New housing legislation has been introduced to Parliament to deliver the “single biggest investment” in affordable and social housing in a decade. States and territories tackling their own housing supply crises will have greater help via new federal bills introduced to Parliament on Thursday (9 February).

Under the umbrella of three new bills — the Housing Australia Fund Bill; National Housing Supply and Affordability Council Bill; and Treasury Laws Amendment (Housing Measures No. 1) Bill — the government has delivered “the single biggest investment in affordable and social housing in more than a decade.

But as we discuss the proposals are small and driven by a Neo-liberal mentality. Does not address the fundamentals of housing affordability but plays around the edge for political advantage. We need better!

http://www.martinnorth.com/

Go to the Walk The World Universe at https://walktheworld.com.au/

We unpick the “supply-side” problems which are often blamed for high home prices, and in the light of a recent report, find that Land Banking is a significant issue, as large players hold on to land parcels to exploit prices rises. This means you cannot solve affordability by changing planning rules! In addition, there is significant information asymmetry and financial players benefit from the current arrangements – while State and Federal Governments look the other way. Go to the Walk The World Universe at https://walktheworld.com.au/

The report is based on a survey that collected responses from just

over 3,600 Australians across three states – New South Wales, Queensland

and Western Australia – with 75% of responses from metropolitan

locations and 25% from regional areas.

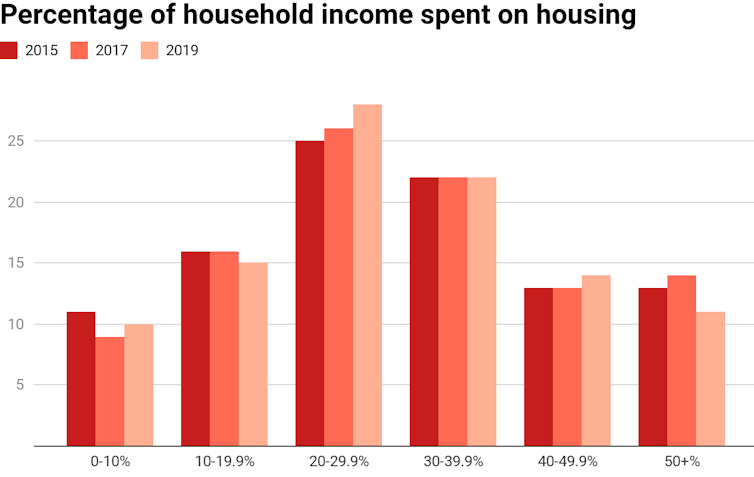

Similar surveys were conducted in 2015 and 2017. This allows for comparisons across the three periods.

Housing costs

The survey asked respondents to estimate the proportion of their

gross income spent on housing costs. Around 40% of all households

reported living rent/mortgage-free (outright owners, young adults living

with parents etc). The chart below shows the distribution across six

bands for the remaining households.

Just under half reported paying over 30% of their income on rent or

mortgage costs. We see little change over the three surveys, although

slightly fewer households are now paying more than 50%.

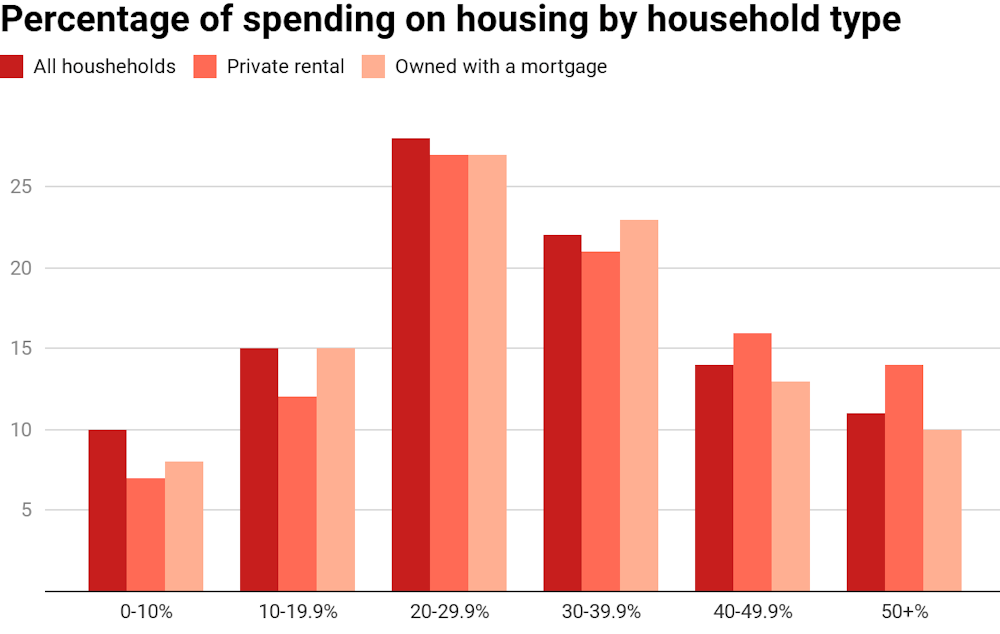

For 2019, slightly more private renters pay over 30% compared to

owners with a mortgage, but renters are more likely to be in the highest

burden groups. The main difference is 60% of renters are forced to take

on these high housing costs while 72% of owners take them on by choice.

Households are very sensitive to changes in housing costs: 40% of

those surveyed said a 10% increase in costs would have a major impact on

their financial position. The expected impact was greater for renters

than owners with a mortgage (44% compared to 38%). A 3% increase in the

mortgage interest rate would have a major impact on the financial

position of 63% of owners.

The impact of sustaining such costs can be severe: 46% said high

housing costs affected their mental health and 30% their physical

health.

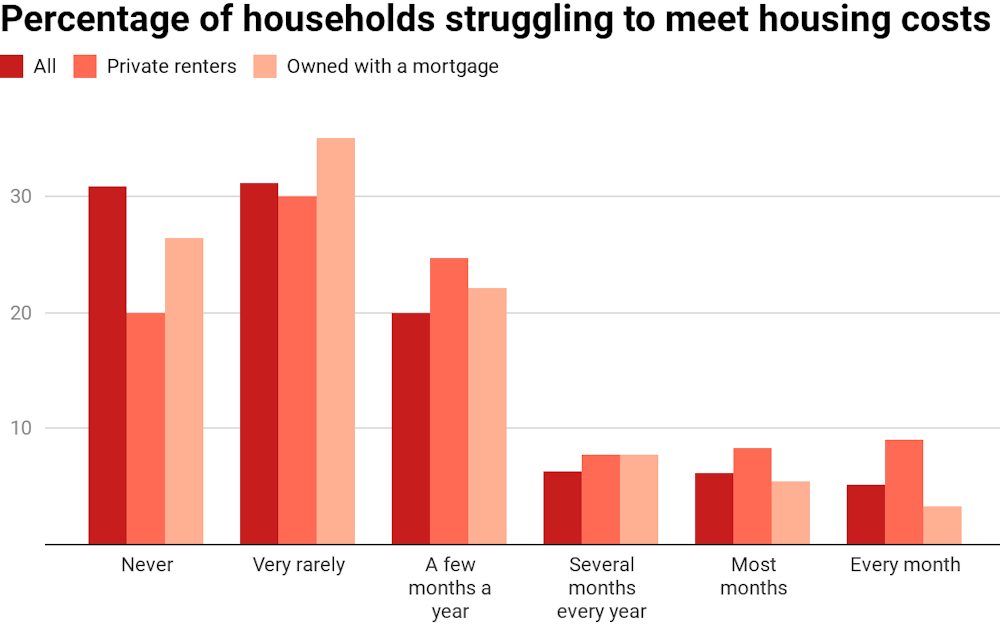

The chart below shows the proportions of households struggling to

meet their housing costs. Again, we see only slight improvement across

the three surveys.

Among all households, 37% reported difficulty regularly meeting

housing costs (at least a few months a year). This rose to around half

of all renters and low-income households and to 56% of one-parent

families.

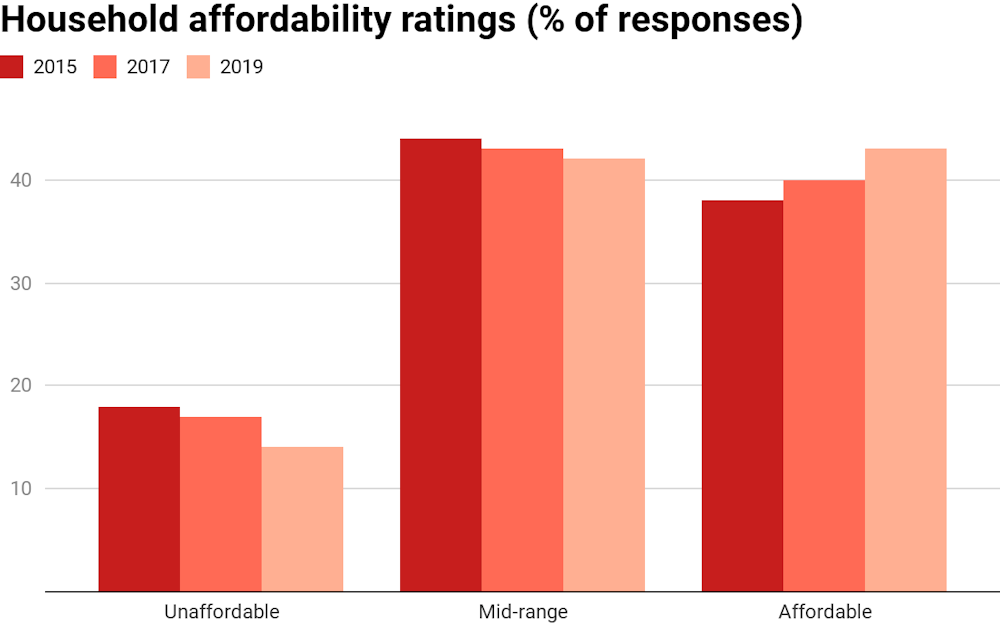

Housing affordability is not just about paying the rent or mortgage.

It also includes running costs such as utility bills and maintenance.

The survey asked respondents to rate the affordability of their housing

on a ten-point scale and the results were collated into three ranks.

The chart below shows some improvement across surveys in the

proportions of households rating their housing as affordable. These

households are largely outside the lower-income groups.

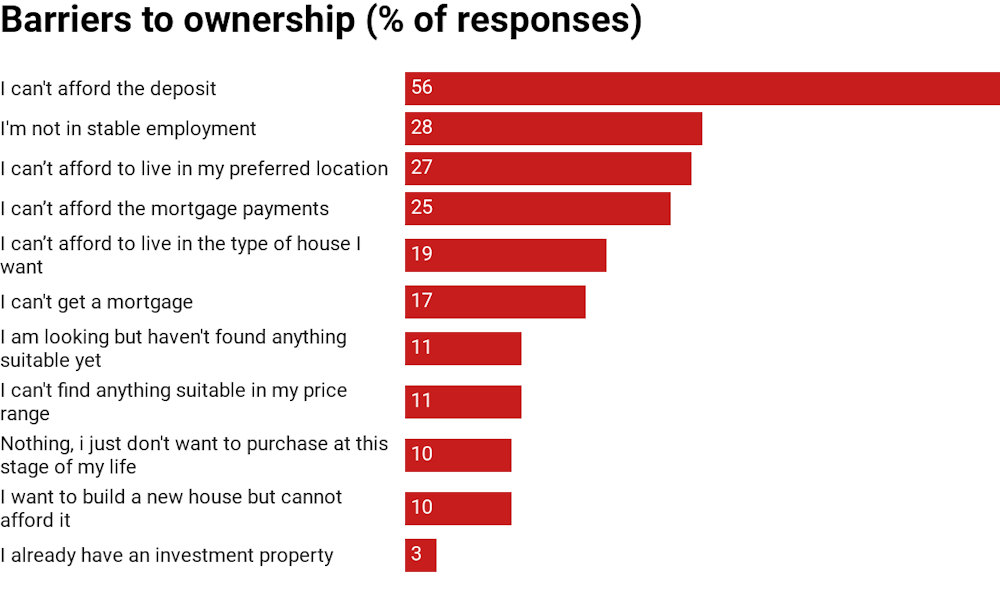

The deposit gap is the biggest barrier for potential home buyers,

almost double the importance of the next barrier – a lack of stable

employment. Other barriers largely revolve around a lack of suitable

stock.

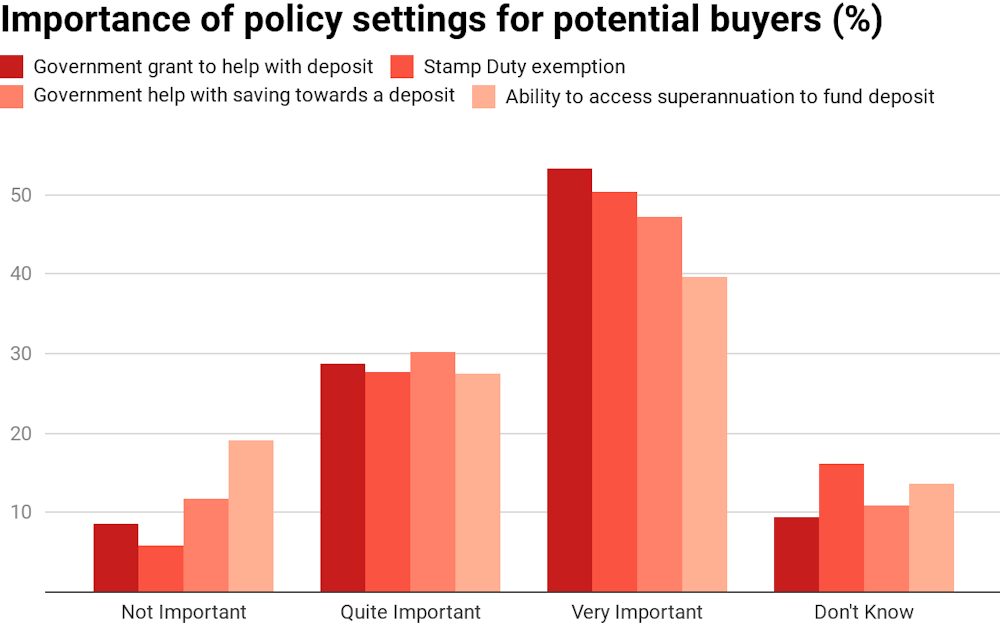

Help for first home buyers is now embedded. Around three-quarters of

potential purchasers regard government help through the various

mechanisms shown in the chart below as quite or very important while

two-thirds would like access to their superannuation to fund a deposit.

For those without help from the “bank of mum and dad”

these policies can mean the difference between home ownership and many

more years living with parents or renting. It is difficult to see how

such help can be equitably removed from the housing system.

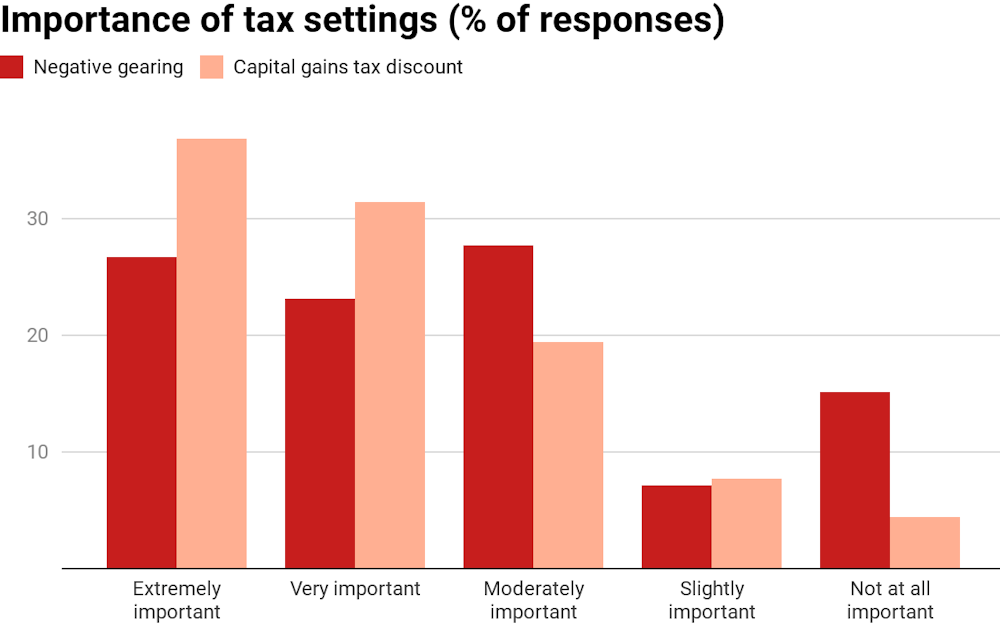

The survey included a number of questions for respondents owning an

investment property and for those thinking about buying one. The capital

gains tax (CGT) discount was more important to investors that negative

gearing. However, only 15% regarded the latter as unimportant.

Around a quarter of investors said they wouldn’t have bought their

property if negative gearing were not available and CGT was half its

current rate. And 28% said they would not buy an investment property in

the absence of negative gearing.

Such results suggest a modest impact on investment demand which could

impact on local housing markets, depending upon the balance between

investors and owner-occupiers in those markets.

Policy development

Between the 2017 and 2019 surveys, house prices and rents fell in large areas of the three states. Yet our analysis shows little impact on affordability for low-income households. Intervention is required to deliver housing affordable to such households.

Large numbers of households are struggling with their housing costs, and not meeting these costs can result in homelessness. This points to the need for more investment in public and community housing.

Ultimately, there is a mismatch between incomes and house prices. Major housing system reform is necessary to redress the balance.

In the meantime, a large and sustained supply of subsidised rental housing and a secure private rental sector that offers a real alternative to ownership are essential components of any future Australian housing system.

Authors: Steven Rowley, Director, Australian Housing and Urban Research Institute, Curtin Research Centre, Curtin University; Alan Duncan, Director, Bankwest Curtin Economics Centre, and Bankwest Research Chair in Economic Policy, Curtin University; Amity James, Senior Lecturer, School of Economics, Finance and Property, Curtin University

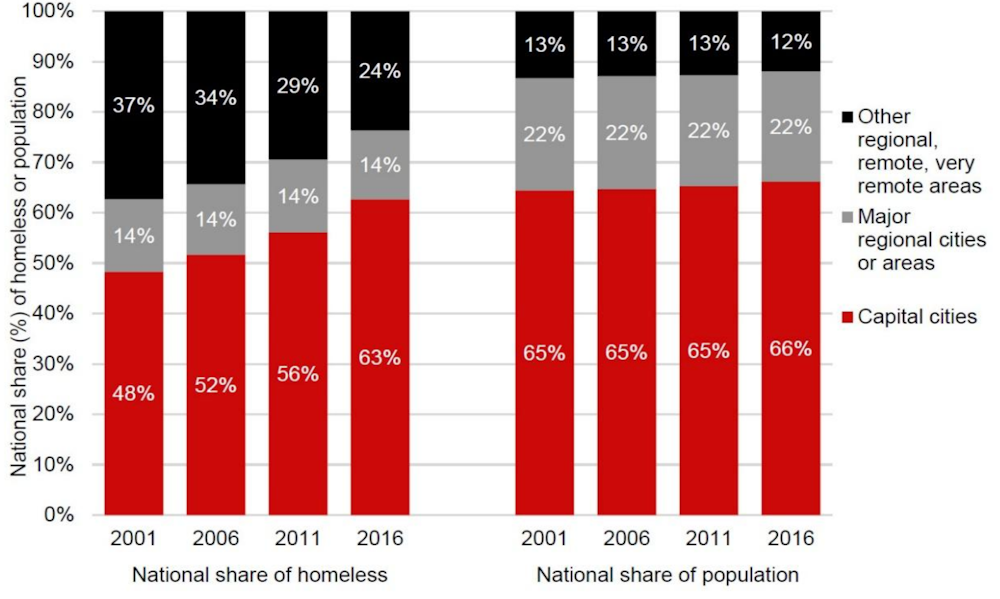

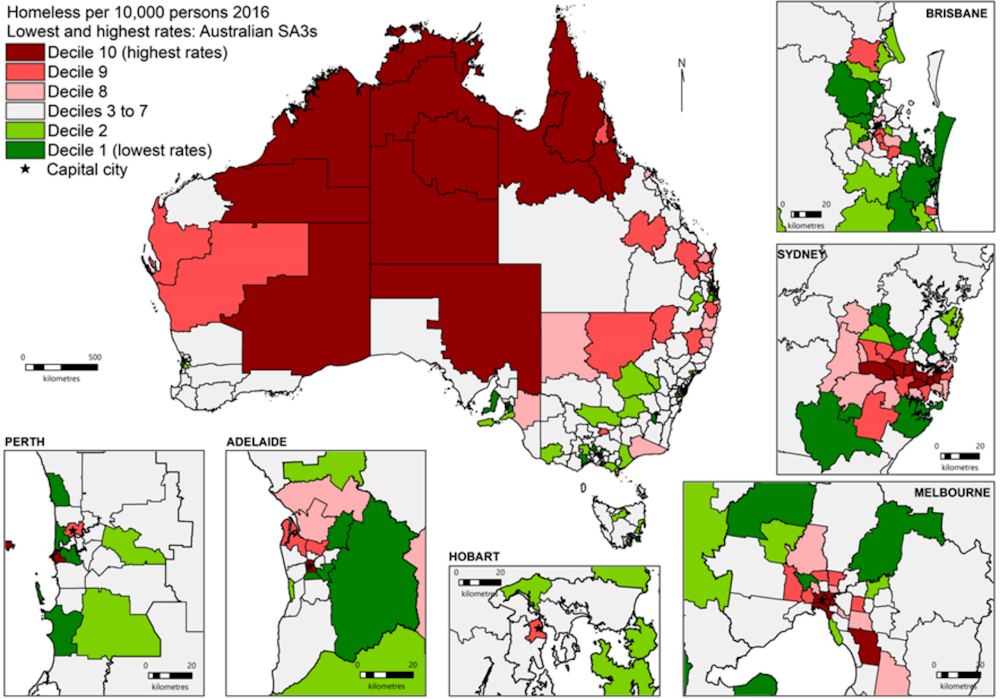

Homelessness has increased greatly in Australian capital cities since 2001. Almost two-thirds of people experiencing homelessness are in these cities, with much of the growth associated with severely crowded dwellings and rough sleeping.

Homelessness in major cities, especially severe crowding, has risen

disproportionately in areas with a shortage of affordable private rental

housing and higher median rents. Severe crowding is also strongly

associated with weak labour markets and poorer areas with a high

proportion of males.

These are some of the key findings of our Australian Housing and Urban Research Institute (AHURI) research released today.

People counted as homeless

on census night live in: improvised dwellings, tents or sleeping out

(rough sleeping); supported accommodation; staying temporarily with

other households (i.e. couch surfing); boarding houses; temporary

lodging; or severely crowded conditions.

How has the geography of homelessness changed?

Nationally, 63% of all homelessness is found in capital cities. That’s up from 48% in 2001.

Shares (%) of homelessness and population by area type

At the same time, homelessness has been falling in remote and very

remote areas. However, it still remains higher in these areas per head

of population.

Homelessness is also becoming more dispersed across major cities.

In Sydney, a corridor of high homelessness rates stretches from the

inner city westward through suburbs such as Marrickville, Canterbury,

Strathfield, Auburn and Fairfield (more than 30km from the CBD).

In Melbourne, high homelessness rates are found in Dandenong (around

25km southeast of the CBD), Maribyrnong and Brimbank to the west,

Moreland and Darebin to the north and Whitehorse to the east, about 15km

from the CBD.

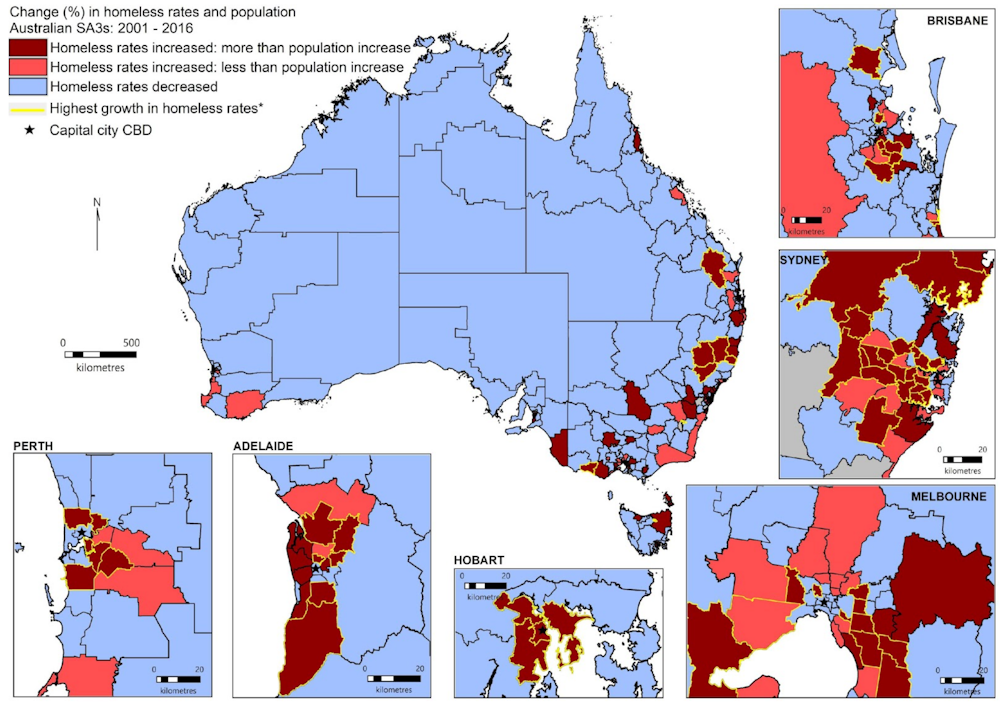

After accounting for population growth, we see a decline in homeless

rates in the CBD and inner areas of Perth, Adelaide, Melbourne and to an

extent Brisbane over the 15 years. At the same time, homeless rates in

outer urban areas have increased. In many regions this increase outpaced

population growth.

Change in homeless rate compared with population growth 2001–2016

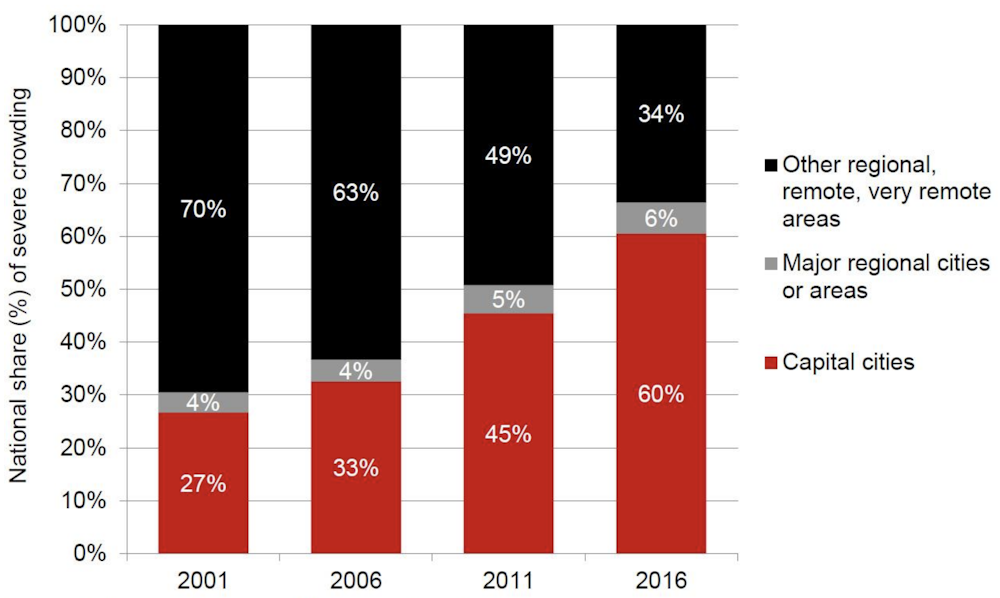

The numbers of households living in severely crowded dwellings in

capital cities have doubled in 15 years, accounting for much of the

growth in homelessness overall. In 2001, this group accounted for 35% of

people experiencing homelessness, with 27% living in cities. By 2016,

severe crowding rates had soared to 44% of all people experiencing

homelessness, with 60% living in capital cities.

Rough sleeping has also transformed into an urban phenomenon — nearly

half of all rough sleepers in Australia are now found in capital

cities.

What is driving these changes?

Homelessness has risen disproportionately in areas with a shortage of

affordable private rental housing and higher median rents. That’s

especially the case in Sydney, Hobart and Melbourne. In capital city

areas with a shortage of affordable private rentals in both 2001 and

2016, severe crowding grew rapidly (by 290.5%) against all homelessness

growth (32.6%).

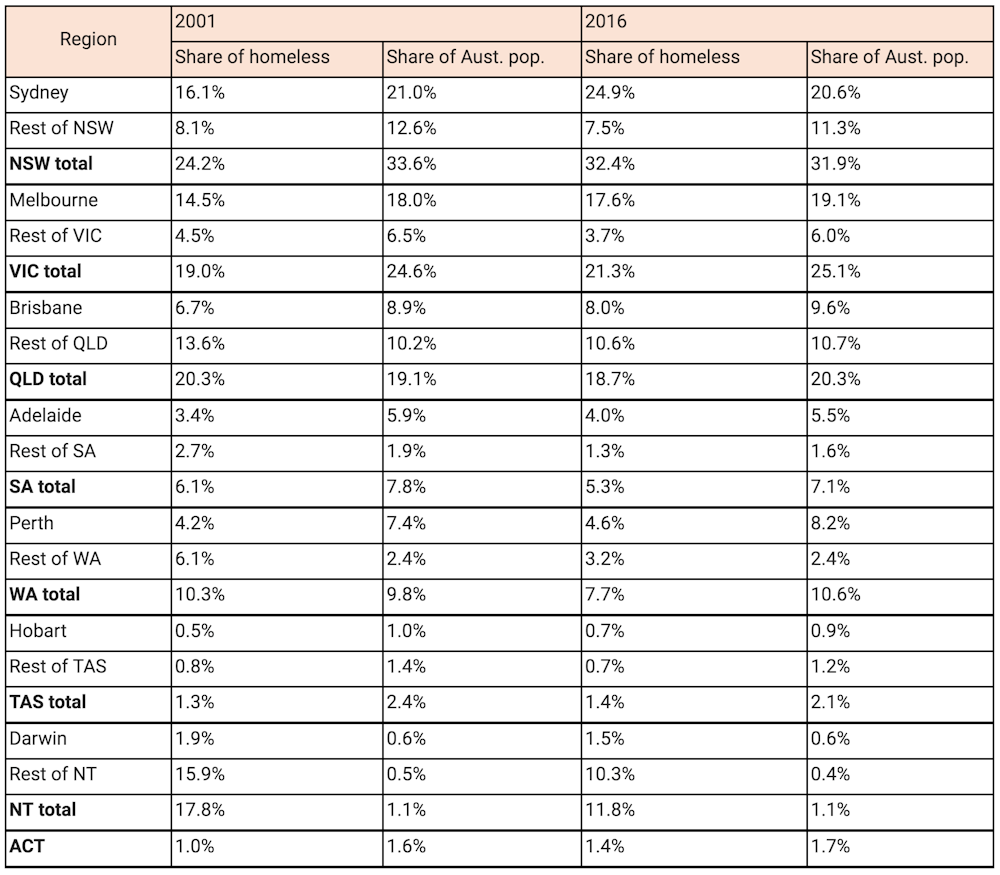

Changes in share of homeless and population by city and region, 2001-16

The effects of rental affordability on homelessness rates still hold

after controlling for other area characteristics. We also find that

these rates are strongly correlated with higher shares of particular

demographic groups in an area, including males, younger age groups,

young families, those with an Indigenous or ethnic background, and

unmarried persons.

Severe crowding in capital cities is also strongly associated with

weak labour markets and poorer areas with a high proportion of males.

However, these associations do not hold for severe crowding in remote

areas.

Governments must find ways to urgently increase both the supply and

size of affordable rental dwellings for people with the lowest incomes.

We also require better integration of planning, labour, income support

and housing policies targeted to areas of high need.

Rates of severe crowding remain highest in remote areas, and

continued efforts to increase housing supply in remote areas, such as

the National Partnership on Remote Housing (NPRH), are needed. Targeted responses are required to combat its growth in major cities.

It is critical that specialist homelessness services, as a first

response to homelessness, are well located to respond in areas where

demand is highest.

Authors: Sharon Parkinson, Senior Research Fellow, Centre for Urban Transitions, Swinburne University of Technology; Deb Batterham, PhD Candidate, Centre for Urban Transitions, Swinburne University of Technology; Margaret Reynolds, Researcher, Centre for Urban Transitions, Swinburne University of Technology

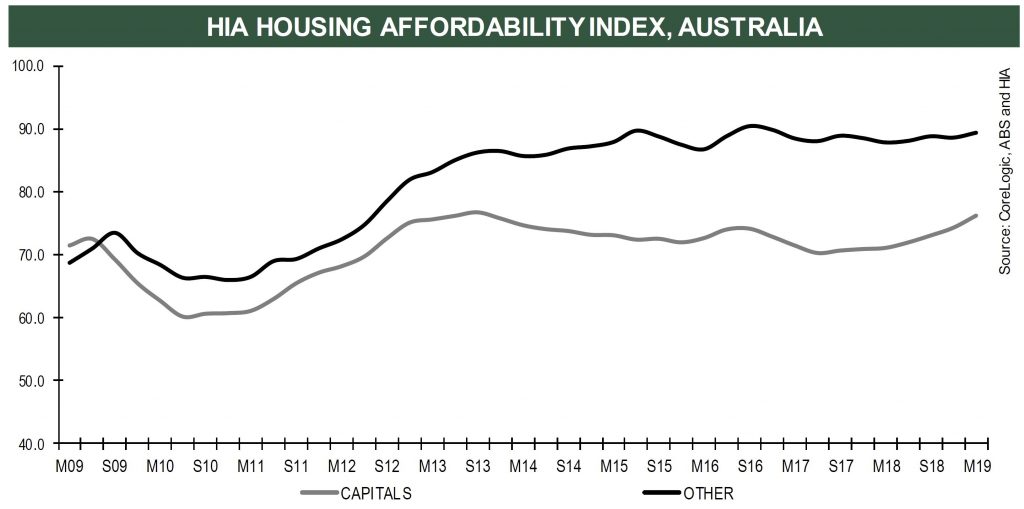

The HIA reported today that there was been a 10% improvement in affordability in a year. They attribute this to – wait for it, more building and wage rises – but do not mention the elephant in the room, the home price falls, which are continuing – at more than 10% in Sydney and Melbourne! No surprise, as home prices fall, affordability improves…

Five of the eight capital cities saw improved affordability over the year to March 2019. Sydney continues to be home to the greatest improvements, its index is up by 12.4 per cent. This was followed by Melbourne (+9.6 per cent), Perth (+7.7 per cent), Darwin (+5.9 per cent) and Brisbane (+2.5 per cent). Affordability deteriorated in Hobart (-5.1 per cent), Canberra (-5.1 per cent) and Adelaide (-1.1 per cent).

HIA’s Affordability Index is calculated for each of the eight capital cities and regional areas on a quarterly basis and takes into account the latest dwelling prices, mortgage interest rates and wage developments.

“The HIA Affordability Index rose by 2.2 per cent in the March 2019 quarter to post the most significant improvement in affordability since September 2013,” said Tim Reardon, HIA Chief Economist.

“The improvement in housing affordability has been experienced across the country, with the exception only of Tasmania and the ACT, where ongoing house price growth has seen affordability remain static,” added Mr Reardon.

“The boom in home building of the past five years is a key factor behind the improvement in housing affordability. With completions of new homes remaining at elevated levels, affordability is poised to continue to improve.

“Wage growth also contributed to the improvement in affordability.

“The improvement in affordability is most significant in east coast capital cities. Affordability in Sydney deteriorated to an extent that in June 2017 it required two average Sydney incomes to be able to afford repayments on an average Sydney home. In just over a year this has improved to only requiring 1.8 standard incomes to purchase the same home.

“Similarly, in Melbourne the Affordability Index has improved by almost 10 per cent in a year,” concluded Mr Reardon.

Blog")