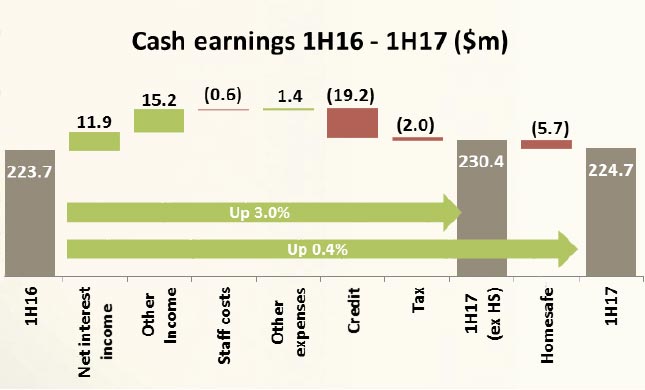

Bendigo and Adelaide Bank have announced an after tax profit of $415.6m, for the year to 30 June 2016. Cash earnings were $439.3m, up 1.6% on 2015, however, cash earnings in the second half were down 4% on the first half.

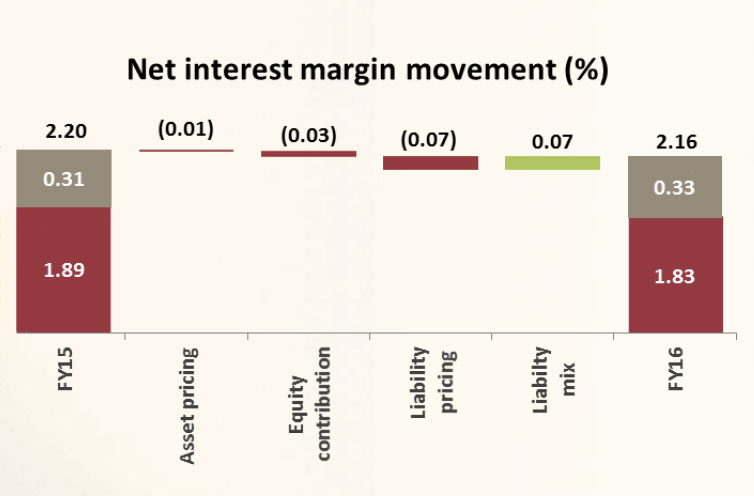

Earnings per share were 95.6 cents, a 0.6% increase on last year. Net interest margin fell 4 basis points compared with FY15, from 2.20% to 2.16%, though increased 1 basis point in the second half, thanks to retail deposits up 8%, to 82%, but against the headwind of fierce mortgage competition.

Return of tangible equity was 12.94%, down 34 basis points on last year, and down 44 basis point 2H16-2H15. Return on equity was also down from 8.94% in FY16 from 9.09% in FY15, a fall of 15 basis points. The dividend, however, per share rose to 68, compared with 66 last year.

The overall results are mixed, and shows the pressure on the bank. On the plus side, mortgage volumes and deposits were up, the asset quality is good – other than perhaps concerns in the rural portfolio, and Great Southern is becoming less of a problem. Finally, expense control is pretty robust, with more headroom, later.

However, the net interest margin is under severe pressure, and the latest competitor moves on home loan rates and deposits will only make this worse. Bendigo only passed on 10 basis points of the RBA cash rate cut. Term deposit competition is rising. Homesafe contains some property price risks, and the bank still has more to do on buttressing its capital base, compared with its peers. In the current low interest rate for longer scenario, Bendio will remain under some pressure. Whilst advanced IRB when approved, may help, a little, but it is not likely they will get to a 25% rate like the majors.

Overall it will be an uphill struggle. Dividends may have to be trimmed to square the circle, into 2017.

Looking in more detail:

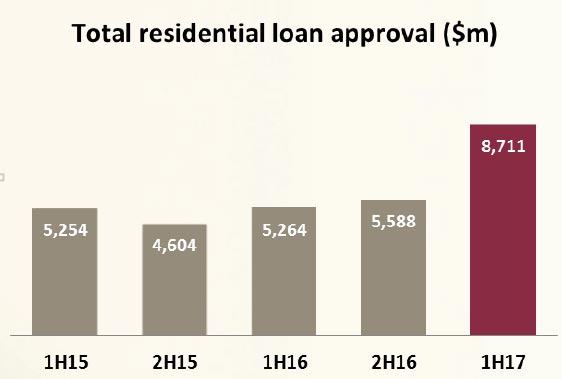

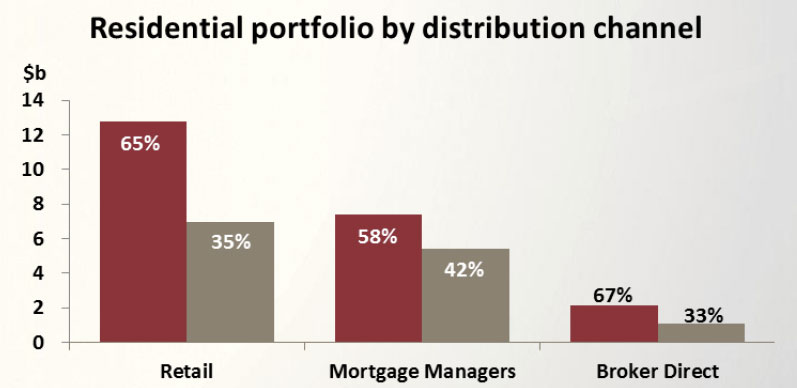

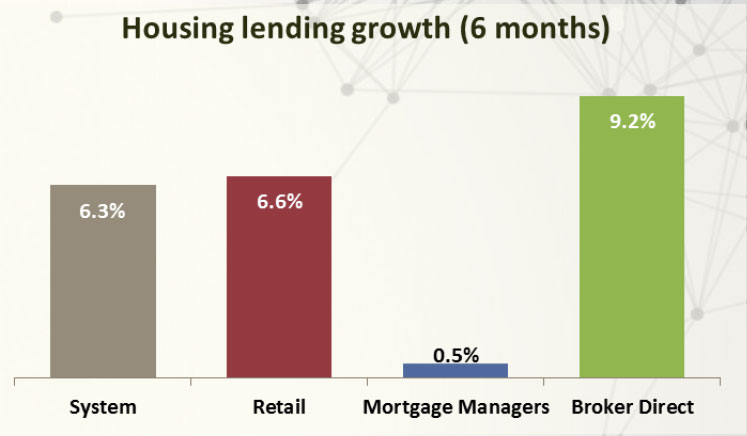

Home lending benefited from the relaunch of Adelaide Bank Broker Direct proposition and a new retail mortgage “Connect Package”. The Mortgage Manage portfolio stablised.

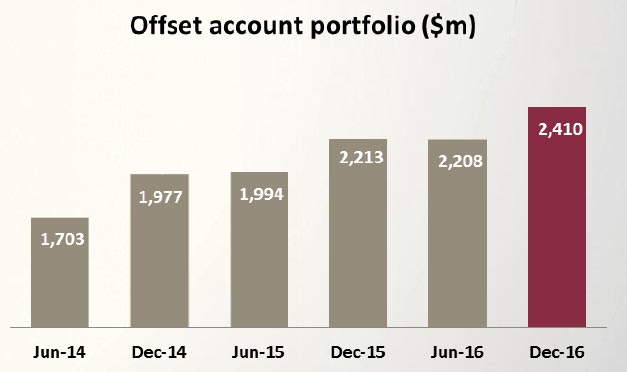

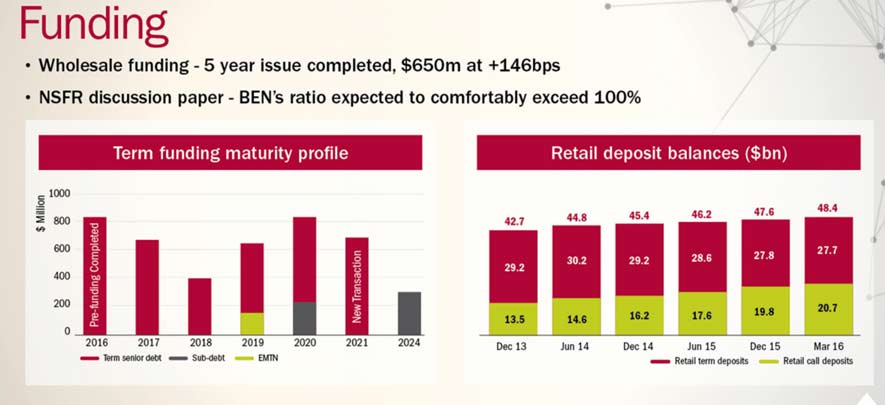

Retail Deposits grew, especially the useful term deposits, whilst wholesale funding and securitisation reduced in the funding mix.

Retail Deposits grew, especially the useful term deposits, whilst wholesale funding and securitisation reduced in the funding mix.

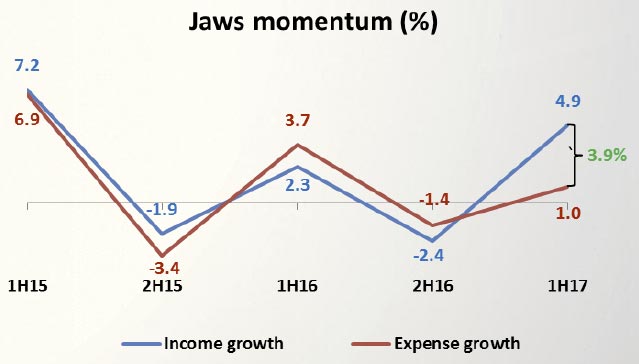

The banks costs rose 1.5% year on year, and the expense to income ratio rose from 55.1% to 56%.

The banks costs rose 1.5% year on year, and the expense to income ratio rose from 55.1% to 56%.

The jaws momentum, tells the story. Expenses are controlled, and they are targetting flat growth in FY17. The efficiency programme generated gains of $7m this year, and more next year. There was in increase in the capitalisation of expenses, and the advanced IRB status, when achieved will create more capacity in this regard.

The jaws momentum, tells the story. Expenses are controlled, and they are targetting flat growth in FY17. The efficiency programme generated gains of $7m this year, and more next year. There was in increase in the capitalisation of expenses, and the advanced IRB status, when achieved will create more capacity in this regard.

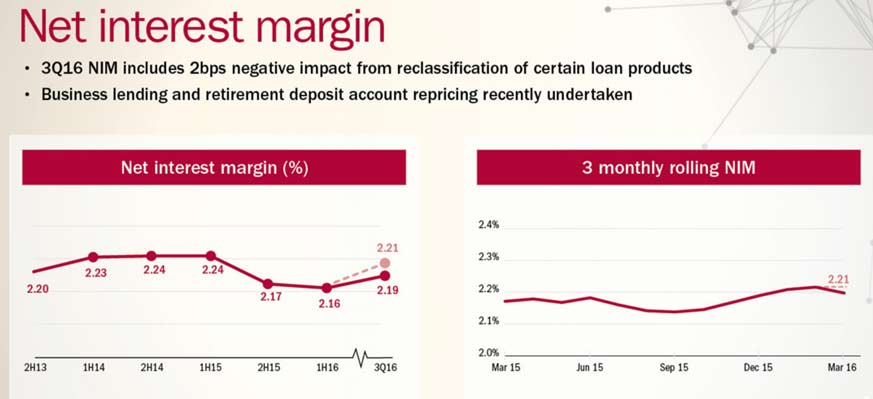

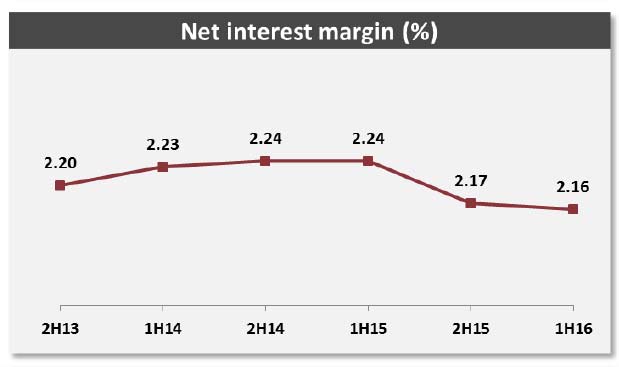

Looking in more depth, NIM tells an important story, with the drop from 2.20 last year to 2.16 in FY16.

Looking in more depth, NIM tells an important story, with the drop from 2.20 last year to 2.16 in FY16.

The trend is not pretty, reflecting the competition in the home loan market, pressure to capture retail deposits, and a reduction in securitisation.

The trend is not pretty, reflecting the competition in the home loan market, pressure to capture retail deposits, and a reduction in securitisation.

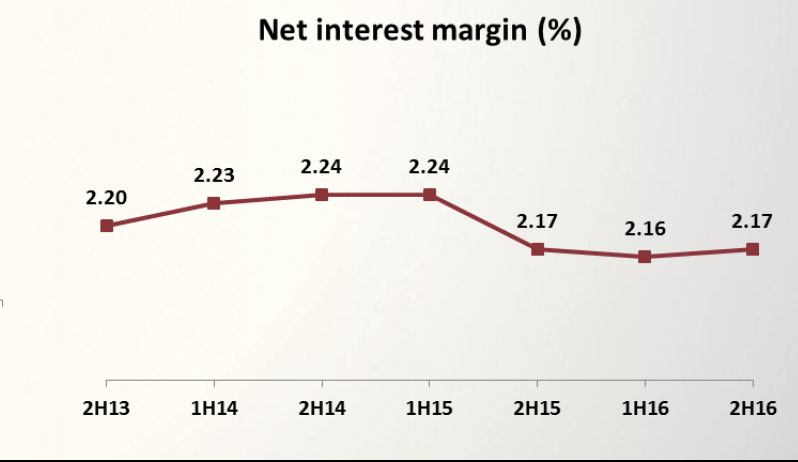

The monthly movement underscores the issue.

The monthly movement underscores the issue.

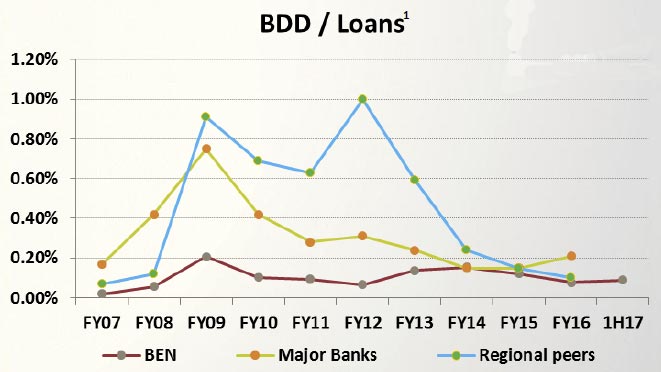

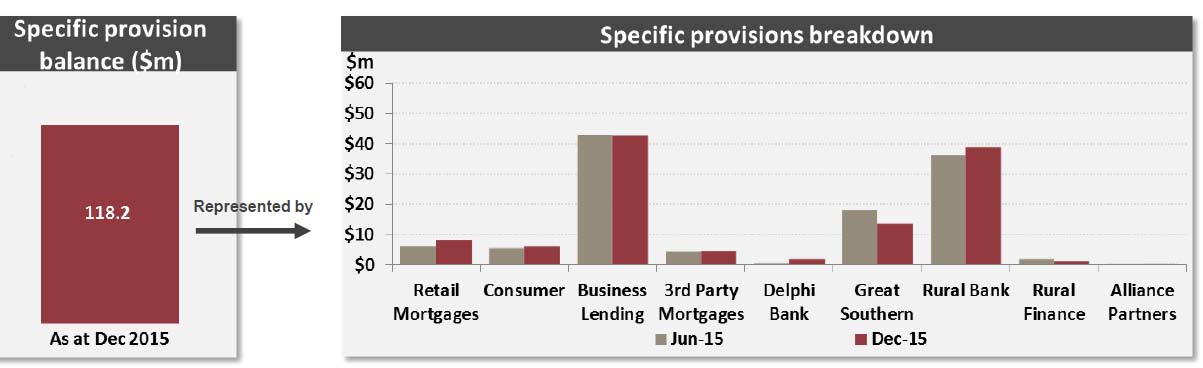

Bad and doubtful debts were down 35% from FY15 at $44.1m.

Bad and doubtful debts were down 35% from FY15 at $44.1m.

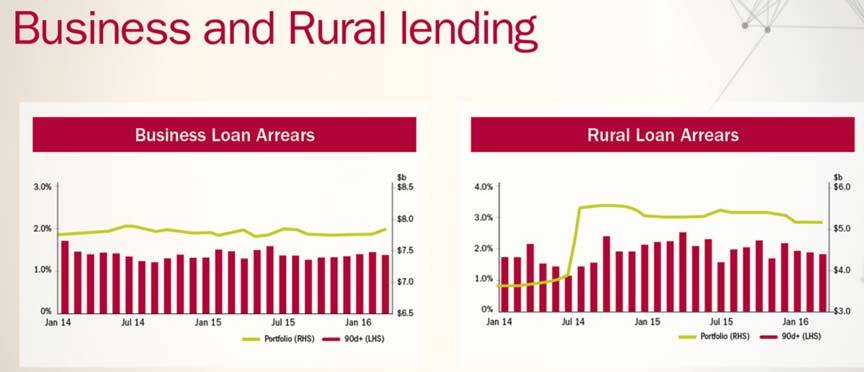

Business loans and mortgage arrears were stable, though the bank introduced an A$4m collective provision overlay for rural dairy exposures. Overall, rural loan arrears lifted quite noticeably in the last quarter. Total arrears before Great Southern rose by 16.4% in 2H16 and total impaired assets were down 2.0%.

Business loans and mortgage arrears were stable, though the bank introduced an A$4m collective provision overlay for rural dairy exposures. Overall, rural loan arrears lifted quite noticeably in the last quarter. Total arrears before Great Southern rose by 16.4% in 2H16 and total impaired assets were down 2.0%.

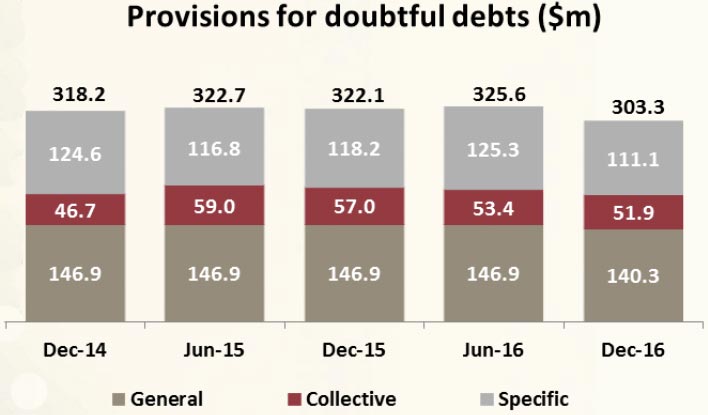

Great Southern provisions are behaving as expected with provisions down from $323.8m to $171.3m. Specific and collective provisions at June 2016 were $23.7m and $19.1m respectively. Collective provisions reduced by $6.1m and total borrowers fell from 3,321 to 1,821.

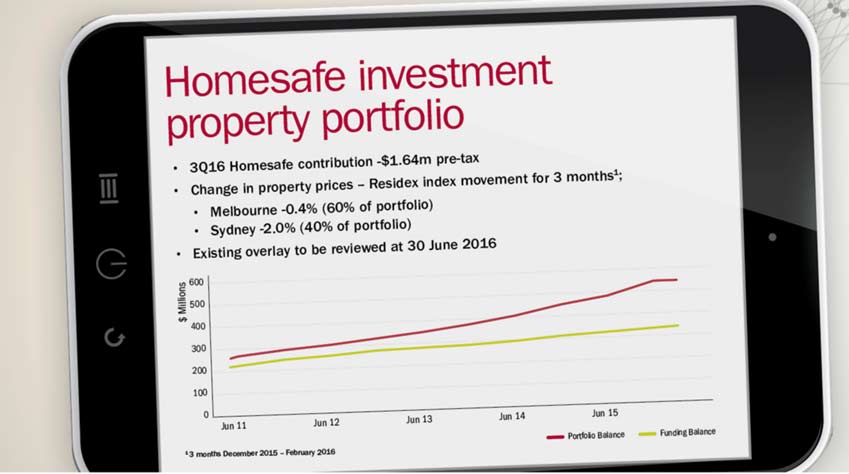

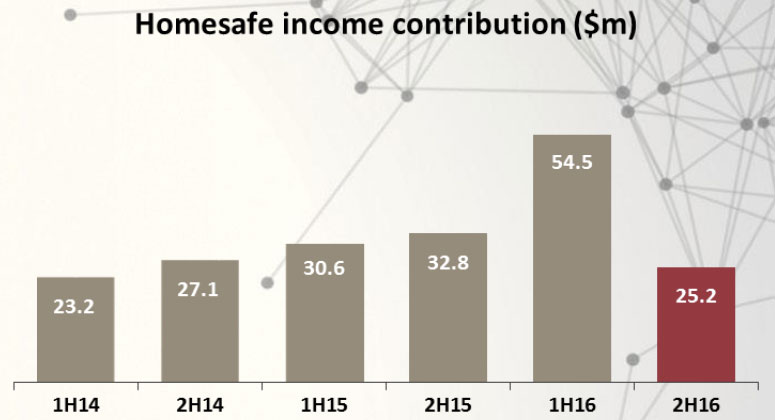

Homesafe contributed $54.5m in 1H16 and $25.2m in $H16, thanks to 10.8% rise in prices in Melbourne, and 9.2% in Sydney (Residex). Total funding provided is $343.6m. $6.4m of overlay was released in 2H16, reducing the total overlay to $23.6m. They assume 3% increase in property prices for the next 18 months, before returning to a long term growth rate of 6%.

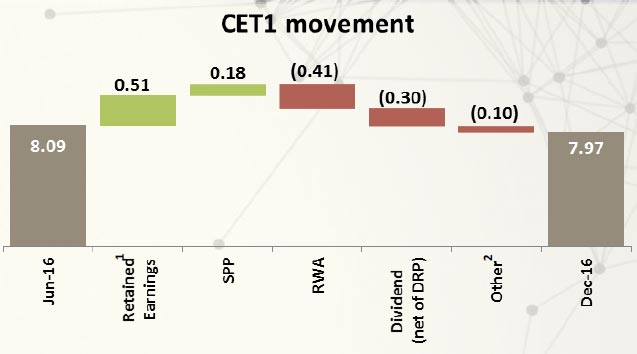

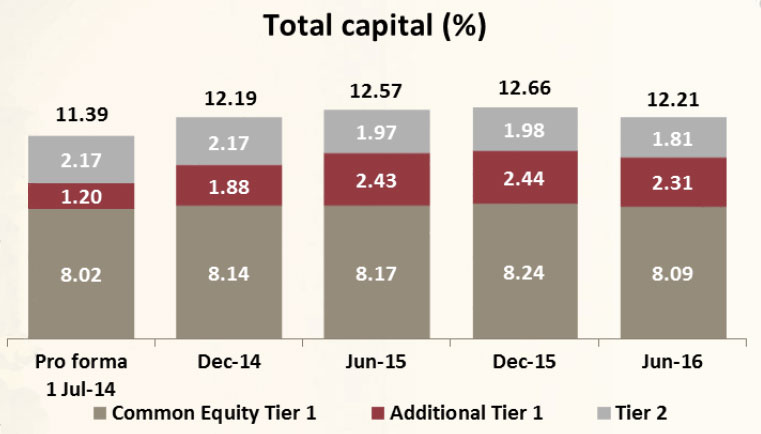

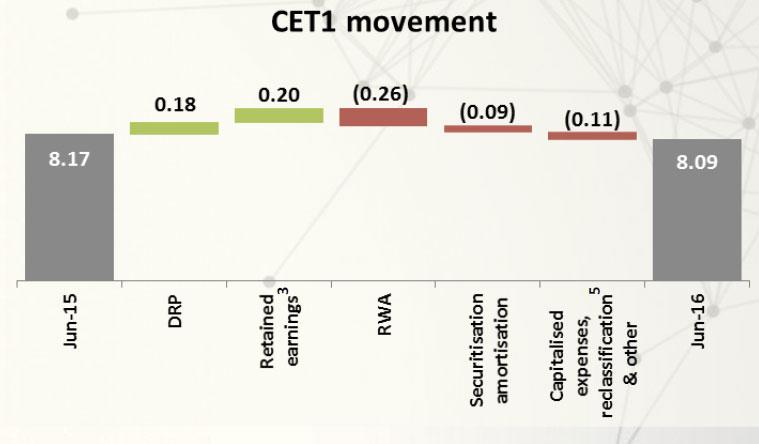

The banks indicative net stable funding ratio was 115% and the liquidity coverage ratio was 118%. Basel III CET1 ratio is 8.09% and total capital 12.21.

However the CET1 ratio was 8 basis points down from 1H.

However the CET1 ratio was 8 basis points down from 1H.

Realised earnings from completed contracts will still be included, but the mark-to-market element will now be excluded. Interesting timing given the fact that home price growth looks to be stalling! This will probably reduce the volatility of earning going forward. But Bendigo had a 6% long run home price growth assumption.

Realised earnings from completed contracts will still be included, but the mark-to-market element will now be excluded. Interesting timing given the fact that home price growth looks to be stalling! This will probably reduce the volatility of earning going forward. But Bendigo had a 6% long run home price growth assumption.