The Australian Prudential Regulation Authority (APRA) today released the results of a review of remuneration practices at large financial institutions which found considerable room for improvement in the design and implementation of executive remuneration structures.

The review examined whether policies and practices in regulated institutions were meeting the objectives of APRA’s prudential framework: that remuneration frameworks operate to encourage behaviour that supports risk management frameworks and institutions’ long-term financial soundness.

APRA’s review comprised detailed analysis of executive remuneration practices and outcomes from a sample of 12 regulated institutions across the authorised deposit-taking institutions (ADIs), insurance and superannuation sectors. The sample of institutions reviewed collectively accounts for a material proportion of the total assets of the Australian financial system.

The review found that remuneration frameworks and practices did not consistently and effectively promote sound risk management and long-term financial soundness, and fell short of the better practices set out in APRA’s existing guidance.

Chairman Wayne Byres said APRA encouraged all regulated institutions to review their remuneration frameworks and address any areas where APRA’s findings indicated room for improvement.

“Both the design and implementation of performance-based remuneration must support effective risk management and the long-term financial soundness of each institution. In this regard, there is considerable room for improvement,” Mr Byres said.

The report identified the need for improvement in:

ensuring practices were adopted that were appropriate to the institution’s size, complexity and risk profile;

the extent to which risk outcomes were assessed, and weighted, within performance scorecards;

enforcement of accountability mechanisms in response to poor risk outcomes; and

evidence of the rationale for remuneration decisions.

In response to the findings, APRA will consider ways to strengthen its prudential framework. A future review of the relevant prudential standards and guidance will take account of the forthcoming Banking Executive Accountability Regime (BEAR), as well as international best practice.

Mr Byres said: “APRA does not believe institutions should be satisfied with simply meeting the minimum requirements on remuneration.

“Well-targeted incentive schemes and firmly enforced accountability systems should be viewed not simply as a matter of regulatory compliance but as essential for sustained commercial success.

“Boards and senior executives should consider the findings of this review and take action to better align their remuneration arrangements with good risk management and the long-term soundness of their institutions.”

Any revisions to the prudential framework will be subject to APRA’s usual practices of stakeholder consultation and engagement.

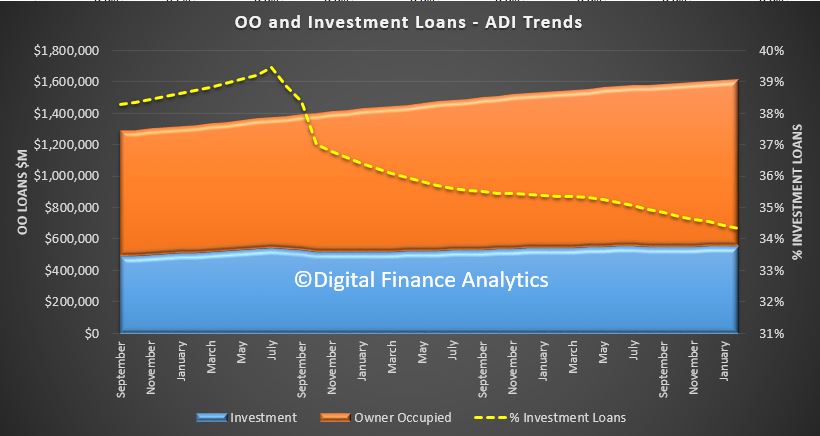

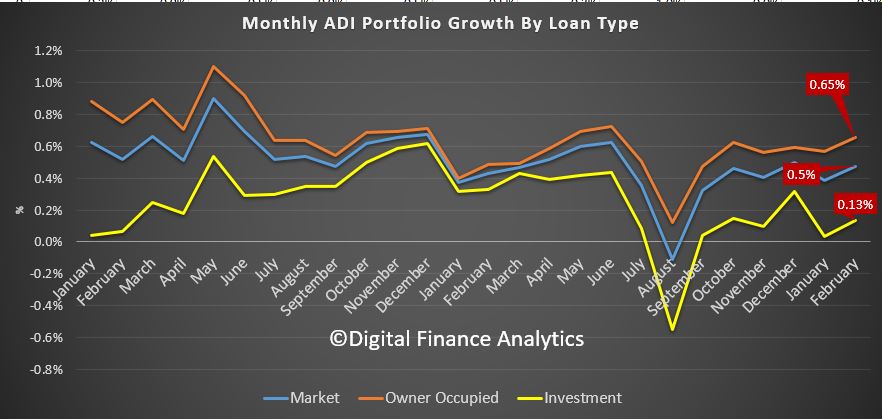

Total mortgage loans on book grew by 0.5%, or if annualised at a rate of 5.7% (still way above inflation and wages growth, so overall household debt is still growing!), to $1.61 trillion. Momentum is drifting up. Within that owner occupied loans rose 0.65% to $1.06 trillion and investment loans rose 0.13% to $553 billion.

The share of investment loans now comprises 34.3% of all loans on book, so the drift down continues as investors flee the market, whilst owner occupied buyers are stronger, but leading to a small net rise. This is not sustainable. The regulators are still keen to see growing consumer debt to support economic growth, never mind the long term consequences.

Here is the monthly tracker, which shows the small rise.

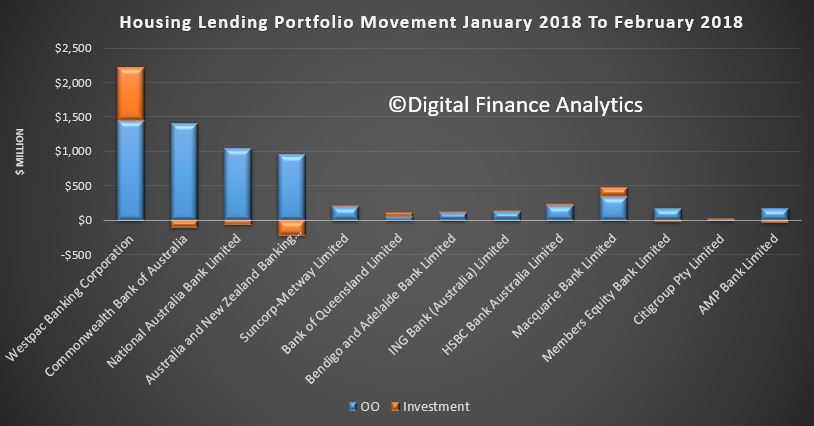

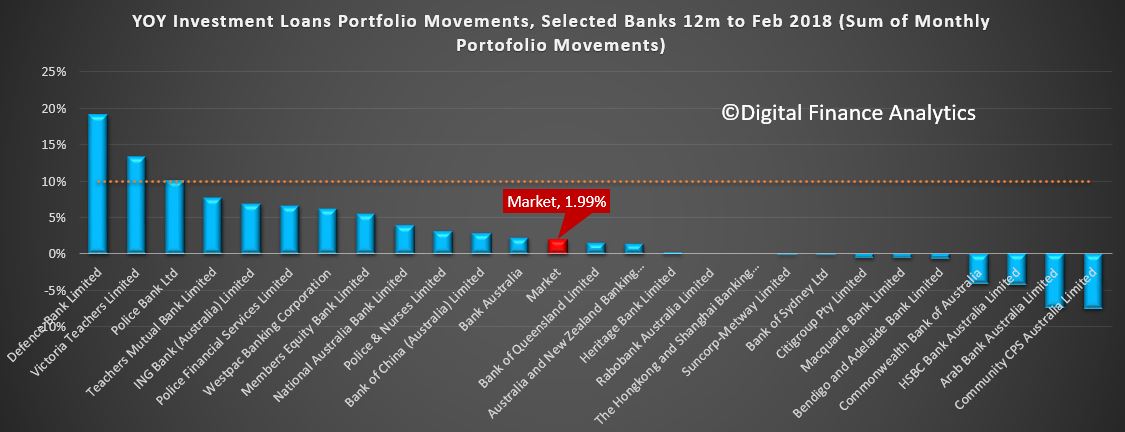

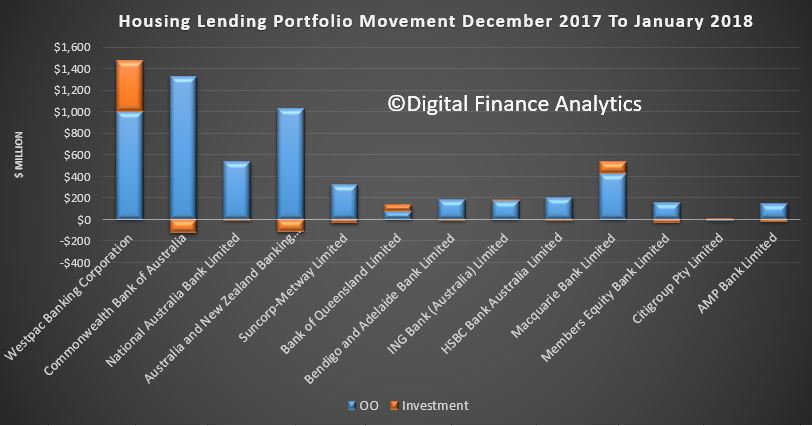

The portfolio movements of the individual banks highlights Westpac’s strong growth in investment loans, compared with the other three majors. Macquarrie is also growing investment loans.

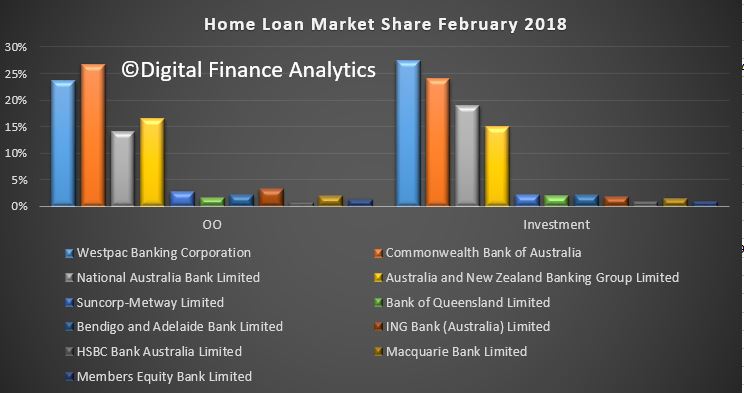

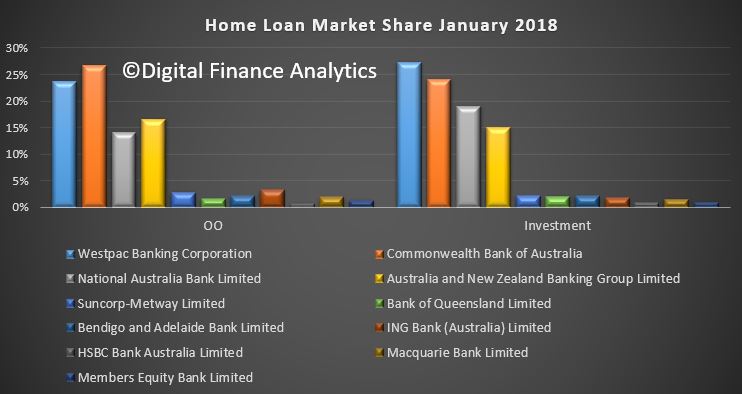

The overall market shares have hardly changed with CBA the largest owner occupied lender and Westpac the largest investment loan lender. We found out quite recently they have around 50% of their investment loans in the interest only category.

The portfolio growth of investment lending is mostly well below the 10% APRA speed limit, which of course, based on their recent statements, is in any case now being superseded by serviceability metrics.

We will look at the RBA data which is also out today, to see movements at a market level, and specifically the trends in the non-bank sector, which we expect to be stronger.

APRA Chairman Wayne Byers made an interesting opening statement today in his appearance before the House of Representatives Standing Committee on Economics, Canberra

First he assures that lending tightening is going to plan, and second there are no plans for a deposit bail-in as might be needed to save a bank from collapse.

But, hold on, listen to his recent reply to the senate on mortgage fraud. There the question was “has APRA found any evidence of misconduct among the major lenders?” Answer, essentially was NO.

Now compare that with the evidence from the Royal Commission, where fraud was well among the collection of significant issues explored.

So I simply ask. Did APRA really not know about the fraud which is clearly in the system? If they did, then the reply to Parliament looks dodgy. But worse, if they really did not have evidence of fraud, then we ask, should they have? To which I think the answer is YES, after all you are the regulator!

Either way this looks really shoddy. Come on APRA. Time to come clean!

Anyhow, here is is statement:

APRA’s 2016/17 Annual Report was tabled some months ago but many of the issues discussed within it remain highly relevant today, reflecting APRA’s ongoing agenda to continue to build resilience in the financial system. As we said in the Report, and I repeat regularly in speeches, building resilience when times are relatively favourable is far easier than trying to restore resilience after a period of adversity.

While there has been a great deal of focus in recent weeks on past conduct being examined by the Royal Commission, there are many other issues that are critical into the future for establishing and maintaining a financial system in which the Australian community can have confidence as to its resilience and safety. I would like to say a few words about some of those areas this morning.

As we have regularly discussed at past hearings, APRA is maintaining a strong focus on the quality of new mortgage lending, and measures to reinforce sound lending standards. Although there are differing views as to the level of competition in the housing lending market, we observed that the type of competition that was occurring was clearly unhealthy: the steady erosion of lending standards in the face of strong competitive pressures to generate volume and grow market share. As a result, we have taken a range of measures to moderate the volume of new lending with higher risk characteristics while stronger lending standards are being reintroduced, backed by higher capital requirements for higher risk portfolios.

In our view, these interventions are achieving their purpose. The quality of new lending today is higher than it has been for some time. However, there is more to be done to make sure the improvements in policies are truly embedded into ongoing practices. So we will inevitably need to continue to allocate significant resources to this issue in the year ahead, making sure the industry delivers on its commitment to do better in the future.

Another critical component of a resilient financial system is ensuring we have a strong regulatory framework, particularly in times of crisis. This framework has been strengthened with the recent passage of the Financial Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Bill 2017. The Bill provides a welcome and substantial improvement to APRA’s crisis management powers, better equipping us to deal with the actual or imminent failure of a financial institution. It is an underappreciated but essential piece of infrastructure that maximises the public sector’s ability to preserve an orderly financial system in times of stress.

Concerns have been expressed in some quarters that the Bill might allow APRA to confiscate or otherwise use depositors’ money to save a failing bank. I would therefore like to use this opportunity to state clearly that that is most definitely not the case. There is no such power in the Bill. Indeed, APRA’s purpose under the Banking Act is to protect depositors, and the idea of ‘bailing in’ deposits would be anathema to that core purpose.

The third important matter that I’d like to highlight this morning is cyber risk. Earlier this month, APRA proposed its first cross-industry prudential standard on information security management, in response to the growing threat of cyber-attacks. The package of measures is aimed at shoring up the ability of APRA-regulated entities to both repel cyber adversaries and respond swiftly and effectively in the event of a breach of their defences.

Australian financial institutions are among the top targets of cyber criminals seeking money or customer data, and evidence suggests the threat is accelerating. This is increasingly one of the most important risks the financial system faces – affecting large and small institutions alike, and stretching across all industries. It is almost inevitable that institutions’ defences will be breached in some way at some time, and no longer implausible to suggest that a cyber-attack could be sufficiently severe to take a regulated institution out of business entirely, with significant losses as a result. The financial institutions we supervise will need to place greater emphasis on, and devote more resources to, this risk into the future, as will APRA. The new standard provides an important new framework within which this will occur.

The fourth area I’d like to mention is the issue of governance. In February this year, APRA announced a package of proposed measures designed to build resilience and improve governance and decision-making in the private health insurance sector. The measures are aimed at introducing stronger prudential standards that have successfully lifted capabilities across other APRA-regulated industries, at a time when the private health insurance sector faces significant strategic and operational challenges. Our emphasis on a strong strategic focus also extends to superannuation. As we said in our Annual Report, we have upped the ante on RSE licensees that appear not to be consistently delivering quality member outcomes, or are not appropriately positioned for future effectiveness and sustainability. To that end, it is pleasing to note that this work is delivering results, with a number of superannuation funds restructuring activities and products in order to deliver better member outcomes, in response to APRA’s observations.

Also related to governance is a review we are close to finalising on the policies and practices in setting senior executive remuneration at large financial institutions. This examined the extent to which remuneration outcomes were consistent with good risk management and long-term financial soundness. We will be publishing the results of this study shortly.

The final major initiative that I would like to mention is the major data transformation program we are undertaking to ensure APRA itself keeps pace with advancements in data, analytics and technology. As part of this program, we have recently embarked on our most substantial program of stakeholder engagement to date as we seek input from the industry into the design and implementation of our next generation data collection tool. This will be the foundation by which we are able not just to improve our own supervisory effectiveness, but also provide more information and transparency to the broader community about the financial health of the industries we supervise.

With those remarks on some of our major work streams, my colleagues and I are happy to answer the Committee’s questions.

The Australian Prudential Regulation Authority (APRA) today announced that it has granted approval to ING Bank (Australia) Limited to begin using its internal models to determine its regulatory capital requirements for credit and market risk, commencing from the quarter ended 30 June 2018.

ING is the first authorised deposit-taking institution (ADI) to be accredited since APRA revised the accreditation process in 2015. Consistent with suggestions from the 2014 Financial System Inquiry, APRA’s changes were intended to make the process more accessible for ADIs to achieve accreditation, without weakening the overall standards that advanced accreditation requires.

APRA continues to engage with other ADIs seeking accreditation to use internal models for calculating regulatory capital requirements.

APRA today released a package of measures, titled Information Security Management: A new cross-industry prudential standard, for industry consultation. The package is aimed at shoring up the ability of APRA-regulated entities to repel cyber adversaries, or respond swiftly and effectively in the event of a breach.

The proposed new standard, CPS 234, would require regulated entities to:

clearly define the information security-related roles and responsibilities of the board, senior management, governing bodies and individuals;

maintain information security capability commensurate with the size and extent of threats to information assets, and which enables the continued sound operation of the entity;

implement information security controls to protect its information assets, and undertake systematic testing and assurance regarding the effectiveness of those controls;

have robust mechanisms in place to detect and respond to information security incidents in a timely manner; and

notify APRA of material information security incidents.

Executive Board Member Geoff Summerhayes said the draft standard built on prudential guidance first released by APRA in 2010 and backed it with the force of law.

“Australian financial institutions are among the top targets of cyber criminals seeking money or customer data, and the threat is accelerating,” Mr Summerhayes said.

“No APRA-regulated entity has experienced a material loss due to a cyber incident, but a significant breach is probably inevitable. In a worst-case scenario, a cyber attack could even force a company out of business.”

Key areas where APRA is hoping to lift standards include assurance over the cyber capabilities of third parties such as service providers, and enhancing entities’ ability to respond to and recover from cyber incidents.

“Cyber security is generally well-handled across the financial sector, but with criminals constantly refining and expanding their tools and capabilities, complacency is not an option,” Mr Summerhayes said.

“Implementing legally binding minimum standards on information security is aimed at increasing the safety of the data Australians entrust to their financial institutions and enhance overall system stability.”

Submissions on the package are open until 7 June. APRA intends to finalise the proposed standard towards the end of the year, with a view to implementing CPS 234 from 1 July next year.

Let’s talk about the bank bail-in conundrum. A couple of weeks back I discussed whether bank deposits in Australia would be safe in a crisis. The video received more than 1,400 views so far, and has prompted a number of important questions from viewers. So today I update the story, and addresses some of the questions raised. The bottom line though is I think we are being sold a pup, which by the way refers to a confidence trick originating in the Late Middle Ages!

Watch the video, or read the transcript.

First, a quick recap, for those who missed the first video. Officially, in Australia currently bank deposits are protected up to $250,000 per person by a Government Guarantee – The Financial Claims Scheme. For banks, building societies and credit unions incorporated in Australia, the FCS provides protection to depositors up to $250,000 per account-holder per ADI according to APRA. Only deposit products provided by ADIs supervised by APRA were eligible to be covered. Amounts between $250,000 and $1 million are not be covered under the Guarantee Scheme. Above $1m banks can elect to pay a fee to the Government for this for protection, but none do. However, as we will see there are even questions about the sub $250k. But note this, the FCS can only be activated by the Australian Government, whilst APRA is responsible for administering the Scheme.

The RBA says upon its activation, APRA aims to make payments to account-holders up to the level of the cap as quickly as possible – generally within seven days of the date on which the FCS is activated. The method of payout to depositors will depend on the circumstances of the failed ADI and APRA’s assessment of the cost-effectiveness of each option. Payment options include cheques drawn on the RBA, electronic transfer to a nominated account at another ADI, transfer of funds into a new account created by APRA at another ADI, and various modes of cash payments.

The amount paid out under the FCS, and expenses incurred by APRA in connection with the FCS, would then be recovered via a priority claim of the Government against the assets of the ADI in the liquidation process. If the amount realised is insufficient, the Government can recover the shortfall through a levy on the ADI industry. Ok, maybe in the case of a single failure

Now, since the Global Financial Crisis, regulators have been working on ways to avoid a tax payer based rescue in a crash, because for example, the UK’s Royal Bank of Scotland was nationalised in 2007. This cost tax payers dear, so regulators want measures put in place to try to manage a more orderly transition when a bank gets into difficulty.

The New Zealand the Open Bank Resolution (not to be confused with Open Banking) is the clearest example of a so called bail-in arrangement. Customer’s money, held as savings in a distressed bank can be grabbed to assist in a resolution in a time of crisis. The thinking behind it is simple. Banks need an exit strategy in case of a problem, and Government bail-outs should not be an option. So a manager can be appointed to manage through the crisis. They can use bank capital, other instruments, like hybrid bonds and deposits to create a bail-in. This approach to rescuing a financial institution on the brink of failure makes its creditors and depositors take a loss on their holdings. This is the opposite of a bail-out, which involves the rescue of a financial institution by external parties, typically governments using taxpayer’s money.

So what about Australia? Well, the Financial Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Bill 2017 is now law, having been through a Senate Inquiry. It all centers on the powers which were to be given to APRA to deal with a banking collapse.

In the bill, there is a phrase “any other instrument” in the list of bail-in items. Treasury said, “the use of the word ‘instrument’ is intended to be wide enough to capture any type of security or debt instrument that could be included within the capital framework in the future. It is not the intention that a bank deposit would be an ‘instrument’ for these purposes”. Yet, deposits were not expressly excluded.

In fact, when the Bill came back to Parliament it went through both houses with minimal discussion (and members on the floor, the chambers were all but empty). And despite a proposal being drafted and with Government Lawyers in parallel to exclude deposits, it was passed on 14th February without this change, leaving the door wide open under “any other instrument”. All the verbal assurances are meaningless.

So, the result appears to be APRA has wider powers now to handle a bank in crisis, and deposits are potentially accessible. They are not expressly excluded, and in a time of crisis, could be bailed-in.

But this is not the end of the story. Treasurer Morrison issued a letter to Liberal government members with some talking points to justify this actions, in response to a wave of protests. But in so doing, he raises more questions.

The first point is that the Deposit Guarantee scheme (the one up to $250k) is not currently active. The Government would need to activate it, and can only do so when an institution fails. This is important because it means that in theory at least, APRA could mount a deposit bail-in before the Government activates the deposit protection scheme. Consider what would happen if many banks all got into difficulty at the same time, as could be the case in a wider banking crisis – after all, they all have similar banking models.

The second point is that the Treasurer makes reference to the 1959 Banking Act, and says that depositors have a claim above other creditors in a bank failure. But in fact the 1959 Act says depositors do indeed rank ahead of other unsecured creditors, but that means the secured creditors come first. So would anything be left in case of a bank failure given the massive exposure to property?

Next, the letter says APRA has now enhanced powers to protect the interests of depositors – not deposits. And looking at the New Zealand situation the bail-in provisions there are framed to do just this, by utilising deposits to help keep the bank afloat, thus protecting depositors. The Reserve Bank of New Zealand says this is IN THE INTERESTS OF DEPOSITORS.

Oh, and finally, Morrison says the way the Bill went into Law was quite normal by being listed in the Senate Order of Business, meaning members had the opportunity to debate the bill if they had wanted to. In fact, only seven Senators were there despite really needing a quorum of 19, but there is a get out in that a quorum is only needed if a division was called, and in this case it was simply nodded through. Democracy in action.

So there you have it. No Deposit Protection currently exists. Its limited to $250k per person if activated by the Government, at their discretion, and the legalisation leaves the door wide open for a New Zealand style of Bail-In. Not a good look.

So what should Savers do? Well, this is not financial advice, but the New Zealand view is that savers should make a risk assessment of banks and select where to deposit funds accordingly. But I am not sure how you do that, given the current low level of disclosures. APRA releases mainly aggregate data and protects the confidentially of individual banks as they are required to do under the APRA act.

Next, do not assume deposits are risk free, they are not. This means lenders should be offering rates of return more reflective of the risks we are taking, currently they are not (in fact deposit rates are sliding, as banks seek to repair margins). You might consider spreading the risks across multiple institutions

Consider alternative savings options (which are limited). Clearly, property, stocks and shares and even crypto currencies are all risky – there are no safe harbours. I guess there is always the mattress.

One other point to make. Several people are calling a bill to bring a Glass-Steagall split between core banking operations and the speculative aspects of banking. Glass-Steagall was enacted in the US in 1933 after the great crash, separating commercial and investment banking and preventing securities firms and investment banks from taking deposits. But in 1999 the US Congress passed the Gramm–Leach–Bliley Act, also known as the Financial Services Modernization Act, to repeal them. Eight days later, President Bill Clinton signed it into law. Following the financial crisis of 2007-2008, legislators unsuccessfully tried to reinstate Glass–Steagall Sections 20 and 32 as part of the Dodd–Frank Wall Street Reform and Consumer Protection Act. Both in the United States and elsewhere, banking reforms have been proposed that refer to Glass–Steagall principles. These proposals include issues of “ring fencing” commercial banking operations and narrow banking proposals that would sharply reduce the permitted activities of commercial banks.

The point of the bill was to isolate the risky bank behaviour, relating to derivatives and trading from core banking activities. In the case of a banking crisis, triggered by a collapse in the financial markets such an arrangement would protect the operations of the core banking. We got a glimpse of that a month ago when US trading volatility shot through the roof.

But, in Australia, the bulk of the risks in the banking system comes not from the derivatives side of the business, but the massive exposure to household debt and the property sector, and the risky loans they have made. We discussed this on the ABC yesterday. More than 60% of all banking assets are aligned with home lending, plus more relating to commercial property. Thus I do not believe a Glass-Stegall type separation would help to mitigate risks to the banking sector here much at all.

Better to push for a definitive change to the APRA Bill and get deposits excluded from the risk of bail-in. Or place a levy on all banks to directly protect depositors as has been put in place in Germany, where a dedicated government entity has been created for just this purpose.

What I find remarkable is that following loose banking regulation for years, during which the banks have returned massive profits to shareholders, and ramped up their risks, depositors are being lined up by the Government to bail out a failing bank. This is simply wrong.

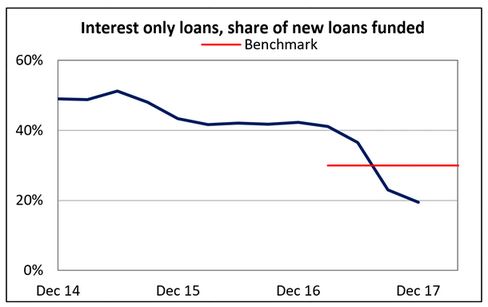

During the session he said that the 10% cap on banks lending to housing investors imposed in December 2014 was “probably reaching the end of its useful life” as lending standards have improved. Essentially it had become redundant.

But the other policy which is a limit of more than 30% of lending interest only will stay in place. This more recent additional intervention, dating from March 2017, will stay for now, despite it being a temporary measure. The 30% cap is based on the flow of new lending in a particular quarter, relative to the total flow of new lending in that quarter.

This all points to tighter mortgage lending standards ahead, but still does not address the risks in the back book.

But the tougher lending standards which are now in place will be part of the furniture, plus the new capital risk weightings recently announced. Its all now focussing on loan serviceability, something which should have been on the agenda 5 years ago!

The evidence before the Senate on mortgage fraud is worth watching.

He also included some interesting and relevant charts.

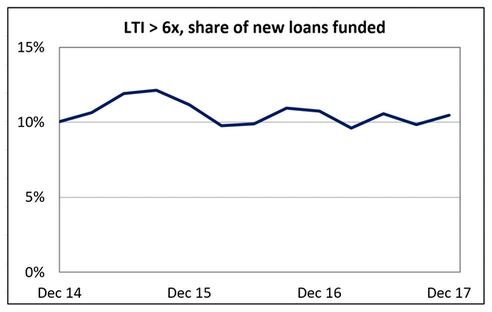

Around 10% of new loans are still Loan to income is still tracking above 6 times loan to income.

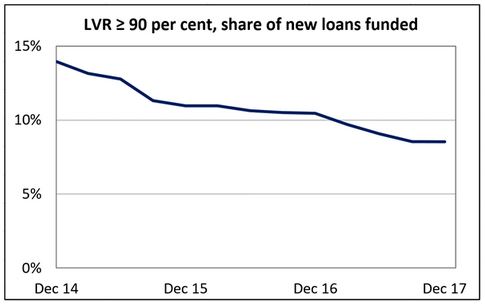

This despite a fall in high LVR new loans.

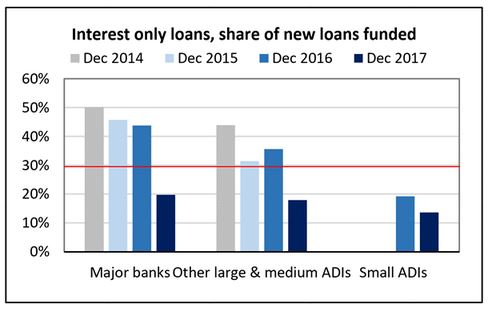

The volume of new interest only loans is down, 20% of loans from the major banks are interest only, higher than other ADI’s

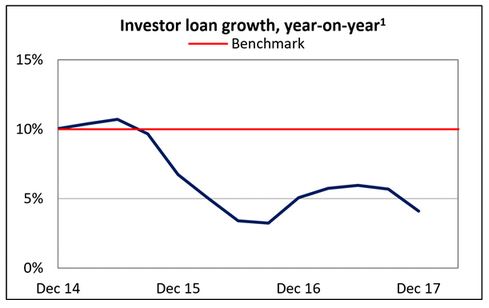

Overall investor loan growth is lower, in fact small ADI’s have slightly higher growth rates than the majors.

As a result of the changes the share of new interest only loans has dropped below the target 30%, to about 20%.

And investor loans are growing at less than 5% overall, significantly lower than previously.

So you could say the APRA caps have worked, but more permanent and calibrated measures are the future.

More broadly, here are his remarks:

I’d like to start this morning by highlighting the importance of the Financial Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Bill 2017 which – with the welcome endorsement of this Committee – was recently passed into law by the Parliament.

The Bill delivers a long-awaited and much needed strengthening of APRA’s crisis management powers, better equipping us to deal with a financial crisis and thereby to protect the financial well-being of the Australian community. Put simply, these powers give us enhanced tools to fulfil our key purpose in relation to banking and insurance: to protect bank depositors and insurance policyholders. That purpose is at the heart of all that we do, and the legislation is designed with that protection very much in mind.

With the Bill now passed, the task ahead for APRA is to invest in the necessary preparation and planning to make sure the tools within the new legislation can be effectively used when needed. We hope that is neither an imminent nor common occurrence, but we have much work to do in the period ahead to make sure we, along with the other agencies within the Council of Financial Regulators that will be part of any crisis response, have done the necessary homework to use these new powers effectively when the time comes.

So that is one key piece of work for us in the foreseeable future. But it is far from the only issue on our plate. With the goal of giving industry participants and other stakeholders more visibility and a better understanding of our work program, we released a new publication in January this year outlining our policy priorities for the year ahead across each of the industries we supervise.1 Initial feedback has welcomed this improved transparency of the future pipeline of regulatory initiatives, and the broad timeline for them.

That publication is one example of our ongoing effort to improve our processes of engagement and consultation with the financial sector and other stakeholders. Another prominent example is that we’ve just embarked on our most substantial program of industry engagement to date as we seek input into the design and implementation of our next generation data collection tool.2 Through this process, which we launched on Monday this week, all of our stakeholders will have an opportunity to tell us – at an early stage of its design – what they would like to see the new system deliver, as well as influence how we roll it out.

More generally, and recognising the increased expectations of all public institutions, I thought it would also be timely to briefly recap the ways APRA is accountable for the work we do supervising financial institutions for the benefit of the Australian community. At a time when Parliament has moved to strengthen APRA’s regulatory powers, we fully accept that these accountability measures take on added importance. They play a crucial role in reassuring all of our stakeholders that APRA is acting at all times according to our statutory mandate.

APRA’s accountability measures are many and varied. They start with the obvious measures such as our Annual Report, our Corporate Plan and Annual Performance Statement, and our assessment against the Government’s Regulator Performance Framework. We obviously also make regular appearances before Parliamentary committees such as this to answer questions about our activities, and now meet with the Financial Sector Advisory Council in their role reporting on the performance of regulators. Our annual budget, and the industry levies that fund us, are set by the Government, which also issues us a Statement of Expectations as to how we should approach our role. We comply with the requirements of the Office of Best Practice Regulation in our making of regulation, and our prudential standards for banking and insurance may be disallowed by Parliament, should it so wish.

To give greater visibility to these mechanisms, we have recently set out an overview of our accountability requirements – including some that we impose on ourselves – on our website so that they can be better understood by our stakeholders.3

I’d like to also note that we will be subject to additional scrutiny this year through two other means:

We expect that aspects of APRA’s activities will be of interest to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. We have already provided, at their request, documents and information to the Commission, and will continue to cooperate fully as it undertakes its important work.

We will be subject to extensive international scrutiny from the IMF over the year ahead as part of its 2018 Financial Sector Assessment Program (FSAP).4 The FSAP will look at financial sector vulnerabilities and regulatory oversight arrangements in Australia, providing a report card on Australia (and APRA in particular) against internationally-accepted principles of sound prudential regulation. As was the case previously, we expect the IMF to find things we could do better. APRA is ready, along with other members of the regulatory community, to give the IMF our full cooperation and look forward to their feedback.

Finally, time does not permit me to discuss our on-going work in relation to housing lending but, anticipating some questions on this issue, I have circulated some charts which might be helpful for any discussion (see attached).

With those opening remarks, we would now be happy to answer the Committee’s questions.

The latest APRA Monthly Banking Statistics to January 2018 tells an interesting tale. Total loans from ADI’s rose by $6.1 billion in the month, up 0.4%. Within that loans for owner occupation rose 0.57%, up $5.96 billion to $1.05 trillion, while loans for investment purposes rose 0.04% or $210 million. 34.4% of loans in the portfolio are for investment purposes. So the rotation away from investment loans continues, and overall lending momentum is slowing a little (but still represents an annual growth rate of nearly 5%, still well above inflation or income at 1.9%!)

Our trend tracker shows the movements quite well. (August 2017 contained a large adjustment.

Looking at the lender portfolio, we see some significant divergence in strategy. Westpac is still driving investment loans the hardest, while CBA and ANZ portfolios have falling in total value, with lower new acquisitions and switching. Bank of Queensland and Macquarie are also lifting investment lending.

The market shares are not moving that much overall, with CBA still the largest OO lender, and Westpac the largest Investor lender.

Looking at investor portfolio movements for the past year, again significant variations with some smaller players still above the 10% speed limit, but the majors all well below (and some in negative territory).

We will report on the RBA data later on, which gives us an overall market view.

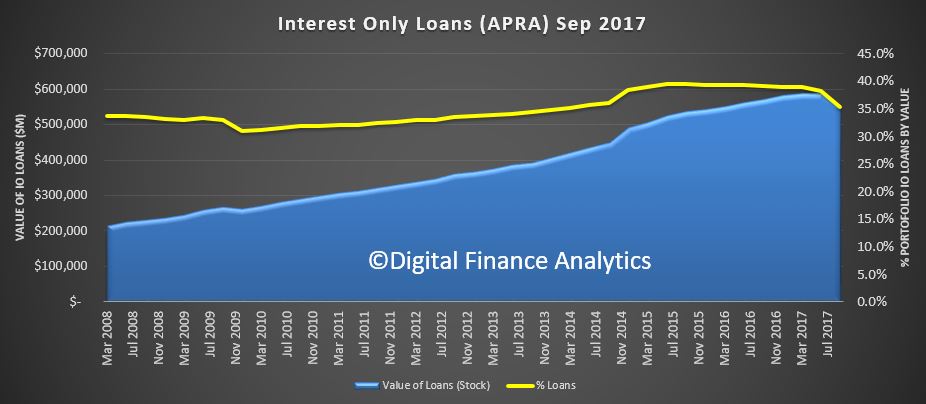

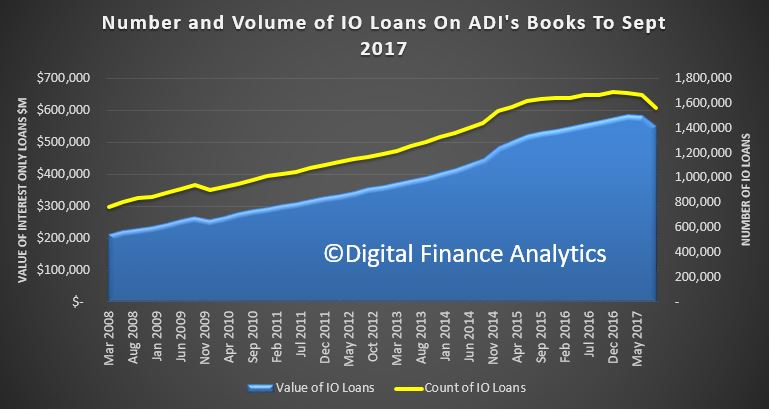

OK, so there has been lots of noise about the Mortgage Interest Only Exposures the banks have, and both APRA and the RBA say they are potentially risky, compared with Principal and Interest Loans. We already showed that conservatively $60 billion of IO loans will fail current underwriting standards. That is more than 10% of the portfolio.

But how many loans are interest only, and what is the value of these loans? A good question, and one which is not straightforward to answer, as the monthly stats from the RBA and ABS do not split out IO loans. They should.

The only public source is from APRA’s Quarterly Property Exposures, the next edition to December 2017 comes out in mid March, hardly timely. So we have to revert to the September 2017 data which came out in December. This data is all ADI’s with greater than $1 billion of term loans, and does not include the non-bank sector which is not reported anywhere!

They reported that 26.9% of all loans, by number of loans were IO loans, down from a peak of 29.8% in September 2015. They also reported the value of these loans were 35.4% of all loans outstanding, down from a peak of 39.5% in September 2015.

So, what does this trend look like. Well the first chart shows the value of loans in Sept 2017 was $549 billion, down from a peak of $587 billion in March 2017. The number of loans outstanding was 1.56 million loans, down from a peak of 1.69 million loans in December 2016.

If we plot the trends by number of loans and value of loans, we see that the value exposed is still very high.

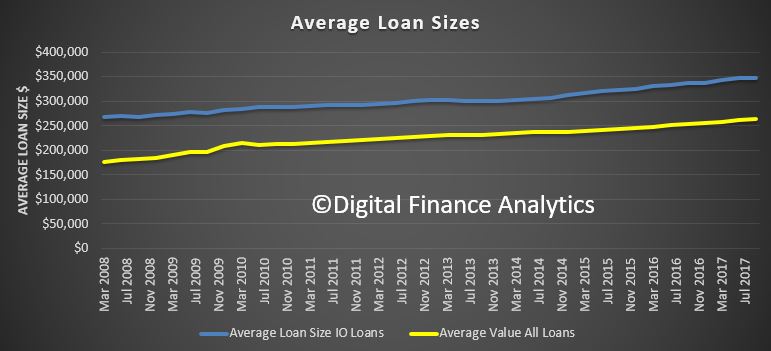

Finally, the average loan size for IO loans is significantly higher at $347,000 compared with $264,300 for all loans. Despite the fall in volume the average loan size is not falling (so far).

The point is the regulatory intervention is having a SMALL effect, and there is a large back book of loans written, so the problem is risky lending has not gone away.

Last Wednesday, the Australian Prudential Regulation Authority (APRA) proposed key revisions to its capital framework for authorized deposit taking institutions (ADIs). The revisions cover the calculation of credit,

market and operational risks. These proposed changes are credit positive for Australian ADIs because they will improve the alignment of capital and asset risks in their loan portfolios. Moody’s says the key proposals are as follows:

Revisions to the capital treatment of residential mortgage portfolios under the standardized and advanced approaches, with higher capital requirements for higher-risk segments

Amendments to the treatment of other exposures to improve the risk sensitivity of risk-weighted asset outcomes by including both additional granularity and recalibrating existing risk weights and credit

conversion factors for some portfolios

Additional constraints on the use of ADIs’ own risk parameter estimates under internal ratings-based approaches to determine capital requirements for credit risks and introducing an overall floor to riskweighted assets for ADIs using the standardized approach

Introduction of a single replacement methodology for the current advanced and standardized approaches to operational risks

Introduction of a simpler approach for small, less complex ADIs to reduce the regulatory burden without compromising prudential soundness

A particularly significant element of the new regime is a reform of the capital treatment of residential mortgages, given that more than 60% of Australian banks’ total loans were residential mortgages as of January 2018.

The improved alignment of capital to risk for residential mortgages will come from hikes in risk weights on several higher-risk loan segments. APRA proposes increased risk weights for mortgages used for investment purposes, those with interest-only features and those with higher loan-to-valuation ratios (LVR). At the same time, risk weights for some lower-risk segments likely will drop. For example, under the standardized approach, standard mortgages with LVR ratios lower than 80% will require risk weights of only 20%-30%, down from 35% under current requirements.

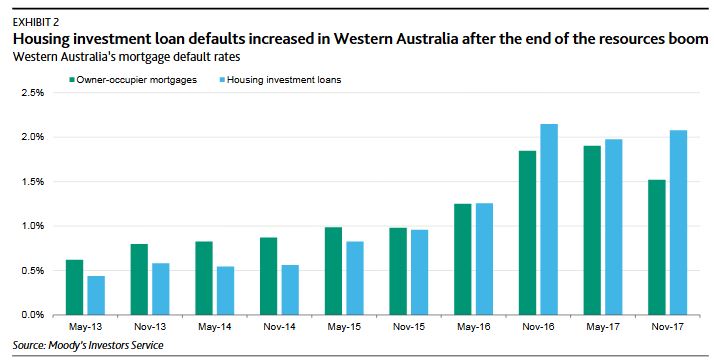

The higher capital charges on investment loans will better reflect their higher sensitivity to economic cycles. During periods of economic strength investment loans perform well. As Exhibit 1 shows, on a national basis

and during a time of strong economic growth, defaults on investment loans have been lower than owner occupier loans.

However, in Western Australia, where the economy has deteriorated following the end of the investment boom in resources, defaults on investment loans have been higher than owner-occupier loans, as Exhibit 2 shows.

Investment loans also are sensitive to the interest rate cycle. During periods of rising interest rates, investment loans tend to experience higher default rates than owner-occupier loans, as shown in Exhibit 3.