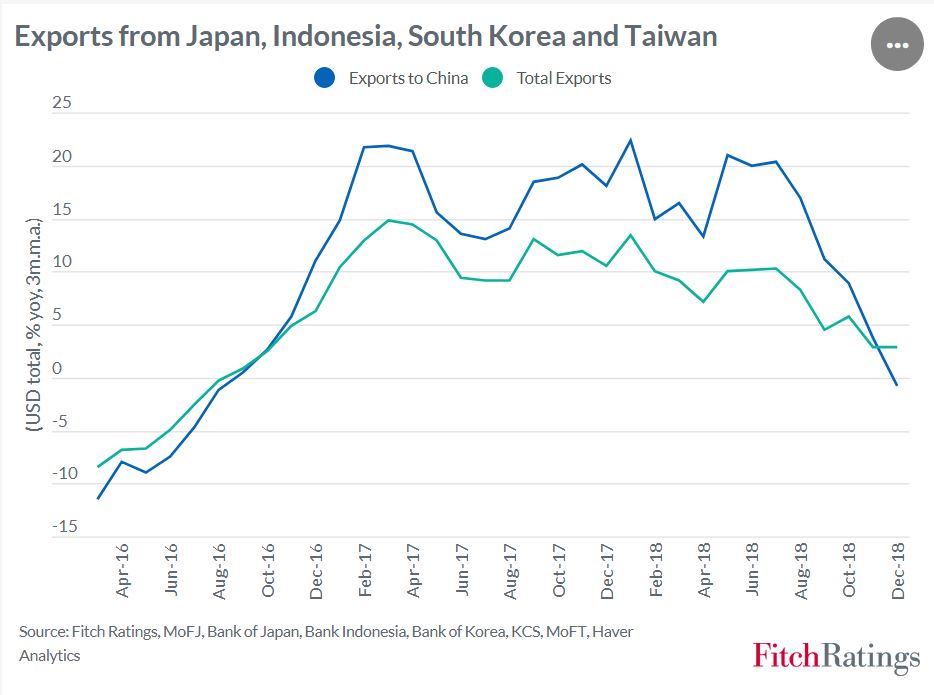

Fitch Ratings says the recent pattern of trade flows in Asia suggests that the sharp decline in world trade growth in the second half of 2018 was primarily due to the slowdown in domestic demand in China rather than the direct impact of tariffs associated with increased US-China trade tensions.

Fitch Ratings latest chart of the month shows that exports to China from a selection of other large economies in Asia have slowed much more sharply than their overall exports. Since intra-Asian trade flows are much less likely to have been affected by the tariff measures imposed by the US and China, this points to weakening domestic demand in China as a key driver of the slowdown. China’s year-on-year import growth (in nominal US dollar terms) turned negative at the end of 2018, despite rising import prices. This was the first decline since 2016 and reflects a slowdown in domestic investment and private consumption.

The US and the Eurozone have also seen their export growth to China

falling more rapidly than total exports. Germany in particular has been

hit hard by declining auto sales in China, although, for the Eurozone as

a whole, exports have also been affected by declining sales in the UK

and Turkey. US exports to China have fallen very sharply in recent

months but these bilateral flows have been distorted by tariff measures,

including possible front-loading of trade flows in mid-2018 ahead of

anticipated further tariff hikes and the subsequent payback. The

evidence from Asia suggests the outlook for Chinese domestic demand will

be a key driver of global trade in 2019.

Three defaults in recent months have highlighted the risk of broader disclosure and governance problems among Chinese corporates, as well as the variable quality of local auditing, says Fitch Ratings. Shandong SNTON Group Co. (Snton, RD), Reward Science and Technology Industry Group Co. (Reward, RD) and Kangde Xin Composite Material Group Co. (KDX, WD) all defaulted on moderate amounts relative to their reported cash holdings.

Corporate defaults are usually driven by insufficient

liquidity, but these companies’ stated cash balances cannot explain the

non-payments. Snton was sued by the Hebei Bank Qingdao Branch on 25

September for CNY139 million, which included defaulted principal of two

drawn facilities. It had a reported cash balance of CNY4 billion at

end-June, of which we estimate roughly half was unrestricted, which

should have provided a significant buffer against default. It was also

able to raise CNY400 million through domestic bond issuance in 1H18,

suggesting normal access to the domestic funding market, despite

generally tight credit conditions.

Reward failed to repay CNY300

million of commercial paper on 6 December, despite having CNY4.9 billion

in cash – just CNY548 million of which was restricted – at end-June

2018, and CNY4.2 billion at end-September, according to its management

accounts. KDX failed to repay CNY1 billion of commercial paper on 15

January. It had reported available cash of CNY15 billion and a net cash

position in September.

These companies did not show other

typical signs of distress prior to the defaults. The rise in Snton’s

leverage in 2017 was above Fitch’s expectations and drove our downgrade

of the company’s rating in May 2018, but its FFO net leverage of around

3.5x at end-June 2018 did not indicate an unsustainable capital

structure. Reward’s FFO interest coverage was over 3.5x in 9M18, while

KDX was around 5x in 1H18.

The defaults call into question the

actual availability and amounts of reported cash balances. The three

companies reported their restricted cash balances in line with Chinese

accounting standards – China GAAP – which mandate similar disclosures on

cash encumbrances to international standards. It is unclear if there

were less formal restrictions in place, such as agreements with lending

institutions to keep sums in designated accounts to support facility

access. In any case, Reward and KDX confirmed to Fitch shortly before

their commercial paper due dates that their holdings of realisable cash

were sufficient to meet obligations.

Uncertainty over the

accuracy of the companies’ books and disclosure of pertinent information

is ultimately related to governance and accounting quality. Governance

issues – often challenging to uncover – have been a factor in Fitch’s

ratings on Reward and KDX. Reward’s ratings have been constrained by its

low transparency as a private unlisted company with concentrated share

ownership. The company changed auditor and re-issued its 2017 accounts

due to disclosure and accounting problems flagged by the regulator.

KDX

is listed on the Shenzhen Stock Exchange (SSE), but an apparent problem

with its disclosure of concerted party arrangements at shareholder

level prompted an SSE investigation, which hampered access to funding

and prompted our downgrade in December. Snton’s case demonstrates

unpredictable financial management. It failed to repay domestic bank

loans, but has continued to service onshore bonds.

All three

companies are audited by domestic accounting firms. International bond

investors have become more receptive of Chinese issuers choosing not to

hire one of the “Big Four” international accounting firms over the past

decade. However, the quality of domestic auditing is variable. It is not

unprecedented for domestic audit firms to be reprimanded for

shortcomings. The auditors of Snton, Reward and KDX have previously

received reprimands, albeit not for their work on these companies.

According to Moody’s on 26 December, China’s State Council’s Financial Stability and Development Committee announced in a statement on the People’s Bank of China website that it was researching multiple ways to help commercial banks replenish capital and push for the issuance of perpetual bonds. The statement extends the thinking laid out by the regulator in 2018, when it suggested ways to augment and replenish banks’ capital with new capital instruments.

Allowing banks to issue perpetual bonds to boost their capitalization is credit positive for Chinese banks, their depositors and senior unsecured creditors. Perpetual bonds are classified as Additional Tier 1 (AT1) securities and ranked lower than senior instruments in a liquidation, meaning that they will strengthen banks’ capacity to absorb losses. The bonds will qualify and be counted toward banks’ total loss-absorbing capacity requirements, which take effect on 1 January 2025, if not earlier.

The move will also ease pressure on banks’ capital.

Although loan growth is slowing, the full phase-in of a capital conservation buffer and the migration of prior shadow banking assets back to banks’ on-balance sheet loans are two sources of strain. Issuing perpetual bonds will widen the pool of potential investors in banks’ capital instruments, creating another channel to raise AT1 capital.

Preference shares have been the dominant form of AT1 instruments that banks have so far issued, but investors with debt-only investment mandates cannot access them. Banks are currently allowed to issue preference shares to increase their overall Tier 1 capital ratios, which requires the approval of the China Banking and Insurance Regulatory Commission (CBIRC) and the China Securities Regulatory Commission. Because perpetual debts are not “shares,” their issuance is likely to require the oversight of both the CBIRC and the People’s Bank of China, as is the case for Tier 2 debt instruments.

Although several banks have expressed interest in issuing more AT1 capital instruments, banks will only begin to issue perpetual debt once the regulator provides further guidance. The size of Chinese banks’ assets means that issuance is likely to be relatively sizable and success will depend on market depth and pricing. Because they are not the same quality of equity capital, perpetual bonds have no impact on a bank’s Common Equity Tier 1 ratio.

While Asia and Europe enjoyed the highest Chinese investment growth in 2017, Australia and New Zealand experienced significant drops, according to Juwai.com’s Chinese Global Property Investment Report. The report provides an estimate of actual Chinese investments in Australian residential and commercial property; via MPA.

According to the report, total Chinese property investment in the two countries fell by 23.2%, from $23.9bn to $18.4bn. Although Australia recorded the largest share of the decline, Chinese investment in the country still remains substantial. Chinese purchases of residential and commercial properties in Australia dropped by 26.8%, from $24bn to $17.4bn.

In a statement, Juwai.com CEO and director Carrie Law said their estimate of Chinese investment in Australian property is based on industry data that helped them calculate the roughly $100bn-worth of new dwelling sales in the country last year.

“About one-quarter of those went to foreign buyers, and that Chinese buyers accounted for about three-quarters of foreign buyer spending. That yields about $19.4bn (US$14.1 billion) in estimated Chinese residential investment,” Law said.

Law attributes last year’s reduced Chinese investment to capital controls, restrictions on bank financing to offshore buyers, and to new foreign buyer taxes and restrictions. She expects moderate growth this year, “which is in line with Beijing’s goal of managed, rational overseas investment”.

Chinese buyers still consider Australia to have long-term value despite the higher stamp duties, Law added. The majority of Juwai’s residential buyers are purchasing properties in the country because they have kids studying or working there, or because it’s a place they plan to visit regularly or retire in.

“Australia offers a stable environment, safety, quality educational institutions, and high quality of life. Both Sydney and Melbourne rank in the top five most liveable cities in the world,” Law said

The report also showed that other than the U.S., Hong Kong, and Japan, Australia was China’s top destination for commercial property investment. Overall, Chinese international property investment rose to $65.9bn, with Australia, U.S., Hong Kong, and Malaysia receiving the most investment.

“Sources like KPMG suggest that Chinese commercial real estate investment accounts for one-third of all Chinese corporate direct investment in the country. Political tensions between the two countries have a greater impact in creating uncertainty with corporate commercial real estate investors than they do with individual investors buying residential property for their own use,” Law said.

China’s recent measures to support the economy mark a shift in the policy stance towards easing and away from the previous singular focus on addressing financial risks, says Fitch Ratings. Easing is likely to stop short of the type of credit stimulus that could add significantly to economic imbalances, but this remains a risk that could have negative implications for the sovereign rating.

A series of loosening measures have been announced over recent months in response to signs that previous tightening has had an overly blunt effect on the economy, exacerbated by risks from trade tensions with the US. Easing measures have included reserve-requirement ratio cuts, liquidity injections, dilution of some recent macro-prudential tightening measures, and circulars that call for more accommodative fiscal policy and other forms of support to the real economy.

The authorities appear eager to avoid another large-scale stimulus, reflecting the sheer scale of the economy’s indebtedness, the prominence of the deleveraging drive and the designation of financial de-risking as one of three “critical policy battles”. Moreover, our baseline scenario is that an aggressive policy response is unlikely to be necessary to meet the authorities’ stated growth objectives, with growth forecast to slow only gradually – to 6.6% in 2018 and 6.3% in 2019 from 6.9% in 2017.

However, the continuing importance of medium-term growth targets suggests that a significant loosening of policy cannot be ruled out in the event of a macroeconomic shock or a slowdown that is sharper than we expect. Rising trade tensions raise the likelihood of such a policy response. We do not see the US tariffs already imposed on USD50 billion of Chinese goods as large enough to revise our China growth forecasts, but the imposition of a further round of US tariffs on USD200 billion in goods, as threatened by the US administration, could have a material effect.

The deleveraging campaign had succeeded in essentially stabilising macro-leverage ratios, with a particularly strong impact on riskier, less transparent lending within the shadow-banking sector. Downward pressure on the rating could emerge over time if we were to assess that a reversal of policy settings could result in a further build-up of the economy’s vulnerabilities. Policy easing is only at a nascent stage, and we last affirmed China’s ‘A+’/Stable sovereign rating in March 2018. The policy stance is among the key sensitivities that we will continue to monitor.

The warning signs are ‘flashing amber’ on a credit crisis in China as the authorities stamp down on excessive lending, says Spectrum Asset Management; via InvestorDaily.

Credit-focused Spectrum Asset Management has issued a note titled Our double Minsky risk that focuses on the likelihood of a credit crisis playing out in China and Australia.

Spectrum principal Damien Wood said both countries have seen a build-up of private debt to record levels: from the business sector in China, and from households (via residential mortgages) in Australia.

Both countries are vulnerable to what is known as a ‘Minksy moment’, a term coined by US economist Paul McCulley in relation to the Russian debt crisis of 1998 and inspired by US economist Hyman Minsky.

The warning sign of a Minsky moment, said Mr Wood, is when the availability of credit starts to shrink.

In China, the government’s “well intended” efforts to cut down on excessive corporate leverage are causing the warning lights to ‘flash amber’ on a Minsky moment, he said.

“In October 2017, China’s central bank governor warned specifically of a Minsky moment for China. In the reported statement, he noted high corporate leverage and rising household debt,” Mr Wood said.

“One key step was to reduce lending from yield chasing ‘shadow’ banks. The concerns were that these key providers of speculative lending were an unsustainable source of finance that promoted poor allocation and management of capital.”

Shadow banking is falling in China, and the net impact is that overall lending growth is slowing, Mr Wood said.

Chinese authorities are looking to “smooth the transition of China Inc’s loan book” by cutting reserve requirements, reducing taxes, and directing banks and lenders to help financial SMEs.

But if these measures do not work, China could look to socialise credit losses.

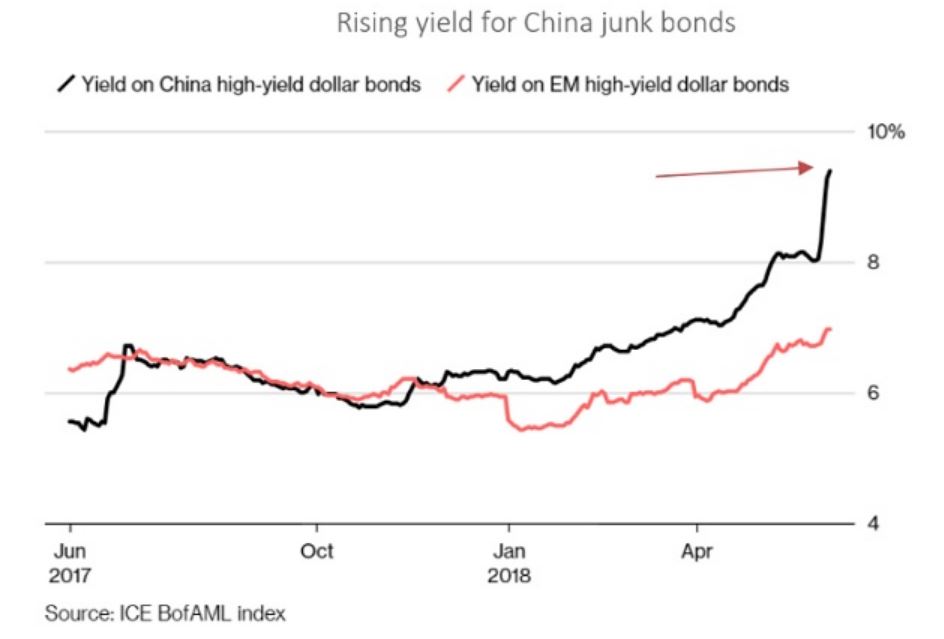

“Notwithstanding the steps taken, a key fall-out from the reduction in credit availability can be seen in the Chinese corporate bond market. Bond default rates are accelerating and credit spreads on corporate bonds have jumped,” Mr Wood said.

If defaults on Chinese corporate bonds continue (see graph above) a “stampede for the exit could begin”, Mr Wood said. “And then we are one step closer to a Minsky moment.”

Australia is facing the prospect of its own Minsky moment when it comes to household debt (which is sitting at 120 per cent), where Spectrum rates the warning light flashing ‘green to amber’.

“The problem is, even if household debt does not cause excessive problems locally, a rapid deleveraging in China would likely hit local financial markets,” said Mr Wood.

“A large debt reduction in China will risk lower than expected demand for our goods from our major export market,” he said.

“Conversely, we doubt a domestically-driven downturn locally would raise an eyebrow in China’s financial markets.”

China’s two recent reserve requirement ratio (RRR) cuts amid slowing economic growth and rising trade risks have prompted market speculation that a new cycle of monetary easing is underway, but Fitch Ratings believes it is too early to conclude recent policy actions mark a clear reversion in stance.

A return to policy settings that add to the economy’s imbalances and vulnerabilities, such as credit stimulus, nevertheless remains a risk and could put downward pressure on China’s sovereign rating, as Fitch has previously stated.

The decision by the People’s Bank of China over the weekend to implement another 50bp RRR cut across much of the banking sector follows a targeted 100bp cut in April. The latest cut will release around CNY700 billion in reserves, effective on 5 July, bringing the combined net reserve injection to CNY1.1 trillion this year. The government has stressed that funds released by the latest cut should be used to support implementation of the debt-to-equity swap programme and small and micro-sized enterprise lending.

Fitch believes that the recent RRR cuts should be viewed in the context of liquidity management measures to ensure interbank funding conditions remain stable amid the ongoing crackdown on shadow banking. The authorities have previously relied on liquidity tools such as the medium-term lending facility, the pledged supplementary lending facility and the standing lending facility to provide liquidity in the face of weak base money growth, but an RRR cut should provide more permanent (and lower-cost) support. This should reduce liquidity risks for smaller banks, in particular, which are net liquidity takers and generally more reliant on shadow financing.

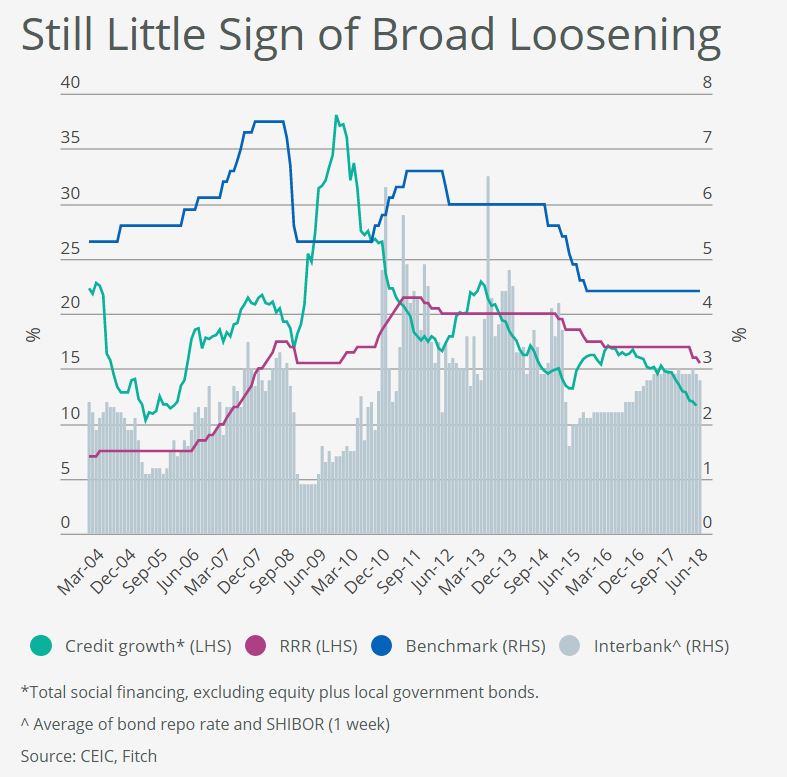

RRR cuts have previously coincided with policy loosening, but periods of clear easing (2008-2009, 2011-2012 and 2015) have also been marked by cuts to benchmark interest rates and a sustained decline in interbank rates, which have so far been absent (see chart). Meanwhile, the authorities continue to maintain a tighter bias towards macro-prudential policies and other financial regulations that aim to close regulatory loopholes, many of which are unlikely to be unwound at this stage, given the prominence the deleveraging campaign has taken at major policy meetings.

For now, Fitch’s expectation is that regulatory tightening will have a more powerful impact on credit growth than the additional liquidity generated by recent RRR cuts. Additionally, while further cuts are still possible, Fitch does not believe banks have sufficient capital to support aggressive asset expansion. That said, these adjustments do suggest that the authorities’ deleveraging drive has likely moved past its apex, and the swift deceleration in credit growth over the past year or so should soon begin to moderate.

Our baseline forecast is that GDP growth will slow during the second half of this year, due to deceleration in credit growth and a softening in the property market. Trade tensions with the US have not so far had a noticeable impact on exports, but could soon become a key policy consideration, given that a buoyant external environment has been an important contributor to China’s strong growth over the past year. If this dissipates, the authorities could be tempted to fall back on domestic stimulus to meet growth targets.

The authorities do have other policy tools beyond credit stimulus to shore up growth. Other forms of stimulus, including an on-balance-sheet fiscal stimulus, would not necessarily be ratings negative. Fitch estimates gross general government debt at less than 50% of GDP, in line with ‘A’ rated peers, which provides some room for fiscal easing. A recent State Council decision to lower taxes, which included a cut to value-added-tax rates, and plans to increase personal income tax deductions perhaps signal an initial step in that direction.

Fitch Ratings says that China’s tightened regulatory stance has slowed the build-up in financial-sector risks and should help improve the financial system’s overall stability. However, Fitch Ratings does not believe these measures have reduced risks meaningfully enough to warrant the type of sector-wide bank rating upgrades recently made by Moody’s. The authorities have also not been tested in their resolve to tackle financial risks if economic growth slowed beyond tolerance levels.

The result of Moody’s approach is rating compression between policy banks and large state banks (and mid-tier banks to some extent), which creates potential for higher rating volatility. Fitch has adopted a ‘through-the-cycle’ approach and differentiates more between institutions that we believe are likely to receive a high level of state support and those for which support is less certain.

Regulatory tightening has slowed credit growth over the last year, particularly shadow-bank activities although they have not declined. Interconnectedness in the financial system has also fallen, as shown by a drop in interbank wealth-management-product investment in 2017 and lower sequential growth in bank claims on non-bank financial institutions since 2H17. The credit-to-GDP growth gap has narrowed, but we still expect our Fitch-Adjusted Total Social Financing to reach around 273% of GDP by end-2018F (269% at end-2017). A change in the outlook on China’s operating environment, currently ‘bb+’/negative, would hinge on continued deceleration in credit growth, with deleveraging reducing contagion risks and improving transparency and governance.

The largest state banks are likely to be less affected by tighter regulation (which could increase asset impairments), given their stronger capital positions and loss-absorption buffers, as well as superior liquidity (and geographical diversification for BOC). These factors underpinned our decision last month to upgrade the Viability Ratings of BOC, CCB and ICBC to ‘bb+’ from ‘bb’.

However, mid-tier banks are more exposed, due to weaker funding and liquidity profiles, larger off-balance-sheet activities, and lower loss-absorption capacity. Moody’s upgraded almost all banks in its ratings portfolio, including some mid-sized ones, noting that they are “managing the transition well by virtue of their capital strength, liability franchise and/or relatively modest involvement in shadow banking activities”. Fitch disagrees with Moody’s view that the mid-sized banks’ involvement in shadow activities is “modest”. We also view their capital as overstated if taking into account off-balance-sheet exposures. Any upgrades to bank Viability Ratings would likely require sustainable improvements in capital buffers commensurate with risk appetite.

Our approach to support ratings for Chinese banks also differs. Fitch does not, for example, factor institutional support into the ratings of Ping An Bank or China Guangfa Bank (both BB+/Stable/b), as their largest shareholders are insurers that are subject to sector-specific regulation and would be similarly affected as the banks in a stress scenario, given the nature of their investments. These two banks represent over half of their largest shareholders’ assets, which raises doubts over their parents’ ability to provide support.

Fitch believes the state’s propensity to support different tiers of banks will vary under a stress scenario, with mid-tier banks unlikely to receive the same level of sovereign support as larger banks. Moody’s gives a three-notch uplift for many mid-tier banks, which is equivalent to the uplift that it gives for BOC, CCB and ICBC. Moody’s also now equalises its ratings of almost all state banks with the policy banks and the sovereign, which means it gives a higher support uplift, of four notches, to ABC and BOCOM than to the largest state banks.

Fitch will continue to focus on differentiating the potential for support in its rating analysis and research. In addition, Fitch’s ‘through-the-cycle’ approach aims to minimise ratings volatility.

The cut in China’s required reserve ratio (RRR) is an example of the authorities using its array of policy tools to guard against liquidity shortages, particularly in prioritised sectors, as it continues its efforts to contain financial risks, says Fitch Ratings.

We continue to believe the authorities’ commitment to tackling risks could be tested if economic growth slows, but we do not interpret this RRR cut as a step toward more expansionary policy. The People’s Bank of China (PBoC) emphasised that its “prudent” monetary policy stance remains unchanged.

The one-percentage point cut will apply to banks that faced high RRR ratios (of 17% or 15%), which includes the large banks, mid-tier banks, city banks, non-county rural and foreign banks. The freed-up liquidity will be used to first repay outstanding medium-term lending facility (MLF) loans, which the PBoC estimates at CNY900 billion. This leaves around CNY400 billion of additional liquidity that will be released into the market, with city and non-county rural banks the most likely to benefit. The PBoC expects these banks to use the extra liquidity to support lending and lower interest rates to micro enterprises, and this will form part of these banks’ Macro Prudential Assessment.

The changes will lower funding costs for banks that currently use the MLF. Banks earn interest of 1.6% on their required reserves, while they pay interest of 3.2% to the central bank on MLF loans. The requirement that banks increase lending to micro enterprises will alleviate pressure on borrowing costs for this targeted sector. It reflects efforts to support inclusive finance – an important component of the authorities’ reform agenda – and is in keeping with the more targeted RRR cut in September 2017, which only applied to banks that meet criteria on lending to rural and micro enterprises.

We stated in previous research that ordinary liquidity support would be forthcoming for banks to manage financial system risk and control financing costs for the real economy. Accordingly, this RRR cut aims to alleviate banks’ funding cost pressures, while ensuring targeted sectors receive adequate and lower-cost bank funding. We believe it should be viewed in this way, rather than as a shift in policy stance. Indeed, macro-prudential tightening measures – aimed at curbing shadow banking and excessive reliance on inter-bank funding – have been more concerted and persistent than we had previously expected. The measures contributed to a slowdown in growth of bank claims on non-bank financial institutions to 3% yoy in February 2018, compared with a 40% CAGR from 2013-2017.

That said, overall renminbi loan growth of 12.8% at end-March was still higher than renminbi deposit growth of 8.7%, implying continued deposit pressures at banks. Recent comments from the PBoC governor also emphasised the ongoing shift toward more market-driven interest rates, while local media reported that the PBoC may relax its informal guidance over bank deposit rates, which may lift deposit costs further.

We still expect efforts to contain financial risks to remain the policy focus through most of 2018, bolstered by the authorities’ confidence in the strong growth momentum sustained over the past year. Nevertheless, the government still clearly places much store in achieving high growth rates – and in particular its target of doubling real GDP per capita between 2010 and 2020. The 2018 growth target is set at around 6.5%, virtually unchanged from 2017’s target. This suggests that near-term growth would not be allowed to fall too far without a policy response. Macro-prudential tightening has so far been made in the context of growth exceeding targeted levels.