Ironic really, that on the day ASIC released its updated lending guidance, BOQ have lowered their interest rate floors for home loan serviceability assessments.

BOQ has reduced its floor rate for mortgage serviceability assessments from 5.65 per cent to 5.35 per cent, with the changes also applicable to its subsidiary Virgin Money. Via The Adviser.

The changes will apply for all new home loan applications submitted from Monday, 9 December.

The interest rate buffer will remain unchanged at 2.50 per cent.

BOQ noted that serviceability rates will

vary depending on the credit product under assessment, with the interest

rate applicable determined as follows:

For variable principal and interest home loans, the actual rate will be applied as the interest rate for serviceability.

For interest-only and fixed rate home loans, the revert rate will be applied as the interest rate for serviceability.

BOQ added that applications submitted

prior to Monday, 9 December, that have not been approved will be

assessed using the new serviceability rates.

In early July, the prudential regulator

scrapped its requirement for a 7 per cent interest rate floor and raised

its recommended buffer rate from a minimum of 2 per cent to 2.5 per

cent.

APRA chair Wayne Byres said the

regulator’s amendments were “appropriately calibrated”, stating that a

serviceability floor of more than 7 per cent was “higher than necessary

for ADIs to maintain sound lending standards”.

Analysts have partly attributed the rebound in home lending activity over the past few months to APRA’s changes.

According to the latest data released

by the Australian Bureau of Statistics, the value of new home lending

commitments rose 1.1 per cent (in seasonally adjusted terms) in

September, following on from a 3.8 per cent rise in August.

New lending commitments are now up 5.6 per

cent (seasonally adjusted) when compared with September 2018, the first

positive year-on-year result seen since mid-2018.

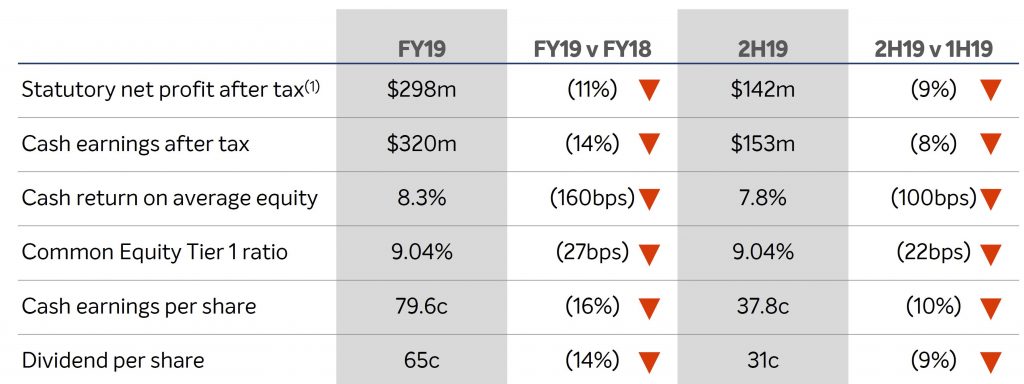

Bank of Queensland today announced FY19 cash earnings after tax of $320 million, down 14 per cent on FY18. Statutory net profit after tax decreased by 11 per cent to $298 million. Basic cash earnings per share was down 16 per cent to 79.6 cents per share. We expect many banks to report a similar story ahead.

The Board has announced a final dividend of 31 cents per share, for a full year dividend of 65 cents per share. This is a reduction of 11 cents per share from FY18. The final dividend payout ratio of 82% was consistent with the interim dividend payout ratio.

They described this as “Disappointing results reflect challenging operating environment”, reflecting a challenging operating environment characterised by slowing credit demand, lower interest rates, a rise in regulatory costs and changes impacting non-interest income.

Total income decreased by $21 million or two per cent from FY18.

Net interest income decreased $4 million, driven primarily by a five basis point reduction in net interest margin to 1.93 per cent. This reduction is attributable to the declining interest rate environment and continued strong competition for loans and deposits.

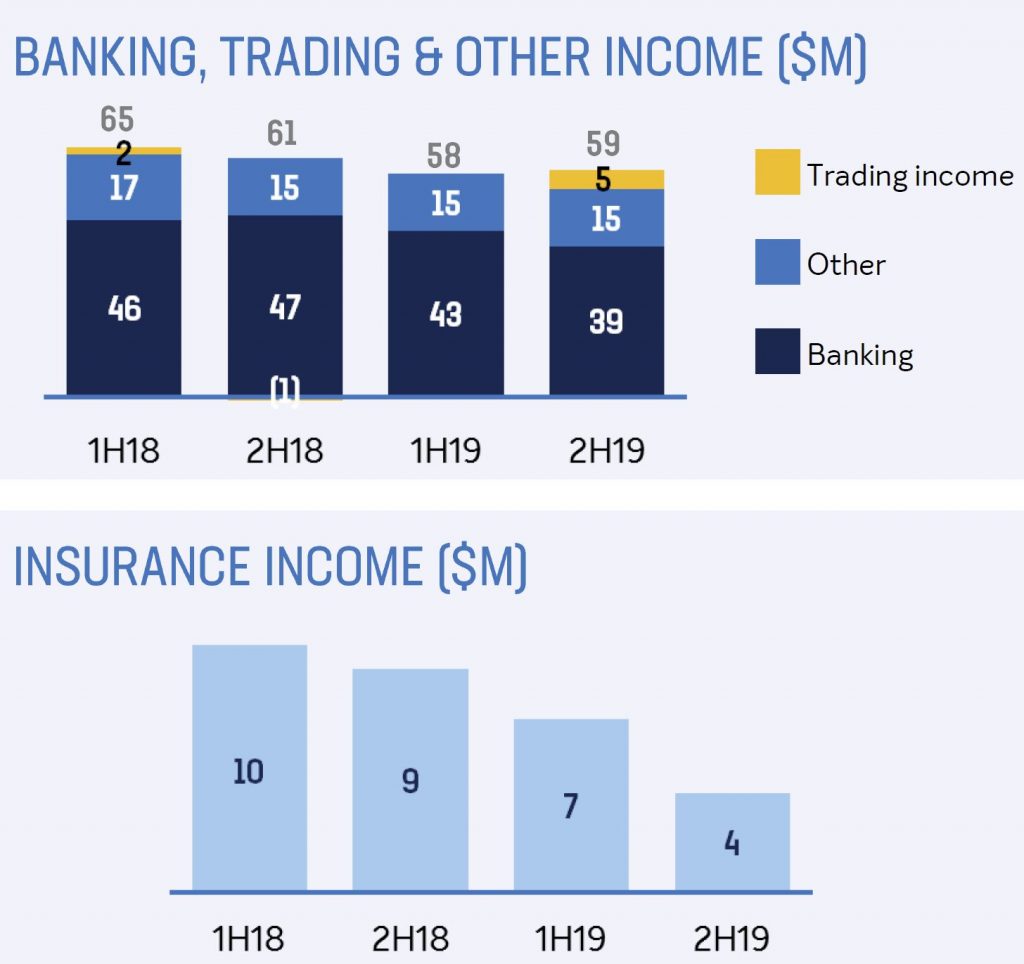

Non-interest income decreased 12 per cent or $17 million, driven by declines in Banking, Insurance and Other income but partially offset by improved Trading income. Banking income reduced $11 million due to lower fee income and a change in arrangements related to BOQ’s merchant offering. Insurance income reduced $8 million or 42 per cent due to changes in the insurance sector which ultimately impacted distribution of St Andrew’s consumer credit insurance through its corporate partners.

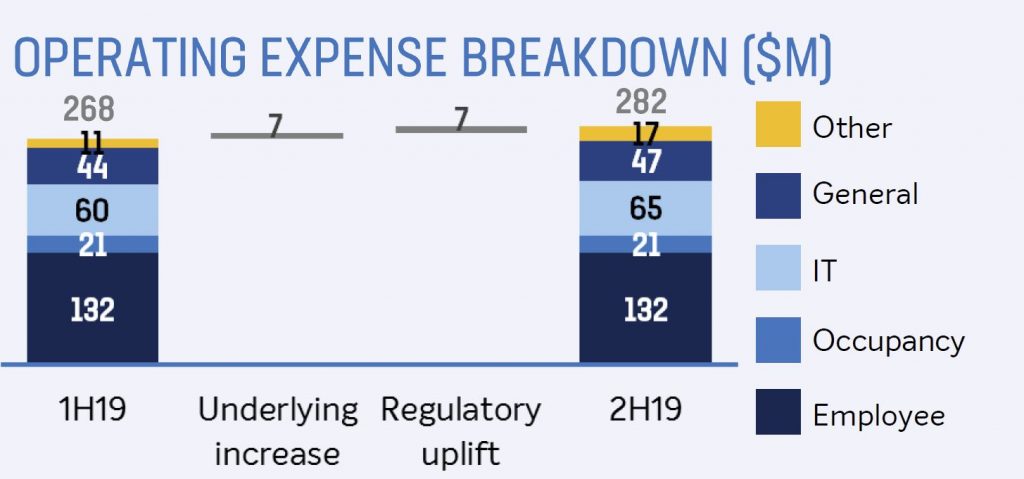

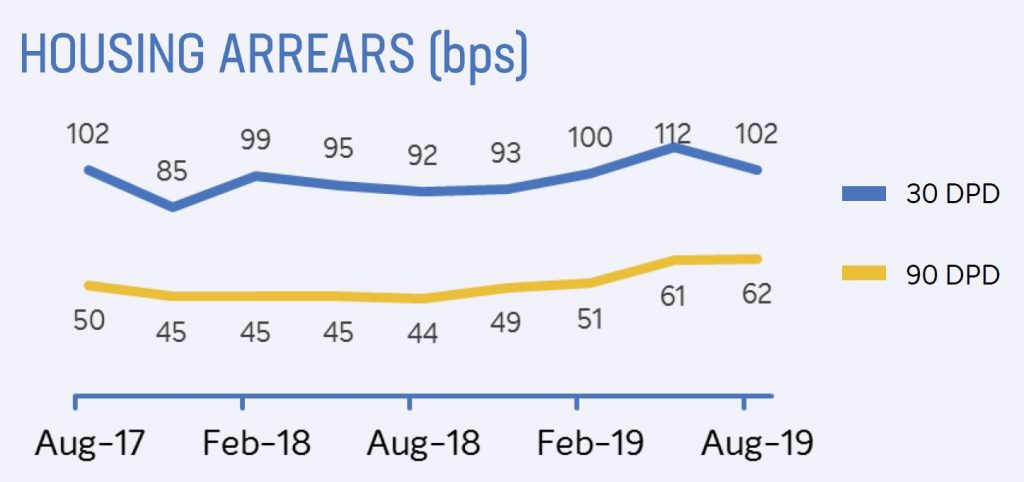

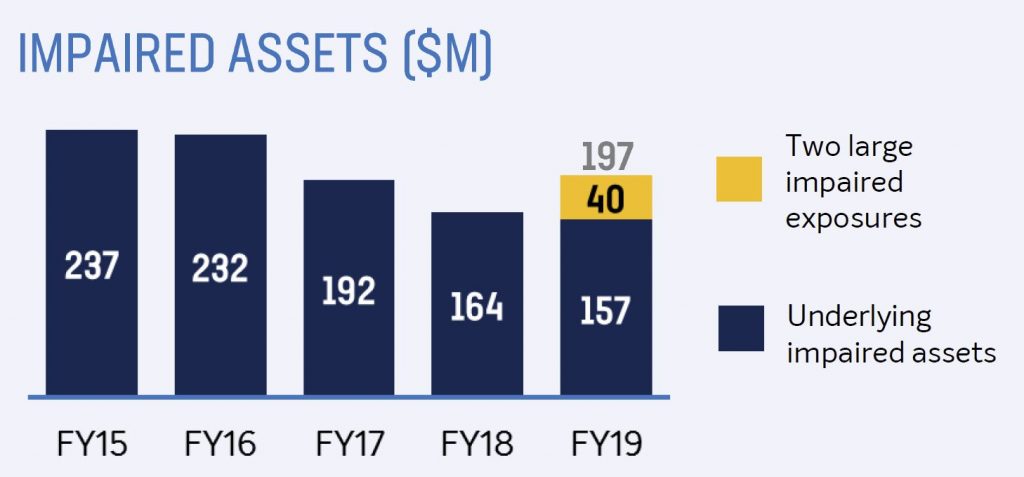

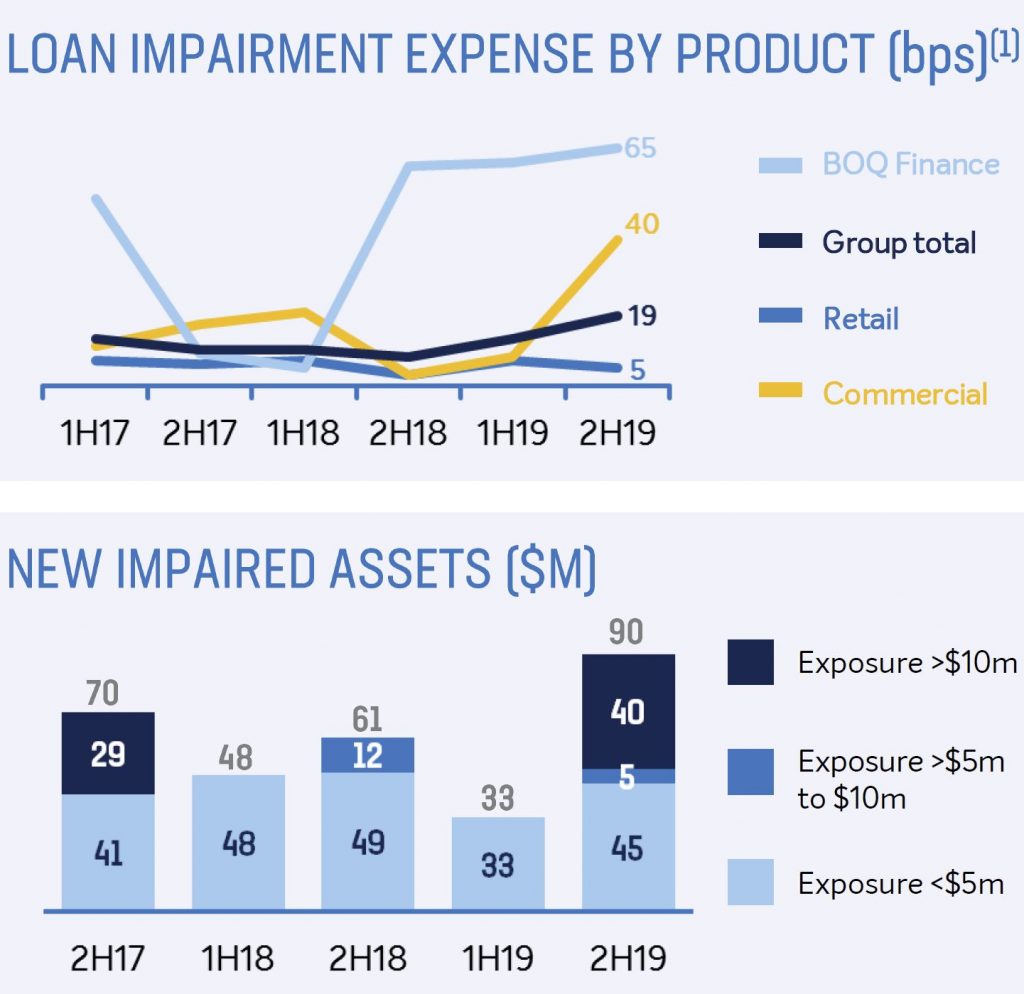

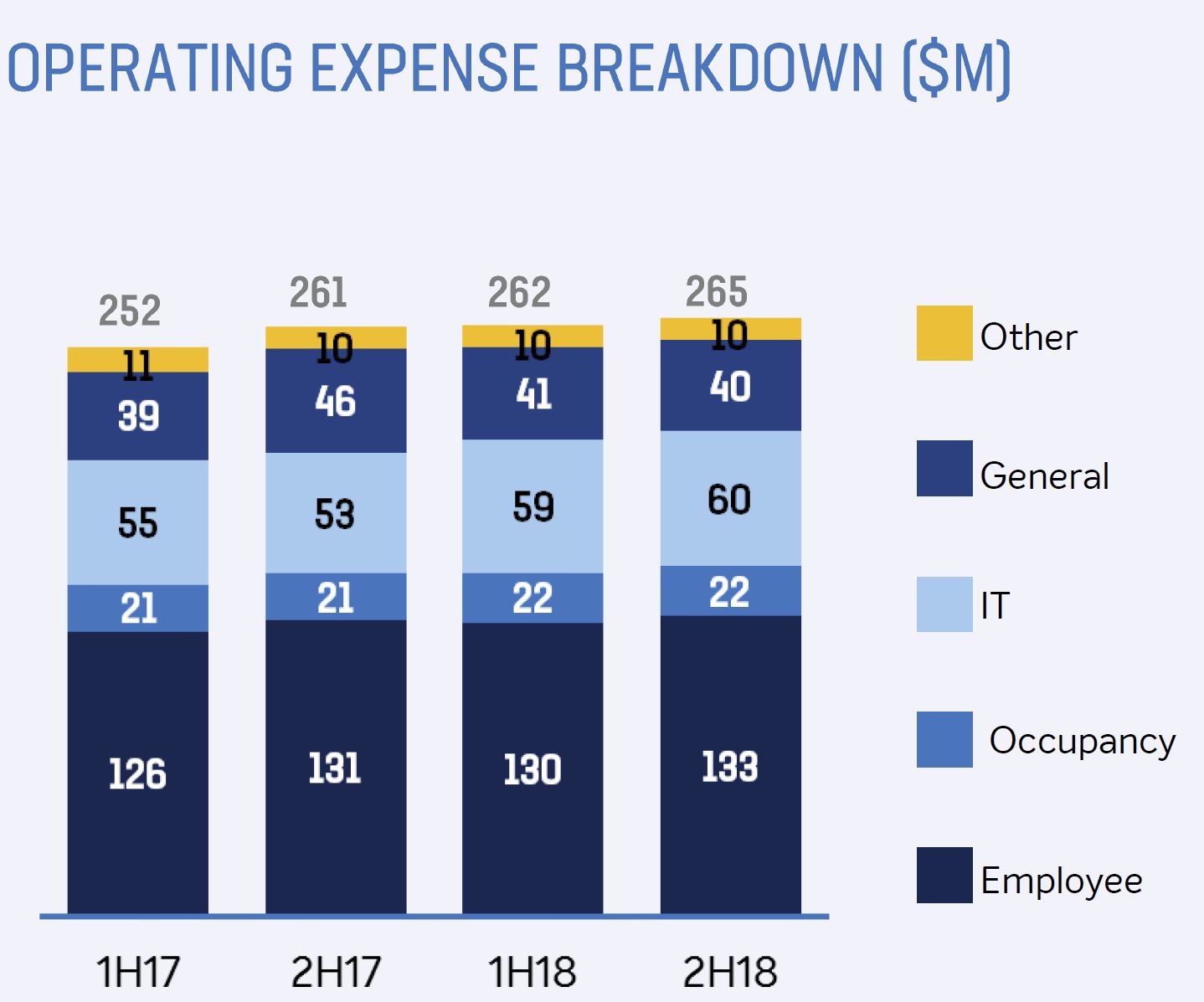

In line with the guidance provided at the 1H19 result, operating expenses increased by $23 million or four per cent from FY18. The increase in expenses was more pronounced in the second half, due to an increase in business deliverables addressing regulatory and compliance requirements. While loan impairment expense increased $33 million to $74 million, equivalent to 16 basis points of gross loans, underlying asset quality remains sound with impairments and arrears remaining at low levels.

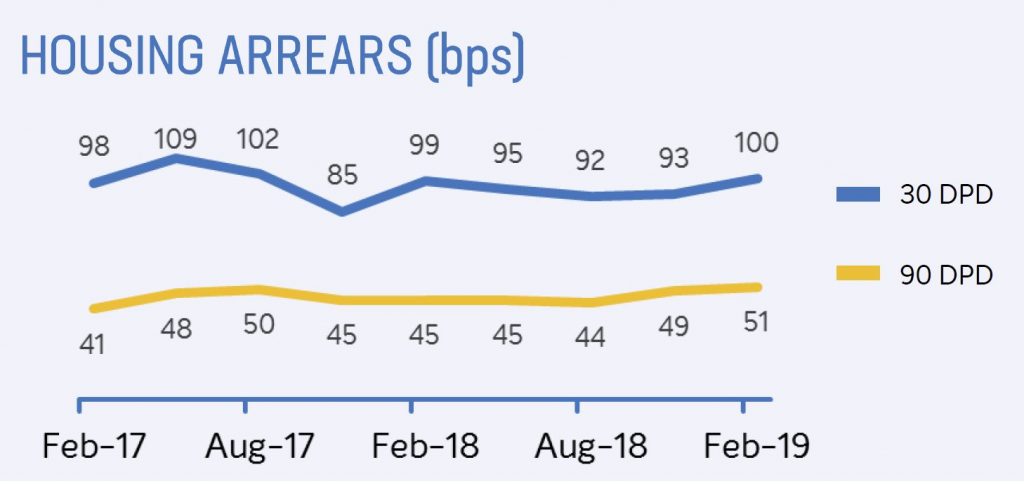

Housing loan arrears over 90 days rose, while 30 day fell.

Implementation of BOQ’s new AASB 9 collective provision model drove an increase in collective provisions due to changes in BOQ’s portfolio and a weaker economic outlook. The increase in collective provisions contributed $22 million of the loan impairment expense uplift.

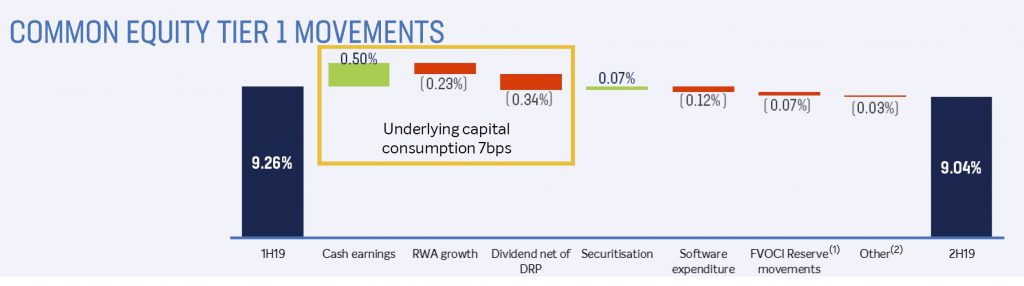

BOQ remains appropriately capitalised with a Common Equity Tier 1 ratio of 9.04 per cent, which is a decrease of 27 basis points from FY18. The reduction was driven by a combination of asset growth being tilted to more capital intensive business lines, increased capitalised investment, reduced earnings and lower participation in the dividend reinvestment plan.

Overall lending growth of two per cent was achieved over the year.

Continued growth momentum was evident in BOQ’s niche business segments. The BOQ Finance portfolio achieved growth of $667 million or 15%, while BOQ Specialist grew lending balances by $756 million across its commercial and housing loan portfolios which are focused on the medical segment. Virgin Money also delivered a consistently strong level of housing loan growth, with the portfolio growing by $914 million to over $2.5 billion.

A key imperative remains rebuilding the foundation for growth in BOQ’s retail bank, which saw a further contraction of $1.4 billion in its residential housing loan book.

Solid progress has also been made across a number of key foundational investments during the year. BOQ’s core technology infrastructure modernisation program has continued to track to plan, with implementation continuing through FY20. This will deliver a more modern, cloud-based technology environment which will allow for improved change capability.

During the year, work began on development of a new mobile banking application for BOQ customers, with a launch expected in 2020. Lending process improvements have also been a key focus to improve customer experience, particularly for home loan applications. A number of regulatory projects have also progressed during the year to address various regulatory and industry changes. These are all critical investments that will support BOQ’s transformation and future aspirations.

Investment in the implementation of a new Virgin Money digital bank has also progressed during the year, with a customer launch planned for 2020. This will require $30 million of capitalised investment during FY20 to complete the phase one build which will deliver a transaction and savings account offering to customers. This is an investment in long term value creation for this iconic brand which has demonstrated success in attracting customers across its existing product suite. It is also anticipated that this investment in a new digital banking platform will be leveraged across the Group in the years ahead.

Commenting on the results and outlook for BOQ, new Managing Director & CEO George Frazis said that there are challenges ahead, however fundamentally, BOQ is a good business.

“Our capital is well positioned for ‘unquestionably strong’, we have a good funding position and our underlying asset quality is sound. “There are numerous opportunities ahead for a revamped BOQ and I will be working closely with the executive leadership team to complete our strategic and productivity review, with a market update on our plans in February 2020,”

ASIC has commenced proceedings in the Federal Court of Australia against the Bank of Queensland concerning unfair contract terms in small business contracts.

ASIC alleges that certain terms used by Bank of Queensland in

contracts with small businesses are unfair. If the Court agrees with

ASIC, the specific terms will be void and unenforceable by the Bank of

Queensland in these contracts.

ASIC alleges that certain terms used by the Bank of Queensland are unfair, as the terms:

cause a significant imbalance in the parties’ rights and obligations under the contract;

were not reasonably necessary to protect the Bank of Queensland’s legitimate interests; and

would cause detriment to the small businesses if the terms were relied on.

Some of the unfair terms pleaded by ASIC include clauses that give

lenders, but not borrowers, broad discretion to vary the terms and

conditions of the contract without the consent of the small business

owner, along with clauses that allow the bank to call a default, even if

the small business owner has met all of its financial obligations.

ASIC is also seeking a declaration from the Federal Court that the

same terms in any other small business contract are also unfair.

Background

If the Federal Court finds that any of the terms of the standard form

contracts are unfair, the unfair terms are void (it is as if the terms

never existed in the contracts). ASIC is seeking that the terms are

declared void from the outset – not from the time of the court’s

declaration. The remainder of the contract will continue to bind parties

if it can operate without the unfair terms.

Since 1 July 2010, ASIC has administered the law to deal with unfair

terms in standard form consumer contracts for financial products and

services, including loans.

With effect from 12 November 2016, the unfair contract terms

provisions applying to consumers under the Australian Consumer Law and

the ASIC Act were extended to cover standard form ‘small business’

contracts.

Small businesses, like consumers, are often offered contracts for

financial products and services on a ‘take it or leave it’ basis,

commonly entering into contracts where they have limited or no

opportunity to negotiate the terms. These are known as ‘standard form’

contracts. Small businesses commonly enter into these ‘standard form’

contracts for financial products and services, including business loans,

credit cards, and overdraft arrangements.

The unfair contracts law applies to standard form small business

contracts entered into, or renewed, on or after 12 November 2016 where:

the contract is for the supply of financial goods or services (which includes a loan contract);

at least one of the parties is a ‘small business’ (under the ASIC

Act, a business employing fewer than 20 people is a ‘small business’);

and

the upfront price payable under the contract does not exceed $300,000, or $1 million if the contract is for more than 12 months.

After successfully leading Westpac’s consumer bank, BOQ’s new boss George Frazis has landed a big job at a much smaller bank with a shrinking mortgage book, via InvestorDaily.

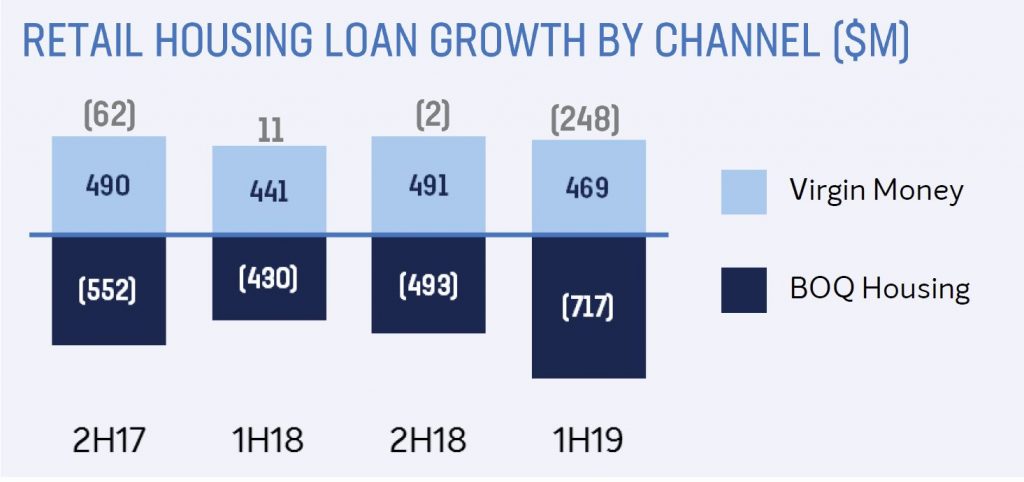

In

April, Bank of Queensland reported reporting negative mortgage growth

of $248 million, down from positive growth of $11 million in 1H18, with

its portfolio dropping to $24.7 billion.

The fall was driven by a

$717 million contraction in settlements through BOQ’s retail bank,

offset by a $469 million rise in home loan volumes through its

subsidiary, Virgin Money Home Loans.

The regional lender is well

aware of the challenges within its retail bank, which is effectively

franchised with branches being run by ‘owner-managers’. Given the

negative press generated by the royal commission, attracting new owner

managers has been difficult for BOQ.

Prior to the appointment of

George Frazis as CEO on 6 June, interim chief executive Anthony Rose

delivered an 8 per cent drop in cash earnings in the first half of

FY19.

“Across

the industry, as you are well aware, there have been significant

changes in the banking landscape which has created revenue headwinds for

the sector. In addition, the outcome from the royal commission is

lifting expectations of the regulators. Adjusting to the new regulatory

environment will come with a higher cost profile, absent any mitigating

actions which we are of course exploring,” Mr Rose said in April.

“BOQ

also has challenges that are specific to our business, particularly in

the retail bank. Our digital customer offering, lending processes and

the inability to attract new owner-managers with the overlay of

regulatory uncertainty, has hampered customer acquisition and returns.”

Mr

Rose, BOQ’s chief operating officer, will remain as interim CEO until

Mr Frazis takes over in September. Rose took charge following the

resignation of John Sutton in December 2018.

Morningstar analyst

David Ellis praised the appointment of Mr Frazis, an experienced banker

with 17 years in the industry, most recently as CEO of Westpac’s

consumer bank and CEO at St George Bank.

“While Frazis has strong

credentials and deeply understands the dynamics of Australia’s consumer

banking industry, he will be taking control of a regional player with a

small geographic distribution footprint, higher funding and operational

costs, a lower credit rating and tougher regulatory capital burden,” Mr

Ellis said.

The Morningstar analyst believes the challenge for

Mr Frazis is to assume a bigger role in a smaller organisation that

lacks market share, brand awareness, distribution capabilities and

funding advantages that major banks enjoy.

“Bank of Queensland’s

lending growth has been subdued for several years,” Mr Ellis said.

“Based on APRA banking statistics for April 2019, the bank’s 12-month

growth in home loans sit at just 0.3 per cent in April, compared to 1.7

per cent a year ago and 11.8 per cent three years prior.”

Bank system home loan growth is 3.3 per cent for the year to April 2019.

With

the RBA cutting rates this month, BOQ has lowered its fixed rates in an

effort to remain competitive in a mortgage market dominated by the big

four. However, with more cash rate cuts expected, Morningstar is

concerned whether BOQ can sustain its course of passing on the

reductions.

“The bank lacks access to lower-cost funding options

and has a much lower return on equity than the major banks,” Mr Ellis

said.

Under Mr Frazis’ leadership, Westpac’s consumer bank

attracted more than a million new customers in the past four years.

Digital channels now account for a third of sales.

“Frazis will have to do the same at Bank of Queensland,” Mr Ellis said

The 2019 half year results from BOQ today really underscores the pressures on the banks – especially regional ones – as home lending slows, and competition for the remaining business rises. And they see similar pressures ahead.

Banking is no longer the cash generating machine it use to be. Expect more loan repricing ahead to try and stablise the business. Their shares were lower. The dividend was cut.

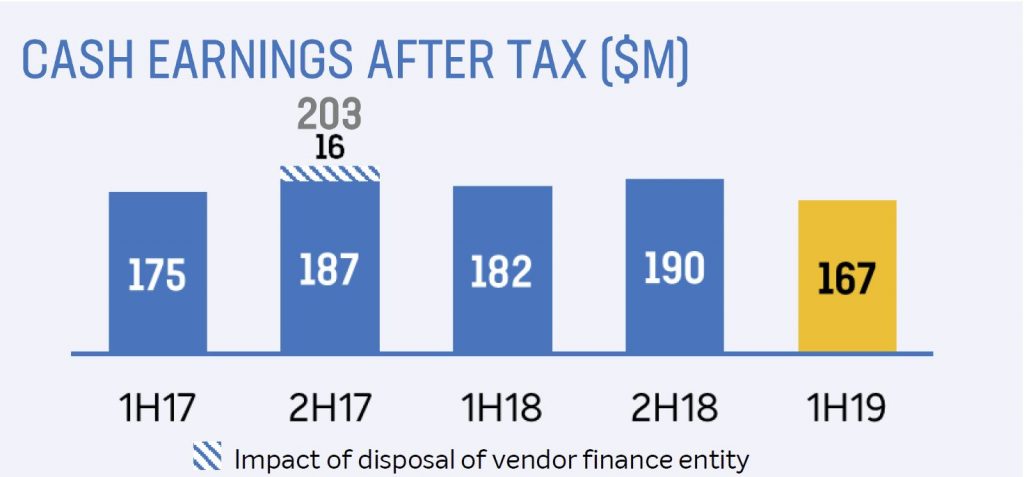

Their cash earnings after tax of $167 million, down 8% compared with 1H18, and 12% down on 2H18. This was pretty much as expected.

Their statutory net profit after tax of $156 million, down 10% on 1H18, or 4% down on 2H18.

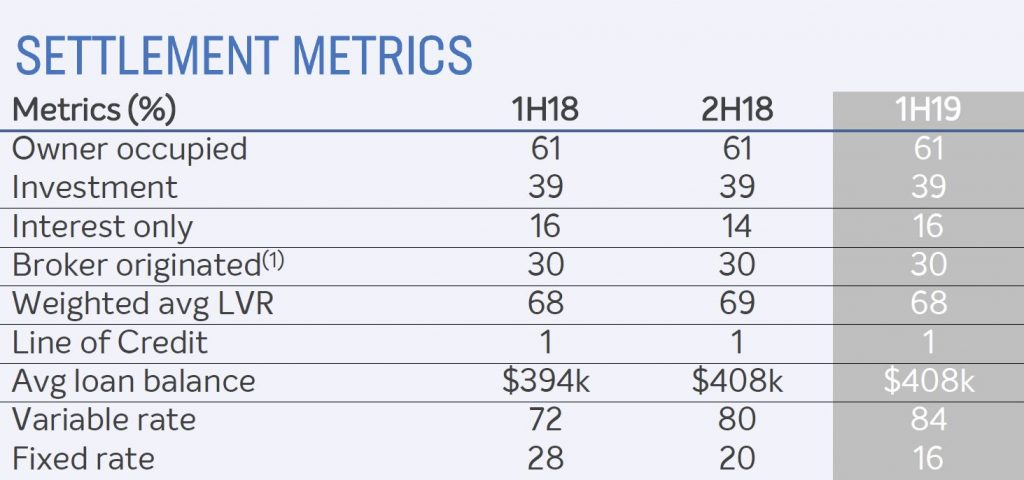

Gross loan growth was 2% in a slowing market, with housing growth through Virgin Money and BOQ Specialist, offset by contraction in branch network.

Home lending settlements included 39% investment lending (higher than the current industry average), 30% via brokers, and 16% interest only lending.

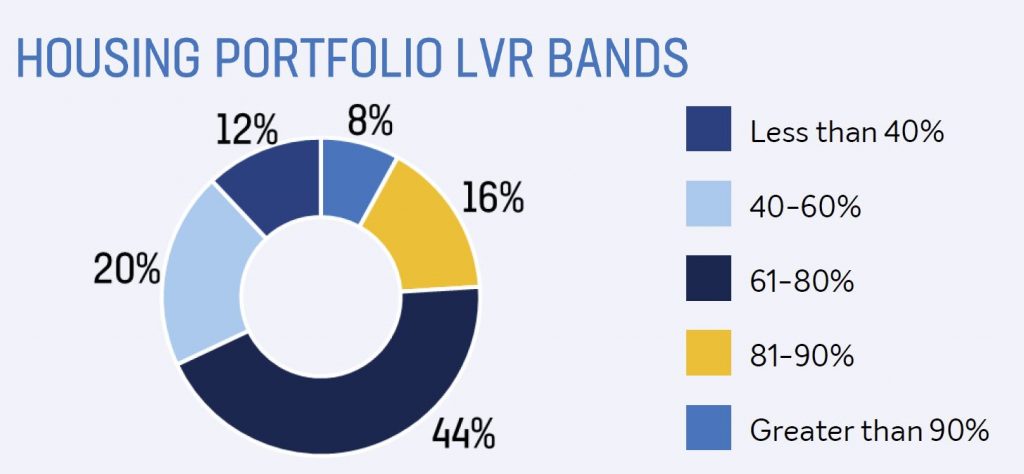

Home Lending LVR’s included 24% above 81% LVR in portfolio. Could become a problem is home prices go on falling.

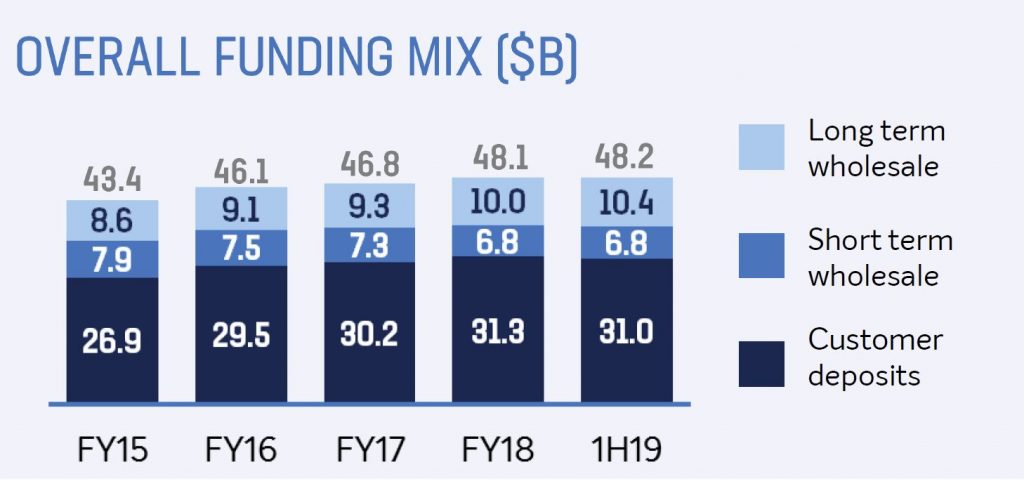

Customer deposits contracted, driven by a reduction in higher cost Term deposits, with a deposit to loan ratio of 68%

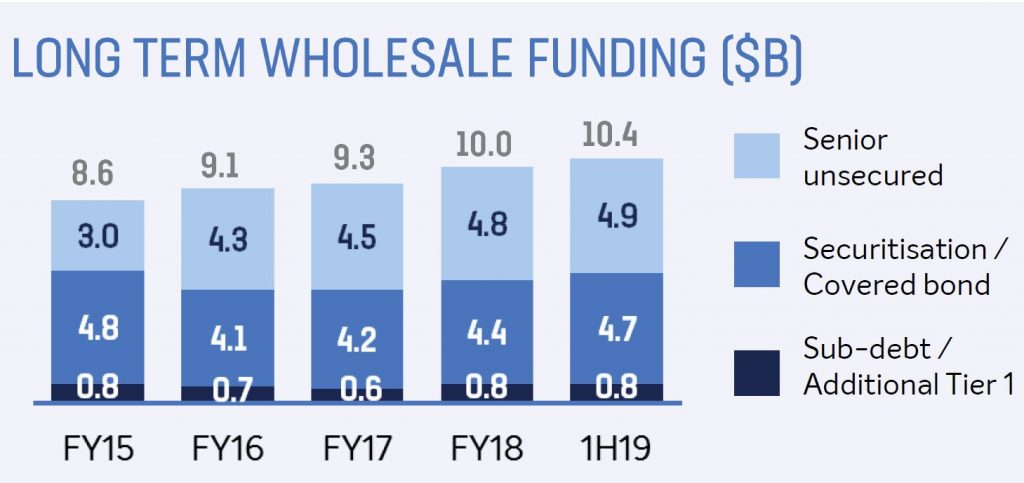

They took advantage of more favourable conditions for long term wholesale issuance

Net interest income was $215m, down 5% compared with 1H18 for the retail banks, and $216m, up 4% for the business bank.

Net Interest Margin was down 4 basis points to 1.94%

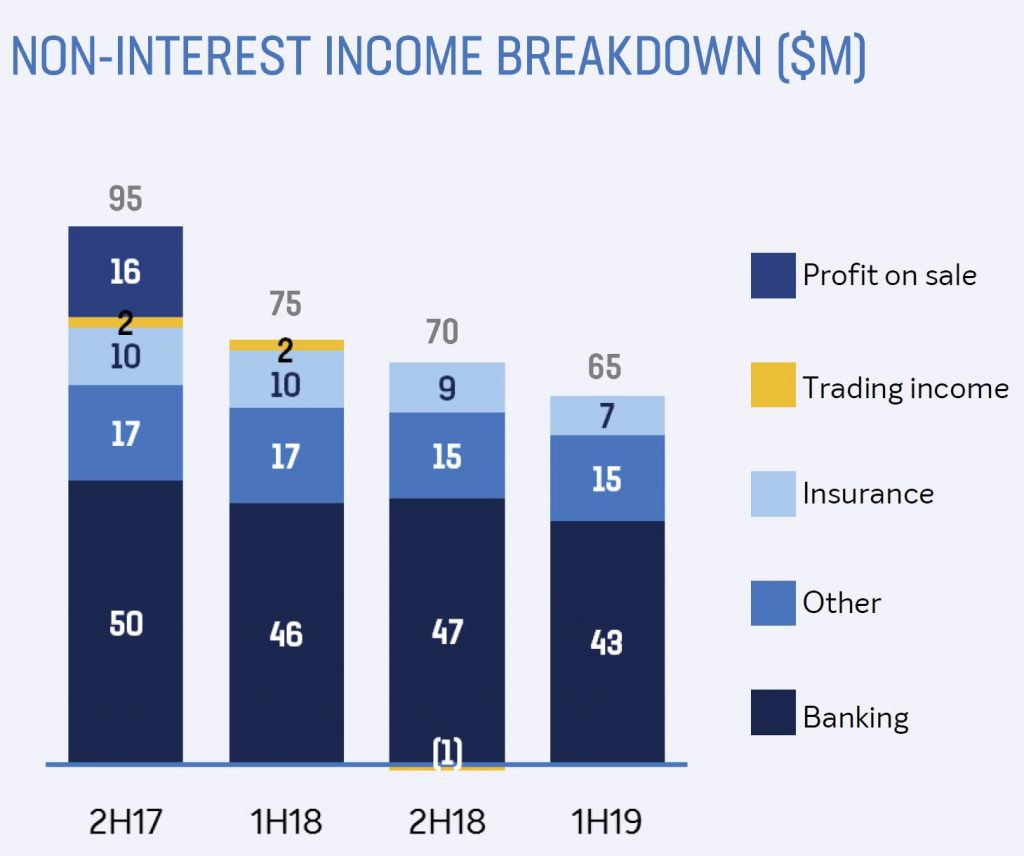

Non interest income was lower at $65m compared with $75m 1H18.

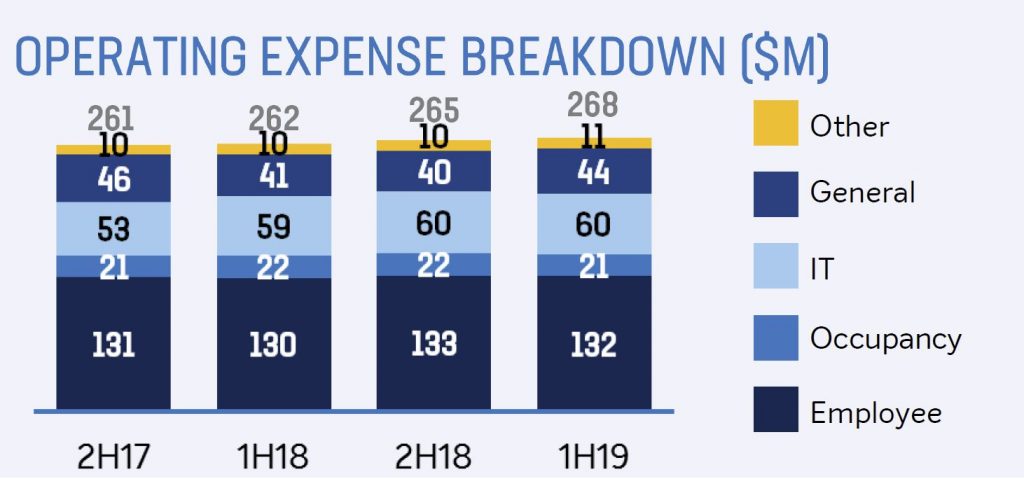

Their cost to income ratio was up 190 bps to 49.5%; They expect amortisation to increase with ongoing investment, plus rising regulatory & compliance costs expected going forward. In fact BOQ took a further $3m below the line for regulatory and compliance spend and $1m for legacy costs.

Operating expense growth was 2% to $268m and they expect higher costs ahead, with an additional $10m for regulatory costs.

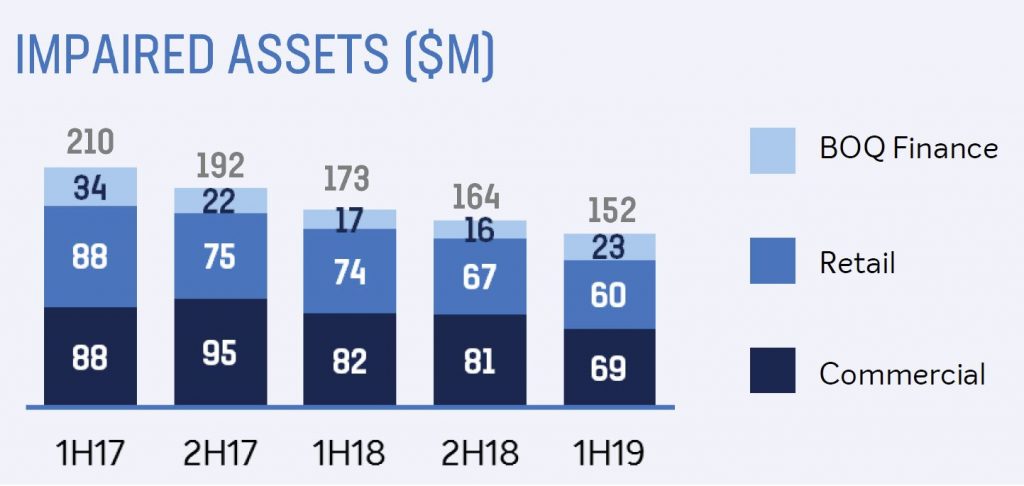

Impaired assets were down to $152m 1H19.

They reported a loan impairment expense of $30 million or 13 basis points of gross loans. There was an uptick in housing arrears.

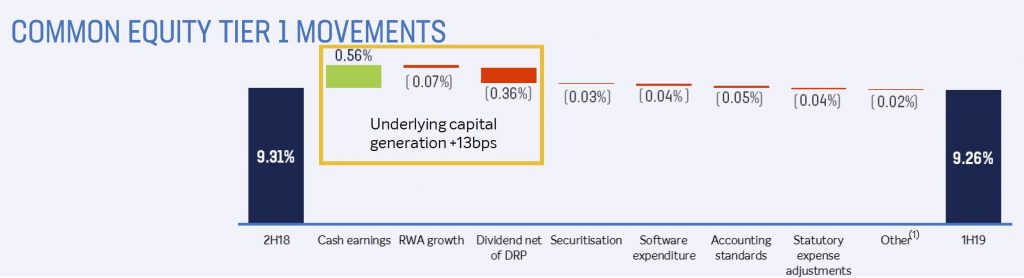

Common Equity Tier 1 (CET1) capital ratio of 9.26%, down from 9.31% 2H18.

The basic earnings per share down 10% to 41.8 cents on 1H18, but 13% down on 2H18.

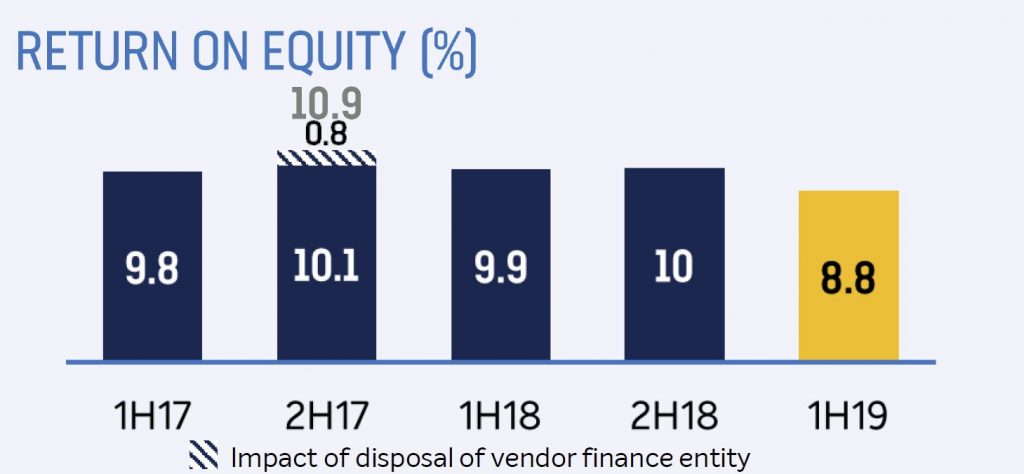

Their return on average ordinary equity was down 110 bps to 8.8%

The fully franked interim dividend was 34 cents per ordinary share, down from 38 cents.

The Bank of Queensland released a trading and earnings update today, ahead of the half year results on 11 April 2019. Their shares dropped significantly and are ~18% lower than a year back.

They said the cash earnings will be in the range of $165-170m, compared with 1H18 cash earnings after tax of $182m.

This is driven by a fall in non-interest income, down $8-10m that $75m in 1H18, thanks to lower fee, trading, insurance and other income lines.

Plus net interest margin will be in the range 1.93% to 1.95% compared with 1.97% in 1H18, and will be around $475m.

There will be more non-recurring expenses, so expenses will be higher.

Loan impairments are expected to be int eh range of 11-13 basis points of gross loans. They say underlying quality remains good.

CET1 capital will be above 9.1% reported last time.

The say conditions will remain challenging with an increasing regulatory burden, including the outfall from the Royal Commission.

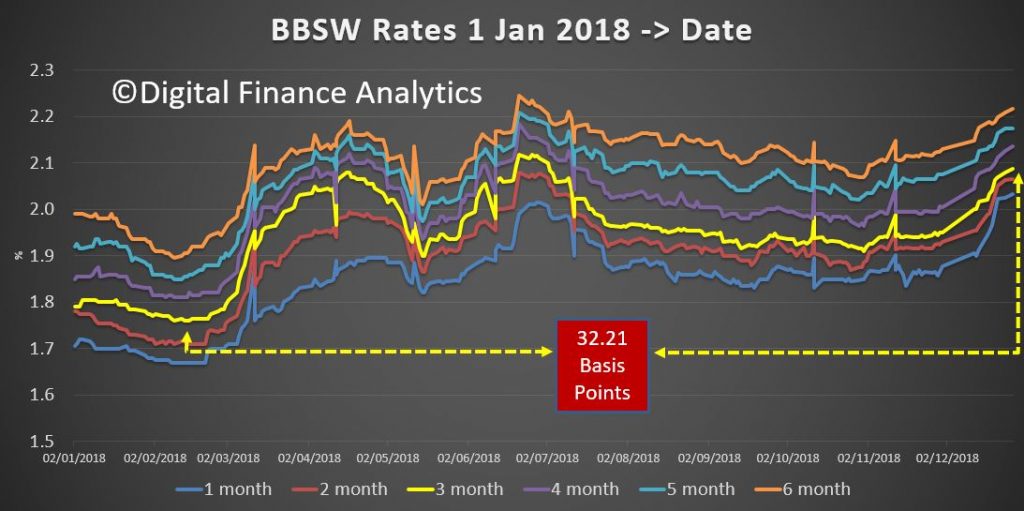

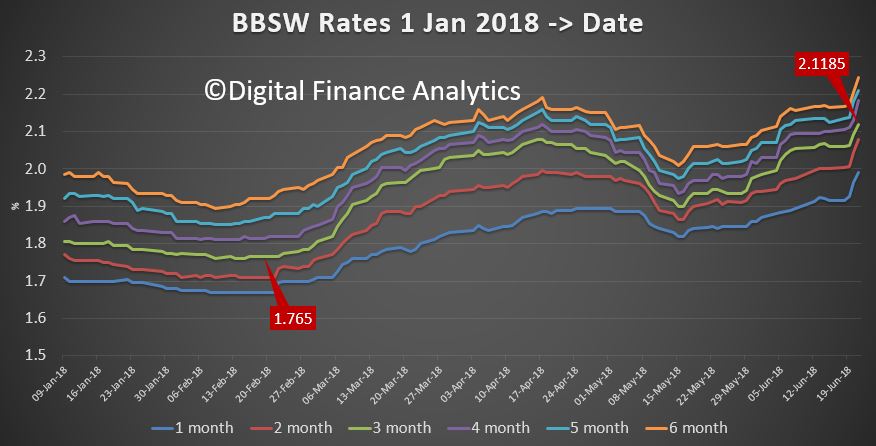

The Bank of Queensland has announced that they will lift mortgage rates for existing borrowers, thanks to higher funding costs, and pressures on bank deposits. The BBSW (interbank funding rate) has risen, and there are limits to how far deposit rates can be cut. We expect other banks to follow.

BOQ announced today that funding cost pressures and “intense”

competition for term deposits were partly behind its decision to lift

interest rates.

The rates of more than 20 of the bank’s home loan products will rise

from Friday with most set to increase by 0.18 percentage points,

including the standard variable rates for owner-occupiers and investors.

The standard variable rate for owner-occupiers paying principal and interest will rise from 5.70% to 5.88% ( comparison rate of 6.04%), while the standard variable investment housing rate will rise from 6.33% to 6.51% (comparison rate of 6.67%).

Six of its line of credit products, including the Clear Path Line of Credit Rate, will also rise by 0.18 percentage points.

The Economy Owner Occupier principal and interest home loan is the only one among the changes that will have a smaller hike of 0.11 percentage points to 3.99% (comparison rate of 4.15%).

As we highlighted yesterday, mortgage stress is on the rise with more than one million households under pressure, and these rate rises will created more pressure on household budgets.

In a statement this morning, Bank of Queensland said the BOQ and Freedom had mutually agreed to terminate the St Andrews Insurance sale and purchase agreement.

“Following the termination of the agreement with Freedom, BOQ will continue to assess its strategic options in relation to St Andrew’s. In the meantime, St Andrew’s continues to be a strongly capitalised business that remains focused on delivering for its customers and corporate partners,” BOQ said.

The troubled Freedom Insurance Group last week completed its

strategic review, which was prompted by ASIC’s recommendations about the

life insurance industry.

As part of the review, which was conducted in collaboration with

Deloitte, the Freedom board identified that the company may face a

liquidity shortfall during calendar year 2019 arising from the timing of

payments of commission clawbacks in the absence of receipts of

commissions from new business sales.

Freedom had been pursuing equity funding for the purposes of the St Andrews acquisition, the process of which has included the provision of confidential due diligence to prospective third-party investors and negotiation of related transaction documentation.

it became clear that the conditions of the transaction would not be satisfied within the time limits contained in the sale agreement they said..

“In this regard, the company is considering alternate options to address the potential shortfall,” the group said in a trading update”.

“In addition, Freedom is implementing initiatives to improve operational efficiency and reduce costs.”

Freedom expects to make a provision for net remediation costs in its

financial accounts for the period ending 31 December 2018 of between

approximately $3 million and $4 million.

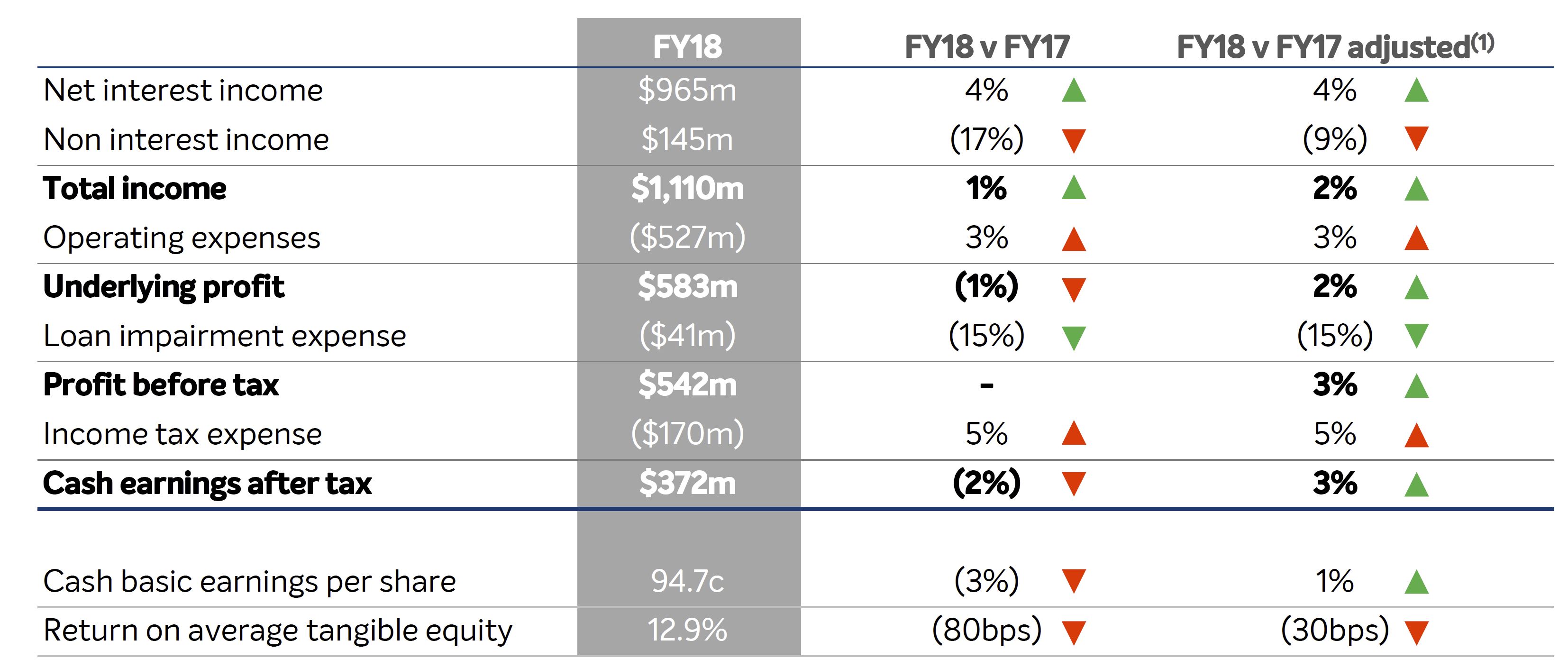

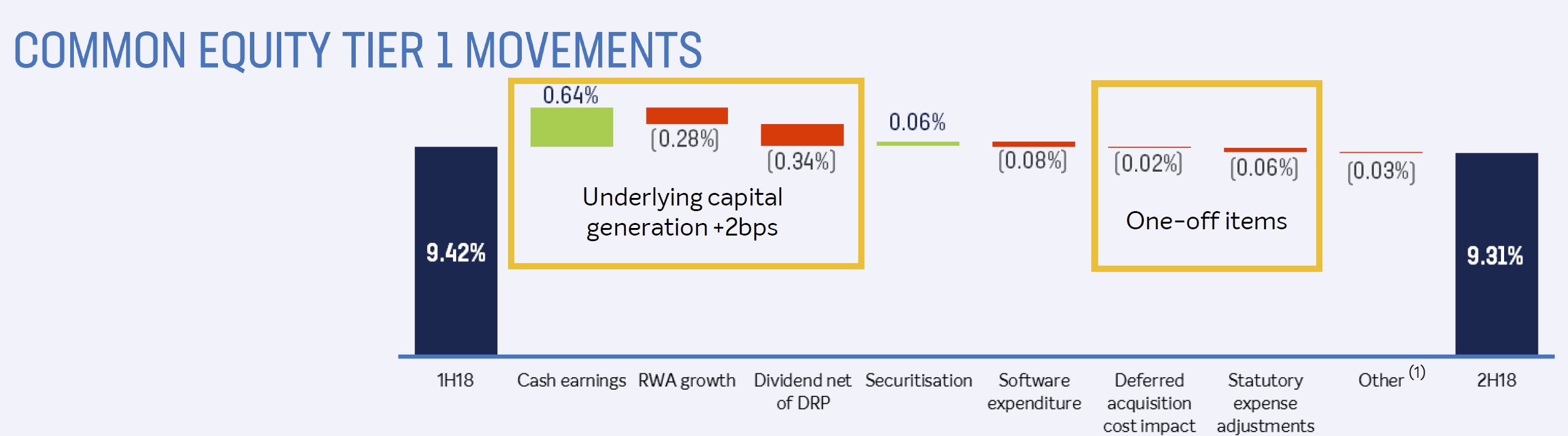

The Bank of Queensland have announced FY18 cash earnings after tax of $372 million, down two per cent on FY17. Statutory net profit after tax of $336 million, was down 5%.

Being a regional is a tough gig, and they continue to drive significant digital transformation, but despite some accounting wizardry, the cracks are showing in our view. The tighter home lending sector, and reduce fee income both hit home. As a result capital is weaker than expected.

Statutory net profit after tax decreased 5 per cent to $336 million. The BOQ Board has maintained a fully franked final dividend of 38 cents per ordinary share. Basic earnings per share was down 3% to 94.7 cents. Their return on average ordinary equity down 50 bps to 9.9%

2H18 cash earning was $190 million and bad loan expenses were lower, down 15% to $41 million or 9 bps of gross loans.

Net interest margin ended the year at 1.98% a little higher, but reflected hedging cost headwind mitigated by improvements driven through funding mix and asset pricing, front book vs back book repricing and >2bps benefit from extension in weighted average life of housing loans, reflecting portfolio trends.

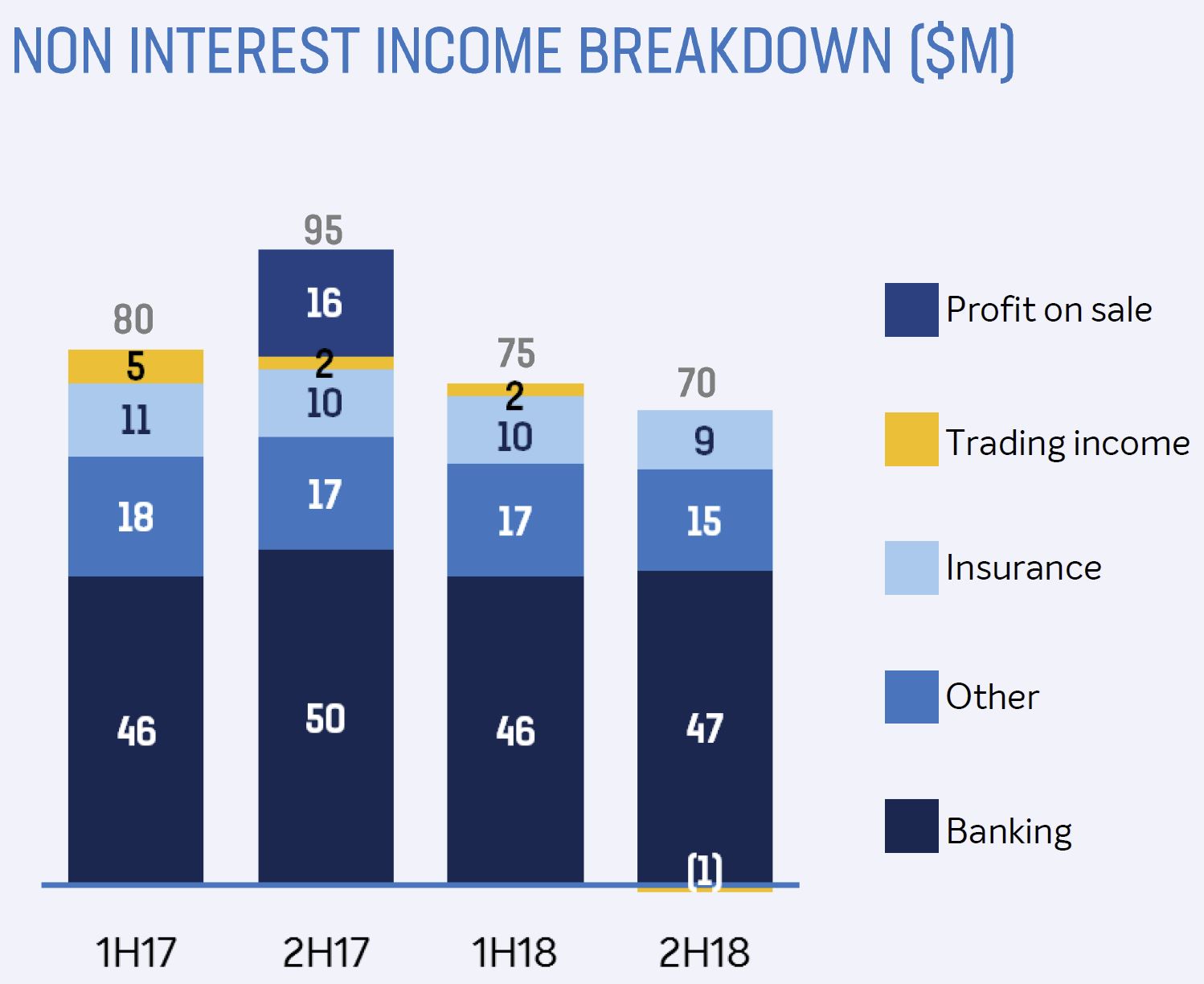

Non interest income fell thanks to ongoing pressure on banking fees, insurance income continuing to trend lower, and limited opportunities for trading income generation.

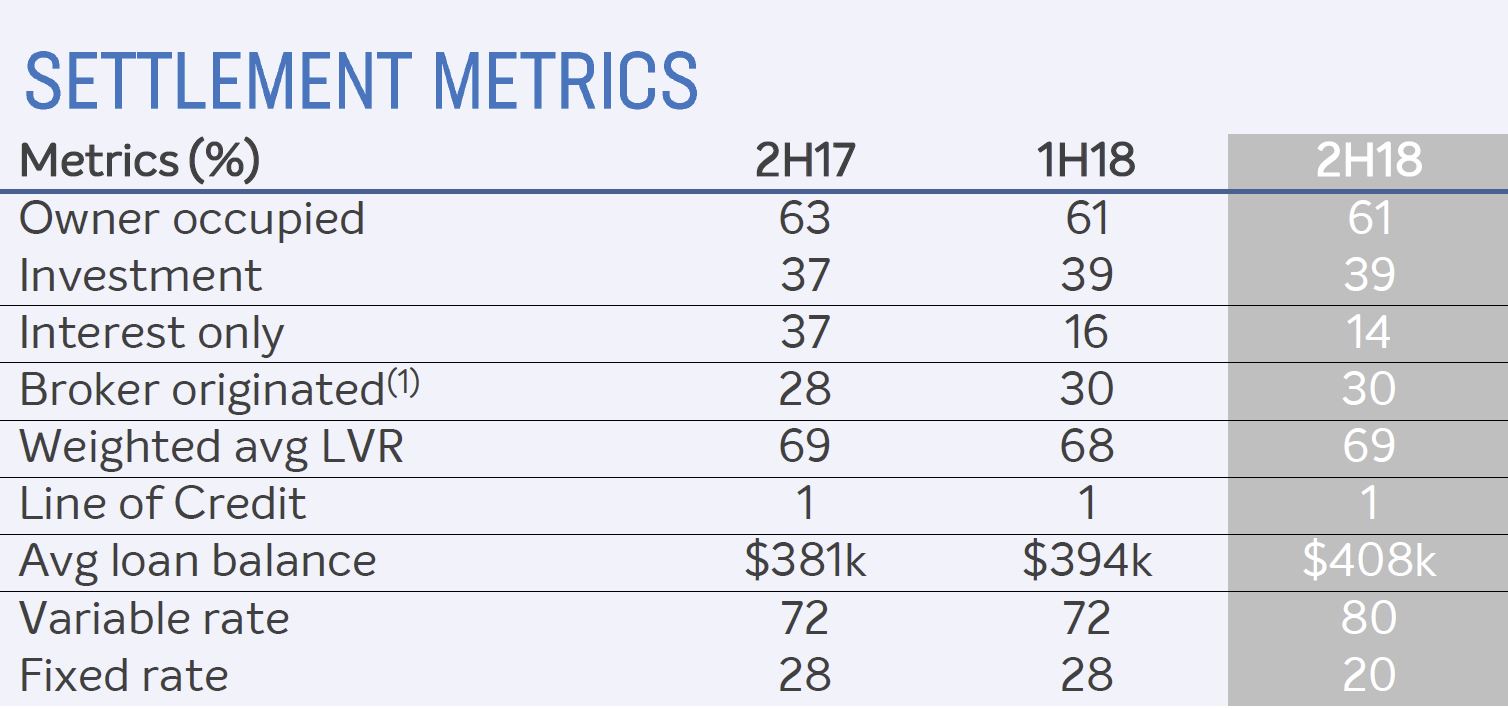

Within their housing portfolio, broker settlements were at 30%. Interest only settlements reduced significantly and owner occupied P&I loans represent 50% of portfolio.

Interest only loans are now 14% of new settlements, down from 37% in 2017. The average loan balance is growing (despite the tighter lending conditions across the industry). They hold 16% above an LVR of 81-90% and 8% greater than 90%.

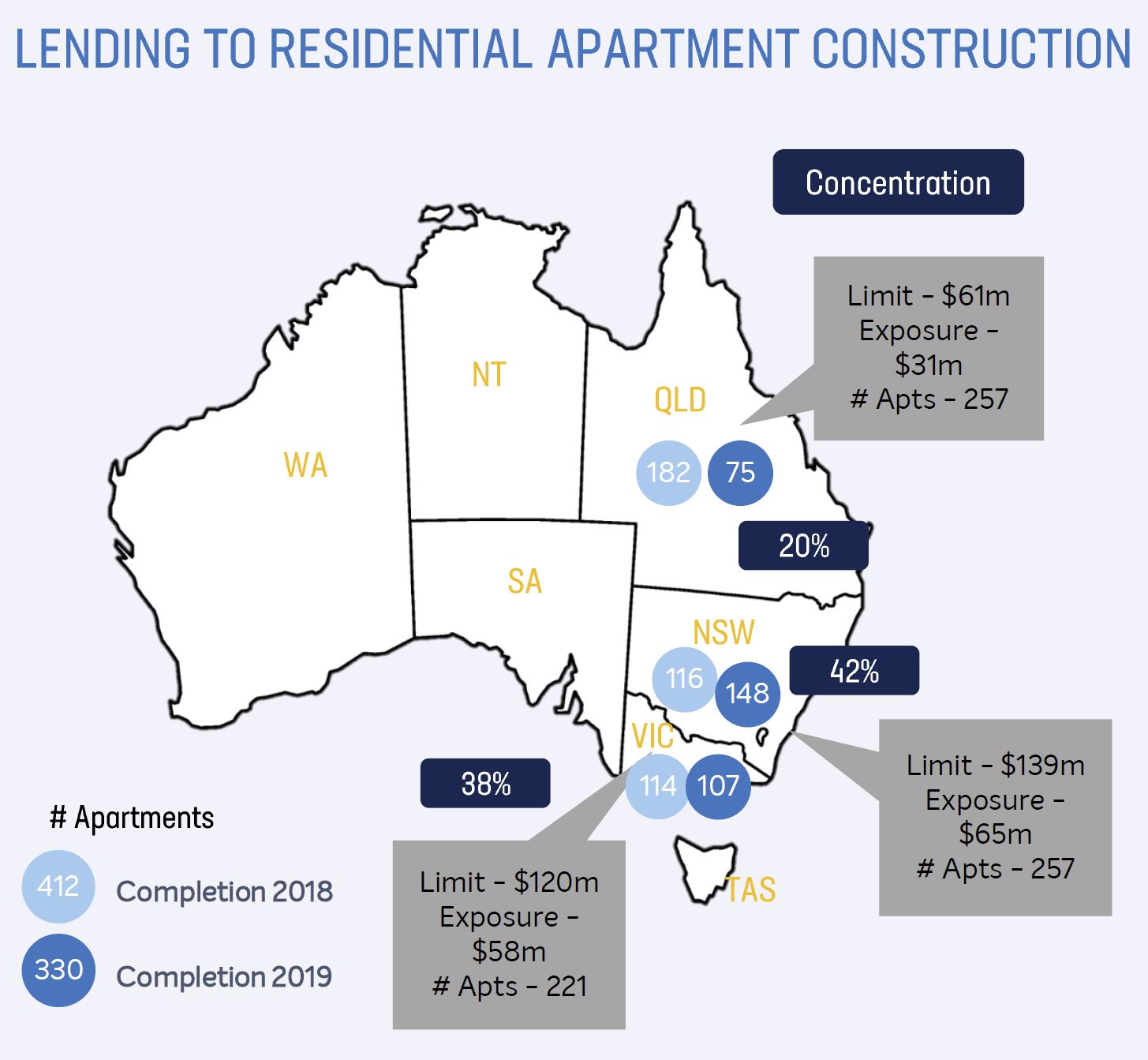

They have $154m current exposure to residential construction, representing 14 developments across 3 states, completing 2018 through 2019. They say it is well diversified intra-state within NSW and VIC.

Overall expenses grew at 3% and cost to income ratio was up 90 bps to 47.5%, despite core operating expense growing at 1%. They increased the amortization of ongoing IT investment and increased capital investment flagged for FY19.

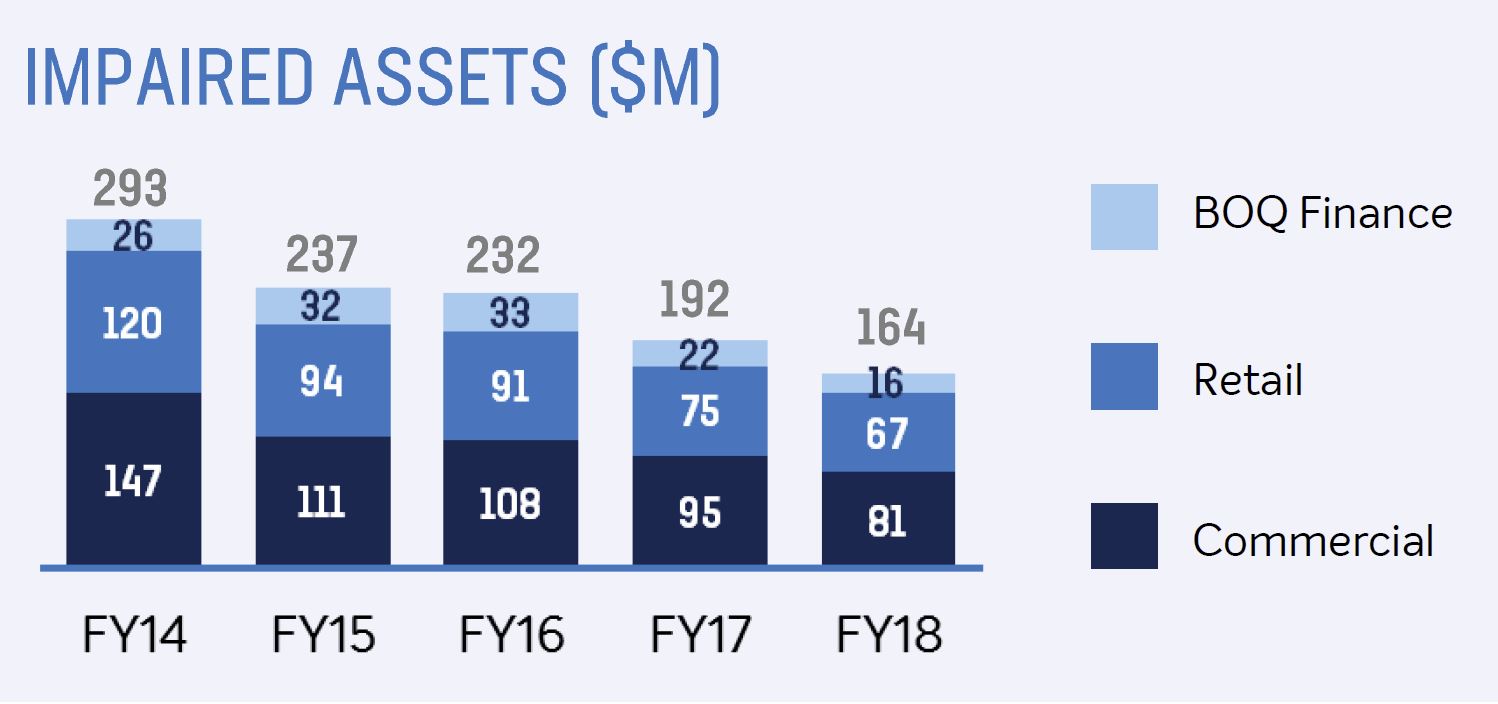

Impaired assets for the year stood at $164 million, down from $192 million in FY17.

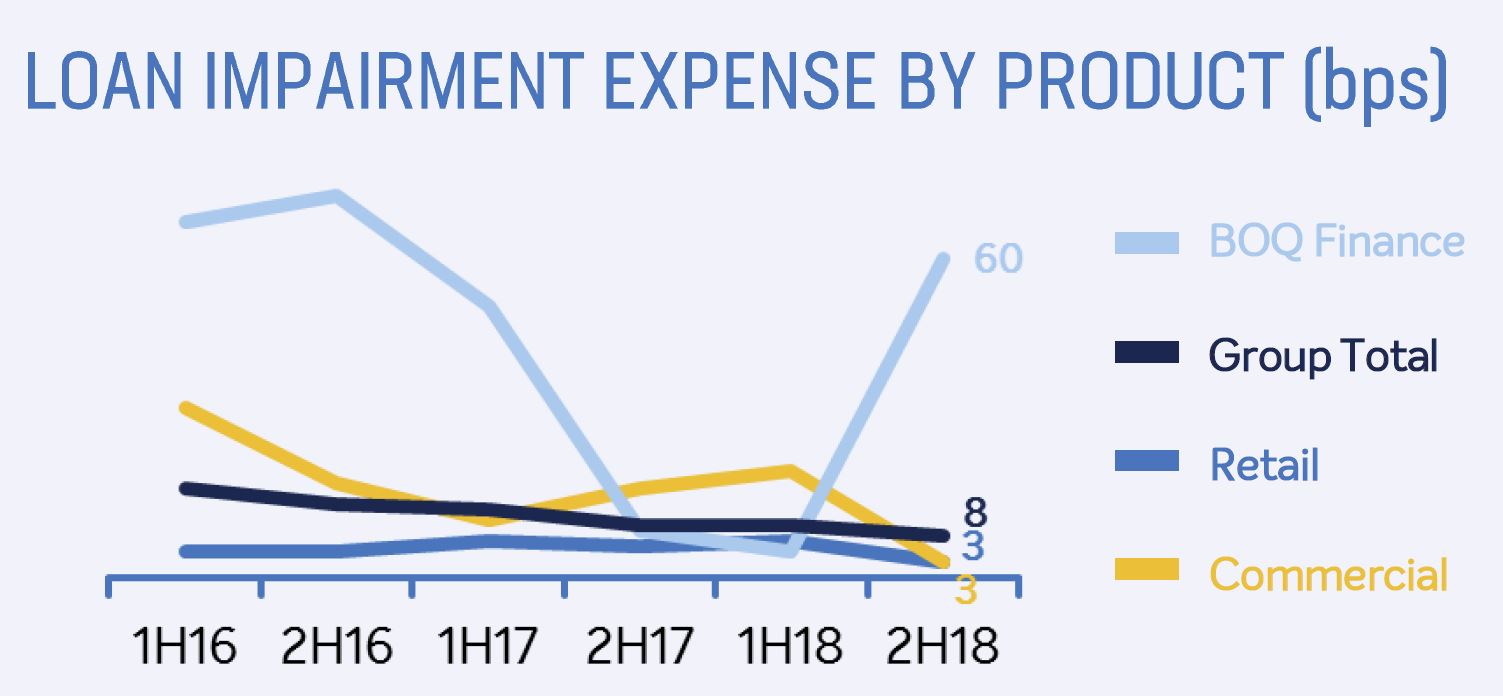

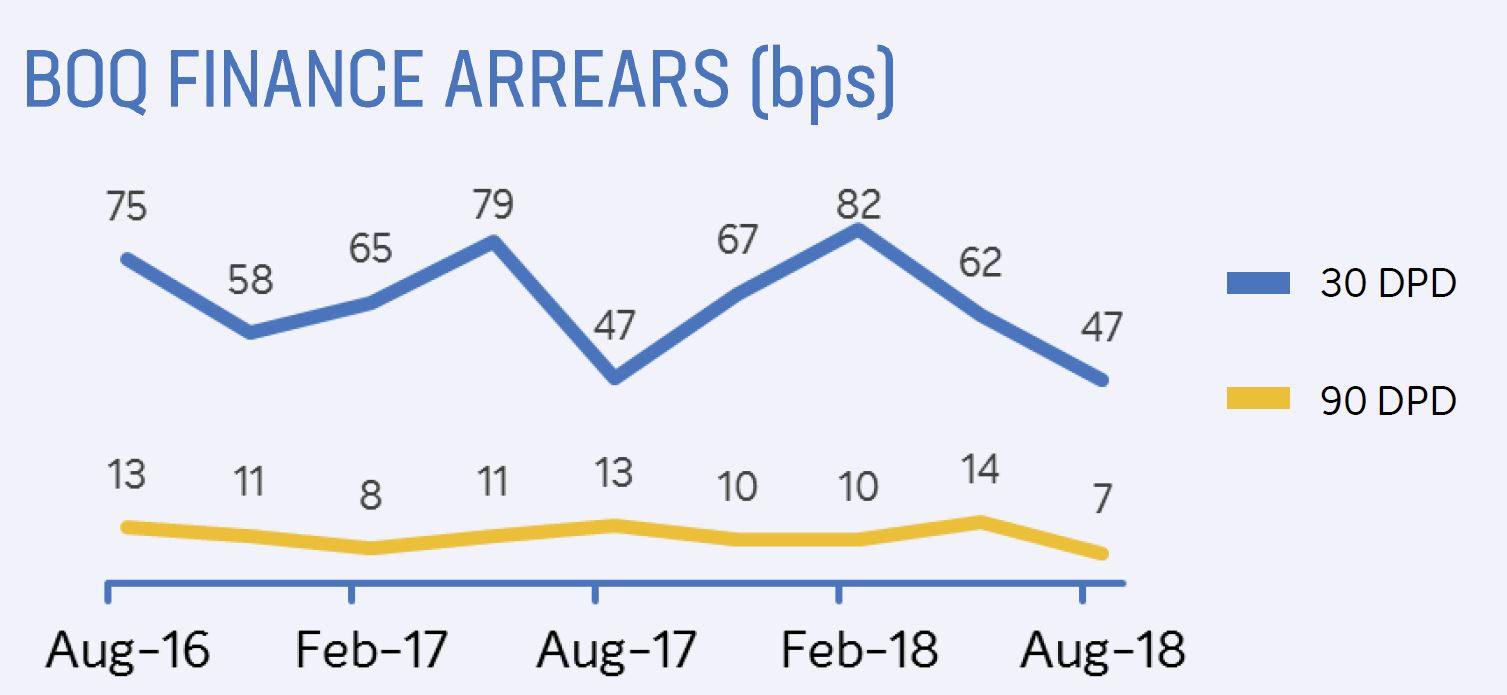

Loan impairments for BOQ Finance rose to 60 basis points in 2H18.

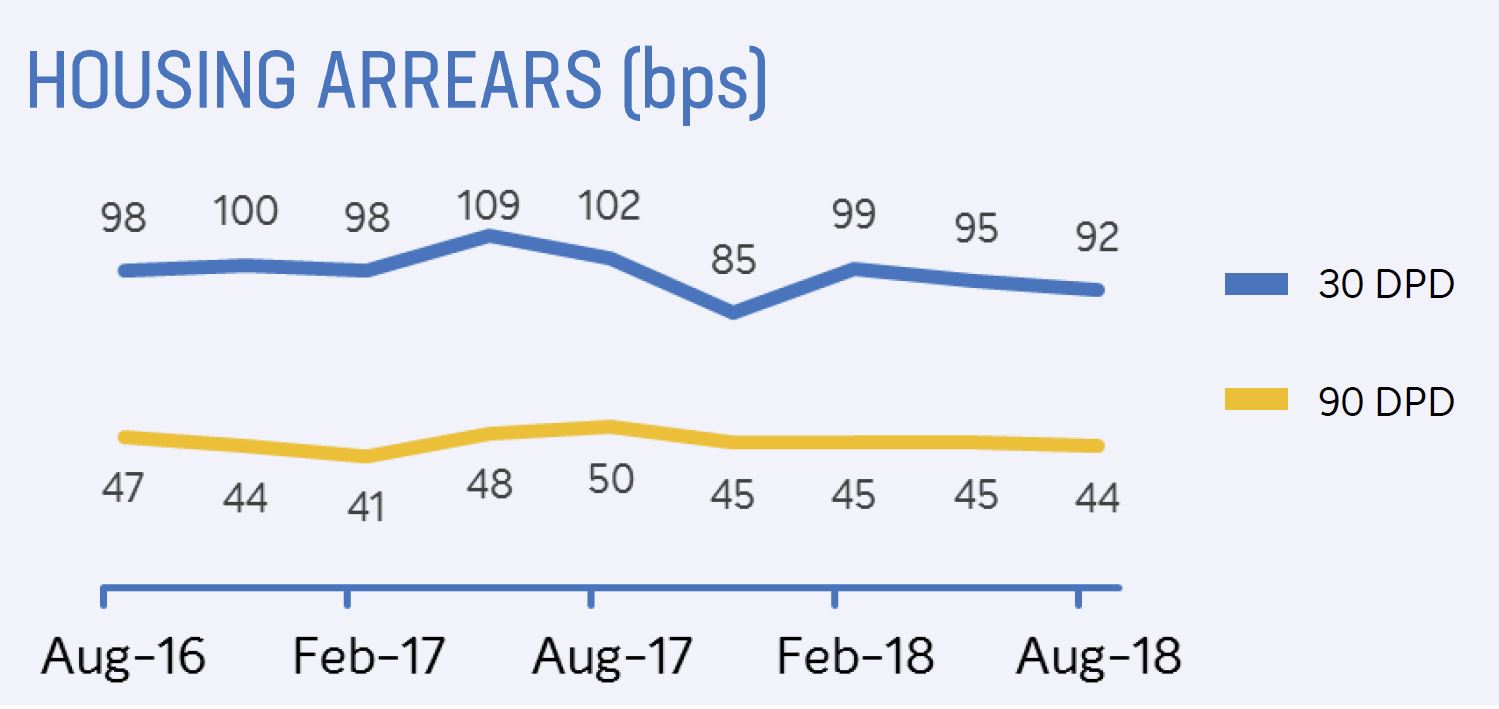

Housing loan arrears are relatively stable.

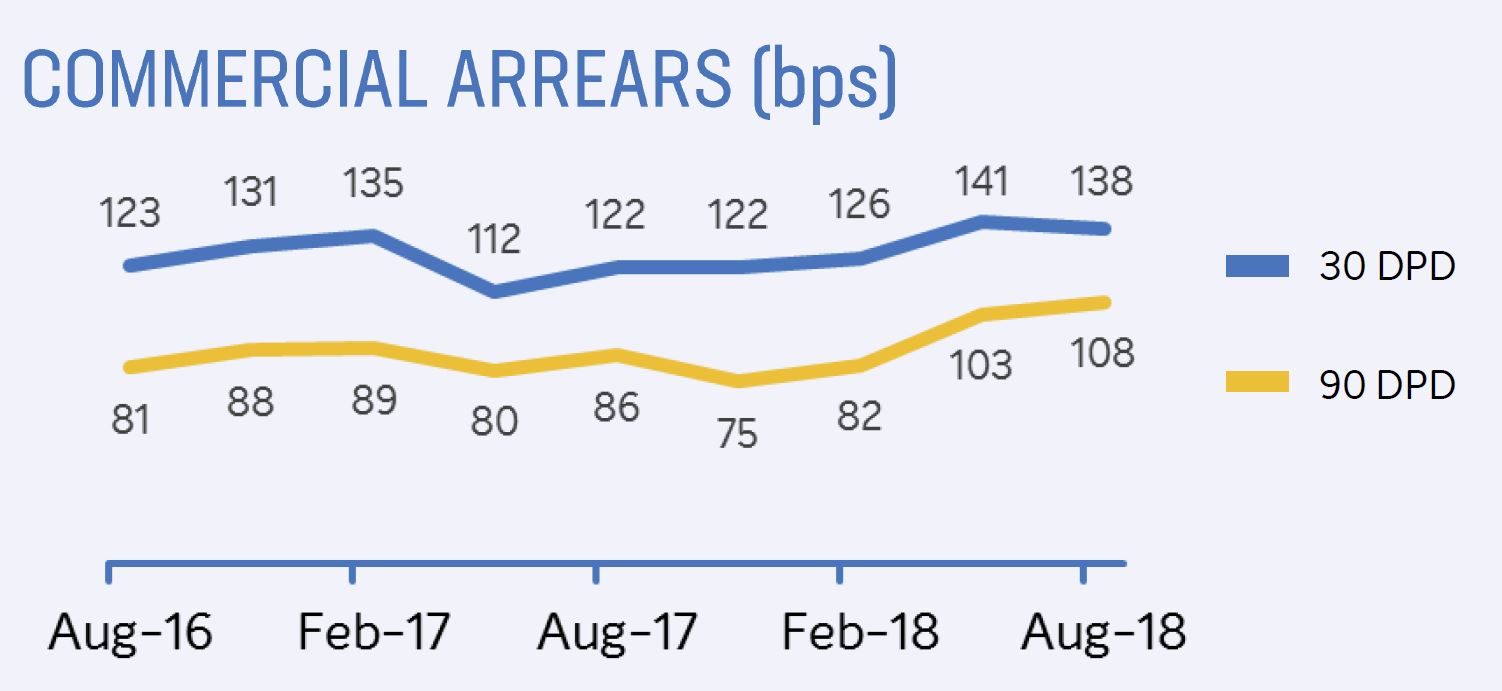

Commercial arrears past 90 day have risen.

BOQ finance arrears appear more volatile.

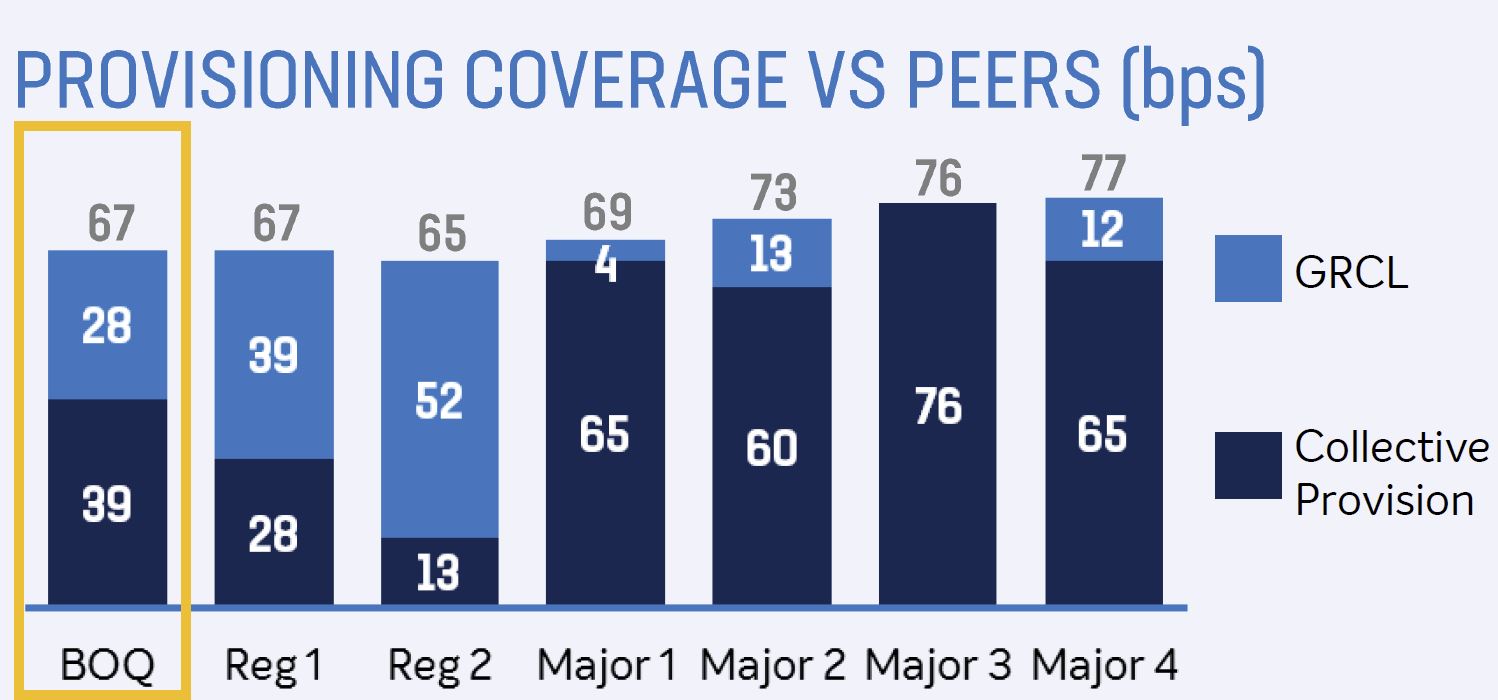

BOQ provisions are at the lower end of the spectrum compared with major players, but similar to other regionals.

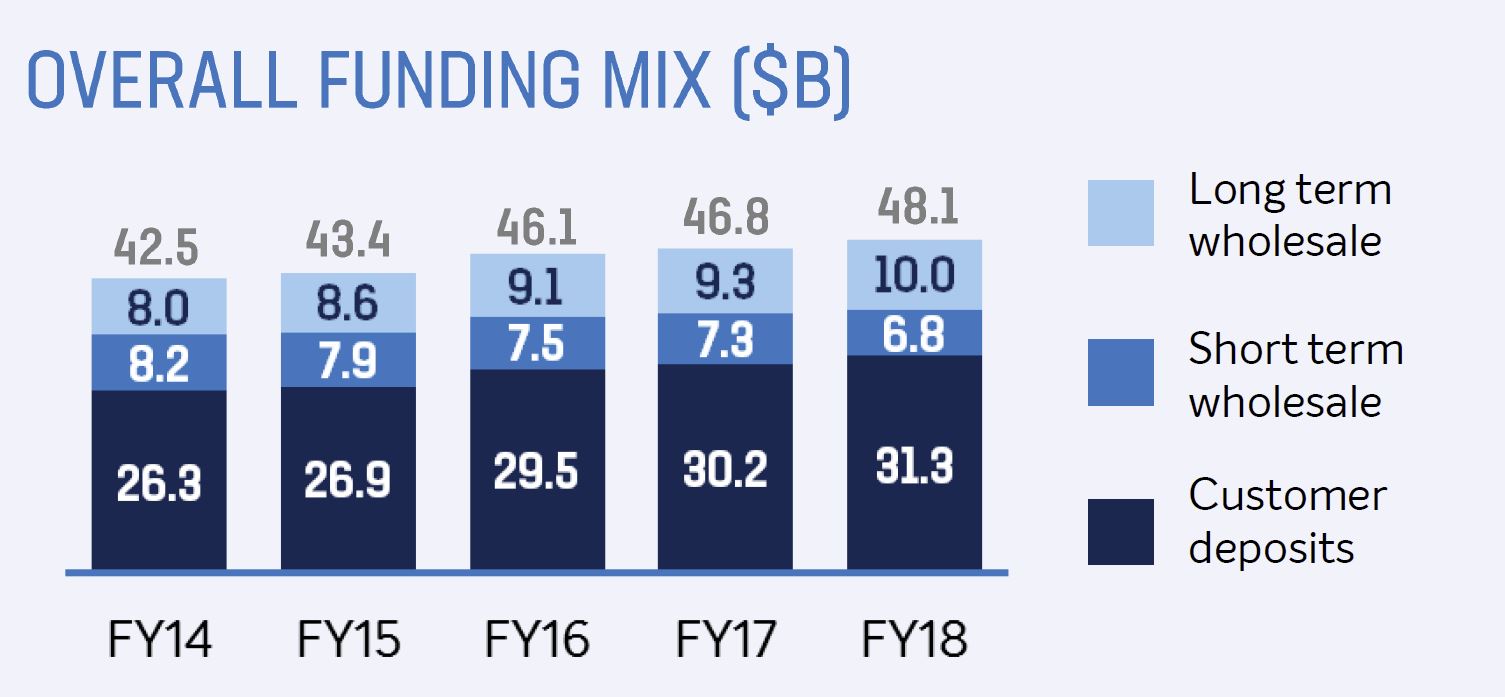

They had a deposit growth rate of 4% and 65% of loans are covered by deposits.

The CET1 ratio at 9.31% is lower than some analysts were expecting.

The underlying capital generation of +2bps, with an impact from one-off items of (8bps) and increased investment spend reduced CET1 by 8bps. We think the banks capital management flexibility is reduced, especially as it flagged it will use 7bps of excess capital over FY19/FY20 to accelerate digital investment.

Finally, its worth noting that there was no update on the progress of the St Andrews disposal, which remains ‘subject to regulatory approval’.

Bank of Queensland has announced it will be increasing interest rates across its variable home loans and Lines of Credit for owner occupiers and investors.

We expect other banks to follow, as they are all sitting on the same funding cost volcano.

BOQ said that the variable home loan rate for owner occupiers (principal and interest repayments) will increase by 0.09 per cent, per annum; variable home loan rate for owner occupiers (interest only repayments) will increase by 0.15 per cent, per annum; variable home loan rate for investors (principal and interest and interest only repayments) will increase by 0.15 per cent, per annum; and Owner occupier and investor Lines of Credit will increase by 0.10 per cent, per annum.

Anthony Rose, Acting Group Executive, Retail Banking said today’s announcement is largely due to the increased cost of funding.

“Funding costs have significantly risen since February this year and have primarily been driven by an increase in 30 and 90 day BBSW rates, along with elevated competition for term deposits.

“While the bank has absorbed these costs for some time, the changes announced today will help to offset the ongoing impact of the increased funding costs.

“These decisions are always difficult and BOQ balances the needs of our borrowers and depositors when making changes,” Mr Rose said.

The interest rate changes are effective Monday, 2 July 2018.