Westpac New Zealand Limited (Westpac) has retained its

accreditation as an internal models bank following completion of an extensive

remediation process required by the Reserve Bank.

In 2017 the Reserve Bank

required Westpac to undertake an independent review of its compliance with

internal models obligations. The review found that Westpac was using a number

of unapproved models and that it had materially failed to meet requirements around

model governance, processes, and documentation.

The Reserve Bank imposed a

precautionary capital overlay in light of the regulatory breaches, and gave

Westpac 18 months to remedy the failures or risk losing its accreditation as an

internal models bank.

Deputy Governor Geoff

Bascand says that following the remediation process, Westpac is now operating

with peer-leading processes, capabilities and risk models in a number of areas.

“Westpac has taken the

findings of the independent review as an opportunity to make meaningful

improvements to its risk management, and we commend it for its co-operative and

constructive engagement in working with Reserve Bank over the remediation

period.

“The changes that Westpac

has made to its internal processes, governance and resourcing, as well as a

suite of new credit risk models for which it has sought approval, have given us

confidence in its capital modelling and compliance and satisfied us that it now

meets the internal models bank standard.

“Looking forward, we will continue

to hold all internal model banks to the same high standards.”

Internal models banks are

accredited by the Reserve Bank to use approved models to calculate their

regulatory capital requirements. Accreditation is earned through maintaining

high risk management standards, and comes with stringent responsibilities for

the bank’s directors and management.

Banks are required to

maintain a minimum amount of capital, which is determined relative to the risk

of each bank’s business. The way that risk is measured is important for

ensuring that each bank has an appropriate level of capital to absorb large and

unexpected losses.

The Reserve Bank will amend

Westpac’s conditions of registration from 31 December to remove the two

percentage point overlay applying to its minimum capital requirements.

As a condition of retaining

its accreditation Westpac will need to satisfy several ongoing requirements,

which it has committed to resolving, Mr Bascand says.

APRA is proposing to adjust its capital requirements for authorised deposit-taking institutions (ADIs) to support the Government’s First Home Loan Deposit Scheme (FHLDS). The scheme aims to improve home ownership by first home buyers, through a Government guarantee of eligible mortgage loans for up to 15 per cent of the property purchase price.

Recognising that the Government guarantee is a valuable form of credit risk mitigation, APRA is proposing to reflect this in the capital framework by applying a lower capital requirement to eligible FHLDS loans.

APRA intends to give effect to this lower capital requirement by adjusting the mortgage capital requirements set out in Prudential Standard APS 112 Capital Adequacy: Standardised Approach to Credit Risk (APS 112).

Specifically, recognising both the minimum 5 per cent deposit required of borrowers and the Government guarantee of 15 per cent of the property purchase price, APRA proposes to allow ADIs to treat eligible FHLDS loans in a comparable manner to mortgages with a loan-to-valuation ratio of 80 per cent.

This would allow eligible FHLDS loans to be risk-weighted at 35 per cent under APRA’s current capital requirements. Once the Government guarantee ceases to apply to eligible loans, (this could be because the borrower pays down the loan to below 80 per cent of the property purchase price, refinances or uses the property for a purpose that is not within the scope of the guarantee.) ADIs would revert to applying the relevant risk weights as set out in APS 112.

APRA invites feedback on this proposal, which will be subject to a

two-week public consultation. APRA intends to release its response,

including additional information on implementation for participating

ADIs, as soon as practicable after the consultation period.

Written submissions on the proposal should be sent to ADIpolicy@apra.gov.au by 11 November 2019

The Australian Prudential Regulation Authority (APRA) has released its response to submissions on proposed changes to the application of the capital adequacy framework designed to support the orderly resolution of a failing authorised deposit-taking institution (ADI).

APRA released a discussion paper in November last year proposing that the four major Australian banks be required to increase their Total Capital by four to five percentage points of risk weighted assets (RWA) over four years. APRA expected the banks would meet the bulk of this requirement by raising additional Tier 2 capital. For small to medium ADIs, extra loss-absorbing capacity would be considered on a case-by-case basis as part of the resolution planning process.

The changes would increase the financial resources available for APRA to safely resolve an ADI, and minimise the need for taxpayer support, in the unlikely event of failure. They also fulfil a recommendation from the 2014 Financial System Inquiry that APRA implement a framework for minimum loss-absorbing and recapitalisation capacity.

Following extensive engagement with a range of stakeholders, APRA has announced an approach that will meaningfully lift the loss-absorbing capacity of the four major banks.

APRA will require the major banks to lift Total Capital by three percentage points of RWA by 1 January 2024. APRA’s overall long term target of an additional four to five percentage points of loss absorbing capacity remains unchanged. Over the next four years, APRA will consider the most feasible alternative method of sourcing the remaining one to two percentage points, taking into account the particular characteristics of the Australian financial system.

APRA amended its initial proposal in response to concerns raised in a number of submissions about a lack of sufficient market capacity to absorb an extra four to five per cent of RWA in Tier 2 issuance and the potential to excessively increase bank funding costs. A number of respondents provided useful market capacity analysis in their submissions. APRA also had extensive dialogue with ADIs, arrangers of Tier 2 issuance in global markets, and significant investors in Tier 2 instruments. Following this consultation process, APRA expects the issuance of an additional three percent of RWA in Tier 2 instruments can be achieved in an orderly manner, and be maintained through varied markets conditions.

APRA Deputy Chair John Lonsdale said the measures were an important step in minimising the risks to depositors and taxpayers should Australia experience a future bank failure.

“The global financial crisis highlighted examples overseas where taxpayers had to bail out large banks due to a lack of residual financial capacity. Boosting loss-absorbing capacity enhances the safety of the financial system by increasing the financial resources that an ADI holds for the purpose of orderly resolution and the stabilisation of critical functions in the unlikely event that it fails.

“Although APRA’s proposed response may increase funding costs for Tier 2 instruments issued by major banks, overall funding cost increases can be expected to remain small. Having taken into account feedback on market capacity, increasing Total Capital requirements by three percentage points by 2024 (instead of the four to five originally proposed) will be easier for the market to absorb and reduce the risk of unintended market consequences.

“By lifting their Total Capital by three percentage points of risk-weighted assets, we estimate the major banks will cumulatively strengthen their loss-absorbing capacity by $50 billion. APRA looked closely at alternative approaches used in other jurisdictions but concluded that increasing the issuance of existing capital instruments was more appropriate taking into account the distinctive characteristics of the Australian financial system,” Mr Lonsdale said.

APRA estimates the increase in Total Capital requirements will have a small impact on overall funding costs – less than five basis points – an estimate well within the range of analysis conducted by the Reserve Bank of Australia using historical market data

The New Zealand Central Bank is steering a path quite different from the RBA with a move to lift bank capital to much higher levels, in the interests of protecting households and businesses in New Zealand.

The costs, they say, are worth the benefits! Indeed the recent IMF report on NZ endorsed their approach.

Australian Banks operating in New Zealand are resisting according to the AFR – “Australia’s banks would have to raise at least $NZ20 billion ($19.1 billion) to satisfy New Zealand capital requirements, leading the big four to threaten a rethink of their business models if the proposals get the green light”.

But of course banks in Australia need higher capital buffers despite what the local regulators may say. NZ is on the better path.

As part of this journey, the New Zealand Reserve Bank released submissions along with a Summary of Submissions (PDF 399 KB) on the latest consultation paper in its Capital Review, which proposes several measures to ensure a safer banking system for New Zealanders.

There was significant and wide-ranging media and public interest in the How much capital is enough? (PDF 545 KB)paper, with written feedback from 161 submitters. Feedback has also been received from analysts and other interested parties who did not make a formal submission.

“The Reserve Bank welcomes the large number of submissions on this consultation, as well as the effort and consideration that has gone into them,” Deputy Governor Geoff Bascand says. “We believe this shows how important this issue is for everyone, and we are pleased that a broader set of stakeholders has taken an interest in the Capital Review.”

In general, submitters support the Reserve Bank’s objective to ensure that New Zealand’s financial system is safe, acknowledging the economic and well-being impacts of banking crises. Many submitters, particularly from the general public, support the proposed higher capital requirements for banks. A number of submitters observe that higher capital requirements could lead to higher borrowing costs for New Zealanders. Some submitters, in particular banks and business groups, question whether the proposed increases are too large and too costly.

Central to the measures proposed in the consultation paper are increases in regulatory capital buffers for locally incorporated banks. The changes include requiring bank shareholders to increase their stake so that they absorb a greater share of losses should their bank fail, improving the quality of capital, and ensuring banks more accurately measure their risk.

Increasing the amount and quality of capital can be reasonably expected to mean that banks can survive all but the most exceptional shocks, Mr Bascand says. “We think the costs of doing so are outweighed by the benefits – someone’s cost is for society’s broader benefit.”

The Reserve Bank is also consulting on changes to the quality of capital, constraints on modelling capital requirements, and the implementation timeline.

It is continuing its stakeholder outreach programme, which includes conducting focus groups to understand the public’s risk appetite, and engagement with iwi, social sector and industry groups, financial institutions and investors. It has also engaged three external experts for an independent review of its proposals.

“The submissions on the proposals are just one part of the review,” Mr Bascand says. “All these inputs will help us to make robust and well-calibrated policies and decisions that best represent society’s interests.”

In this context, Mr Bascand welcomed reports by two key international financial institutions and a major rating agency last week that support the proposals to increase bank capital ratios.

Following its recent mission to New Zealand, the International Monetary Fund has released a Concluding Statement that highlights the need for strengthening bank capital levels and that the proposals appear commensurate with the systemic financial risks facing New Zealand. The Organisation for Economic Co-operation and Development’s latest Economic Survey of New Zealand expects increases in capital will likely have net benefits for New Zealand. And Standard and Poor’s says that the proposals should not have material impacts on overall credit availability.

The Capital Review began more than two years ago, when the Reserve Bank published an issues paper and opened the first of four public consultations. It will publish its response to the submissions alongside final decisions, expected in November 2019.

Implementation of any new rules will start from April next year. There will be a transition period of a number of years before banks are required to meet the new requirements

The Australian Prudential Regulation Authority (APRA) has released its response to the first round of consultation on proposed changes to the capital framework for authorised deposit-taking institutions (ADIs).

The package of proposed changes, first released in February last year, flows from the finalised Basel III reforms, as well as the Financial System Inquiry recommendation for the capital ratios of Australian ADIs to be ’unquestionably strong’.

ADIs that already meet the ‘unquestionably strong’ capital targets that APRA announced in July 2017 should not need to raise additional capital to meet these new measures. Rather, the measures aim to reinforce the safety and stability of the ADI sector by better aligning capital requirements with underlying risk, especially with regards to residential mortgage lending.

APRA received 18 industry submissions to the proposed revisions, and today released a Response Paper, as well as drafts of three updated prudential standards: APS 112 Capital Adequacy: Standardised Approach to Credit Risk; the residential mortgages extract of APS 113 Capital Adequacy: Internal Ratings-based Approach to Credit Risk; and APS 115 Capital Adequacy: Standardised Measurement Approach to Operational Risk.

The Response Paper details revised capital requirements for residential mortgages, credit risk and operational risk requirements under the standardised approaches, as well as a simplified capital framework for small, less complex ADIs. Other measures proposed in the February 2018 Discussion Paper, as well as improvements to the transparency, comparability and flexibility of the ADI capital framework, will be consulted on in a subsequent response paper due to be released in the second half of 2019.

After taking into account both industry feedback and the findings of a quantitative impact study, APRA is proposing to revise some of its initial proposals, including:

for residential mortgages, some narrowing in the capital difference that applies to lower risk owner-occupied, principal-and-interest mortgages and all other mortgages;

more granular risk weight buckets and the recognition of additional types of collateral for SME lending, as recommended by the Productivity Commission in its report on Competition in the Financial System; and

lower risk weights for credit cards and personal loans secured by vehicles.

The latest proposals do not, at this stage, make

any change to the Level 1 risk weight for ADIs’ equity investments in

subsidiary ADIs. This issue has been raised by stakeholders in response to

proposed changes to the capital adequacy framework in New Zealand. APRA has

been actively engaging with the Reserve Bank of New Zealand on this issue, and

any change to the current approach will be consulted on as part of APRA’s

review of Prudential Standard

APS 111 Capital Adequacy: Measurement of Capital later this year.

APRA’s consultation on the revisions to the ADI capital framework is a

multi-year project. APRA expects to conduct one further round of consultation

on the draft prudential standards for credit risk prior to their finalisation.

It is intended that they will come into effect from 1 January 2022, in line

with the Basel Committee on Banking Supervision’s internationally agreed

implementation date. An exception is the operational risk capital proposals for

ADIs that currently use advanced models: APRA is proposing these new

requirements be implemented from the earlier date of 1 January 2021.

APRA Chair Wayne Byres said: “In setting out these latest proposals, APRA has

sought to balance its primary objectives of implementing the Basel III

reforms and ‘unquestionably strong’ capital ratios with a range of important

secondary objectives. These objectives include targeting the structural

concentration in residential mortgages in the Australian banking system, and

ensuring an appropriate competitive outcome between different approaches to

measuring capital adequacy.

“With regard to the impact of risk weights on competition in the mortgage

market, APRA has previously made changes that mean any differential in overall

capital requirements is already fairly minimal. APRA does not intend that the

changes in this package of proposals should materially change that calibration,

and will use the consultation process and quantitative impact study to ensure

that is achieved.

“It is also important to note that the proposals announced today will not

require ADIs to hold any capital additional beyond the targets already

announced in relation to the unquestionably strong benchmarks, nor do we expect

to see any material impact on the availability of credit for borrowers,” Mr

Byres said

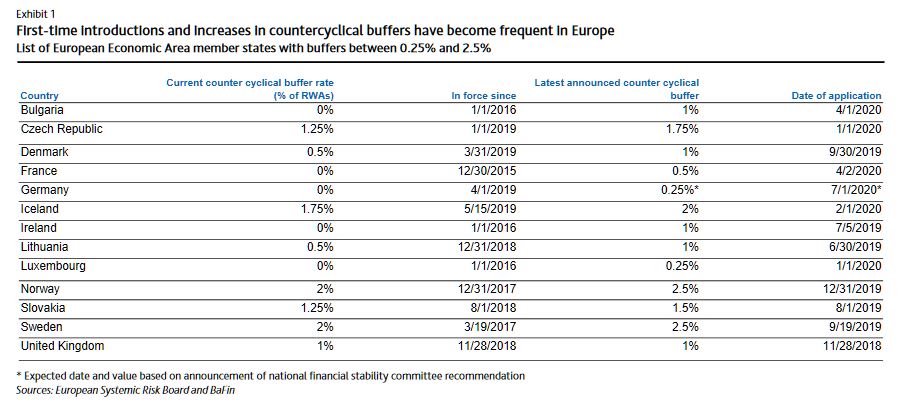

On 27 May, Germany’s bank supervisor Bundesamt für Finanzdienstleistungsaufsicht (BaFin) published a recommendation of the national financial stability committee that would require banks to hold an additional 0.25% capital cushion against their domestic riskweighted assets (RWAs). At the same time, BaFin indicated its intention to follow this recommendation, which would become binding after a 12-month transition period on 1 July 2020. Via Moody’s.

The announcement is credit positive for German banks because it will encourage those with tighter capital cushions to set aside additional funds for risks that could surface in the case of changes to the current macroeconomic environment, foremost those related to a potential underestimation of future credit risks in a cyclical downturn, risks to collateral values in residential mortgage lending or risks related to the future interest rates trajectory.

Germany is the 13th country in the European Economic Area to introduce a countercyclical capital buffer, and in most fellow member states the first step introduction has been followed by at least one increase later. Exhibit 1 provides an overview of initial and current countercyclical buffer (CCyB) requirements.

Germany’s 0.25% proposal will apply to German exposures of all European Economic Area banks and it remains very close to the bottom of the range compared with Norway and Sweden, whose CCyBs will reach the maximum of 2.5% later this year. Even so, we believe BaFin’s moderate first step and its ability to increase the requirement will lead German banks to further strengthen their capital buffers and it clearly signals BaFin’s aim to maintain the pace of systemwide RWA growth at a sound level. RWA growth, as a result of increased lending in combination with tighter RWA measurement rules, outpaced capital retention of Germany’s largest institutions during 2018 according to the supervisor, leading to declines in capital ratios.

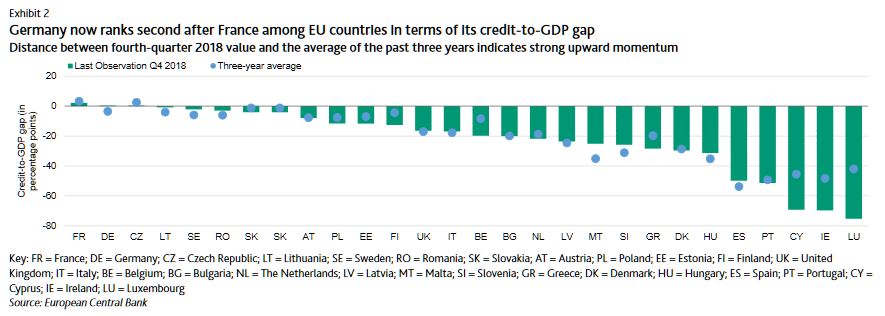

In setting the level of the CCyB, regulators are exercising their judgment while taking into account a range of factors including any deviation of the credit-to-GDP ratio from its long-term trend, asset price levels, business lending conditions, and any increase in the stock of nonperforming loans. While below the formulaic +2% threshold that would flag a potential need for raising the CCyB, exhibit 2 shows the German credit-to-GDP gap has been closing to a large extent in recent quarters.

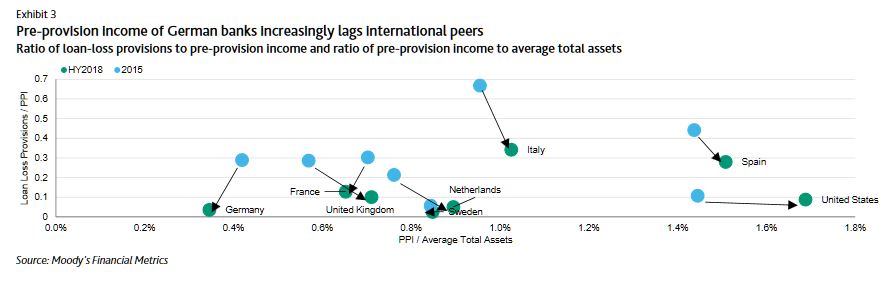

The German announcement echoes a recent recommendation by the International Monetary Fund, which had laid out a similar reasoning in the preliminary view of its annual Article IV mission which assesses the economic and financial development in the Germany. Regarding asset and profitability risks observed by the financial stability committee, we share the view that the German banking system’s current profitability is vulnerable once loan-loss provisioning needs normalise upwards, since the system’s preprovision income levels have further lost ground against international peers

While the sector’s continued prudence in new residential mortgage origination benefits banks, the financing of the banking sector’s long-term fixed-rate assets through current-account deposits results in asset-liability mismatch risks that we expect will at least in part become visible once interest rates rise and if they do so at a faster pace than the banks expected.

The

Reserve Bank has revoked ANZ Bank New Zealand Limited’s (ANZ) accreditation to

model its own operational risk capital requirement due to a persistent failure

in its controls and attestation process.

ANZ

is now required to use the standardised approach for calculating appropriate

operational risk capital. From March 2019, this will increase its minimum

capital held for operational risk by around 60%, to $760 million.

The

Reserve Bank requires banks to maintain a minimum amount of capital, which is

determined relative to the risk of each bank’s business. The way that risk is

measured is important for ensuring that each bank has an appropriate level of

capital to absorb large and unexpected losses.

“Accreditation

is earned through maintaining high risk management standards, and comes with

stringent responsibilities for the bank’s directors and management,” says

Deputy Governor Geoff Bascand.

“The

Reserve Bank’s role is to review and approve internal models. The onus is then

on bank directors to ensure, and attest, that their bank is compliant with the

Reserve Bank’s regulatory requirements. To do that, bank directors need to be

satisfied that the internal assurance processes that sit behind the

attestations are being adhered to.

“ANZ’s

directors have attested to compliance despite the approved model not being used

since 2014. The fact that this issue was not identified for so long highlights

a persistent weakness with ANZ’s assurance process.”

The

Reserve Bank had encouraged ANZ to undertake a full review of its attestation

process, and assess its compliance with capital regulations, Mr Bascand

says. ANZ’s failure to use an approved model was revealed through that

review.

“A

bank’s disclosure statement is required to contain certain statements signed by

each director of the bank. These must state, among other things: whether the

bank has systems in place to monitor and control adequately the banking group’s

material risks and whether those systems are being properly applied; and

whether the bank has complied with its conditions of registration over the period

covered by the disclosure statement.

“These

directors’ attestations are important because they strengthen the incentives

for directors to oversee, and take ultimate responsibility for, the sound

management of their bank.

“We

continue to work with ANZ in assessing its systems controls before determining

any further action.”

ANZ

is one of four big banks in New Zealand that are accredited by the Reserve Bank

to use their own risk models – the internal models approach – in calculating

their regulatory capital requirements.

The

Reserve Bank is currently consulting on its capital framework for banks. Among

the many decisions to be made, and in part due to proven weaknesses with the

internal models approach, it is proposing that all banks adopt a new

standardised approach for calculating operational risk capital.

Note to editors:

Attestation

regime

A

bank’s disclosure statement is required to contain certain statements signed by

each director of the bank. These must state, among other things: whether the

bank has systems in place to monitor and control adequately the banking group’s

material risks and whether those systems are being properly applied; and

whether the bank has complied with its conditions of registration over the

period covered by the disclosure statement.

These

directors’ attestations are important because they strengthen the incentives

for directors to oversee, and take ultimate responsibility for, the sound

management of their bank.

What are

capital requirements?

Bank

capital is a source of funding that banks use that stand first in line to

absorb financial losses they might make. The Reserve Bank, like other

regulators around the world, sets the minimum level of capital a bank must use

to fund its operations. The more capital a bank has, the less likely it is to

fail.

There

are three broad types of risks that banks are required to have capital for:

Credit risk – the risk that

borrowers will be unable to pay back their loans

Market risk – the risk that

a change in market conditions, such as changes in the exchange rate, will cause

losses for banks

Operational risk – other risks

that relate largely to the systems of a bank, such as a computer systems

failure

What is

internal modelling?

Locally

incorporated banks in New Zealand can calculate their capital requirements in

two ways: the internal models approach or the standardised approach.

Under

the internal models approach a bank is able to use statistical models to assess

the riskiness of its business such as the risk of its mortgage loans, or its

level of operational risk. The bank’s internal models need to be approved by

the Reserve Bank to ensure they are conservatively designed. Banks also need to

meet several qualitative criteria to use this approach, such as proper

governance and validation of these internal models. The banks in New Zealand

that are accredited to use the internal models approach are ANZ, ASB, BNZ, and

Westpac.

Under

the standardised approach, the amount of capital that is required is prescribed

in a set of formulae by the Reserve Bank. This approach is simpler for

banks to use than the internal models approach and easier to implement.

What is an

operational risk model?

Operational risk capital requirements are designed to

provide banks with sufficient capacity to absorb a wide range and magnitude of

operational risk-related losses (from, for example: inadequate or failed

internal processes, people or systems; or from external events, including legal

risks). Underestimation of the amount of operational risk capital that a bank

needs can undermine a bank’s financial soundness and could make it more likely

to fail.

What is the

Capital Review?

The Capital Review is a review of the capital

requirements that the Reserve Bank sets for locally incorporated banks. It

seeks to address several questions about New Zealand’s current framework: What

should New Zealand’s risk tolerance be for banking crises? Do banks have sufficient

levels of capital? What should the quality of capital be in New Zealand? Should

we allow internal modelling for capital requirements? Should there be a

significant difference between internal modelling and standardised approaches?

As part of its current Capital Review, the Reserve

Bank is reviewing its capital framework for banks. Due in part to proven

weaknesses with the internal models approach and in line with moves by other

supervisor banks around the world, the review proposes that all banks adopt a

new standardised approach for calculating operational risk capital.

The Australian Prudential Regulation Authority (APRA) has proposed updating its prudential standard on credit risk management requirements for authorised deposit-taking institutions (ADIs).

Credit risk refers to the possibility that a borrower will fail to meet their obligations to repay a loan, and is usually considered the single largest risk facing an ADI.

APRA has released a discussion paper proposing changes to Prudential Standard APS 220 Credit Quality (APS 220), which requires ADIs to control credit risk by adopting prudent credit risk management policies and procedures.

APS 220 was last substantially updated in 2006, and there has been significant evolution in credit risk practices since then, including more sophisticated analytical techniques and information systems. APRA’s plan to modernise the standard was prompted by its recent supervisory focus on credit standards, and also reflects contemporary credit risk management practices.

The discussion paper outlines APRA’s proposals in the following areas:

Credit risk management – The

revised APS 220 broadens its coverage to include credit standards and the

ongoing monitoring and management of an ADI’s credit portfolio in more

detail. It also incorporates enhanced Board oversight of credit risk and

the need for ADIs to maintain prudent credit risk practices over the

entire credit life-cycle.

Credit standards – The revised

APS 220 incorporate outcomes from APRA’s recent supervisory focus on

credit standards and also addresses recommendation 1.12 from the Final

Report of the Royal Commission in relation to the valuation of land taken

as collateral by ADIs.

Asset classification and

provisioning – The revised APS 220 provides a more consistent

classification of credit exposures, by aligning recent accounting standard

changes on loan provisioning requirements, as well as other guidance on

credit related matters of the Basel Committee on Banking Supervision.

To better describe the

purpose of the revised standard, APRA also proposes renaming it Prudential Standard APS 220 Credit Risk

Management.

The proposed reforms are due to be implemented from 1 July 2020, while an

accompanying prudential practice guide (PPG) and revised reporting standards

will be released for consultation later this year.

In a related development, APRA has also released a letter to industry

expressing concerns related to ADIs’ increasing exposure to funding agreements

with third party lenders, including peer to peer (P2P) lenders.

Blog")