Recent media coverage about mortgage brokers has been quite negative, with allegations of poor ethical standards and false application data being used by some to bolster loan applications. So in this post and in our latest video blog we look at data from our household surveys to portray the current state of play.

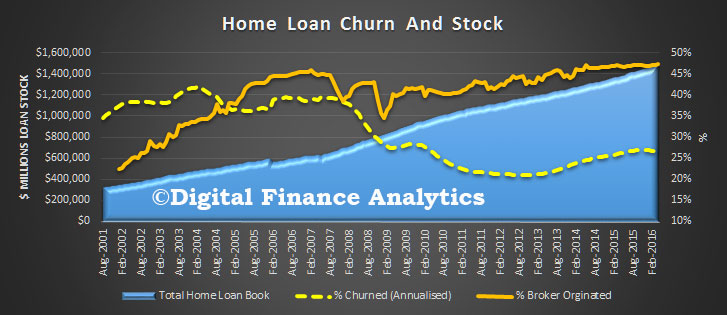

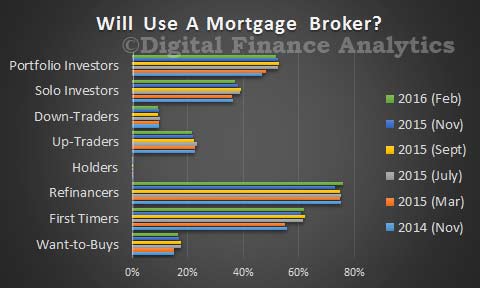

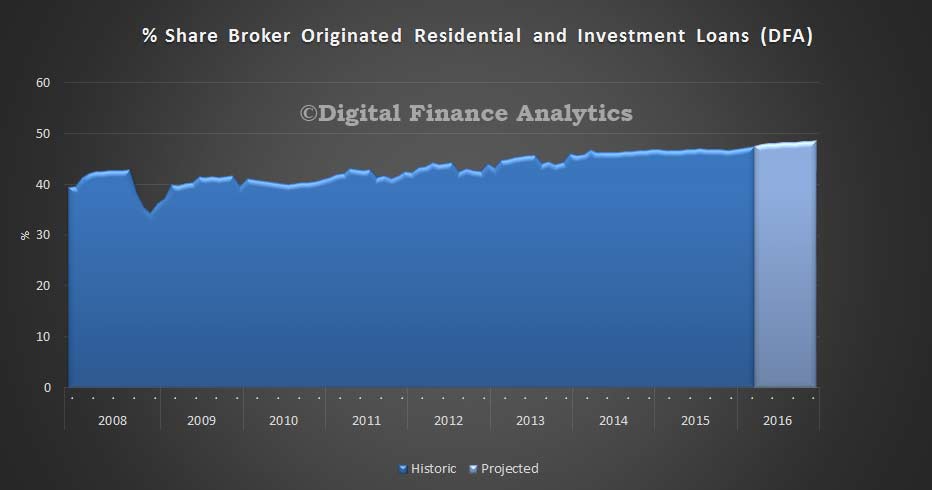

To begin, mortgage brokers have become a significant feature in the mortgage industry landscape. Indeed almost half of new loans are now originated by brokers. Different household segments have different propensities to use brokers. Those seeking to refinance, first time buyers and property investors are most likely to use a mortgage broker.

We expect this growth to continue, thanks to the current appetite for refinancing, and the broker focus now apparent among major banks. For example CBA, in their recent results reported to December 2015 that 45% of their loans came via the broker channel, up from 40% a year earlier. In addition regional players and credit unions are using brokers, alongside foreign banks operating here and the non-bank sector.

We expect this growth to continue, thanks to the current appetite for refinancing, and the broker focus now apparent among major banks. For example CBA, in their recent results reported to December 2015 that 45% of their loans came via the broker channel, up from 40% a year earlier. In addition regional players and credit unions are using brokers, alongside foreign banks operating here and the non-bank sector.

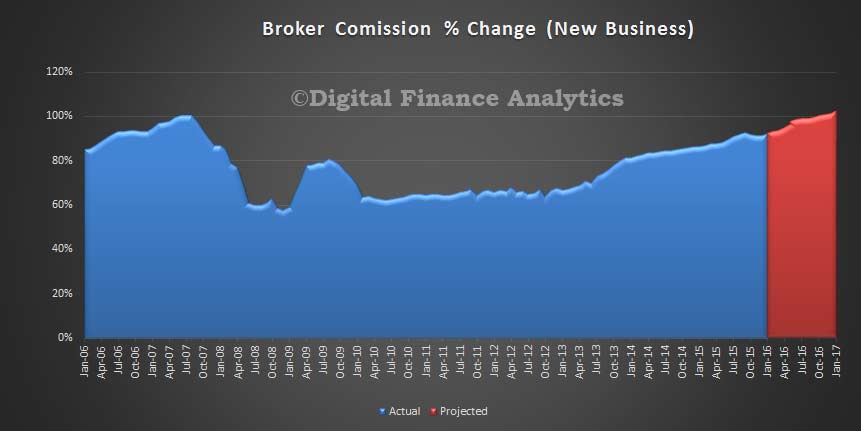

Commissions have been tweaked recently, and the industry commission take is now back up to pre-GFC levels, (after adjusting for inflation) because whilst overall commissions were trimmed, volumes have grown.

Commissions have been tweaked recently, and the industry commission take is now back up to pre-GFC levels, (after adjusting for inflation) because whilst overall commissions were trimmed, volumes have grown.

Remember that brokers get a commission payment at the start of the loan, as well as a trail paid in subsequent years. The bigger the loan, the bigger the commission. Very few aggregators normalise actual commissions paid – although Mortgage Choice does, so they claim their brokers are less influenced by commission structures.

Remember that brokers get a commission payment at the start of the loan, as well as a trail paid in subsequent years. The bigger the loan, the bigger the commission. Very few aggregators normalise actual commissions paid – although Mortgage Choice does, so they claim their brokers are less influenced by commission structures.

“At Mortgage Choice we pay your broker the same rate, no matter which home loan you choose from our wide choice of lenders. That means you can tap into a Mortgage Choice broker’s expertise at no charge, with peace of mind that they have your best interests at heart”.

Some brokers refund a proportion of the commission from the lender back to the borrower. For example Peach Home Loans says:

“When we arrange your loan we are doing quite a bit of the work that the lender’s staff would otherwise have to do and as a result the lenders pay us a commission on the upfront (loan amount) – this is typically around 0.6% or $600 per $100,000. We try to recover our costs from this commission and then share what is left over with you. Lenders also pay us a small trailing commission typically from 0.15% to 0.25% pa paid on the outstanding loan balance … and this is where we try to make our profit.. after all we are in business to make a profit.”

Consider next who is the broker working for? Whilst some are directly employed by banks or aggregators, others are self employed businesses. They are mostly aligned to aggregators or banks to get access to the lender lists and access to various tools and calculators. As a broker, they want to do a deal and the legislation controlling their conduct says they need to consider the financial status of an applicant to ensure the loan is “not unsuitable.” From ASIC’s responsible lending provisions:

“As a credit licensee, you must decide how you will meet the responsible lending obligations. RG 209 sets out our expectations for compliance. Meeting your responsible lending obligations will require taking three steps:

- make reasonable inquiries about the consumer’s financial situation, and their requirements and objectives;

- take reasonable steps to verify the consumer’s financial situation; and

- make a preliminary assessment (if you are providing credit assistance) or final assessment (if you are the credit provider) about whether the credit contract is ‘not unsuitable’ for the consumer (based on the inquiries and information obtained in the first two steps).

In addition, if the consumer requests it, you must be able to provide them with a written copy of the preliminary assessment or final assessment (as relevant)”.

This is quite weak protection, because suitability may depend on many factors, including financial sophistication of the potential borrowers, income and expenditure assessments and other elements.

The list of lenders a broker may consider will depend on the lender panel they have access to. Most brokers will access a restricted list of potential lenders, and cannot offer a “whole of market” view of options. Quite often they will use on-line tools with a client to come up with the best deals, although often the basis for selection and lender recommendation is vague and is often not fully disclosed.

Some brokers are very proactive when it comes to shepherding the loan application through to funding, others less so. Some brokers will also keep a diary note to instigate a possible refinance conversation down the track.

But, to be clear, whilst many brokers will give good advice, they are in an area of potential conflict thanks to commissions, and limitations thanks to the panel. Brokers should be disclosing potential commissions and also their selection criteria.

The alleged poor conduct where brokers falsify applicant data is in our view a marginal activity of a “few bad apples.” That said, consumers should be using a mortgage broker with their eyes open. Ask yourself if the broker is truly working in your best interests.

APRA recently said that they considered loans written via brokers to be more risky than loans written direct by the banks. APRA chairman Wayne Byres said:

“Third-party originated loans tend to have a materially higher default rate compared to loans originated through proprietary channels.”

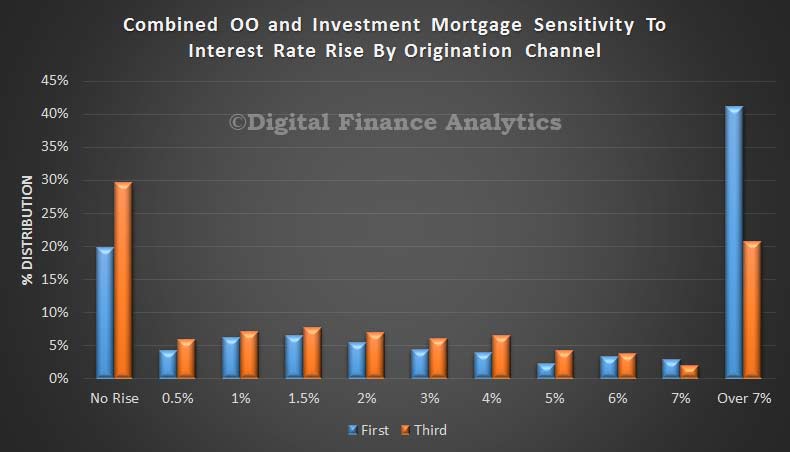

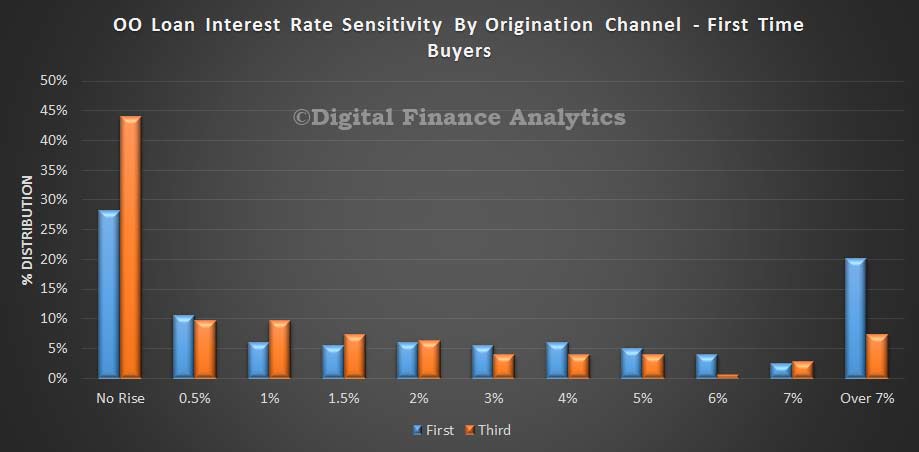

So we decided to analyse our current household survey data, looking at relative risks between third party (broker) and first party (bank) loans. We tested risks by asking households about their perceived sensitivity to interest rate rises on mortgage loans. You can read about our approach here.

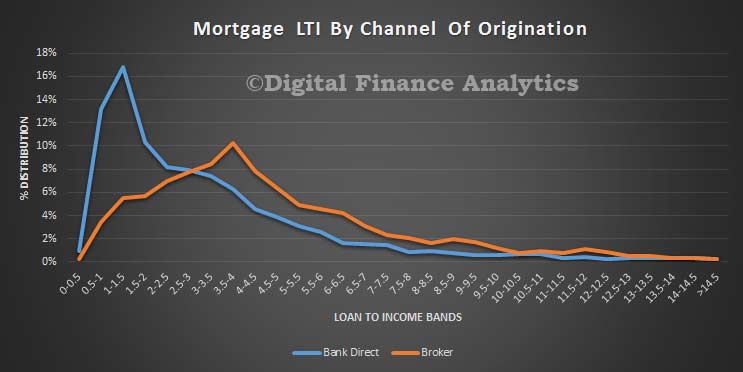

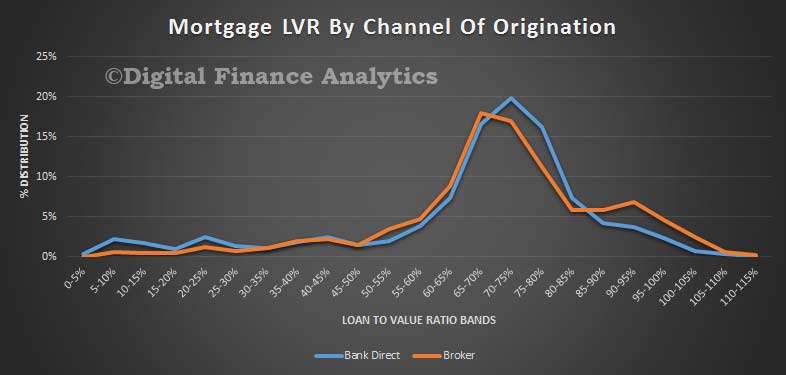

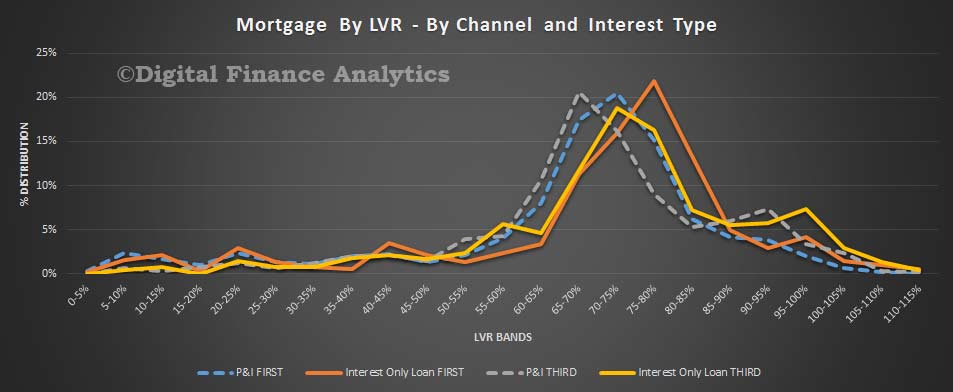

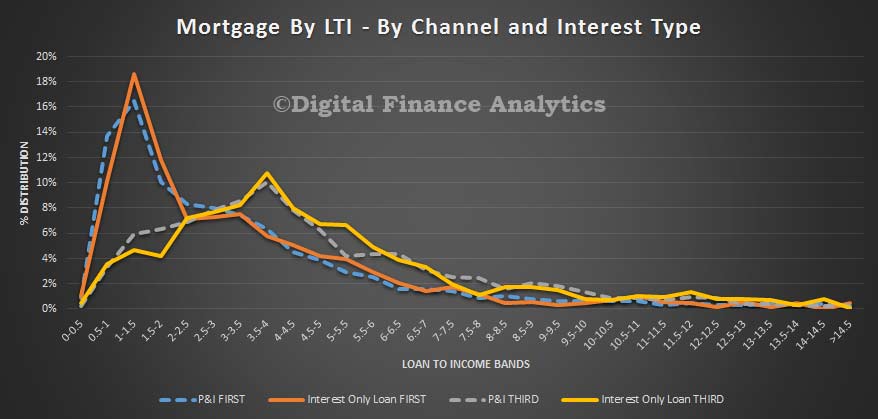

The results show that households who originated loans via brokers have less headroom and more exposure to potential interest rate rises (should they occur). For example, among owner occupied first time buyers, 28% of those who got a loan direct from a bank said they would have difficulty if rates rose at all from their current levels, whereas for owner occupied borrowers via a broker this rose to 43%, a significantly higher proportion. Further analysis showed that on average loans via brokers was at a higher loan to value and loan to income ratio than those direct via the bank.

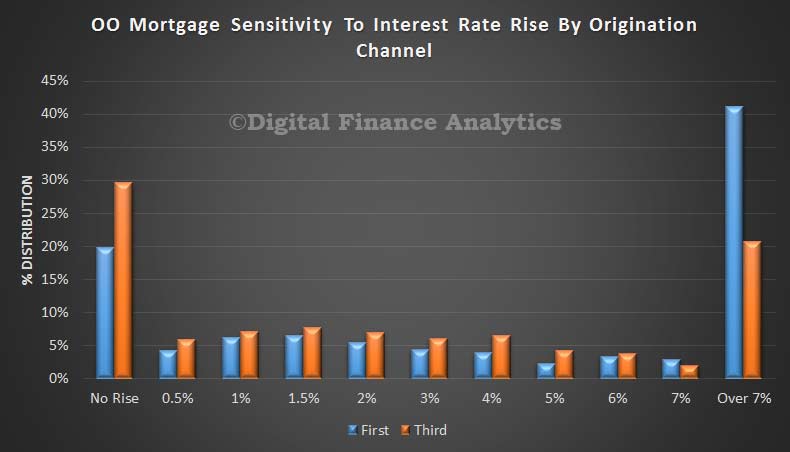

There was a similar, though less extreme shift in risk across all owner occupied portfolios, with 40% of borrowers direct from a bank saying they could cope with more than 7% rise, compared with 20% of those via a broker.

There was a similar, though less extreme shift in risk across all owner occupied portfolios, with 40% of borrowers direct from a bank saying they could cope with more than 7% rise, compared with 20% of those via a broker.

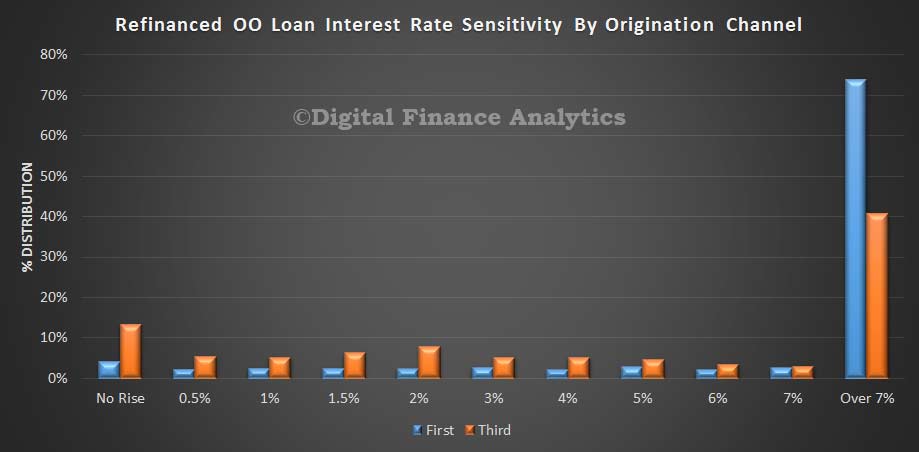

Looking at refinanced owner occupied loans we again saw a higher proportion less able to cope with a rise in rates among households who got their loan via a broker channel.

Looking at refinanced owner occupied loans we again saw a higher proportion less able to cope with a rise in rates among households who got their loan via a broker channel.

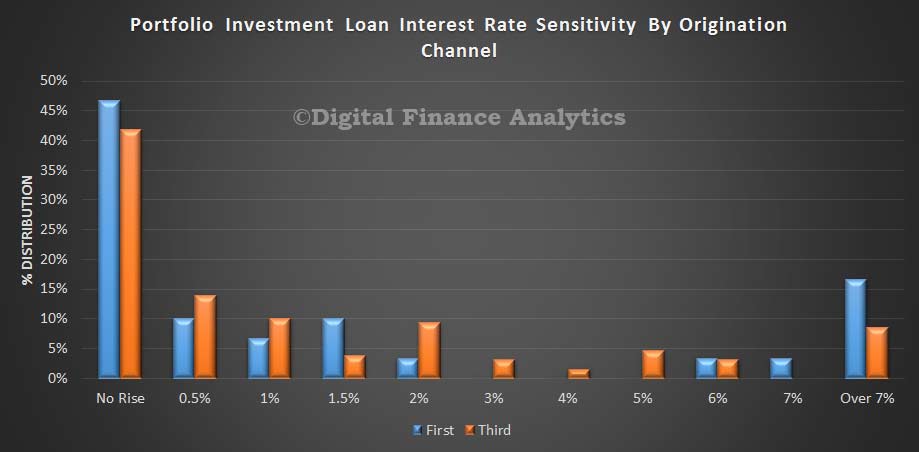

On the investment property side of the ledger, among portfolio investors – those with multiple properties in a portfolio, there was a higher proportion who would be exposed by any rate rise among those going direct to a bank, compared with a broker – but the difference is quite small and combined more than 40% of portfolio investors would have issues if rates rose.

On the investment property side of the ledger, among portfolio investors – those with multiple properties in a portfolio, there was a higher proportion who would be exposed by any rate rise among those going direct to a bank, compared with a broker – but the difference is quite small and combined more than 40% of portfolio investors would have issues if rates rose.

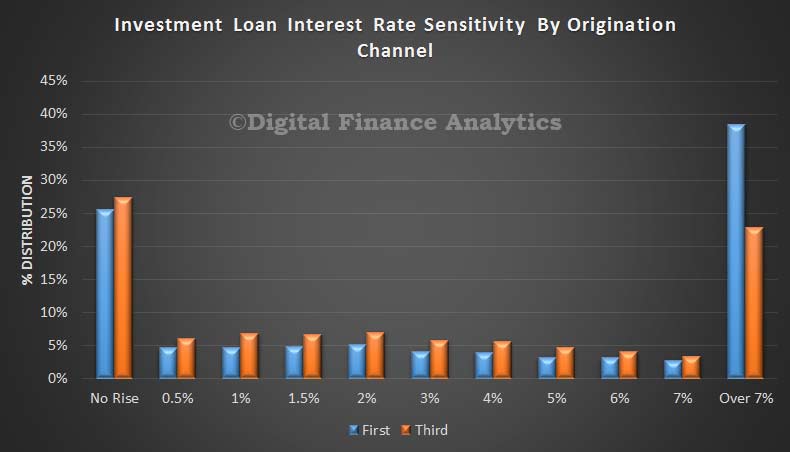

When we looked at all investment loans, we found that households who obtained a loan via a broker were slightly more likely to be under the gun if rates rose, and a significantly higher proportion of borrowers who went direct to a bank were confident of handling a rise of more than 7% from current levels.

When we looked at all investment loans, we found that households who obtained a loan via a broker were slightly more likely to be under the gun if rates rose, and a significantly higher proportion of borrowers who went direct to a bank were confident of handling a rise of more than 7% from current levels.

Consolidating all the results, we conclude that households who accessed loans via brokers have on average less head room to accommodate rate rises compared with those who went direct. APRA is correct.

Consolidating all the results, we conclude that households who accessed loans via brokers have on average less head room to accommodate rate rises compared with those who went direct. APRA is correct.