If you have savings with a bank in Australia, it is highly likely you are being ripped off. After all, Australian Consumers depend on retail deposit products to conduct their everyday banking, to safely store over $1.4 trillion of their savings and, importantly, to earn a decent return on these funds.

However, as I have been highlighting in recent shows, changes in the cash rate (often referred to as the ‘official interest rate’) via the RBA, and which is the rate paid on lending between banks in the overnight cash market only indirectly affect the cost of funding from retail deposits and the interest rates paid on retail deposit products.

Banks are quick to lift mortgage rates on mortgages, but have been significantly less market driven in terms of deposit rates, with many savers loosing out. Yet relatively few consumers switch deposit products, despite there often being a range of alternative products offering better interest rates and conditions. This loyalty tax means consumers earn significantly less than they should, over all on deposits, which boosts bank profits significantly.

So now the ACCC just completed a report on Retail Deposit Account. They gathered information, and documents on retail deposit products supplied by 14 of the largest banks in Australia. These banks collectively hold more than 90% of household deposits in Australia. This included seeking information directly from these banks as to their retail deposit products and from APRA and RBA, as well as reviewing the information available to the public on the banks’ websites.

The ACCC findings highlights that despite the importance of transaction accounts, savings accounts and term deposits, the ongoing challenges consumers face in searching for, comparing, and switching between products means that consumer engagement with the market for retail deposit products is relatively low. This low level of engagement means many consumers miss out on earning more from their savings.

Widespread strategic and selective pricing also adds difficulty for consumers when seeking to locate key product information and compare market offerings. This lack of transparency may also damage consumer confidence in the market.

Given the range of factors that banks take into account and the strategic pricing approaches they employ when setting their retail deposit rates, the interest rates received by consumers do not automatically follow movements in the cash rate target.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

If you have savings with a bank in Australia, it is highly likely you are being ripped off. After all, Australian Consumers depend on retail deposit products to conduct their everyday banking, to safely store over $1.4 trillion of their savings and, importantly, to earn a decent return on these funds.

However, as I have been highlighting in recent shows, changes in the cash rate (often referred to as the ‘official interest rate’) via the RBA, and which is the rate paid on lending between banks in the overnight cash market only indirectly affect the cost of funding from retail deposits and the interest rates paid on retail deposit products.

Banks are quick to lift mortgage rates on mortgages, but have been significantly less market driven in terms of deposit rates, with many savers loosing out. Yet relatively few consumers switch deposit products, despite there often being a range of alternative products offering better interest rates and conditions. This loyalty tax means consumers earn significantly less than they should, over all on deposits, which boosts bank profits significantly.

So now the ACCC just completed a report on Retail Deposit Account. They gathered information, and documents on retail deposit products supplied by 14 of the largest banks in Australia. These banks collectively hold more than 90% of household deposits in Australia. This included seeking information directly from these banks as to their retail deposit products and from APRA and RBA, as well as reviewing the information available to the public on the banks’ websites.

The ACCC findings highlights that despite the importance of transaction accounts, savings accounts and term deposits, the ongoing challenges consumers face in searching for, comparing, and switching between products means that consumer engagement with the market for retail deposit products is relatively low. This low level of engagement means many consumers miss out on earning more from their savings.

Widespread strategic and selective pricing also adds difficulty for consumers when seeking to locate key product information and compare market offerings. This lack of transparency may also damage consumer confidence in the market.

Given the range of factors that banks take into account and the strategic pricing approaches they employ when setting their retail deposit rates, the interest rates received by consumers do not automatically follow movements in the cash rate target.

An important discussion about the games banks are playing in relation to the setting of deposit interest rates, in the context of the RBA rate hikes. Steve Mickenbecker from Canstar and I explore the elements which are driving returns lower than they should be, and what we can do about it. Another case of the apathy tax at work! Steve Mickenbecker is in Canstar’s Group Executive Team, bringing more than 30 years of experience in the Australian financial services industry. As a financial commentator for Canstar, Steve enjoys sharing his expertise across topics such as home loans, superannuation, insurance, mortgages, banking, credit cards, investment, budgeting, money management and more. Go to the Walk The World Universe at https://walktheworld.com.au/

I caught up with Steve Mickenbecker, Group Executive, Financial Services & Chief Commentator at Canstar to discuss the latest in deposit account rates as they fall though the fall.

Note: DFA has no commercial relationship with Canstar

I caught up with Steve Mickenbecker, Group Executive, Financial Services & Chief Commentator at Canstar to discuss the latest in deposit account rates as they fall though the fall.

Note: DFA has no commercial relationship with Canstar

Let’s talk about the bank bail-in conundrum. A couple of weeks back I discussed whether bank deposits in Australia would be safe in a crisis. The video received more than 1,400 views so far, and has prompted a number of important questions from viewers. So today I update the story, and addresses some of the questions raised. The bottom line though is I think we are being sold a pup, which by the way refers to a confidence trick originating in the Late Middle Ages!

Watch the video, or read the transcript.

First, a quick recap, for those who missed the first video. Officially, in Australia currently bank deposits are protected up to $250,000 per person by a Government Guarantee – The Financial Claims Scheme. For banks, building societies and credit unions incorporated in Australia, the FCS provides protection to depositors up to $250,000 per account-holder per ADI according to APRA. Only deposit products provided by ADIs supervised by APRA were eligible to be covered. Amounts between $250,000 and $1 million are not be covered under the Guarantee Scheme. Above $1m banks can elect to pay a fee to the Government for this for protection, but none do. However, as we will see there are even questions about the sub $250k. But note this, the FCS can only be activated by the Australian Government, whilst APRA is responsible for administering the Scheme.

The RBA says upon its activation, APRA aims to make payments to account-holders up to the level of the cap as quickly as possible – generally within seven days of the date on which the FCS is activated. The method of payout to depositors will depend on the circumstances of the failed ADI and APRA’s assessment of the cost-effectiveness of each option. Payment options include cheques drawn on the RBA, electronic transfer to a nominated account at another ADI, transfer of funds into a new account created by APRA at another ADI, and various modes of cash payments.

The amount paid out under the FCS, and expenses incurred by APRA in connection with the FCS, would then be recovered via a priority claim of the Government against the assets of the ADI in the liquidation process. If the amount realised is insufficient, the Government can recover the shortfall through a levy on the ADI industry. Ok, maybe in the case of a single failure

Now, since the Global Financial Crisis, regulators have been working on ways to avoid a tax payer based rescue in a crash, because for example, the UK’s Royal Bank of Scotland was nationalised in 2007. This cost tax payers dear, so regulators want measures put in place to try to manage a more orderly transition when a bank gets into difficulty.

The New Zealand the Open Bank Resolution (not to be confused with Open Banking) is the clearest example of a so called bail-in arrangement. Customer’s money, held as savings in a distressed bank can be grabbed to assist in a resolution in a time of crisis. The thinking behind it is simple. Banks need an exit strategy in case of a problem, and Government bail-outs should not be an option. So a manager can be appointed to manage through the crisis. They can use bank capital, other instruments, like hybrid bonds and deposits to create a bail-in. This approach to rescuing a financial institution on the brink of failure makes its creditors and depositors take a loss on their holdings. This is the opposite of a bail-out, which involves the rescue of a financial institution by external parties, typically governments using taxpayer’s money.

So what about Australia? Well, the Financial Sector Legislation Amendment (Crisis Resolution Powers and Other Measures) Bill 2017 is now law, having been through a Senate Inquiry. It all centers on the powers which were to be given to APRA to deal with a banking collapse.

In the bill, there is a phrase “any other instrument” in the list of bail-in items. Treasury said, “the use of the word ‘instrument’ is intended to be wide enough to capture any type of security or debt instrument that could be included within the capital framework in the future. It is not the intention that a bank deposit would be an ‘instrument’ for these purposes”. Yet, deposits were not expressly excluded.

In fact, when the Bill came back to Parliament it went through both houses with minimal discussion (and members on the floor, the chambers were all but empty). And despite a proposal being drafted and with Government Lawyers in parallel to exclude deposits, it was passed on 14th February without this change, leaving the door wide open under “any other instrument”. All the verbal assurances are meaningless.

So, the result appears to be APRA has wider powers now to handle a bank in crisis, and deposits are potentially accessible. They are not expressly excluded, and in a time of crisis, could be bailed-in.

But this is not the end of the story. Treasurer Morrison issued a letter to Liberal government members with some talking points to justify this actions, in response to a wave of protests. But in so doing, he raises more questions.

The first point is that the Deposit Guarantee scheme (the one up to $250k) is not currently active. The Government would need to activate it, and can only do so when an institution fails. This is important because it means that in theory at least, APRA could mount a deposit bail-in before the Government activates the deposit protection scheme. Consider what would happen if many banks all got into difficulty at the same time, as could be the case in a wider banking crisis – after all, they all have similar banking models.

The second point is that the Treasurer makes reference to the 1959 Banking Act, and says that depositors have a claim above other creditors in a bank failure. But in fact the 1959 Act says depositors do indeed rank ahead of other unsecured creditors, but that means the secured creditors come first. So would anything be left in case of a bank failure given the massive exposure to property?

Next, the letter says APRA has now enhanced powers to protect the interests of depositors – not deposits. And looking at the New Zealand situation the bail-in provisions there are framed to do just this, by utilising deposits to help keep the bank afloat, thus protecting depositors. The Reserve Bank of New Zealand says this is IN THE INTERESTS OF DEPOSITORS.

Oh, and finally, Morrison says the way the Bill went into Law was quite normal by being listed in the Senate Order of Business, meaning members had the opportunity to debate the bill if they had wanted to. In fact, only seven Senators were there despite really needing a quorum of 19, but there is a get out in that a quorum is only needed if a division was called, and in this case it was simply nodded through. Democracy in action.

So there you have it. No Deposit Protection currently exists. Its limited to $250k per person if activated by the Government, at their discretion, and the legalisation leaves the door wide open for a New Zealand style of Bail-In. Not a good look.

So what should Savers do? Well, this is not financial advice, but the New Zealand view is that savers should make a risk assessment of banks and select where to deposit funds accordingly. But I am not sure how you do that, given the current low level of disclosures. APRA releases mainly aggregate data and protects the confidentially of individual banks as they are required to do under the APRA act.

Next, do not assume deposits are risk free, they are not. This means lenders should be offering rates of return more reflective of the risks we are taking, currently they are not (in fact deposit rates are sliding, as banks seek to repair margins). You might consider spreading the risks across multiple institutions

Consider alternative savings options (which are limited). Clearly, property, stocks and shares and even crypto currencies are all risky – there are no safe harbours. I guess there is always the mattress.

One other point to make. Several people are calling a bill to bring a Glass-Steagall split between core banking operations and the speculative aspects of banking. Glass-Steagall was enacted in the US in 1933 after the great crash, separating commercial and investment banking and preventing securities firms and investment banks from taking deposits. But in 1999 the US Congress passed the Gramm–Leach–Bliley Act, also known as the Financial Services Modernization Act, to repeal them. Eight days later, President Bill Clinton signed it into law. Following the financial crisis of 2007-2008, legislators unsuccessfully tried to reinstate Glass–Steagall Sections 20 and 32 as part of the Dodd–Frank Wall Street Reform and Consumer Protection Act. Both in the United States and elsewhere, banking reforms have been proposed that refer to Glass–Steagall principles. These proposals include issues of “ring fencing” commercial banking operations and narrow banking proposals that would sharply reduce the permitted activities of commercial banks.

The point of the bill was to isolate the risky bank behaviour, relating to derivatives and trading from core banking activities. In the case of a banking crisis, triggered by a collapse in the financial markets such an arrangement would protect the operations of the core banking. We got a glimpse of that a month ago when US trading volatility shot through the roof.

But, in Australia, the bulk of the risks in the banking system comes not from the derivatives side of the business, but the massive exposure to household debt and the property sector, and the risky loans they have made. We discussed this on the ABC yesterday. More than 60% of all banking assets are aligned with home lending, plus more relating to commercial property. Thus I do not believe a Glass-Stegall type separation would help to mitigate risks to the banking sector here much at all.

Better to push for a definitive change to the APRA Bill and get deposits excluded from the risk of bail-in. Or place a levy on all banks to directly protect depositors as has been put in place in Germany, where a dedicated government entity has been created for just this purpose.

What I find remarkable is that following loose banking regulation for years, during which the banks have returned massive profits to shareholders, and ramped up their risks, depositors are being lined up by the Government to bail out a failing bank. This is simply wrong.

Australians are being encouraged to repay debt instead of putting money in the bank, as new data confirms that savings accounts are paying record low rates of interest.

The Reserve Bank reported in recent days that online savings accounts and bonus savers were paying less than a third of what they were a decade ago, with term deposits not much better.

Average interest rates on online savers peaked at 7.3 per cent in 2008 before plummeting. They were sitting at 1.65 per cent in April, according to the latest RBA figures.

Back in the golden years, a saver with $10,000 could have earned more than $600 a year in an online account. Now, they’d be very lucky to get $200.

(Data on online savers only goes back to 2004 because that’s when they started being offered in Australia. NAB was the last of the big four to offer them in September 2005.)

Bonus savings accounts, which offer conditional bonus interest on top of base rates, went as high as 5.5 per cent in 2008. They’ve dropped since to 1.95 per cent.

Gregory Mowle, a financial literacy expert, said with rates so low, Australians should consider paying off debt instead.

“As an alternative to a savings account, if someone has debt, any form of debt, get out of it. It’s the best form of savings you can have,” he told The New Daily.

“For people with debt, my message is, rather than parking your $500 somewhere and barely earning 1 per cent, well, if you’re being charged 15 per cent on a $5000 credit card debt, repay the debt instead.”

He also encouraged Australians with bonus saver rates to keep a close eye on the fine print.

“If a certain minimum balance isn’t kept in the account or if you withdraw money out or don’t put a certain amount back in, you won’t get that token interest rate payment.”

Even at low rates, saving is still a good idea

Mr Mowle acknowledged there is a good economic argument for rock-bottom rates.

“Rates are at record lows because the government and the lenders want you to borrow money. If everybody saved, the economy would collapse.”

But he said saving is still a good idea, especially to protect against emergencies such as job loss.

Don’t even think about experimenting with the share market or other sophisticated investments until you have, at a “bare minimum”, enough savings to cover three months of living expenses, Mr Mowle said.

“Some people jump straight into shares because their personality says savings accounts are too boring. But I think someone should have at least three months’ worth of cash there before they start to diversify and look at things like equities.”

Savings accounts may be boring, but they’re also safe, he said.

“I’d caution to people not to be chasing alternatives to your basic savings products because promised higher rates always come with guaranteed higher risk.”

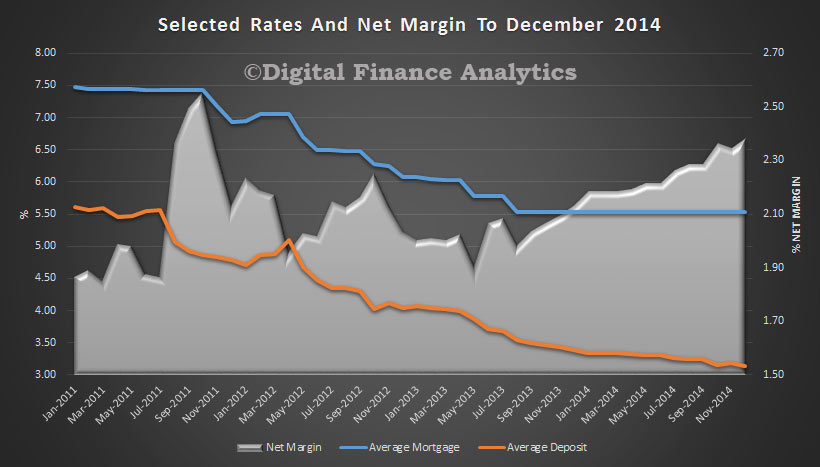

Continuing our analysis of bank margins, we have updated our industry model, with the latest funding and product data. At an aggregate industry level, we see that the average home lending rate has remained static (because whilst there are substantial discounts for new loans, the bulk of the back book has not seen any rate reduction) since 2013. The RBA last reduced their cash rate in August 2013, and the benchmark rate has remained static since then.

So, despite the fact that the banks are unlikely to be able to reduce their provisions much further (as they did last year) to bolster profits, and their increased capital requirements, the highlighted net increase in margins bodes well for bank performance, though at the expense of borrowers, who are not enjoying rate reductions, and depositors who are seeing their interest rates continuing to fall.

“Today I will talk about the imminent arrival of the revised liquidity regime for the Australian financial sector. I will recap some of its features, particularly how they relate to the Reserve Bank, and discuss some of the impact that it is having on market pricing.

An important aspect of the Basel III liquidity standard, the Liquidity Coverage Ratio (LCR), comes into effect in under one month’s time at the beginning of 2015. The LCR requires that banks hold sufficient ‘high quality liquid assets’ (HQLA) to withstand a 30-day period of stress. The amount of HQLA a bank needs to hold is determined by the composition and maturity structure of its balance sheet. The more liabilities that run off within that 30-day window, the more HQLA that needs to be held. At the same time, particular types of investors or depositors are assumed to be less stable than others (in terms of their likelihood of withdrawing funds), which also results in a greater need for liquid assets.

As has been known for some time, the Australian financial system does not have an especially large stock of HQLA. The only instruments that have been deemed to meet the Basel standard of liquidity are debt issued by the Commonwealth and state governments (CGS and semis) along with cash balances at the Reserve Bank. The banking system’s overall liquidity needs are greatly in excess of what could reasonably be held in those assets. To put some numbers on this, APRA has determined that for next year, the Australian banking system’s liquidity needs amount to $450 billion. The total stock of CGS and semis on issue currently amounts to around $600 billion. If the banks were to attempt to meet their liquidity needs solely by holding only CGS and semis, a number of problems would arise. Firstly, any attempt would likely be in vain, because there are a large number of other entities which are required to or want to hold CGS and semis too. Second, in the process of trying to do this, the liquidity of the market for these securities would be seriously compromised. This would be completely self-defeating as the overall aim is to have the banks hold more liquid assets.

To address these circumstances, an important component of the liquidity regime in Australia is the committed liquidity facility (CLF) where, on the payment of a 15 basis point fee, banks will be able to obtain a commitment from the Reserve Bank to provide liquidity against a broad range of assets under repurchase agreement.

APRA has recently determined that the total CLF requirements of the Australian banking system for 2015 amount to around $275 billion. This amount was determined by first assessing that the amount of CGS and semis that could reasonably be held by banks without unduly affecting market functioning was $175 billion. The Reserve Bank provided this assessment to APRA. The CLF amount is then simply the difference between this and the overall liquidity needs of the system.

The banks that require a CLF from the Reserve Bank sign a deed of agreement with us and pay their fee before the end of this year. Then from the beginning of next year, the arrangement comes into effect.

I have talked before about some of the impact on pricing in various markets of the new liquidity regime.[4] We have attempted to limit the impact on the price of CGS and semis, but necessarily, because the banks are holding more of these securities than previously (Graph 1), the price is higher (and the yield lower) than would otherwise be the case.

Graph 1

Overall, the impact of the LCR on market pricing is relatively small. The larger changes have been around deposit pricing and the terms and conditions of deposits, which I will come to shortly, but there have been some other effects which are worth commenting on.

Firstly, a less discussed aspect of the liquidity standard is the requirement for a demonstrated internal liquidity transfer pricing model for banks. This has required banks to fully reflect the liquidity cost in the price of the various services they offer customers. This has resulted in a change in the price and/or terms and conditions of a number of facilities. One noteworthy example is a line of credit where, in the past, banks often did not factor into the price they charged for this facility, the potential draw on liquidity this entailed, particularly in a stressed situation. On the other hand, longer fixed-term deposits are more attractive to banks and consequently have been repriced upwards (see below).

A second impact which has been evident more recently is a widening in the spread between bank bills and OIS (Graph 2). In the depths of the crisis, such a widening was often an indicator of stress in the financial situation. But that does not appear to be the case currently as other indicators of bank creditworthiness are little changed, including spreads on longer term borrowing and CDS premia.

Graph 2

Instead, our assessment is that in large part, this reflects the new liquidity regime combined with some other dynamics in the market. The graph shows that the widening has been most pronounced at the longer bank bill maturities, and indeed is quite small for a one month bank bill. This is because issuing a one month bill has little attraction to a bank: its liquidity cost is relatively high as its maturity is likely to occur within the 30-day liquidity window. Hence a bank would need to hold HQLA of similar size to the amount of funding the bank bill raised. Instead, there is a greater incentive to issue at longer maturities and so the spread on 6-month bills has widened by more as there has been greater supply of such paper.

Over the past two months, the original term to maturity of bank bills and certificate of deposits on issue has changed noticeably, with the stock of 6-month bills increasing by $7.3 billion (11 per cent) and 12-month bills by $1.4 billion (43 per cent). In contrast, the stock of outstanding bills with an original tenor shorter than five months has declined by a total of $9.7 billion (8½ per cent).

At the same time, the cost of Australian dollars in the forward FX market has been quite elevated. This high price in the forwards market has been due to a number of factors including the tendency of hedge funds to fund their Australian dollar shorts in this market, as well as an increase in the use of this market by foreign bank branches to fund Australian dollar lending.

Historically, Australian banks have tended to raise a significant share of their short-term funding in foreign markets, mostly in US dollars, and then swap them back into Australian dollars to fund their Australian dollar-denominated asset base. They would swap these foreign currency funds when the cost was sufficiently attractive, leaving it in foreign currency in the interim. Under the new liquidity regime, the cost of short-term foreign currency funding is higher, so this is less attractive. Combined with a higher swap cost, the all-in cost of short-term offshore funding is higher and hence domestic issuance is relatively more attractive. As a result we have seen more of it, which has contributed to the widening in the spread to OIS.

Finally, I will return to the impact of the LCR on deposit pricing. Graph 3 shows the evolution of the funding mix of Australian banks over the past decade. The rise in the share of deposit funding from 2008 is readily apparent, as is the decline in the share of short-term and long-term wholesale funding. The growth in deposits is now of a similar pace to that in bank lending, having been considerably faster over recent years. As a result, the deposit share of funding has levelled off.

Graph 3

The increase in deposit funding was in part a result of the increased returns on offer, as banks actively sought this outcome by offering higher interest rates. (It also reflected a shift on the part of investors for the perceived safety of a bank deposit.) The interest rate on both at-call and term deposits rose markedly compared with money market rates of equivalent maturity (Graph 4). As you can see from the graph, this process of paying higher deposit rates has largely run its course.

Graph 4

Within this overall repricing, there have been some changes in the mix of deposit rates and products as a result of the introduction of the LCR. As I mentioned earlier, banks have an incentive to reduce the amount of liabilities that roll off in less than 30 days. Deposits which are deemed to be subject to high run-off rates and those which are callable within 30 days will be more expensive for banks. Banks are therefore working towards converting many of these less stable deposits into a more stable deposit base. For example, retail and SME deposits are deemed to be ‘stickier’ than institutional deposits. Part of this transition is being induced by price signals: interest rates offered on new or existing deposit products which are deemed to be more stable are rising relative to interest rates on products deemed to be less stable.

These types of changes appear to have accelerated recently as we draw closer to the implementation of the LCR and probably still have some way to run. To date, we have seen only a few banks offer notice of withdrawal accounts to customers. These accounts require the depositor to provide the bank with 31 days or more notice of a withdrawal (obviously 31 days is one day longer than the 30-day liquidity stress period). Interest rates offered on these accounts are among the higher rates offered in the deposit market. It may be that we see a broader move to these types of accounts or changes in terms and conditions on existing accounts through the course of next year.

We have also seen a fall in the growth of term deposits relative to transaction and at-call deposits over the past few years. In fact term deposits as a share of banks’ funding has been falling while transaction and at-call deposits have been growing strongly. Part of this is because a flattening of the yield curve has made investors less inclined to invest in longer term deposits. But in part it is because under the LCR, some transactional and operational deposits are subject to lower run-off rates than deposits that are largely attracted by higher interest rates. Indeed, there has been some indication that banks have been transitioning depositors into deposit products treated more favourably under the LCR.

But banks are not limited to just changing their deposit offerings. We could see them look for more opportunities to package retail deposits with other products as the deposits of customers that also have other relationships with the bank are deemed to be more stable under the LCR.

So to conclude, the full implementation of the new liquidity regime in Australia is imminent. From the beginning of next year, banks in Australia will be fully subject to the Liquidity Coverage Ratio. This has already had an impact on the pricing and nature of a number of financial products, as well as the structure of bank liabilities. While the bulk of the impact may be behind us, there are still a number of changes in the pipeline, particularly around deposits.”

Blog")