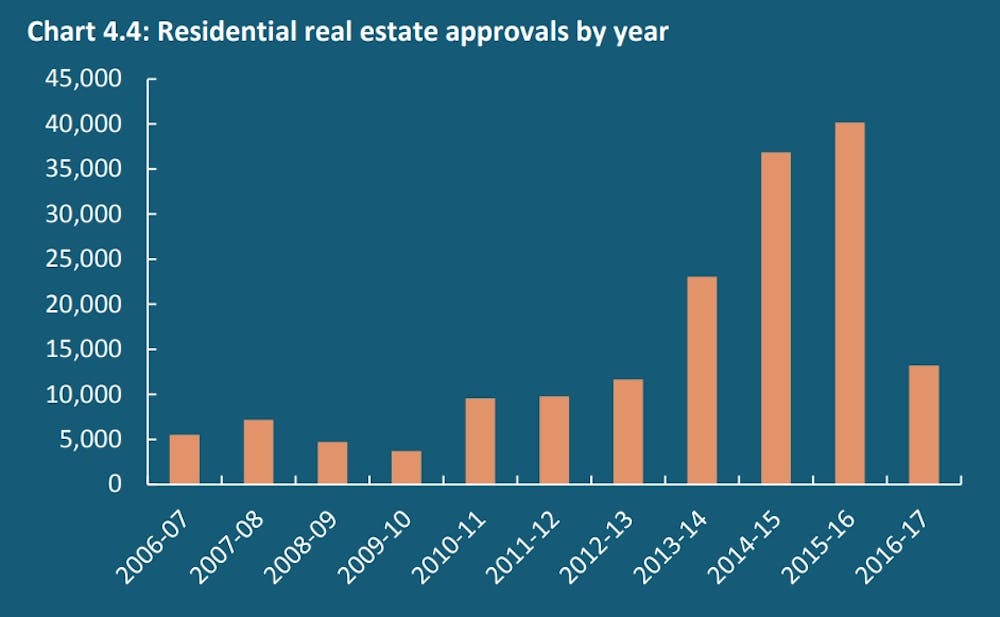

Australia’s Foreign Investment Review Board (FIRB) reported this week that foreign residential real estate approvals dropped significantly in the 2016-17 period.

Whereas 2015-16 saw 40,149 approvals granted, totalling A$72.4 billion, the figure for the following year was just 13,198 approvals, totalling A$25.2 billion. On these numbers, the foreign property investment boom looks to be over.

This is bad news for the property and financial industries, who are already feeling the pressure of weak household income growth, tighter lending restrictions on local borrowers, and a slowing in housing market activity in key Australian cities.

FIRB suggests that declining demand from China is a factor in the overall decline in overseas approvals. Chinese demand may have been weakened by a range of factors, including the new FIRB application fees, Chinese overseas direct investment capital controls, and the changing global economy.

But if the cycle is moving from boom towards bust, we have learned several things along the way.

Lesson 1: We still need more data

In 2014 the House of Representatives Standing Committee on Economics undertook an inquiry into foreign investment in residential real estate. It acknowledged the growing public disquiet about the level of this foreign investment, adding that:

…there is no accurate or timely data that tracks foreign investment in residential real estate. No one really knows how much foreign investment there is in residential real estate, nor where that investment comes from.

Four years on, FIRB is still flagging the limitations of data collection and analysis. Without fine-grained data, it’s hard to forecast how much, if at all, the injection of foreign capital can push up local house prices.

The latest figures come with a caveat. The approvals data represent potential investment, rather than actual investment. There are key differences between the two. Potential investors might, for example, seek approval for multiple properties while only intending to buy one of them.

We need the government to collect more extensive and detailed data on individual foreign real estate investment, and make it publicly available. This needs to cover more than approvals data at the city level, but data on investment levels in neighbourhoods or even individual housing developments.

Lesson 2: People on the property ladder are less hostile to foreign buyers

Data from Sydney reveals widespread concern about foreign investment. Almost 56% of Sydneysiders believed foreign investors should not be allowed to buy residential real estate in Sydney. Only 17% of respondents in our study thought the government’s regulation of foreign housing investment was effective.

Just over half of Sydneysiders say they would not want Chinese investors buying properties in their suburb. And 78% thought foreign investment was driving up housing prices in greater Sydney.

Yet those who have real estate investments were more likely to support foreign investment than those who don’t. This suggests that Sydneysiders with equity in the housing market, such as homeowners or investors, might view foreign buyers pushing up housing values as positive. And they might fear that the new decline in foreign investment might depress their assets.

Lesson 3: Housing is built with specific buyers in mind

When Chinese real estate investment started to rise significantly in 2013-14, property developers scrambled to model this new emerging market. The real estate media rushed to map out where Chinese investors were keenest to buy, and how best to design and market property developments to this new foreign client base.

The growing numbers of Chinese and Indian migrants in Australia means property investors need to consider the cultural sensitivity of the residential property they purchase to ensure they maximise the resell value.

Between 2013 and 2017, property developers, both local and foreign, regularly contacted me to ask if I had any up-to-date research on foreign investors’ consumer preferences and market forecasts. I did not. But there was no shortage of advice out there, covering everything from feng shui-informed housing design to the key needs of foreign university students.

Some global real estate agents suggested to their clients that they could buy an Australian home to accommodate their child while they were studying at an Australian university, and then use the capital gain from the property sale to pay back the tuition fees.

Many property developers were formulating medium- to long-term development pipelines that included the foreign capital and consumer preferences of foreign investors. It is unclear, now, whether much of this housing stock will ever be built. If it is, will it suit the changing future needs of our cities, or address our ongoing housing affordability problems?

In other words, what sorts of properties will be left as the legacy of the recent foreign real estate investment mania?

Lesson 4: Racialised housing debates are simplistic and harmful

We need to take care not to conflate domestic Chinese-Australian buyers with international Chinese investors. Much of the media coverage of the new report features stereotyped images of Asian families buying an Australian home. But given the foreign investment rules and logistics involved, these pictures are far more likely to depict Chinese-Australians than foreigners.

Understanding the long-term migration and education plans of the investors is important too. Different investor groups will interact with the city in different ways, and their impact on society can be vastly different too. For example, super-rich absentee investors will have a different impact on neighbourhood life compared with that of middle-class migrants or international students.

If the federal government wants to court foreign investment, then better education about the possible risks and benefits of individual foreign real estate investment is needed. Our research suggests that the government’s pro-foreign investment stance must be accompanied with strategies to protect intercultural community relations in Australia.

…fluctuation in property prices recorded for Sydney have been caused by the forces linking the city to the Australian economy and to the remainder of the world.

Daly charted the influx of foreign people and capital into Sydney between 1850 until 1981, as wealth was channelled through the financial services sector and into urban real estate. Along the way, he observed that one “group to attract the abuse of the general population were the Chinese”.

Domestic and foreign real estate investment have long been connected to the financial services industries, and the built environment is central to creating and storing surplus capital. Australian cities continue to be heavily influenced by global money today.

A key lesson is that domestic and foreign housing booms, bubbles and busts are thus better understood as cycles within our housing and financial system, rather than as a set of short-term ruptures to this system.

We need to think about the collective impacts of domestic and foreign real estate investment over the long-term in our cities if we are serious about addressing housing inequality.

Author: Dallas Rogers, Program Director, Master of Urbanism. School of Architecture, Design and Planning, University of Sydney

After listening to feedback from brokers, a national mortgage manager has revealed that it will soon launch a new mortgage product for overseas buyers.

Better Choice has this year consolidated Iden Loan Services, Future Financial and Pioneer Mortgage Services under the Better Choice brand and is now providing prime residential loans to owner-occupiers and investors, complementing its existing specialist and low doc residential and commercial product range.

Product innovation has been a high priority for the mortgage manager, which distributes exclusively through the broker channel and has eight different funders.

“One of the things that our brokers have told us is that they need a non-resident product,” Better Choice head of relationship management Natalie Sheehan told The Adviser.

“We currently offer a mortgage to expats. As of next week, we will be offering a non-resident product. That’s for foreign investors purchasing residential and commercial real estate in Australia.

“This is something we have been trying to bring to market for a while. We have the funding in place and will be bringing that product to market next week.”

The major banks pulled out of the non-resident lending market in 2015. Only a handful of lenders still offer mortgages to foreign buyers.

But innovative products have been a blessing for Better Choice, which has seen a 70 per cent spike in settlement volumes after expanding its product suite in July.

Investor and interest-only mortgages have been hugely popular as the banks use pricing and policy levers to limit the growth of these products.

Ms Sheehan said: “We definitely listen to what our brokers are telling us and it is clear they are struggling to find a solution for their clients because of the tightening up of servicing.

“Also the tightening up of policy around investment lending. When brokers are looking for products, we are talking to our funders and looking at new product design.

“We have been able to deliver additional choice and convenience to our brokers, who in turn can now offer better solutions to their clients.

“Having multiple funders allows us to choose a range of options to meet our brokers’ needs for a tailored solution for their clients, all under one umbrella. This also allows us to seamlessly transition existing specialist borrowers into a prime solution as their credit profile improves.”

RBA Head of Financial Stability Jonathan Kearns, spoke at Aus-China Property Developers, Investors & Financiers today. He said the Bank has responsibility to promote the stability of the financial system as a whole so carefully monitors property markets because poor commercial property lending and the large stock of residential property debt means risks to financial stability and household resilience.

The high valuation of commercial property increases the potential for a sharp correction and so the risks from commercial property lending. The high level of household mortgage borrowing also brings risks, both for lenders and households.

He also discussed the impact of purchases and financing by foreigner investors and banks. Nationally, purchases by foreign buyers are equivalent to around 10-15 per cent of new construction, or about 5 per cent of total housing sales. But he said, these purchases by foreign buyers do not, on the whole, reduce the supply of dwellings available to local residents and in fact may actually contribute to expansion of the housing stock. However, these purchases by foreign buyers, particularly for investment purposes, are a more recent phenomenon and so their impact on the housing cycle is less clear.

Property and Financial Stability

The property market is important for financial stability for a number of reasons. In the past, banks have experienced substantial losses on their commercial property lending because of its large cycles. Residential property is also important for financial stability because residential mortgages account for a very large share of banks’ lending in Australia. Because of the high value of households’ mortgage debt and housing assets, the property market also has implications for the resilience of households’ balance sheets. Today, I will outline the connection of financial stability with commercial property, and then with residential property.

Internationally, banks experienced substantial losses on their commercial property lending in the financial crisis. In Australia the performance of commercial property lending also deteriorated, but losses were relatively moderate.

Graph 1

However, Australia does have its own history in the early 1990s of large losses on commercial property lending, resulting in individual lenders needing to be rescued and threatening the stability of the financial system. In five years, Australian banks experienced losses of around 10 per cent of their loans, concentrated in their commercial property lending.

This was a classic boom-bust or ‘hog cycle’ story. The second half of the 1980s saw buoyant economic conditions, strong growth in commercial property prices and a large increase in commercial property construction.

A ready supply of credit fuelled the boom. Following bank deregulation and the entry of foreign banks into the domestic market in the mid 1980s, the domestic banks competed to hold on to their market share. Lending standards were lowered and business credit grew by around 25 per cent each year in the second half of the 1980s. With the economy overheating, monetary policy was tightened. Increased interest payments and the economy falling into recession resulted in rising losses on business lending. Office prices halved from their peak as construction initiated in the late 1980s added to supply in an already falling market. Losses mounted at banks with two having to be rescued, and one major bank needing to raise capital.

As notable as this episode seems, it follows a script that had played out before domestically and has since internationally. There are several aspects to commercial property lending that make it inherently risky, and typically more risky than residential mortgage lending. A large share of banks’ commercial property lending is for construction and development, including for large apartment buildings. Construction and development loans tend to be riskier because the property isn’t yet earning rent, things can go wrong in the often complex construction phase, and market conditions can change in the several years or more it takes to complete large projects. Losses can also be greater on lending for commercial property than for residential property because borrowers with a limited liability company structure have less incentive to repay than individual residential mortgage borrowers who face full recourse.

Adding to the risk is that the availability of finance for commercial property has tended to be pro-cyclical. A booming property market has often led to an easing of both lending standards and borrowers’ collateral constraints just as demand for funding is rising. Relative to residential property, the greater ability for funding to come from outside established lenders adds to this cyclicality. Commercial property lending can be syndicated and large individual projects make it easier for new banks to enter the market at a relatively low cost. This cyclicality of lending can accentuate the cycles in commercial property construction and prices.

Foreign investors may add to the cyclicality of the commercial property market if they tend to enter the market when prices have been rising and there are more properties for sale. Alternatively, if foreign investors’ decisions are largely influenced by conditions in their home country rather than the domestic market they may actually moderate the domestic property cycle. Foreign banks direct links to domestic banks tend to be small, so their impact on the domestic financial system is likely to be indirect through an amplification of the credit cycle and property market.

Historically, residential property lending has been less risky for banks than commercial property lending. Indeed, the stress test conducted by APRA indicated that Australian banks have sufficient capital to survive a deep recession and a collapse in the housing market. However, the sheer size of mortgage lending on Australian banks’ books means that residential loan performance is critical to banks’ health and so the stability of the broader financial system. Housing debt is also important for the resilience of the household sector in Australia. The ratio of household debt to income is high in Australia relative to other advanced economies, and has edged higher since the financial crisis.

In Australia, unlike many other countries, individual households also borrow to directly purchase investment properties, which may add to risk. More than one-in-ten tax payers owns an investment property. Most of these are geared, so much so that the majority do not earn positive income for their owners. While these borrowers generally start with smaller loans, and most of the debt is held by high-income households, they have less incentive to pay down their mortgage ahead of schedule because of the tax benefits of debt and so tend to retain higher mortgage balances over the lifetime of the loan.

Despite the high level of mortgage borrowing, various factors mitigate the risks to the financial system. Housing debt is mostly well secured. Limits on the maximum loan-to-valuation for mortgage lending and house price appreciation over time mean that existing borrowers generally have a large amount of equity in their homes. In addition, the ability of Australian borrowers to make excess payments on their mortgage, and that this is a tax effective way for owner occupiers to save, means that borrowers tend to accumulate large pre-payments (‘mortgage buffers’). Close to two-thirds of loans have such pre-payments, which collectively amount to two and half years of scheduled mortgage repayments at current interest rates.

As with commercial property, foreign buyers of residential property could amplify cycles or transmit foreign shocks. Non-residents purchasing Australian real estate as an investment may choose between different countries based on expected returns, which can increase the correlation of the Australian market with other countries. Changes in economic and regulatory conditions in foreign buyers’ home countries can also be transmitted to their demand for Australian property. But if purchases of residential property by foreign buyers mainly depend on conditions in their home country, their participation could actually have a moderating impact on the Australian housing cycle.

Having explained why we take a significant interest in the property market from a financial stability perspective, I would now like to provide an update on recent developments in the commercial and residential property markets and the role that international investors, finance and developers have played.

Commercial Property

One part of the commercial property sector that the Reserve Bank has been watching closely is loans for the development of residential property. The surge in apartments recently completed and under construction in the major cities raises the risk of price falls. The construction of new apartments has been largest relative to the existing stock in Brisbane and inner-city Melbourne, though it is largest in absolute numbers in Sydney.

Prices for other types of commercial property have risen sharply with a strong increase in demand from international investors seeking the relatively high yields available on Australian commercial property. Exceptionally low long-term interest rates globally have pushed up valuations for property and other assets, all the more so because relatively strong and stable global economic growth in the past few years has reduced investors’ perception of the current risks. While there has not been a surge in construction, the run up in commercial property prices raises the risk of a sharp correction, for example if there is a change in sentiment or a pick-up in long term interest rates.

Graph 2

Commercial office markets have been strongest in Sydney and Melbourne with low vacancy rates and rising prices. In contrast, conditions have been weaker in Perth where vacancy rates increased sharply with the downturn in the state economy from the decline in mining investment.

Conditions in retail property markets have also been relatively subdued across Australia. In part, this reflects strong competition in the retail sector from new entrants and online retailers. However, banks have continued to grow their lending for new retail developments and refurbishments with an increased focus on entertainment, hospitality, services and mixed residential.

Overall, Australian banks have tightened their lending conditions for commercial property in recent years. Restrained lending by Australian banks has provided an opportunity for new entrants into the market. Asian banks have grown their commercial property lending sharply, more than doubling their market share in just two years, although it remains relatively small. This strong growth in commercial property lending by Asian banks is reminiscent of European banks’ growth in the lead up to the financial crisis. However, whereas Australian banks eased their lending standards in that pre-crisis period in order to compete, this time Australian banks do not appear to have eased lending standards.

Graph 3

Residential Property

The Australian residential property market has been strong in the post-financial crisis period as interest rates have been kept low to support economic activity and to boost low inflation. Since 2009, national housing prices have risen by around two thirds and growth of housing credit has outpaced that of incomes. By 2014, concerns grew about the risks from an increase in riskier types of lending, including interest-only loans and investor lending at high loan-to-valuation ratios as well as rising household indebtedness. In response to these concerns, the Australian Securities and Investments Commission (ASIC) increased its scrutiny of lending practices and APRA implemented several macro prudential measures in late 2014 and then again in early 2017, on both occasions after consultation with the Council of Financial Regulators, which the Governor of the Reserve Bank chairs. There are several aspects to these regulatory measures. For each authorised deposit-taking institution (ADI), the growth of investor housing lending has been capped at 10 per cent. Interest-only loans can be no more than 30 per cent of new mortgage lending. In addition, APRA has been monitoring high loan-to-valuation mortgage lending and instructed lenders to pay closer attention to loan serviceability criteria, such as the interest rate buffer applied to the current low mortgage rates and borrowers’ expenses.

These measures have played a role in reducing the build up in risks from household borrowing. Lenders responded to the restrictions by increasing their interest rates for interest-only loans and investor lending. In response, the share of new loans that are interest-only has been falling, and overall investor credit growth has remained below the 10 per cent threshold. Many existing borrowers have also switched their interest-only loans to principal-and-interest loans and there has been a decline in the share of new loans at high loan-to-valuation ratios.

While riskier types of lending have moderated, and investor credit growth has slowed, the pace of overall housing credit growth has been fairly stable this year as borrowing by owner-occupiers has picked up. Conditions in the housing market have eased, particularly in Sydney where prices had experienced strong growth and are particularly high, possibly giving lending restrictions greater impact in Sydney. In Melbourne, conditions remain stronger than in other capital cities. On the other side of the country, and at the other end of the spectrum in terms of housing market conditions, the Perth housing market remains weak. Prices have fallen gradually over the past two to three years, with rents also falling as the rental vacancy rate has increased to its highest level since 1990.

The strong demand driving housing price growth reflected not only low interest rates but also strong population growth. With rising demand and prices, dwelling investment increased strongly. A notable feature of the recent dwelling construction cycle has been the marked increase in the share of higher density construction, a helpful response to the shortage of well-located land in Australia’s large cities. Approvals for new higher density dwellings went from being less than half those of detached dwellings less than a decade ago to being almost on par in recent years. But the longer time to build higher-density dwellings than detached houses increases the risk that a large number of new dwellings could be completed just as the housing market turns down, so amplifying the housing cycle.

Graph 4

This surge in apartment construction has been largest in Sydney, but has also been notable in Melbourne. While the number of apartments being built in Brisbane has been smaller compared to its population, it has been greater relative to the existing stock of apartments. Peak apartment completion in Brisbane is expected to occur this year, capping a three-year period in which the number of apartments has increased by over one-third from the stock in 2015. Perth has also seen strong growth in a relatively small stock of apartments.

This change in the composition of the housing stock is resulting in a rebalancing of relative prices, with prices for detached dwellings growing faster than those for apartments in the major cities over the past five years. In the weaker housing markets of Brisbane and Perth, this has seen apartments experience small price falls in recent years. To date, despite valuations for some apartments at settlement being lower than the purchase price off the plan there have not been widespread reports of higher rates of settlement failure or any notable increase in arrears or losses for banks.

Purchases by foreign buyers have received considerable focus in recent years. Non-residents are able to purchase newly constructed dwellings in Australia, while temporary residents, such as those in Australia for work or study, are able to purchase an existing dwelling for their primary residence. It has been hard to get a firm estimate of how large these purchases are, but drawing on a range of sources, it seems that, nationally, purchases by foreign buyers are equivalent to around 10-15 per cent of new construction, or about 5 per cent of total housing sales. The share of new construction purchases is highest in Melbourne and Sydney. It is also higher for apartments, but it is still only perhaps around one-quarter of newly built apartments. Many foreign buyers come from China, seemingly around three-quarters. Purchases of new properties by foreign buyers have eased over the past year, reportedly because of stricter enforcement of Chinese capital controls and tighter access to finance for foreign buyers.

Purchases by foreign buyers do not, on the whole, reduce the supply of dwellings available to local residents and in fact may actually contribute to expansion of the housing stock. Foreign buyers in Australia for work or study would have been renting if they did not purchase. Other foreign buyers rent the property as an investment and so contribute to the rental stock. Also, there are some new developments that only proceed because they get high pre-sales from foreign buyers.

The strength of the Australian property market, and the participation by foreign buyers, has also enticed some foreign developers to Australia for specific projects, but overall they remain a small part of the market. Foreign banks also have a very small role in residential property lending in Australia.

Given their significance for financial stability, the Reserve Bank carefully monitors property markets. History has taught us that commercial property lending can result in substantial losses for banks. And the large stock of residential property debt means that it too is important for financial stability and household resilience.

The high valuation of commercial property, which is common to many other assets, increases the potential for a sharp correction and so the risks from commercial property lending. The high level of household mortgage borrowing also brings risks, both for lenders and households.

Purchases and financing by foreigner investors and banks have been prominent in the current commercial property cycle. We have seen this before and are well aware of the impact this can have on the cycle. The increased purchases of dwellings by foreign buyers, particularly for investment purposes, are a more recent phenomenon and so their impact on the housing cycle is less clear.

APRA has investigated commercial property lending standards to ensure these are not eroded, while measures by APRA and ASIC aim to reduce the riskiness of new residential lending. And the Reserve Bank, with its mandate for overall financial stability, will continue to closely monitor risks from property markets and lending.

The legislation to tighten some aspects of investment property, and levy a charge on vacant foreign owned property has been passed in the Senate.

The legislation prevents property investors from claiming travel expenses when travelling between properties, as well as tightening depreciation on plant and equipment tax deductions.

Foreign owners will be charged a fee if they leave their properties vacant for at least six months in a 12-month period, in an attempt to release more property to ease supply. The latest Census showed that there are 200,000 more vacant homes across Australia than there were ten years ago.

Introduced with the Foreign Acquisitions and Takeovers Fees Imposition Amendment (Vacancy Fees) Bill 2017, the bill amends the: Income Tax Assessment Act 1997 to: provide that travel expenditure incurred in gaining or producing assessable income from residential premises is not deductible, and not recognised in the cost base of the property for capital gains tax purposes; and limit deductions for plant and equipment assets used for producing assessable income from residential premises to when the asset was first used for a taxable purpose; Foreign Acquisitions and Takeovers Act 1975 to implement an annual vacancy fee on foreign owners of residential real estate where residential property is not occupied or genuinely available on the rental market for at least six months in a 12-month period; and Taxation Administration Act 1953 to make consequential amendments.

Lenders eyeing up wealthy foreigners currently locked out of the banks and developing new processes to combat fraud

Non-resident lending could be set for a return as non-bank lenders become increasingly interested in the sector.

According to La Trobe Financial’s vice president Cory Bannister, “non-resident is a great example of a product that suits non-banks generally.” Speaking at MPA’s Non-Banks Roundtable last week, Bannister said that the low LVRs, low arrears and high net-worth associated with non-resident borrowers made them similar to prime clients.

The banks largely pulled out of non-bank lending in early 2016, citing fears of fraud. However, Bannister believes non-banks can operate safely: “we believe it requires manual assessment and that’s the single characteristic which meant the banks had to step out of that space.”

La Trobe, who have lent to non-residents on and off over the past year, have an international desk with bilingual staff which help ‘weed out’ fraudulent cases.

Growing niche in expat lending

Two other lenders at the panel were already lending to Australian expats: Better Mortgage Management and Homeloans Ltd.

Expats often struggle to find finance at the banks because they earn income abroad and in foreign currencies. BMM’s managing director Murray Cowan told the panel that “I think the expat sector may have been unfairly characterised as the same as non-residents and that might have created a bit of an opportunity for us there.”

Aaron Milburn, director of sales and distribution at Pepper Money, said that although Pepper doesn’t currently lend to non-residents “I wouldn’t discount it for the future.” He noted that Pepper’s international spread helped provide the infrastructure to do so.

Can non-banks handle non-residents?

Non-banks at the panel were concerned however that a return to non-resident lending could lead to a surge in business.

In fact, it could cause volumes to triple ‘overnight’, suggested Homeloans and RESIMAC general manager of third party distribution Daniel Carde. The panel broadly agreed that such a surge would be difficult to deal with. “No business is set up for triple volumes,” argued Liberty’s national sales manager John Mohnacheff “we can probably handle 5-10% variability”.

A note of caution was sounded by FirstMac founder Kim Cannon. “The RBA wants to stop [non-residents buying property]; they don’t want to cure it,” he told the panel. He warned that surge in non-residents getting financed by non-banks would be “treading on dangerous ground” with regulators.

According to new analysis by Credit Suisse, demand for housing from Chinese buyers remains strong, especially the purchase of new developments, and this will put a floor under property especially in the main urban centres of Sydney and Melbourne.

As reported in Business Insider, new restrictions on foreign investors are unlikely to stop the flow of housing demand from China, according to Credit Suisse analysts Hasan Tevfik and Peter Liu.

And crackdowns on capital outflows by Chinese authorities appear not have slowed China’s appetite for Australian property, the pair say.

“We calculate foreign buyers are acquiring the equivalent of 25% of new housing supply in NSW, 17% in Victoria and 8% in Queensland. Almost all of this is from China,” the analysts said.

Updated to June, the figures show that foreign buyers are snapping up Australian property at an annualised rate of $10 billion per year across NSW, Victoria and Queensland.

That’s only a small percentage of Australia’s $6.7 trillion housing market, but importantly, it makes up a significant percentage of the demand for new housing supply.

Nearly a third of new housing stock being built in NSW is being bought by foreigners. Obviously not all of that is for new dwellings, but the vast majority would be.

And while much has been made of the crackdown on investor-funds leaving China, the Credit Suisse research shows the actual impact has been minimal.

Here are Tevfik and Liu’s comments :

In December 2016, the Chinese authorities introduced new and stronger capital controls to slow money flowing out of the middle kingdom. Our tax receipt data help measure how effective these controls have been — and it seems they haven’t been. In NSW, where we have three complete (and reliable) quarters of tax receipt data, we can see foreign demand for property has so far hovered around $1.4 to $1.6bn per quarter.

After concluding that China’s crackdown doesn’t appear to be stemming off-shore capital flows, Tevfik and Liu also noted that Chinese investors are cashed up and ready to spend.

There are currently 1.6 million US dollar millionaires in China, and that converts to shared wealth of a whopping $13 trillion – around twice the size of Australia’s housing market.

“As our property market becomes more global perhaps we should be concentrating less on Australian incomes as a measure of buying power and more on wealth creation in the Asian region,” the analysts said.

So, what factors could stem the seemingly invevitable flow of capital from Asian markets into Australian property?

Tevfik and Liu highlighted the potential impact of recent tax increases on foreign investors introduced by Australian states, as well as the impact from a devaluation of the Chinese currency.

Victoria and Queensland also impose additional taxes on foreign investors of 7% and 3% respectively, calculated as a proportion of the purchase price.

However, they said that past examples from other international suggest the impact on house prices will be small.

“The introduction or increase of a tax on foreign buyers seems to slow demand to a point where property prices decelerate, but it does not cause housing values to contract,” Tevfik and Liu said.

This chart shows the impact on house prices in other international markets after the implementation of tax increases on foreign investors.

“Based on the experience of other cities around the world, we do not believe the recent increase in taxes by NSW will cause property prices to contract,” the pair said. Although they added that Chinese investors are an easy target for Australian state governments, and didn’t rule out further rate increases in the future.

A more likely scenario to reduced demand, the analysts said, would be a devaluation of China’s currency, the renminbi.

“From our many and various discussions with Chinese investors and companies, there is a consensus view that the renminbi is set to depreciate further from here. If and when it does the buying power of Chinese investors will diminish.”

Tevfik and Liu noted that the renminbi has been broadly depreciating since 2014. In that context, they added that Chinese policy-makers are focused on stability ahead of the 19th Communist Party Congress later this month, but said movements in the currency after that will be worth monitoring.

In summary, the two analysts dispute recent reports suggesting foreign investor demand will slow. On the contrary, “we forecast these flows to continue at a strong pace and will serve to cushion the downside in activity and prices”, they said.

“It’s different this time. While we acknowledge residential investment and house price inflation are set to moderate we don’t think there will be a collapse. The foreign buyer has never before been as an important driver of the Australian housing market as she is now.”

According to the South China Morning Post, cash-rich Chinese firms – the big spenders in the global property market in the past four years – are getting cold feet as Beijing tightens controls on outbound investment.

“Requests for overseas acquisitions are already drying up,” said Paul Guan, a partner with global law firm Paul Hastings who advises Chinese institutional investors on overseas real estate.

“Business owners all know the Chinese government has sent a clear signal this time that they want to curb overseas investment in the property sector,” Guan said.

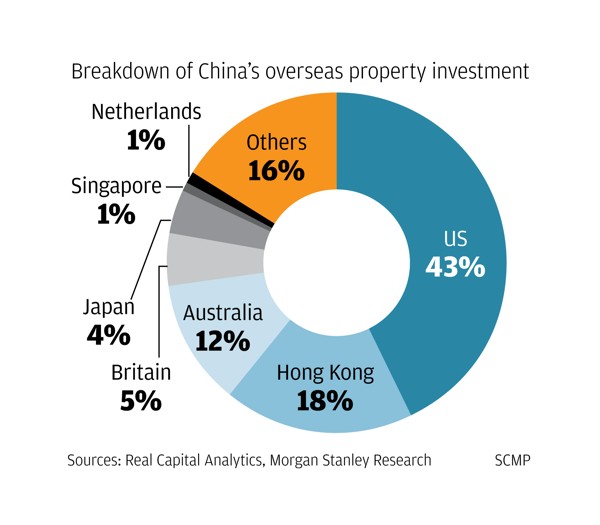

The move will put pressure on prices in key property markets from New York to London. The top three overseas destinations for Chinese property investors in 2016 were the United States, Hong Kong and Australia, while pending deals have accumulated mainly in Britain and the US over the past six months, according to Real Capital Analytics.

Chinese were the biggest foreign investors in US and Australian real estate last year, accounting for 25 per cent of deals in the US and 26 per cent in Australia.

They also accounted for 25 per cent of all central London commercial property acquisitions in 2016, while some 80 per cent of residential land sold in Hong Kong so far this year was bought by Chinese firms, according to data from Morgan Stanley. Chinese investment in the city has quadrupled since 2012, the financial services firm said.

“Transaction volumes will definitely go down in the hot destinations, and property prices could also be affected,” said Hans Kang, chief investment officer of InfraRed NF Investment Advisers.

On Friday, the State Council said it would restrict overseas investment in a number of areas including property, hotels, the film industry and other forms of entertainment, and sports clubs. Investors would have to seek special approval from the regulators for such ventures.

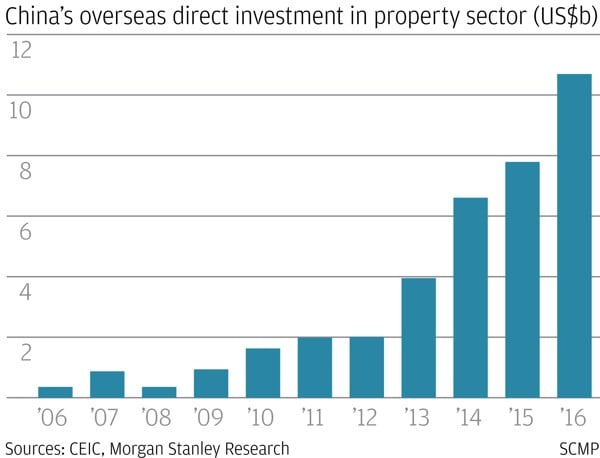

Outbound investment by Chinese companies has surged since 2013, with Beijing pushing for more of them to go global and as foreign exchange reserves continued to pile up.

But the government has since 2015 become worried about the scale of capital outflows, particularly in property, at a time when the yuan has sharply depreciated and there are fears of a domestic property bubble, creating problems for the country’s balance of payments.

Added to those fears are companies that borrow money on mainland China to buy overpriced overseas assets, which runs counter to President Xi Jinping’s deleveraging efforts.

“That could hit the financial stability of China’s banking system if there are any fluctuations in outside markets,” Kang said.

“Chinese buyers accounted for 25 per cent of all central London commercial property acquisitions in 2016, according to Morgan Stanley.

In past months, policymakers have tightened regulations on “irrational overseas investment” and ordered banks to check the credit exposure of a number of aggressive dealmakers including Wanda, Fosun International, HNA Group and Anbang Insurance Group.

All of those companies had been on a shopping spree in overseas property markets in recent years.

Anbang, for example, made headlines in 2014 with its US$2 billion purchase of New York’s Waldorf Astoria hotel.

HNA Group, which owns Hainan Airlines, meanwhile bought a 25 per cent stake in Hilton Worldwide Holdings for US$6.5 billion last year. It has also paid a record HK$27.2 billion for four residential sites in Hong Kong since November.

And Wang Jianlin, who runs one of China’s biggest property developers, Wanda, has invested some A$2 billion (US$1.58 billion) in two mega mixed-use projects in Australia since 2014.

Wang Jianlin, who runs Wanda, has invested US$1.58 billion in two mega mixed-use projects in Australia since 2014.

But now those dealmakers find themselves under intense government scrutiny, their ambitious global plans have come to a screeching halt and their focus is shifting back to the domestic market.

Wang told financial media outlet Caixin last month that his company would “actively respond to the state’s call and divert its main investments to China” after it sold off US$9.3 billion of assets to rivals in order to repay debts.

The retreat is already being felt in global markets. Outbound property investment by mainland Chinese firms was down 82 per cent in the first half from a year ago – and it’s expected to plummet 84 per cent for the whole year to US$1.7 billion, according to Morgan Stanley. The total investment in 2016 was US$10.6 billion.

That trend will create headwinds for prices in Hong Kong, the US, Britain and Australia over the medium term – especially for office assets in Manhattan, central London and Hong Kong, which is the most exposed, it said.

Guan from the law firm said prices in the high-end residential market in New York were also likely to be hit by the loss of Chinese buyers.

For the first time since October 2012, no contracts worth over US$10 million were signed in the city last week, according to data from Olshan Realty.

Others were more positive, and believed the impact of the restrictions would be limited to related markets, which would continue to be shaped by broader macroeconomic trends and fundamentals.

“Fortunately, the United States’ key markets are still desirable enough that without one particular flow of capital from a region, the impact should be nominal if all economic and market conditions are normal and healthy,” said Andrew Feldman of New York-based real estate agency Triplemint.

Added to that, many Chinese companies had already moved currency overseas and could continue to issue debt or equity through offshore platforms if they wanted to invest in property, according to Ben Briggs, executive vice-president of Briggs Freeman Sotheby’s International Realty based in Xiamen.

“They will just do the investments in a more quiet and sophisticated way,” Briggs said.

Thomas Lam, senior director of Knight Frank, agreed that the restrictions would not stop Chinese companies from investing abroad.

“In the longer term, going global will continue and it will remain an essential means for Chinese companies to diversify risks and secure sustainable returns,” Lam said.

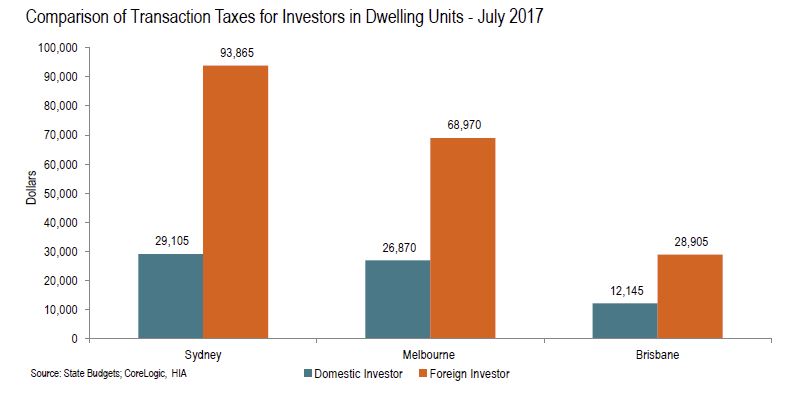

The HIA says recent changes to stamp duty in NSW mean that foreign investors now pay almost $100,000 in transaction taxes to acquire a standard apartment in Sydney – almost four times as much as local buyers.

This remarkable finding is contained in the latest Stamp Duty Watch report which has just been released by the Housing Industry Association.

The average stamp duty bill in Australia paid by resident owner occupiers is also up by 16.4 per over the year to $20,725, even though dwelling prices increased by just 10.5 per cent .

On the owner occupier side, stamp duty drains family coffers of $107 each and every month over a 30-year mortgage term. For owner occupiers, the typical stamp duty bill now amounts to $20,725 – an increase of some 16.4 per cent on a year ago.

Shelling out so much in stamp duty drains the household piggy bank of vital funds for their home deposit. Families are then forced to take out larger mortgages and incur heavier mortgage insurance premiums.

Foreign investors are a vital component of rental supply in cities like Sydney and Melbourne. With rental market conditions now so tight in Australia’s two biggest cities, should we really be placing more and more barriers in the way of new supply?

New financial year brings additional charges and regulations as Treasury predicts number to more than halve.

Capital controls, bank lending standards and foreign buyer taxes could “wind back the clock to 2015”, international real estate portal Juwai.com has warned.

The new financial year has hit foreign buyers with increased stamp duty – 8% in NSW and 7% in Victoria – as well as a new vacancy tax and 50% cap on off-the-plan properties sold to non-residents.

Lending to foreign buyers remains extremely tight, brokerage Alliance Mortgage Solutions told MPA with just a handful of non-banks continuing to lend to borrowers at relatively high rates. Additionally, the fall in the Chinese renminbi has made Australian property relatively more expensive.

Speaking in May, Australian Treasury Secretary John Fraser noted that “the number of all foreign investment applications for residential housing has fallen from 40,000 in 2015 16 to an expected 15,000 in 2016 17.”

Australia is falling behind globally

The warning by Juwai.com chief of operations Sue Jong was part of an otherwise optimistic report on Chinese investment in real estate abroad, which hit $133.7bn in 2016

Australia remains the second most popular destination for real estate, after the USA, but Jong observed that “investment flows have decreased markedly from their peak, while remaining strong by historic standards.”

Globally, Juwai.com expects 2017 to be one of the top three years on record for Chinese investment, arguing that there is still plenty of pent-up demand to invest in China. Relative to population size, Chinese investors own less real estate than Slovenians.

It’s far from guaranteed that the Australian Government’s measures will reduce foreign buyer demand. Writing in MPA, Juwai.com’s Australian head Jane Lu suggested fewer than 5% of their clients would be hit by the tax, many of which were wealthy enough not to care.

Brokers diversifying away from the sector

A further fall in foreign buyer numbers would be a further nail in the coffin for brokers working with this group.

Back in 2014, industry rankings such as MPA’s Top 100 Brokers report were dominated by brokers working with foreign buyers.

Whilst many of these brokers remain in the industry, they have had to make major changes; Alliance Mortgage Solutions, one of this year’s MPA’s Top 10 Independent Brokerages, saw 35% of their business affected and have introduced client fees in response.

Other Top 10 brokerage N1 Loans, part of ASX-listed N1 Holdings, has diversified into real estate, using real estate agents to drive customers to their brokers. “We’ve had this plan for 18 months to diversify, CEO Ren Wong told MPA “our aim is to have mortgage broking revenue less than 50% of the overall revenue competition.”

Sydneysiders are concerned that foreign investors, and particularly Chinese real estate investors, are pushing up housing prices, according to survey findings published this month. A majority believed foreign investors should not be allowed to buy residential real estate in Sydney.

The federal budget was the government’s latest attempt at navigating a policy solution that supports its pro-foreign investment position while responding to public concern about housing affordability in Australian cities.

China’s government is also searching for a policy solution to restrict the large amount of capital that’s flowing out of the country. But the Chinese crackdown “doesn’t appear to be working”.

We surveyed almost 900 Sydneysiders to investigate their views on foreign real estate investment. The effectiveness of government regulations on foreign investment and investors was a major concern for respondents.

Views on government regulations

The survey obtained the views of people aged over 18 living in the Greater Sydney region. They were asked about housing affordability, foreign investment, the drivers of Sydney housing prices, and perceptions of Chinese investors specifically.

Support for the government’s regulation of foreign investment in housing was weak. Only 17% of respondents thought it was effective.

Almost 56% of participants believed foreign investors should not be allowed to buy residential real estate in Sydney. Only 18% believed this should be permitted.

More than 63% of participants disagreed that the “government should encourage more foreign investment in greater Sydney’s housing market”. Only 12% of participants agreed with this.

These views stand in stark contrast to the government’s geopolitical support for foreign investment in Australia.

Views on foreign investors

There is little fine-grained data about the impacts of foreign capital and investors on specific neighbourhoods and developments in Australian cities. Therefore, we did not set out to compare public attitudes against the limited empirical evidence on the effects of foreign real estate investment in Sydney.

What’s significant about the survey results is that Sydneysiders have strong views on foreign investment, despite the absence of reliable evidence. Participants’ concerns about foreign investors and investment were consistent with their concerns about the government’s foreign investment rules.

Around 63% of Sydneysiders identified the Chinese as the heavyweights of foreign investment. This is likely to be accurate, given the concentration of Chinese investment in Sydney and Melbourne.

When presented with the statement “I welcome Chinese foreign investors buying properties in my suburb”, more than 48% of participants disagreed.

Other studies, however, have shown the potential for public confusion between domestic Australian-Chinese and international Chinese buyers.

Views on the drivers of housing prices

Respondents were asked to choose up to three drivers of house prices based on their understanding of Sydney’s housing market. By far the most commonly nominated driver of house prices (64% of respondents) was foreign investors buying housing.

Roughly one in three survey participants saw low interest rates (37% of respondents) and domestic home owners (32%) and investors (32%) as the drivers of higher housing prices. Local housing analysts generally agree with this.

But more than three in four participants (78%) agreed with the statement:

Foreign investment is driving up housing prices in greater Sydney.

When framed inversely, as “Foreign investment has no impact or very small impact on greater Sydney’s housing market”, more than two-thirds of participants (68%) disagreed with the statement.

Only 6% of our participants disagreed that foreign investment was increasing real estate prices. Around 11% agreed that foreign investment had no or minimal impact.

Views on housing supply and affordability

We expected people to report that foreign people and capital are driving up housing prices and making it more difficult for Australians to compete in the housing market. But we were surprised by the findings about Sydneysiders’ views on foreign capital and housing supply.

A strong message from the real estate and property development industries is that foreign investment increases housing supply, which in turn puts downward pressure on prices.

Politicians and lobby groups argue this will help improve housing affordability in major Australian cities. But many housing analysts argue that this supply solution does not stack up for purchases made by either foreign or domestic investors.

It seems that Sydneysiders don’t accept the real estate industry message about foreign investors increasing housing supply, and therefore helping to ease housing affordability pressures.

When asked if “Foreign investment can help increase housing supply in greater Sydney”, 48% of participants disagreed with the statement. Another 25% “neither disagreed or agreed”.

An unresolved policy dilemma

The government’s dilemma is how to manage foreign investment alongside an increasing housing affordability problem in major Australian cities.

This month’s federal budget included a crackdown on foreign investors, but the government still supports foreign real estate investment.

Our survey results support other studies that suggest this pro-foreign investment stance must be accompanied by strategies to protect intercultural community relations. This must happen alongside efforts to improve housing affordability.

Authors: Dallas Rogers, Senior Lecturer, Faculty of Architecture, Design and Planning, University of Sydney; Alexandra Wong, Engaged Research Fellow, Institute for Culture and Society, Western Sydney University; Jacqueline Nelson, Chancellor’s Postdoctoral Research Fellow, University of Technology Sydney