growth slowed from 2012 onward when we have had a large run up in home prices.

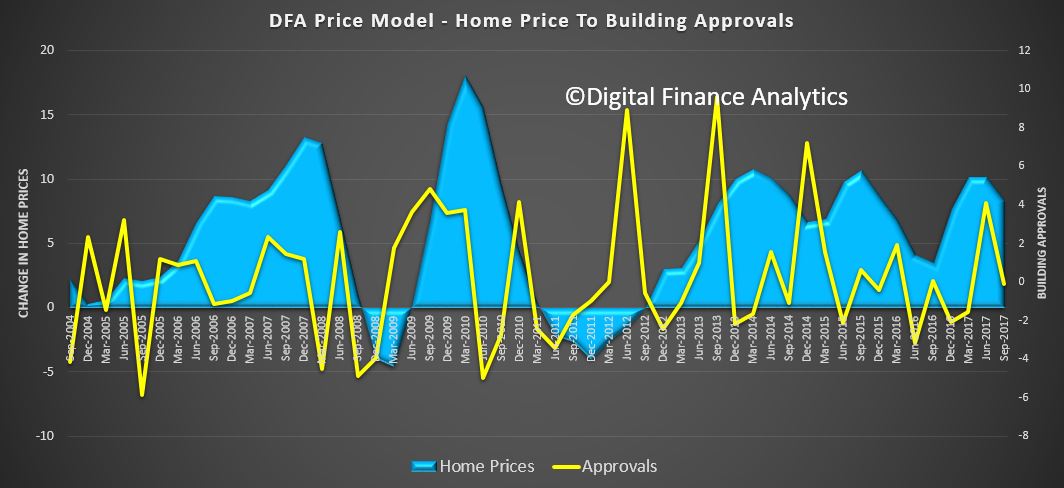

We then turned to building approvals, and even adjusting for the delay between approvals and commencements, there is little correlation.

We then turned to building approvals, and even adjusting for the delay between approvals and commencements, there is little correlation.

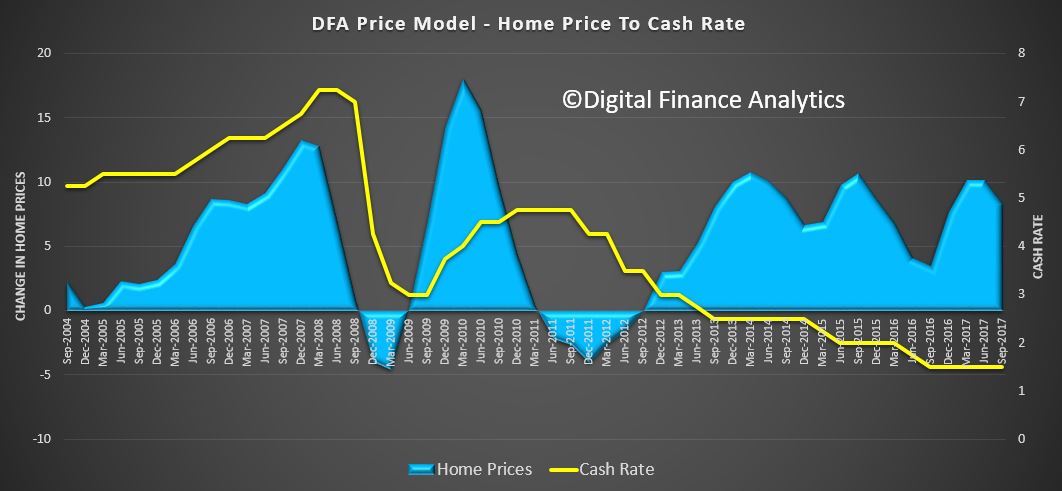

Up next is the RBA cash rate. Here we see an inverse linkage, in that as interest rates are cut, home prices expand. This also suggests that should rates rise, home prices will fall.

Up next is the RBA cash rate. Here we see an inverse linkage, in that as interest rates are cut, home prices expand. This also suggests that should rates rise, home prices will fall.

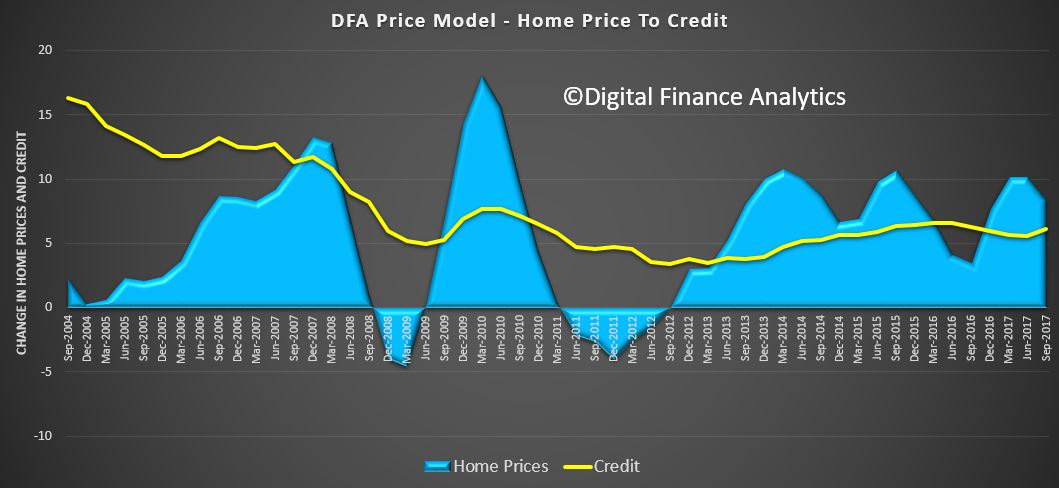

And here is the reason. The correlation between home prices and credit availability are clear to see. As credit rose from 2012 onward, home prices did too. It also suggests that if credit availability is tightened, we should expect prices to fall – take note, given the current tighter underwriting standards now in force. This is why I predict ongoing falls in property prices.

And here is the reason. The correlation between home prices and credit availability are clear to see. As credit rose from 2012 onward, home prices did too. It also suggests that if credit availability is tightened, we should expect prices to fall – take note, given the current tighter underwriting standards now in force. This is why I predict ongoing falls in property prices.

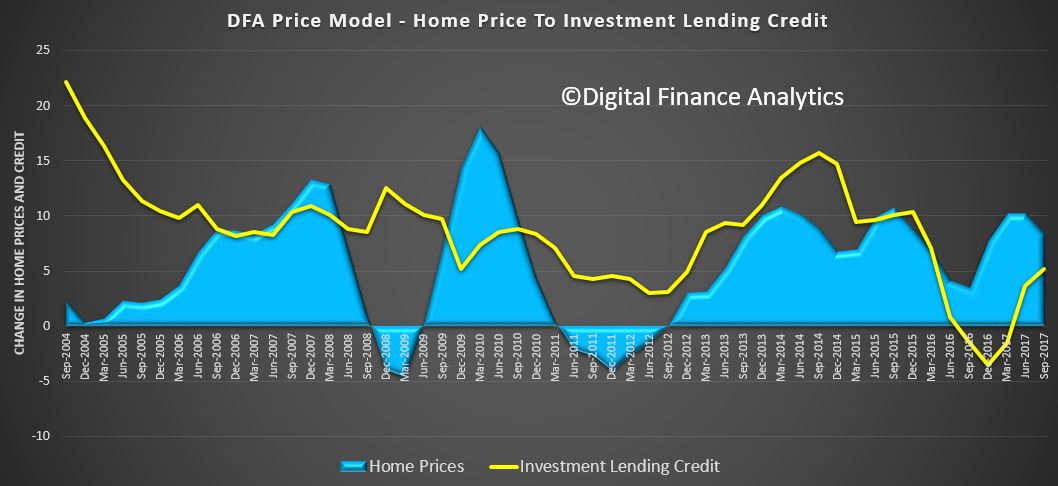

And more specifically, credit for property investment is even more strongly correlated. As we know investors are attracted by the capital growth, and also the capital gains and negative gearing tax breaks available.

And more specifically, credit for property investment is even more strongly correlated. As we know investors are attracted by the capital growth, and also the capital gains and negative gearing tax breaks available.

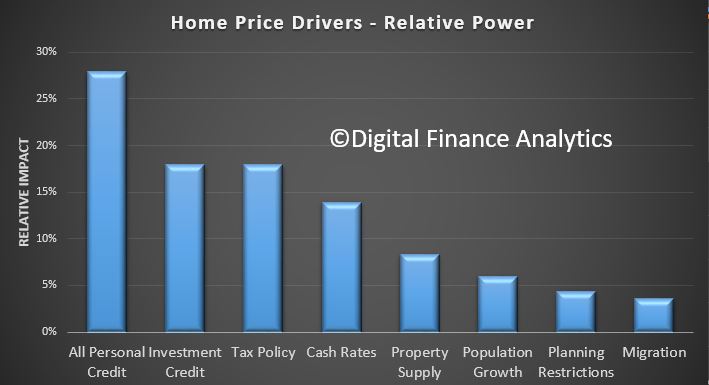

So then, we rolled all these factors into our overall model, and examined the relative influence of each on home prices. The four most powerful levers in terms of home prices is first overall growth in personal credit, including mortgages and other loans at 27% of total impact. Investment lending contributed a further 18%, followed by tax policy for investment property at 17% and the cash rate at 14%. The other factors, the ones which are spoken about the most, property supply, population growth, planning restrictions and migration, together make up just 22% of total impact. Or in other words, without addressing the credit elephant in the room, tax policy and interest rates, the chances of taming prices is low.

So then, we rolled all these factors into our overall model, and examined the relative influence of each on home prices. The four most powerful levers in terms of home prices is first overall growth in personal credit, including mortgages and other loans at 27% of total impact. Investment lending contributed a further 18%, followed by tax policy for investment property at 17% and the cash rate at 14%. The other factors, the ones which are spoken about the most, property supply, population growth, planning restrictions and migration, together make up just 22% of total impact. Or in other words, without addressing the credit elephant in the room, tax policy and interest rates, the chances of taming prices is low.

So now I can quote the recent Grattan report again, but with renewed vigour. “…much of the debate has focused on policies that are unlikely to make a real difference. Unless governments own up to the real problems, and start explaining the policy changes that will make a real difference, Australia’s housing affordability woes are likely to get worse”.

So now I can quote the recent Grattan report again, but with renewed vigour. “…much of the debate has focused on policies that are unlikely to make a real difference. Unless governments own up to the real problems, and start explaining the policy changes that will make a real difference, Australia’s housing affordability woes are likely to get worse”.

And the greatest of these is credit policy, which has for years allowed banks to magic money from thin air, to lend to borrowers, to drive up home prices, to inflate the banks balance sheet, to lend more to drive prices higher – repeat ad nauseam! Totally unproductive, and in fact it sucks the air out of the real economy and money directly out of punters wages, but make bankers and their shareholders richer.

One final point the GDP calculation we use in Australia is flattered by housing growth (triggered by credit growth). The second driver of GDP growth is population growth. But in real terms neither of these are really creating true economic growth.

To solve the property equation, and the economic future of the country, we have to address credit. But then again, I refer to the fact that most economists still think credit is unimportant in macroeconomic terms!

The alternative is to continue to let credit grow well above wages, and lift the already heavy debt burden even higher. Current settings are doing just that, as more households have come to believe the only way is to borrow ever more. But, that is, ultimately unsustainable, and why there will be an economic correction in Australia, and quite soon.

Is it the case that a better governance model needs to be wrapped around fractional reserve banking to direct capital creation into productive enterprises or that the moral hazard implicit in placing money creation in private hands is not worth the risk to the greater good ?

Banking appears to be, as Paul Volker has noted, an industry with almost no innovation. It would serve everyone much better if it was a smaller, simpler and more predictable business.