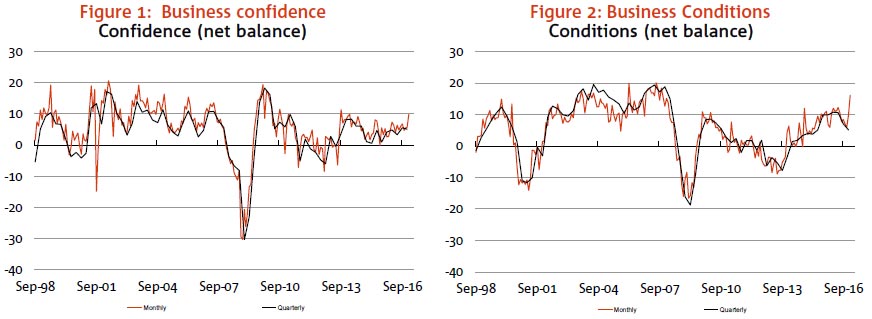

We look at the last business surveys.

Blog")

/

RSS Feed

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

We look at the last business surveys.

We look at the last business surveys.

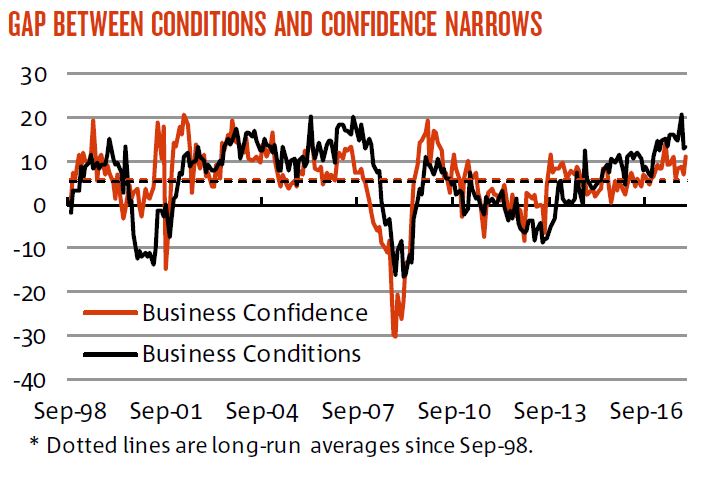

The recently released NAB monthly business survey to December 2017 reports a strong business sector in Australia at present, with conditions holding steady at well-above average levels and confidence almost catching up this month.

The business confidence index bounced 4pts to +11 index points, the highest level since July 2017, perhaps driven by a stronger global economic backdrop and closes the gap between confidence and business conditions.

Business confidence is strongest in trend terms in Queensland and SA and to a lesser extent NSW. Confidence is also reasonable in WA, and is in line with business conditions in the state. Victoria and Tasmania meanwhile are reporting levels of confidence which are lower than their reported level business conditions.

Mining and construction are the most confident, with the latter picking up in recent months after trending down between July and October, suggesting that a positive outlook for non-residential construction may be offsetting any concerns around apartment oversupply and a slowdown in the Sydney housing market. In contrast, retail confidence is surprisingly strong, and well above reported conditions. The retail industry has been a consistent underperformerin the NAB Business Survey, and is the only industryreporting negative business conditions.

The employment index pulled back a little in December, and while it remains consistent with a solid rate of job creation, it does suggest employment growth may ease back from current extraordinary heights.

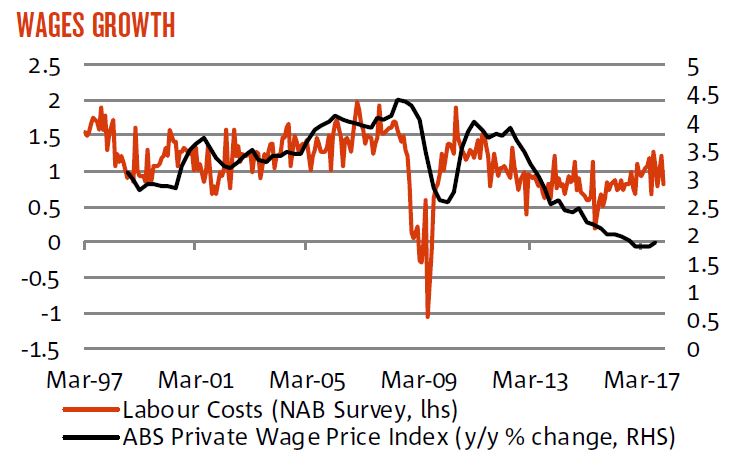

But whether this will begin to lift wages growth is another question, with labour costs rising.

Australian businesses have never had it better, according to the latest National Australia Business (NAB) survey released today.

The survey’s conditions index — a composite indicator that measures trading activity, profitability and employment — surged by a massive 7 points to +21, leaving it at the highest level since the survey began in 1997.

On this measure, Australian businesses have not had it this good in at least two decades.

As the chart below shows, there were enormous increases recorded in trading and profitability, suggesting that demand was rampant during October.

Source: NAB

But are business conditions as strong as the NAB survey suggests?

While no one doubts that things have improved over the past year — strong growth in employment, for one, suggests they have — but the strength in the NAB survey is significantly greater than in other alternate business indicators such as the Ai Group’s measures on manufacturing, services and construction activity levels.

Like the NAB survey, they too have been around for years, and they paint a very different picture on the current momentum in the business sector.

In October, respondents in those surveys reported that activity levels improved at a slower pace than September, and well below the levels seen just a few months ago.

Services fell to 51.4, manufacturing to 51.1 and construction to 53.2, remembering that a reading over 50 indicates that perceived activity levels improved from one month earlier.

So activity levels improved according to those surveys, but at a marginal pace.

While they are constructed differently, they both look at perceived business conditions in Australia.

And while the Ai Group respondents did report an improvement in activity levels, one has to ask whether that would lead to the boom in profitability and trading conditions reported by respondents in the NAB survey?

Given the divergence, caution is understandably warranted.

That’s something that Alan Oster, Chief Economist at the NAB, stressed following the release of October report, noting that a sharp improvement in manufacturing conditions contributed to the outsized move.

“This is an extremely strong result and of itself would suggest a better than expected performance for the economy,” he said.

“However, it is unclear just how long conditions can remain at these record levels given that the result was driven by a surprise jump in manufacturing.”

Adding to the need for caution, Oster said the surveys lead indicators also softened over the month, which, along with an unchanged reading on business confidence, raised questions as to whether the bounce in the conditions index can be sustained.

“Some of the leading indicators such as forward orders — which have been giving a more accurate read on the strength of the economy — have actually softened a little in recent months,” he said.

“Less upbeat readings on business confidence may also be telling, with firms previously indicating that uncertainty around the outlook for their business is holding confidence back.”

Given softer internals in the NAB report, along with the slowdown in other business indicators, it will be interesting to see whether the NAB’s conditions index will retrace its October surge next month.

Things are undoubtedly looking better for Australian business, but it’s probably best to keep the champagne on ice, says Tom Kennedy, Economist at JP Morgan.

“Although firms’ operating conditions have obviously improved, the sectoral momentum in the survey [from] manufacturing and mining makes us think that the magnitude of the improvement is overdone and the implications for economic growth and monetary policy need to be faded,” he says.

George Tharenou, Economist at UBS, agrees with Kennedy’s assessment.

“The conditions [index] is now giving an incredibly bullish signal on the economy with a spike to a record high,” he says.

“However, it has been average or above for most of the last three years and has just not translated through to the hard data like GDP, CPI or wages.”

John Fraser, Secretary to the Treasury spoke about Australia’s Business Investment Challenge in his Sir Leslie Melville Lecture.

The bottom line is as the mining investment boom ended, Australia has struggled with weak investment in the non-mining sectors, weighing on the labour market, productivity and ultimately economic growth.

Governments to pursue coordinated reforms that provide businesses with certainty, promote innovation and productivity improvements and support the ongoing transformation of the economy.

But there are no silver bullets!

One thing we know will be vital to our economic prosperity going forward is business investment.

Investment in new productive capacity creates employment opportunities, raises future incomes and supports innovation.

Recent Treasury research indicates that Australia has generally been more reliant on capital deepening than multifactor productivity growth to fuel its aggregate labour productivity growth.

This research is publicly available on the Treasury Research Institute website.

We are doing far more research in Treasury but some necessarily must remain confidential.

Productivity-enhancing policies are vital because of the link between productivity gains and real wage increases.

We know that higher productivity is the best way to increase real wages across the economy and, based on Treasury’s recent analysis of longitudinal business data, it is clear that average real wages are higher for businesses with higher labour productivity.

Both capital deepening and multifactor productivity will be important to support further growth in labour productivity – so business investment is critical to our economic prosperity.

Recent trends

Over the past decade, Australia’s experience with business investment has played out in two starkly different stages.

Chart 1 – This chart shows the unprecedented investment boom to build new supply capacity in the mining sector in response to strong demand for resources and higher commodity prices.

Such was the strength of the mining boom that total business investment increased as a per cent of GDP noticeably over this period.

This was one important factor in our economy’s resilience through the GFC, supporting jobs in a whole range of industries and seeing benefits flow on to wages and capital returns throughout the economy.

Of course, it is hard to know precisely why our economy fared so well during the GFC.

The flexibility of the economy, prudent monetary policy and a sound financial system – as well as demand from China – all played their part but it is difficult to single out any individual factor.

While mining investment declined for a time during the GFC, the demand for our resources was such that mining investment increased through to its peak in 2012-13, helping to counteract the global tide of recession through that period.

Since then, mining investment has rapidly receded.

Crucially, business investment outside of the mining sector did not take up the slack as the trend in mining investment reversed.

The share of non-mining business investment as a per cent of GDP began to fall following the GFC, and in recent years has fallen to around its lowest share of GDP in the past 50 years.

In 2016‑17, non-mining business investment was around 9 per cent of GDP.

As is clear from the chart, this is between 2 and 2 ½ percentage points of GDP below the long run average prior to the GFC – so there remains a gap that we would hope non-mining investment could fill.

In an environment of low interest rates and generally positive economic developments the extent of the weakness in non-mining investment was somewhat perplexing.

Australia has not been alone in facing this challenge.

In meetings with my counterparts from the New Zealand, Canada, UK and Ireland Treasuries over recent years weak business investment has been one of the key concerns discussed.

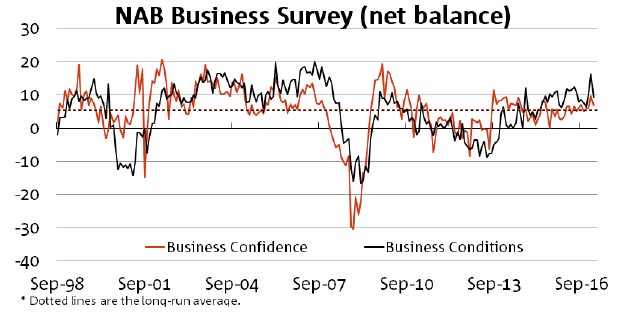

The February NAB Business Survey gave back the surprisingly strong gains seen in the previous month. But the overall results are still quite positive, and not uniform across the states.

Some payback was flagged in last month’s Survey as temporary factors were thought to have been behind much of the spike in both business conditions and confidence. However, despite the pull-back, both of these indicators remain at levels consistent with solid business activity in the near-term, and are higher than through much of H2 2016.

The business conditions index dropped by 7 points in February, more than unwinding the 6 point jump in January, to be at +9 index points – still above the series long-run average. The fall in business conditions was reflected across all three components of the index (trading conditions/sales, profitability and employment), although the bulk of the deterioration seems to have come from sales, which is now noticeably weaker than it was back in December. Profitability did not spike with the other components in January and saw only a small moderation. Employment also weakened slightly, but is still well up on December levels – an strong outcome and indicative of a strengthening underlying trend (which has been more encouraging than ABS labour market statistics). By industry, we remain concerned about retail conditions, but all other industries (including mining) recorded positive business conditions in February. Additionally, conditions are looking good across most states, with WA the main exception. Cost price measures in the Survey were mixed, although labour costs held up and retail prices accelerated (but are still relatively soft).

NAB’s Business confidence index dropped back a little as well in the month, but is still suggesting that business sentiment remains relatively upbeat – consistent with the overall tone seen in financial markets. The business confidence index fell 3 points to +7 index points in February, which is slightly above the series long-run average. Other indicators were reasonably solid as well, with capacity utilisation rates holding up, consistent with a solid (albeit easing) read on capital expenditure. Forward orders, however, continue to look relatively muted.

A drop in activity indicators had been anticipated for the February NAB Monthly Business Survey, meaning these results do not fundamentally change NAB’s outlook for the economy. Indeed, business conditions are still at quite lofty levels, consistent with our expectation for the economy to enjoy solid rates of growth in the near-term. There are, however, still some points of concern such as the persistent weakness evident in retail conditions, which warrant close monitoring. Additionally, it is the longer-term growth picture that is more concerning, particularly as the contribution from LNG exports, temporarily higher commodity prices and the residential construction boom fade, putting pressure on the labour market. However, the RBA is increasingly putting emphasis on financial stability concerns, which is likely to impact the response of monetary policy.

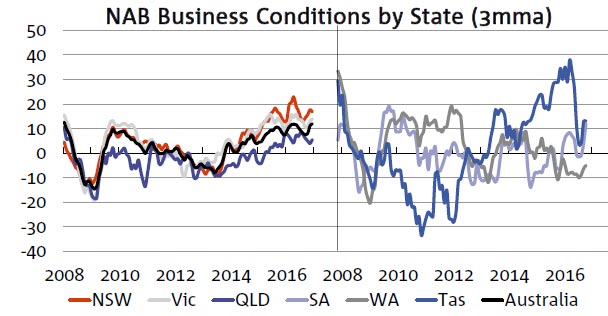

By state, outcomes were quite mixed in this month’s Survey, although most states are generally looking quite solid. NSW and WA saw the largest falls in business conditions, down 6 and 9 points respectively, although conditions in NSW still look quite good at +14 index points. WA on the other hand was very weak at -11 index points, the only state to be negative, despite positive conditions reported nationally in the mining industry. In contrast, SA saw a very large increase in conditions during the month. Looking through the monthly volatility, NSW maintains the highest conditions in trend terms (+17), followed by Victoria (+14). Meanwhile, WA is weakest (-5), followed by Qld (+5). In terms of confidence, Queensland is best in trend terms (see p8 for details).

According to the latest NAB Business Survey for January 2017, both business conditions and confidence jumping to much higher levels.

The strength witnessed in last month’s NAB Monthly Business Survey continued into January, with both business conditions and confidence jumping to much higher levels. While these outcomes are certainly pointing to an improvement in the domestic economy after a soft patch through much of H2 2016, a degree of caution should still be exercised given the diverse and rapidly changing seasonal influences at this time of year (which potentially includes the shift in Chinese New Year to January this year).

In terms of the headline numbers, the business conditions index jumped by a solid 6 points in January, to +16 index points, which is around pre-GFC boom levels. This month, another rise in trading conditions contributed to the outcome, but there was also a noticeable jump in employment conditions, which bodes well for the generally underperforming labour market – the employment index hit its highest level since 2011.

Meanwhile, profits were unchanged at solid levels. By industry, last month’s surprise spike in wholesale conditions was unwound (as anticipated), but that seems to have been more than offset at the aggregate level by improvements in personal services, while retail and mining are no longer negative. NSW enjoyed the bulk of the improvement in conditions, while the rest of the mainland states were relatively steady. Cost price measures in the Survey also lifted notably, suggesting a build in wage pressures, although retail price inflation remained very subdued.

Business confidence also jumped in the month, aligning itself with the general enthusiasm seen in financial markets and more positive sentiment towards the global economic outlook. The business confidence index jumped 4 points to +10 index points in January, which was well above the series long-run average. Responses on capital expenditure were also much more encouraging in January, consistent with a rise in capacity utilisation – although forward orders do not point to a continuation of that strength in the near-term.

Recent strength in the NAB Business Survey is consistent with an anticipated rebound in economic activity, following the very weak Q3 2016 National Accounts. With that said, a confluence of seasonal factors suggests it is unwise to get too carried away with the result just yet, especially as key industries like retail remain extremely weak (despite improving in the month), which suggests the outlook for consumption remains cloudy. NAB Economics also have concerns for the longer-term growth picture, as the contribution from LNG exports, temporarily higher commodity prices and the residential construction boom fade, keeping pressure on the labour market.

Nevertheless, in light of the recent flow of data, NAB’s economic forecasts (which include expectations for the RBA’s cash rate) are currently under review – to be published tomorrow.

The December NAB Monthly Business Survey indicated a reprieve from the steady moderation in business conditions seen late last year.

That outcome points to a stronger outlook for the economy, but we remain cautious given other aspects of the Survey that suggest the rebound might prove to be temporary. Weakness in retail conditions is particularly concerning, while we are not seeing any real signs in the Survey of a convincing recovery in non-mining investment – crucial to both near-term and longer-term growth prospects (although the drag from the mining sector should soon ease). While some ‘bounce-back’ from the weather affected Q3 GDP can be expected, a return to a more subdued growth track thereafter still seems likely as the positive effects from the housing construction cycle, commodity exports, and (temporarily) higher commodity prices washes out.

Business conditions saw an impressive rebound this month, largely unwinding the steady downward trend seen since mid-2016. The business conditions index (an average of trading conditions (sales), profitability and employment) jumped 5 points, to +11 index points, which is well above the long-run average for the series (+5). Meanwhile, business confidence has been quite steady over the past year, and December was no different. The confidence index was unchanged at +6 index points, consistent with the long run average.

According to Mr Alan Oster, NAB’s Chief Economist, “the rebound in business conditions is certainly encouraging, but at this stage we are not getting too carried away with the result. Stronger business conditions in December largely reflected unexpectedly strong improvements in some industries, which might not be sustained, while other indicators were generally mixed as well. As for business confidence, the stability we have seen for some time now has been welcome, but it does not fully reflect the strength in business conditions. That might suggest that business still has a high degree of concern about global uncertainties in particular”.

By industry, the improvement in business conditions in December was most pronounced in wholesale and transport & utilities, while manufacturing and retail recorded deterioration. “We were a little surprised by the strength in wholesale, particularly given much more subdued conditions in related industries such as manufacturing and retail. Retail is now the weakest industry in the Survey, which is concerning given the importance of household consumption to the outlook”, said My Oster. Looking through monthly volatility, service industries remain the best performers.

Within business conditions, the jump was completely driven by higher trading conditions and profitability, while the employment index was unchanged at relatively subdued levels.

According to Mr Oster, “employment conditions have remained stubbornly muted and suggest the labour market is still not generating enough jobs to bring the unemployment rate down from its elevated level. That said, the employment index does point to slightly stronger employment growth than we have been seeing from the ABS Labour Force Survey of late”.

The near-term outlook improved marginally in this month’s Survey, with the forward orders index jumping above its long-run average level. However, the capacity utilisation rate, which is relevant to future employment and capital expenditure, eased back. According to Mr Oster, “the outcome for forward orders suggests good near-term prospects for activity, but the drop in capacity utilisation warrants monitoring, especially if it points to a continuation of the downward trend seen over the second half of 2016”.

“The headline results from the Survey indicate some upside risk to the outlook, but the mixed results below the surface suggest a degree of caution is warranted. Importantly, we are not seeing any real signs of a convincing recovery in non-mining investment in the Survey, which is crucial to both near-term and longer-term growth prospects” said Mr Oster. While some ‘bounce-back’ from the weather affected Q3 GDP can be expected, a return to a more subdued growth track thereafter still seems likely as the positive effects from the housing construction cycle, commodity exports, and (temporarily) higher commodity prices wash out.

Two more 25bp rate cuts are still expected from the RBA this year in response to ongoing low inflation and a more subdued growth outlook. NAB Economics will be issuing an update on the economic outlook in coming weeks.