Today we discuss which post codes will be most impacted by the interest only mortgage loan reset issue, and update our estimates of the number and value of loans likely to be impacted. This received media coverage in the AFR and the Australian over the weekend.

We discussed recently the size of the interest only loan mortgage portfolio, in the light of tighter lending standards now in place. We also discussed the issue in a recent edition of the Property Imperative Weekly video blog.

Here are some facts.

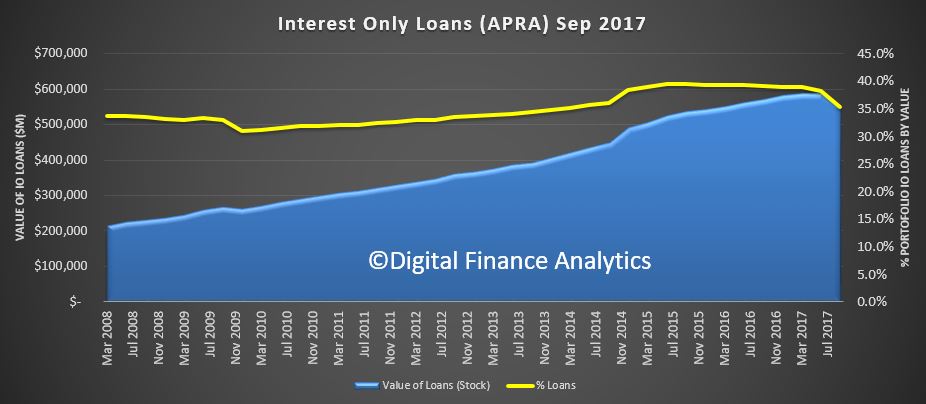

The value of IO loans in Sept 2017 was $549 billion, down from a peak of $587 billion in March 2017. The number of loans outstanding was 1.56 million loans, down from a peak of 1.69 million loans in December 2016.

Lenders are now required to make a more detailed assessment of a borrower when the loan comes up for periodic review, typically after 5, or in some cases 10 years. Some of the changes we are seeing are:

Lenders are now required to make a more detailed assessment of a borrower when the loan comes up for periodic review, typically after 5, or in some cases 10 years. Some of the changes we are seeing are:

- rental income cut to 80% of flows, to allow for vacancy periods

- borrowers must have a stated concrete plan to repay the capital element of the loan (vague “from property sale”, probably wont be sufficient, especially given current home price movements).

- overall borrower income and serviceability to be assessed

- loans to be assessed as if they were a principal and interest loan

In addition, loans must be “suitable” taking into account the overall financial footprint and objectives of the borrowers (and this must be documented in case of later action). Otherwise the loan could be voided.

If an interest only loan comes up for review, and it fails to be renewed because it falls outside current assessments, borrowers have limited choices.

- They may shop around for an alternative lender. Most banks are following the same regulatory guidelines (though there are some differences as to how the rules are being applied). Non-banks are less restricted at the moment (but watch this space..).

- They may move to a principal and interest loan, which could double the monthly repayments. Bearing in mind half of investment properties are under water on a net rental basis, this means finding funds from other sources. If multiple properties and loans are involved, this could be a cascading problem

- Arrange to sell the property. We are already seeing some forced sales, especially in Sydney and Melbourne. More will follow.

Recent UBS research suggested that some borrowers are not aware they have an IO loan, so might get a very nasty surprise when then bank contacts them!

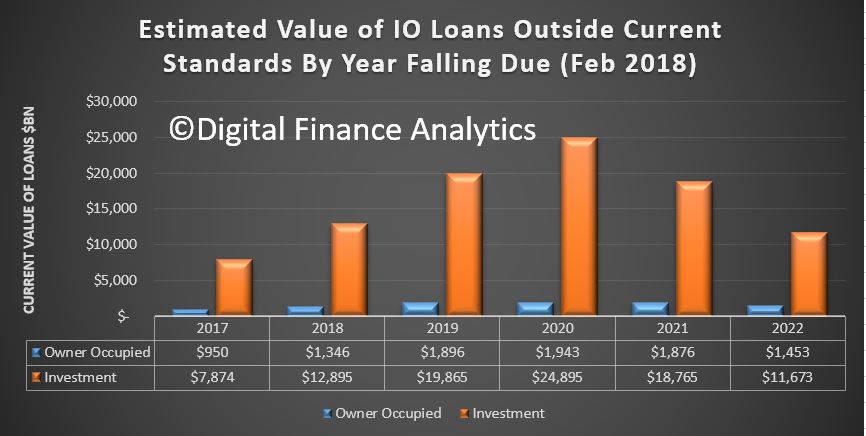

Using data from our household surveys to end February we re-ran our analysis of IO loans which will fall outside serviceability currently. We had previously estimated $60 billion were exposed, but this has now risen, first because we extended the analysis by a year, and second because we updated the lending standards which have become tighter in recent weeks. It is now a $100 billion problem on a $550 billion loan book. More than 220,000 households will be caught over the next few years.

Here is the state breakout.

Here is the state breakout.

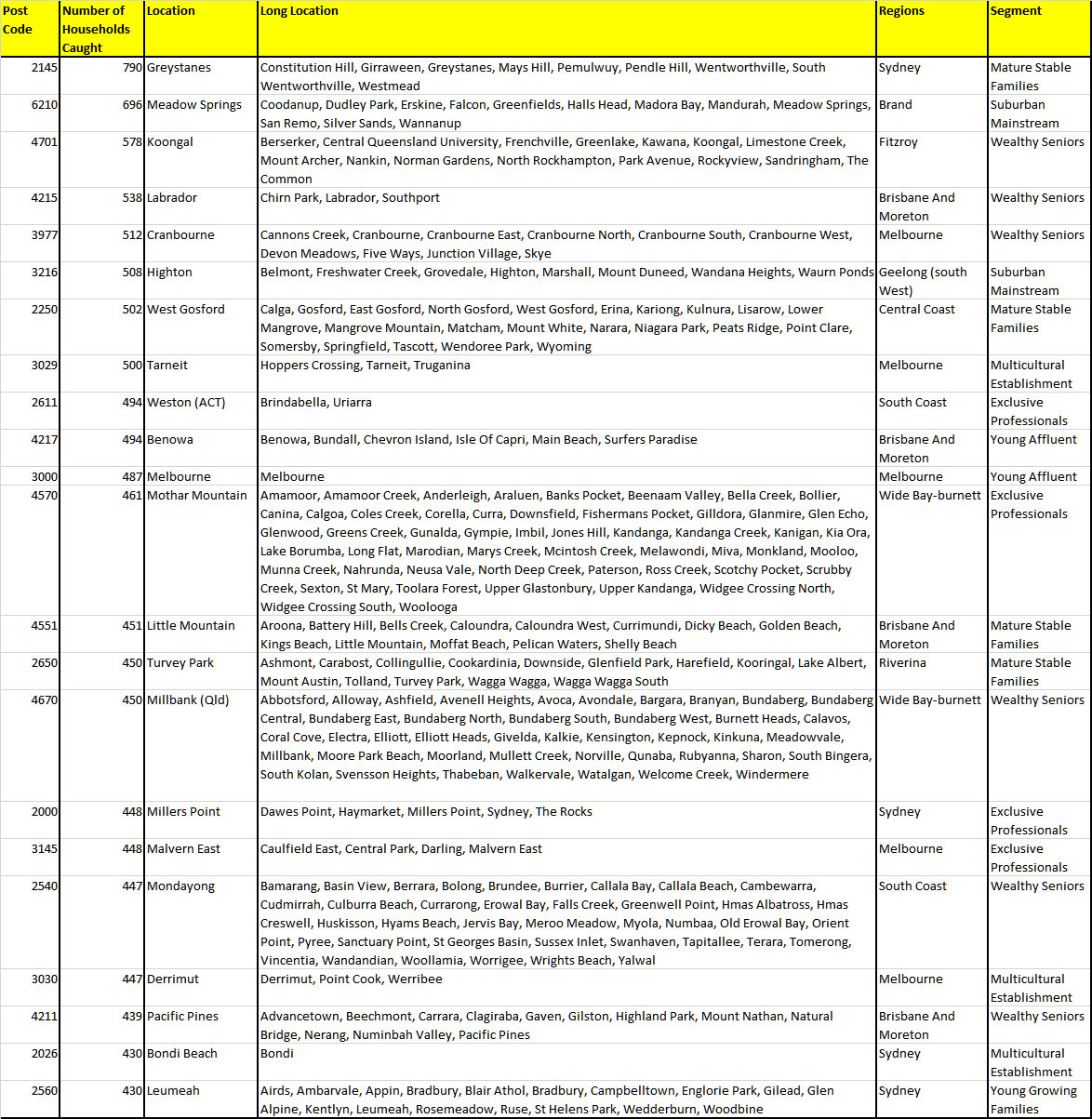

We can then identify the post code where the borrowers are residing. This may of course be different from where the investment properties are located. Here is the list of top post codes impacted. Click to view the larger version. Note the household segments which are impacted are predominately more affluent ones!

We can then identify the post code where the borrowers are residing. This may of course be different from where the investment properties are located. Here is the list of top post codes impacted. Click to view the larger version. Note the household segments which are impacted are predominately more affluent ones!

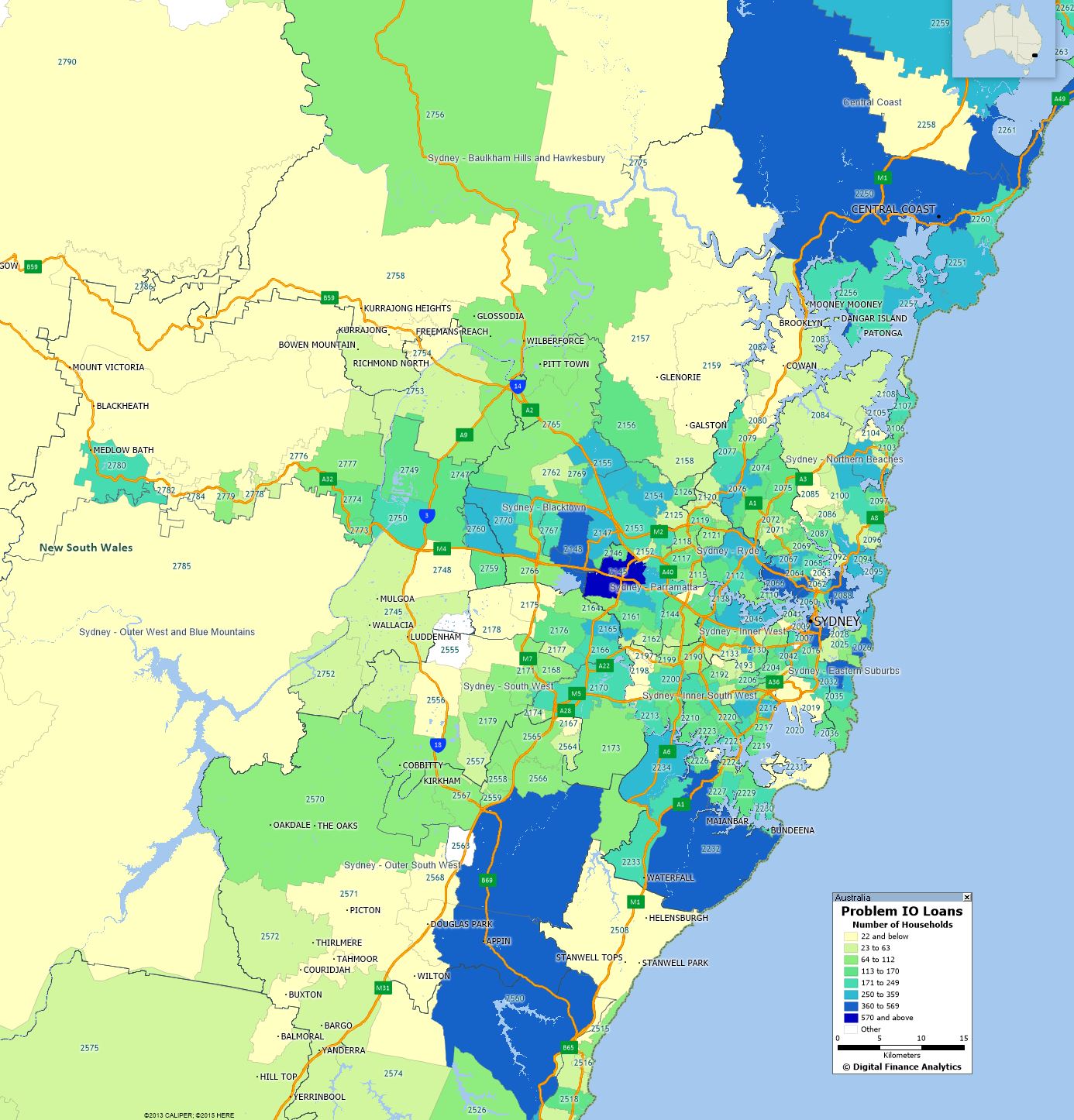

Finally, to get the juices flowing here is the geo-mapping for Greater Sydney. We will share other locations in subsequent posts. Again you can click on the map to view a larger version.

Finally, to get the juices flowing here is the geo-mapping for Greater Sydney. We will share other locations in subsequent posts. Again you can click on the map to view a larger version.

This is a significant issue, and mirrors the US in 2005 onwards as loans were reset to higher rates, lifting repayments. But the difference in Australia is that the households most impacted appear to be more affluent. In theory, therefore they may be able to rearrange their finances, but investors of course have the freedom to exit the market. Expect more forced sales in the months ahead, with consequential downward pressure on home prices as a result.

This is a significant issue, and mirrors the US in 2005 onwards as loans were reset to higher rates, lifting repayments. But the difference in Australia is that the households most impacted appear to be more affluent. In theory, therefore they may be able to rearrange their finances, but investors of course have the freedom to exit the market. Expect more forced sales in the months ahead, with consequential downward pressure on home prices as a result.