The April ABS release showed a surprise small rise in the unemployment rate. So we look at the figures and ask if this is significant, given the budget papers expectation of higher unemployment ahead.

Lots of mistaken observations about the latest ABS Employment figures. So we look at the statistical anomalies which explain the differences, and look at the different methods used compared with the Roy Morgan series.

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

The ABS released their latest data on the labour market today, and it was not quite what was expected by the markets. In fact the seasonally adjusted unemployment rate rose to 3.5 per cent in August 2022, according to the ABS.

The key reason for the rise in unemployment was the 0.2% lift in the labour force participation rate to 66.6%. The participation rate now sits just below the record high 66.8% recorded in June.

Today’s post is brought to you by Ribbon Property Consultants. If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you. Buying property, is both challenging and adversarial. The vendor has a professional on their side. Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make. Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest. Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

We examine the latest ABS data relating to employment for May 2022. The engine is running hot, but many more than usual are off sick. Rates are probably close to as low as they will go, as rates rise and business investment falters.

We look at the latest employment numberwang, as well as the consumer confidence and leading indicators. Are the current mob good economic managers?

Go to the Walk The World Universe at https://walktheworld.com.au/

Today’s post is brought to you by Ribbon Property Consultants.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

The ABS released their Labour statistics data today, and in came in line ball with last month. Not as strong as economists were expecting. That said, the labour market is tight because external labour supply from temporary works and migration has stalled thanks to the pandemic. Essentially the supply has dropped by around 500,000. So this is hardly great economic management, and if migration is powered up again, the unemployment will rise. The latest projections are for a fall to 3. Something then a subsequent reversal as migration kicks in.

And remember the threshold is an hour worked to qualify as employed! The seasonally adjusted unemployment rate remained at 4.0 per cent in March 2022, according to data released today by the Australian Bureau of Statistics (ABS).

The ABS, said: “With employment increasing by 18,000 people and unemployment falling by 12,000, the unemployment rate decreased slightly in March, though remained at 4.0 per cent in rounded terms. “4.0 per cent is the lowest the unemployment rate has been in the monthly survey. Lower rates were seen in the series before November 1974, when the survey was quarterly.”

The unemployment rate continued to fall faster for women than for men.

Today’s post is brought to you by Ribbon Property Consultants.

If you are buying your home in Sydney’s contentious market, you do not need to stand alone. This is the time you need to have Edwin from Ribbon Property Consultants standing along side you.

Buying property, is both challenging and adversarial. The vendor has a professional on their side.

Emotions run high – price discovery and price transparency are hard to find – then there is the wasted time and financial investment you make.

Edwin understands your needs. So why not engage a licensed professional to stand alongside you. With RPC you know you have: experience, knowledge, and master negotiators, looking after your best interest.

Shoot Ribbon an email on info@ribbonproperty.com.au & use promo code: DFA-WTW/MARTIN to receive your 10% DISCOUNT OFFER.

The latest ABS Employment numbers came in better than expected, and with an unemployment number of 4% was better than expected. But are we reading the numbers right, and does it give the full picture. We examine the evidence.

The latest edition of our finance and property news digest with a distinctively Australian flavour.

Go to the Walk The World Universe at https://walktheworld.com.au/

Seasonally adjusted hours worked fell by 8.8 per cent between December 2021 and January 2022, according to the Australian Bureau of Statistics (ABS).

The changes in hours worked were more pronounced than for other key indicators, with employment increasing by around 13,000 people, unemployment by 6,000 people and the unemployment rate remaining at 4.2 per cent.

But there are deeper reasons why the numbers are the way they are, and today we explore this…. in a word – migration, or the lack of it…!

Go to the Walk The World Universe at https://walktheworld.com.au/

The latest edition of our finance and property news digest with a distinctively Australian flavour.

In today’s show we look at the latest employment data from the US, and Australia and discuss the implications, and highlight that the numbers tell us less than many think about what is going on. Not least, do people spend less time looking for jobs when the Government hands out more support?

Numberwang is a recurring sketch in Series 1 and 2 of That Mitchell and Webb Look. It is a fictional television series in which the two contestants call out seemingly random numbers which are occasionally told to be Numberwang. Each episode varies slightly, with the basic format remaining each time.

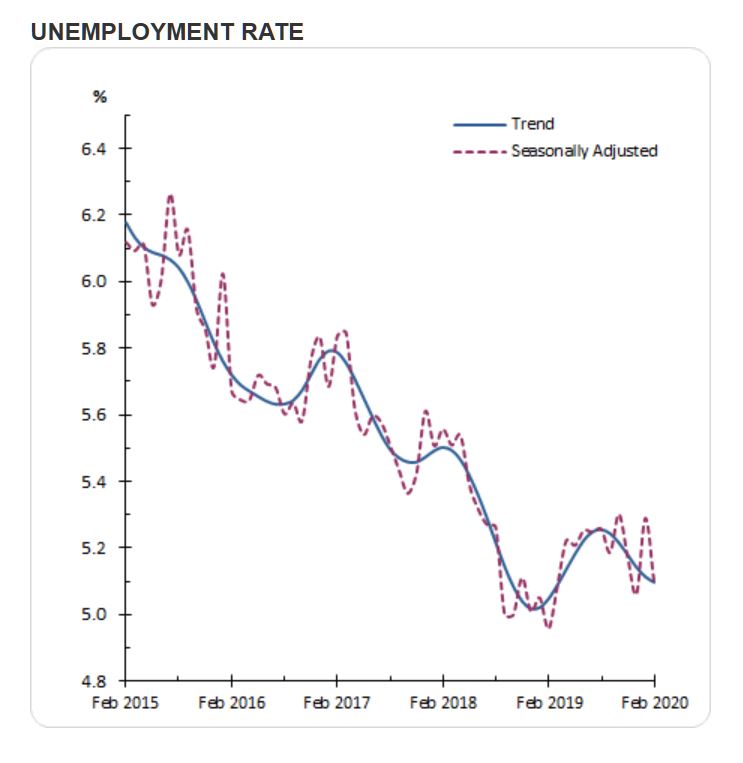

Australia’s trend unemployment rate remained steady at 5.1 per cent in February 2020, from a revised January 2020 figure, according to the latest information released by the Australian Bureau of Statistics (ABS) today.

ABS Chief Economist Bruce Hockman said: “The trend unemployment rate remained steady at 5.1 per cent for a third consecutive month.”

There was no notable impact on February 2020 Labour Force statistics resulting from the recent bushfires or COVID-19. The February reference period was in the first half of the month and pre-dates the notable increases in confirmed cases in Australia of COVID-19.

Employment and hours

In February 2020, trend monthly employment increased by around 21,000 people. Full-time employment increased by around 13,000 and part-time employment increased by around 8,000 people.

Over the past year, trend employment increased by around 241,000 people (1.9 per cent), below the average annual growth over the past 20 years (2.0 per cent).

Full-time employment growth (1.5 per cent) was below the average annual growth over the past 20 years (1.6 per cent) and part-time employment growth (2.7 per cent) was also below the average annual growth over the past 20 years (3.0 per cent).

The trend monthly hours worked decreased by less than 0.1 per cent in February 2020 and increased by 0.8 per cent over the past year. This was lower than the 20 year average annual growth of 1.6 per cent.

“We have seen a decrease in the trend hours worked in recent months, even though employment has continued to grow. This largely reflects a fall in the total hours worked by men”, added Mr Hockman.

Underemployment and underutilisation

The trend monthly underemployment rate remained steady at 8.6 per cent in February 2020, and increased by 0.3 percentage points over the past year.

The trend monthly underutilisation rate also remained steady at 13.7 per cent in February 2020, an increase of 0.4 percentage points over the past year.

States and territories trend unemployment rate

The monthly trend unemployment rate increased in Victoria and decreased in Queensland, South Australia and Tasmania in February 2020. The unemployment rate remained steady in all other states and territories.

Over the year, unemployment rates fell in Queensland, South Australia, Western Australia, Tasmania and the Australian Capital Territory. Unemployment rates increased in New South Wales, Victoria, and the Northern Territory. Seasonally adjusted data

The seasonally adjusted unemployment rate decreased by 0.2 percentage points to 5.1 per cent in February 2020, while the underemployment rate remained steady at 8.6 per cent. The seasonally adjusted participation rate decreased by 0.1 percentage points to 66.0 per cent, and the number of people employed increased by around 27,000.

In original terms, the incoming rotation group in February 2020 had a higher employment to population ratio than the group it replaced (62.7% in February 2020, compared to 61.8% in January 2020), however it was lower than the sample as a whole (62.8%). The incoming rotation group had a higher full-time employment to population ratio than the group it replaced (43.6% in February 2020, compared to 43.4% in January 2020), and was higher than the sample as a whole (43.2%).

The incoming rotation group had a higher unemployment rate than the group it replaced (5.9% in February 2020, compared to 5.3% in January 2020), and was higher than the sample as a whole (5.5%). The incoming rotation group had a higher participation rate than the group it replaced (66.6% in February 2020, compared to 65.2% in January 2020), and was higher than the sample as a whole (66.5%).