ASIC has today started a four week consultation on draft guidance about the new best interests duty for mortgage brokers.

The new obligations were legislated by the Parliament in response to Recommendation 1.2 of the Royal Commission.

From 1 July, the obligations will require mortgage brokers to act in

the best interests of consumers and to prioritise consumers’ interests

when providing credit assistance.

Announcing the

consultation, ASIC Commissioner Sean Hughes said, ‘The obligations

properly align the interests of mortgage brokers with the interests and

expectations of their clients – the borrowers. Consumers should feel

confident that their broker is offering the best loan for their

circumstances and we expect that consumer outcomes will improve as a

result of this reform.’

‘We have released this

draft guidance for consultation as early as possible, to help promote

certainty for mortgage brokers as industry prepares for the new

obligations to commence in July’ Mr Hughes added.

ASIC’s proposed approach to the guidance is outlined in Consultation Paper 327 Implementing the Royal Commission recommendations: Mortgage brokers and the best interests duty

(CP 327). Consistent with the legislation, the draft guidance is

high-level and principles-based, but also incorporates practical

examples. The purpose of the guidance is to explain the obligations

introduced by the Government, it does not prescribe conduct or impose

additional obligations.

The draft guidance is

structured around the key steps common to the credit assistance process

of brokers, such as gathering information, considering the product

options available and presenting options and a recommendation to the

consumer.

ASIC welcomes views from

all interested stakeholders on the proposals in CP 327, as well as the

draft guidance. This will allow ASIC to understand how the guidance can

best assist brokers to meet these new legal obligations. ASIC expects

that the new obligations will also improve competition in the home

lending market.

ASIC seeks public comment on the draft guidance by 20 March 2020.

ASIC intends to publish final guidance before the obligations commence on 1 July 2020.

Download

Consultation Paper 327: Implementing the Royal Commission recommendations: Mortgage brokers and the best interests duty

Background

In February 2019, Parliament passed the Financial Sector Reform (Hayne Royal Commission Response—Protecting Consumers (2019 Measures) Act 2020,

which introduces a best interests duty for mortgage brokers in response

to Recommendation 1.2 of the Royal Commission. The duty is a statement

of principle which seeks to align the interests of the mortgage broker

with the interests and expectations of the consumer.

ASIC’s proposed guidance

will assist mortgage brokers to comply with these new legal obligations

by setting out ASIC’s views on what the best interests duty provisions

require and steps that can minimise the risk of non-compliance.

The best interests duty

introduced by the Government applies in addition to the responsible

lending obligations. ASIC’s draft guidance explains the interaction of

these two obligations, including that information gathered for the

purpose of complying with the responsible lending obligations may help

brokers to comply with the best interests duty.

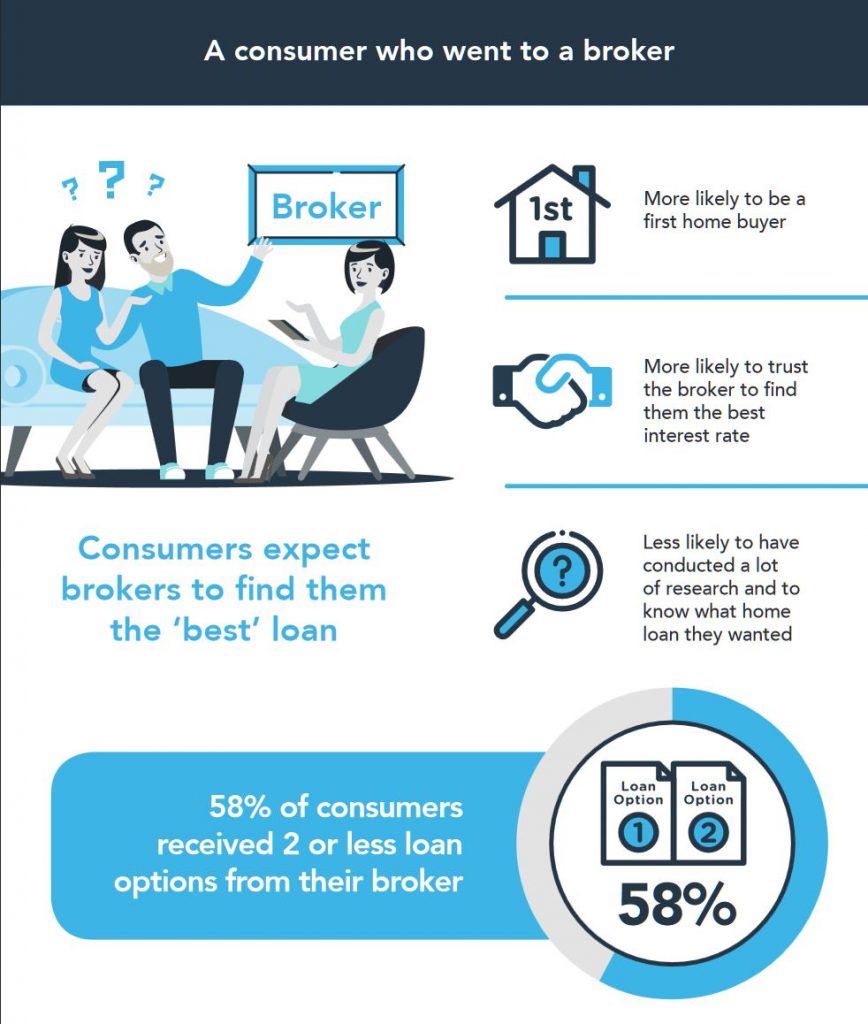

ASIC’s draft guidance follows research we published last year in Report 628Looking for a mortgage: Consumer experiences and expectations in getting a home loan. Key findings from this research included:

consumers who visit a mortgage broker expect the broker to find them the ‘best’ home loan;

mortgage brokers were inconsistent in the

ways they presented home loan options to consumers, sometimes offering

little (if any) explanation of the options considered or reasons for

their recommendation; and

first home buyers were more likely to take out their loan with a mortgage broker.

The government has released the draft legislation implementing 22 recommendations and two additional commitments which arose from the Hayne Royal Commission, including recommendations 1.6 and 2.7 which establish a compulsory scheme for checking references for prospective financial advisors and mortgage brokers. Via Australian Broker.

Before the royal commission began, under

ASIC’s Regulatory Guide 104, both Australian financial services

licensees and Australian credit licensees were meant to undertake

appropriate background checks before appointing new representatives,

through referee reports, searches of ASIC’s register of banned and

disqualified persons or police checks.

However, despite this requirement’s existence, the royal commission found financial services licensees weren’t doing enough to communicate the backgrounds of prospective employees among themselves, highlighting that licensees “frequently fail to respond adequately to requests for references regarding their previous employees” and that they do not “always take the information they receive seriously enough”.

As such, financial advisers facing

disciplinary action from an employer were able to simply leave and find

another to employ them.

Recommendation 1.6 and 2.7 seek to address this systemic weakness.

The latter looks to promote better

information sharing about the performance history of financial advisers,

focusing on compliance, risk management and advice quality, while the

former made sure this change is extended to mortgage brokers as well.

According to the draft legislation, the

reporting obligation “targets misconduct by and serious compliance

concerns about individual mortgage brokers” and “recognises that in the

industry, other parties such as lenders and aggregators are often well

positioned to identify this misconduct”.

Obligation to undertake reference checking and information sharing

New law: Both Australian financial

services licensees and Australian credit licensees are subject to a

specific obligation to undertake reference checking and information

sharing regarding a former, current or prospective employee.

Current law: Australian financial services

licensees are subject to general obligations, including taking

reasonable steps to ensure its representatives comply with the financial

services laws and credit legislation.

Civil penalty for failure to undertake reference checking and information sharing

New law: Australian financial services

licensees and credit licensees who fail to undertake reference checking

and information sharing regarding a prospective employee are subject to a

civil penalty.

Current law: No equivalent.

The proposed legislation will be in

consultation until 28 February, with interested parties invited to make a

submission before the deadline.

The final best interests duty bill for mortgage brokers has been tabled in Parliament, outlining the role brokers need to take when helping a borrower from 1 July 2020. From The Adviser.

The amended Financial Sector Reform (Hayne Royal Commission Response—Protecting Consumers (2019 Measures)) Bill 2019 has been tabled in Parliament today (28 November).

The key features of the new law are:

mortgage brokers must act in the best interests of consumers in relation to credit assistance in relation to credit contracts;

where

there is a conflict of interest, mortgage brokers must give priority to

consumers in providing credit assistance in relation to credit

contracts;

mortgage brokers and mortgage intermediaries must not accept conflicted remuneration;

employers,

credit providers and mortgage intermediaries must not give conflicted

remuneration to mortgage brokers or mortgage intermediaries; and

the circumstances in which these bans on conflicted remuneration apply are to be set out in the regulations.

Notably,

the duty to act in the best interests of the consumer in relation to

credit assistance is a principle-based standard of conduct that applies

across a range of activities that licensees and representatives engage

in.

As such, what conduct satisfies the duty will depend on the

individual circumstances in which credit assistance is provided to a

consumer in relation to a credit contract.

The duty does not

prescribe conduct that will be taken to satisfy the duty in specific

circumstances. Instead, it is the responsibility of mortgage brokers to

ensure that their conduct meets the standard of “acting in the best

interests of consumers” in the relevant circumstances.

However, the new duty will mean that there could be circumstances

where the mortgage broker may not have acted in a consumer’s best

interests even if the responsible lending obligations were complied

with. For example, even if a home loan product is ‘not unsuitable’,

recommending it to the consumer might not be in the consumer’s “best

interests”, the accompanying documentation reads.

The penalty for breaking this duty for both credit representatives and licensees is 5,000 penalty units.

Examples of the duty in action – white label called in question

In the explanatory materials, there are examples of steps that may need to be taken for this new duty. These include:

prior to recommending any home loan product or other credit contract to a consumer based on consideration of that consumer’s particular circumstances, the mortgage broker may need to consider a range of products (including the features of those products), form a view about which products are in the consumer’s best interests and then inform the consumer of the range and the options it contains;

any recommendations made would be expected to be based on consumer benefits, rather than benefits that may be realised by the broker; that is, a broker should not recommend a loan by prioritising factors that cannot be substantiated as delivering benefits to that particular consumer (such as the broker’s relationship with the lender), over factors and features which affect the cost of the product or are more relevant to the consumer;

in cases where critical information is not obtained when inquiring about a consumer’s circumstances, the broker could be expected to refrain from making a recommendation about a loan where there is a consequent risk that the loan will not be in the consumer’s best interests.

Interestingly, the new duty also

outlines that “a broker would not suggest, from their aggregator’s

panel of lenders, a white label home loan that has the same features as a

branded product from the same lender, but with a higher interest rate,

because it would not be in the best interests of the consumer to pay

more for an otherwise similar product”.

The explanatory materials go on to outline that during a periodic review, a broker “would not suggest that the consumer remain in a credit contract without considering whether this would be in the consumer’s best interests”.

“For

example, it may be a breach of the duty if the broker suggested the

consumer remain in their current home loan when they could refinance to a

cheaper product as the broker did not want to incur the consequent

liability to the lender when their commission payments were clawed

back,” it reads.

Helping consumers understand their decision implications

The

materials also outline that there may be situations where the

consumer does not properly understand the implications of different

choices and so the broker may have to assist them to understand why a

particular loan is or is not in their best interests, which could inform

the brokers’ actions.

An example given is if a consumer asks the

broker if they should take out an interest-only home loan on a property

they are looking to buy. The home loan will have a higher interest rate

than a principal and interest home loan. The broker helps the consumer

to understand the difference in cost of the two home loans, and other

differences in the way in which they operate, including that the

consumer will only build equity if the property’s value increases or

they make additional repayments, and the implications of moving to

higher repayments at the end of the interest-only period.

Another

example is if a consumer asks the broker if they should take out a home

loan with an offset account as they have heard this can save them money,

even though the interest rate is slightly higher. The broker helps the

consumer to understand what is in their best interests, based on the

difference between the higher interest rate and the savings that

consumer could reasonably expect through utilisation of the offset

account.

Comments from Frydenberg

At the second reading this afternoon (28 November), Treasurer Josh Frydenberg said: “[T]he

bill introduces a best interests duty for mortgage brokers that will

ensure that consumers’ interests are prioritised when a mortgage broker

provides credit assistance, as regulated by the National Consumer Credit

Protection Act 2009. In practice this will mean that, in accordance

with Commissioner Hayne’s recommendations, a duty will apply in relation

to the provision of consumer credit assistance and not business

lending.

“The

government is also reforming mortgage broker remuneration, and the bill

provides for a regulation making power to this end. The regulations will

require the value of upfront commissions to be linked to the amount

drawn down by borrowers instead of the loan amount; ban campaign and

volume based commissions and payments; and cap soft dollar benefits.

“Further,

the period over which commissions can be clawed back from aggregators

and mortgage brokers will be limited to two years, and passing on this

cost to consumers will be prohibited.

“After

careful consideration, the government decided to delay consideration of

aspects of Commissioner Hayne’s recommendations for mortgage

brokers—namely moving to a borrower-pays remuneration structure. We will

be doing a review with the Council of Financial Regulators and the

Australian Competition and Consumer Commission (ACCC). That will be

carried out in three years time.

“Implementation

of these reforms, as recommended by the royal commission, is a critical

component of restoring trust and confidence in Australia’s financial

system and is part of the Morrison government’s plan for a stronger

economy.”

The government will also introduce the Financial

Sector Reform (Hayne Royal Commission Response – Stronger Regulators

(2019 Measures)) Bill 2019. The Bill implements a further four

additional commitments the Government announced at the time of

responding to the Royal Commission and will ensure that ASIC can

effectively enforce existing laws.

“The government is taking

action on all 76 recommendations contained in the Final Report of the

Royal Commission and, in a number of important areas, is going further.

Restoring trust in Australia’s financial system is part of our plan for a

stronger economy,” Mr Frydenberg said.

Westpac Group has announced that it will remove the claim process for upfront commissions paid on post-settlement drawdowns on broker-originated home loans, via InvestorDaily.

For all subsequent upfront commissions payable from 1 January 2020,

brokers and third-party introducers will automatically receive

remuneration.

Westpac revealed that subsequent upfront commission will remain

payable for each eligible home loan following the 12-month anniversary

of the loan settlement.

“This change delivers on our commitment to continue to review and improve the broker commission model,” Westpac stated.

Westpac’s announcement comes amid calls from broking industry stakeholders for more equitable remuneration arrangements.

Last month, Connective director Mark Haron noted the impact of contrasting remuneration policies adopted by lenders off the back of the Combined Industry Forum’s move to limit the upfront commission paid to brokers to the amount drawn down by borrowers (net of offset).

Mr Haron said that some lenders had opted to withhold the payment of

commission for additional funds arranged by a broker, which are utilised

by a borrower after a pre-determined period post-settlement.

The Connective director added that the disparity in the application of the CIF reforms had increased risks of “lender choice conflicts”, which could hinder compliance with the newly proposed best interests duty.

Loan Market’s executive chairman Sam White, has also noted his concerns with existing net of offset arrangements.

Mr White called for an arrangement that better aligns with existing

clawback provisions, which, under the federal government’s newly

proposed bill, would limit the clawback period to two years.

“Our belief is that net of offset should mirror clawback provisions,” Mr White said.

“If it is good enough for banks to claw back the money over two

years, it should also be good enough to increase the upfronts over that

same time period.”

Like Mr Haron, Mr White revealed that Loan Market would also be

lobbying for reform to existing net of offset arrangements as part of

the consultation process for the government’s best interests duty bill.

The push for reforms to net of offset policies follow the release of

the Mortgage & Finance Association of Australia’s Industry

Intelligence Service report, which revealed that, over the six months to

March 2019, the national average annual gross value of commissions

collected per broker dropped by 3 per cent when compared to the previous

corresponding period, falling to a historic low of $128,709.

The decline was driven by a 10.6 per cent fall in the average upfront

commission received by a broker, down from $75,604 to $67,554 – offset

by a 6.9 per cent increase in the average annual gross trail commission

received per broker, from $57,189 to $61,155.

Reductions in commission revenue have also prompted calls from both industry associations and aggregators for “fair and equitable” clawback arrangements.

Mr Haron and the Australian Finance Group’s head of industry and partnerships Mark Hewitt, recently indicated that they would be lobbying for clawback reform during the consultation period for the federal government’s proposed best interests duty bill.

The Mortgage and Finance Association of Australia (MFAA) has released a report examining the broker channel’s performance over the past six months; via AustralianBroker.

The eighth edition of the Industry Intelligence Service

Report (IISR) drew on data supplied by 12 major aggregators from October

2018 to March 2019.

While the the broker channel achieved a record high market

share of 59.7% during the period, it settled just $87.56bn in home loans

– the lowest six-month value recorded since the MFAA commenced

reporting in 2015, down 10.32% on the previous year.

The average value of new home loans settled per broker also

continued to decline but at a rate “far greater than ever before,” down

10.66% on the year before.

The number of loan applications also reached never before

charted territories, with applications down 8.53% from the period before

and 13.39% year-on-year.

Further, the average number of applications lodged per broker declined across all states excepting Tasmania.

The broker population is down from the record high of

17,040 industry participants, with the net industry turnover –

accounting for those joining and leaving the industry, as well as those

moving between aggregators – up to 10.9% from 9.6% a year ago.

Notably, despite the proportion of new female recruits

increasing by 10% compared to new male recruits, the population of

female brokers declined over the six months, down 1.79%.

All of these factors contributed to a fall in the average

total broker remuneration “to the lowest levels ever observed” by the

IISR.

Average combined remuneration has dropped 3.49% from the

last six month period and is down 3.08% year on year. Compared to the

high of April to September in 2016, it’s down 9.64%.

The report linked the decline to the lower upfront commissions as trail increased across all states.

The MFAA reiterated throughout the report that the

inhospitable credit environment did not only impact the broker channel,

as the value of home loans settled directly with lenders was down 15.71%

from the last six months and 19.1% from the year before.

ASIC has highlighted that some consumers are taking out home loans when cheaper alternatives may well exist. Brokers do not come out that well!

Today ASIC has released a report Looking for a mortgage: Consumer experiences and expectations in getting a home loan.

As part of this research, ASIC followed over 300 consumers in the

process of taking out a home loan and surveyed another 2,000 consumers.

This research examines consumer decision-making in relation to home loans to identify what factors influence their journey.

Key findings from our research include:

consumers who visit a mortgage broker expect the broker to find them the ‘best’ home loan

mortgage brokers were inconsistent in the ways they presented home

loan options to consumers, sometimes offering little (if any)

explanation of the options considered or reasons for their

recommendation

first home buyers were more likely to take out their loan with a mortgage broker.

The report shows that consumers taking out a loan directly through a

lender were more likely to be a refinancer or have had previous

experience taking out home loans. Consumers who went directly to a

lender valued convenience, with 69% taking out their loan with a lender

they had an existing relationship with.

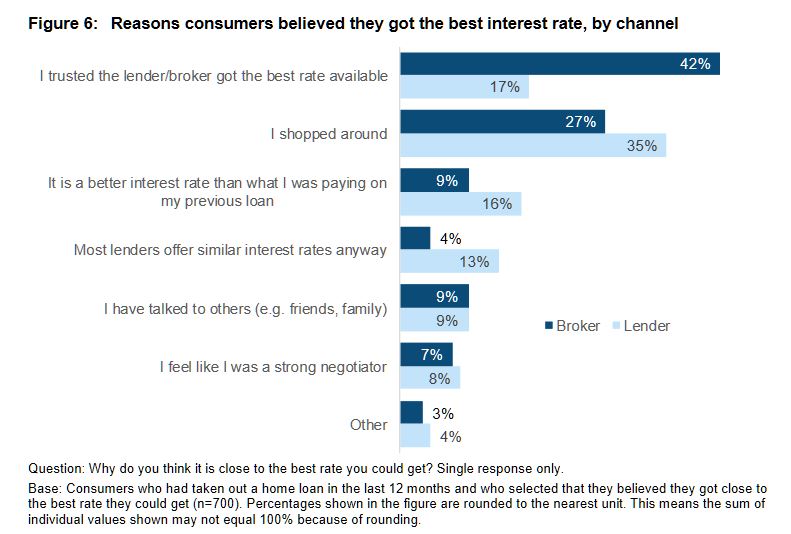

Taking out a home loan is a complex process and consumers told us it

can be an ‘overwhelming’ experience. Although most consumers set out to

find the best loan they could, 1 in 5 consumers believed that they could

have got a better interest rate on their home loan or were not sure

whether they had even got a good rate.

In launching ASIC’s report, Commissioner Sean Hughes said, ‘A home

loan is one of the most important financial commitments a consumer will

make. Lenders, brokers and aggregators must step up to make it easier

for consumers to meaningfully compare loan options and for brokers to

communicate how a home loan option has been selected for them.’

‘ASIC strongly supports the recent Government announcement to enact a best interests duty for mortgage brokers. Importantly, the implementation of such a duty will align the role of brokers to the reasonable expectations of consumers.’

‘Our research also suggests that some consumers are taking out home loans when cheaper alternatives may well exist. We are working with other regulators to develop a new home loan interest rate tool to improve price transparency for consumers to compare options. We expect this tool will be made available on ASIC’s MoneySmart website next year.’

Background

In March 2017, ASIC published the findings of our review into the

effect of remuneration structures in the mortgage broking market on the

quality of consumer outcomes: see Report 516 Review of mortgage broker remuneration

(REP 516). We found that current remuneration practices create

conflicts of interest that may contribute to poor consumer outcomes.

As part of this review we also found that consumers who obtained their loan through a broker:

borrow more

have higher loan to valuation ratios

spend more of their wage on a mortgage

take out more interest-only loans

get the same rate as customers that go directly to a lender.

Consumers can also use MoneySmart’s mortgage calculator to compare home loans and work out whether they can save money by switching to another mortgage.

Aussie Home Loans boss James Symond has described the mortgage industry’s mammoth lobbying efforts as a “case book study” in uniting a competitive industry – via InvestorDaily.

Few

sectors of the financial services universe had more riding on the 2019

federal election than mortgage broking. A Labor victory would have been a

devasting blow to the third-party channel, which is responsible for

helping most Aussies secure finance to buy a home.

“The industry

banded together. You couldn’t be prouder of them all. This is a case

book study of an industry that felt vulnerable and came together and

stepped up to defend itself,” Mr Symond told Investor Daily. “You had

individual mortgage brokers working in small businesses around the

country having one-on-one meetings with MPs,” he said.

Regardless

of what their individual political views might have been, this election

was deeply personal for mortgages brokers, who earn an average of

around $86,000 – far from what some might consider the “big end of town”

that Labor was hell bent on destroying. Shorten effectively galvanised a

formidable opposition in the third-party channel by failing to back

down on remuneration changes.

After the Hayne royal commission

recommended scrapping broker commissions, the industry quickly united to

lobby both sides of the government. The result saw an enlightened

coalition confirm no changes would be made to broker remuneration.

Labor, on the other hand, would act on Hayne’s view and ban trail

commissions while introducing a higher cap of 1.1 per cent on upfront

commissions.

With

the opinion polls prior to the election pointing to a Labor victory,

the mortgage industry was making one hell of a gamble.

“It was

very much a bet, because we couldn’t infiltrate Labor,” Mr Symond said.

“With the Liberals, we got onto the right people who listened, who were

open to being educated about how the mortgage broking industry operates

and its value to consumers. But Labor was simply not interested.

“We got lucky that the coalition got back in. We don’t have to worry about the fact that Labor wouldn’t listen.”

It

was a major misstep for Labor not to interact with the mortgage broking

fraternity, given the opposition’s strong stance on economic matters.

Negative gearing reforms were a major policy for Labor, which could have

easily won over an army of mortgage brokers and the first-home buyers

they represent by coming to the table on remuneration. Linking

affordability and home ownership with the value proposition of a

mortgage broker is easy enough to spin.

On the flipside, those

with negatively geared properties who use the services of a broker would

be highly unlikely to vote for a Shorten government. Including many

brokers themselves.

“Labor had their own agenda,” Mr Symond said. “They didn’t give a hoot about mortgage brokers.”

“Thankfully the coalition got in, because it would’ve been a different story if they didn’t. We have some stability now.”

The

broking industry has the government on its side and will continue to

drive competition in the mortgage market – something that was in serious

jeopardy if Labor had succeeded and scrapped trail commissions.

In

addition to Aussie Home Loans, listed broking businesses like Mortgage

Choice, AFG and Yellow Brick Road – which recently confirmed that it is

doubling down on mortgages – will be the obvious beneficiaries of the

Coalition’s win.

What will be interesting to watch is how the

major banks react. While they have historically moved as a group, the

question hanging over the broking industry has led them in different

directions in recent years.

The royal commission and the 2019

federal election were arguably the final battles in a multiyear campaign

that has ultimately sealed a victory for the third-party channel and

the millions of home buyers it serves.

The results of the federal election are in – but what does it mean for the broking industry? We unpack the key policy positions regarding the third-party channel – via The Adviser.

In

a closely-run campaign that was neck-and-neck between the Australian

Labor Party and the Coalition, Prime Minister Scott Morrison clinched

the lead on election night (18 May).

Despite

there being some surprises on the night – including Queenslanders

swinging away from Labor to the Coalition; the fact that opinion polls

are fallible; and the shock departure of former PM and Liberal candidate

for Warringah, Tony Abbott (who lost his seat to Independent candidate

Zali Steggall) – Mr Morrison will remain as the 30th Prime Minister of

Australia.

Bill Shorten,

leader of the opposition, conceded to Mr Morrison on Saturday night,

saying it was “in the national interest” and wished him “good fortune

and good courage”.

The mortgage broking industry – which has a strong presence in Queensland, where Labor lost several of its seats – has been vocal supporters of the Coalition Government, given its stance on broker remuneration.

The

industry will likely not see any imminent, radical changes to

remuneration in the next three years under this Coalition, given its

previous commitments.

Both the abolition of trail and upfront commissions were recommended by Commissioner Hayne in his final report for the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

While the Coalition had initially said in its official response to the final report that it would ban trail commission payments for new mortgages from 1 July 2020, it later delayed any decision on fundamentally changing the structure of broker remuneration until three years’ time.

In

March of this year, Treasurer Josh Frydenberg said that the government

would look at reviewing the impacts of removing trail in three years’

time rather than abolishing it next year as originally announced,

following concerns regarding competition.

He

commented: “[F]ollowing consultation with the mortgage broking industry

and smaller lenders, the Coalition government has decided to not

prohibit trail commissions on new loans but rather review their

operation in three years’ time”.

The

review, to be undertaken by the Council of Financial Regulators and the

Australian Competition and Consumer Commission will therefore look at

both the impacts of removing trail as well as the feasibility of

continuing upfront commission payments.

Speaking

to the broking and real estate industries via teleconference earlier

this month, Mr Frydenberg thanked mortgage brokers for their “absolutely

critiical role in the economy” and “for what they do for our community”

and emphasised that the Coalition government’s response to the “cathartic” banking royal commission was to adopt all the recommendations in one form or another, but to leave broker remuneration largely alone until a review in three years’ time.

The

Treasurer said: “[W]ith respect to the ban on upfront and trail

commissions, as recommended by commissioner Hayne, that we would leave

that to a review in a few years’ time.

“The

reason is that mortgage brokers play an absolutely critical role in our

economy, and they help generate competition in that market, and we

don’t want to see mortgage brokers put out of business with,

effectively, their business just migrating to the big banks.”

Mr

Frydenberg said this position was taken after the government reviewed

the royal commission report and after speaking to key stakeholders about

“consumer and business access to financial services, the overall

stability of the financial system, the impact of competition and, of

course, on economic growth”.

“What

we don’t want to do is weaken competition and strengthen big banks,” he

said, adding that mortgage brokers were “overwhelmingly small

businesses” and sole traders.

The Coalition Government’s stance differs from Labor’s position,

which has said it backs a fixed fee for upfront commissions [at 1.1 per

cent] and a ban on trail commissions for new loans from 1 July 2020.

“We

believe this is problematic on a number of levels, particularly because

many mortgage brokers will be worse off under Labor than they are today

and could be put out of business.

“It will also impact on competition and, ultimately, their customers,” the Treasurer said earlier this month.

“Today…

brokers get paid higher amounts for more complex loans, but under the

Labor Party’s model they won’t be remunerated for this, which will

exclude certain consumers from using mortgage brokers. And a fixed fee

could drive brokers to encourage churn and put them in clear conflict

with their best interests duty.”

Mr

Frydenberg noted that it was also “not clear as to whether Labor’s

policy includes GST or whether it includes the aggregator’s fee”.

“I

think the Labor Party [has] created significant doubt in the sector

and, obviously, concern – that is the feedback that we are getting,” he

said.

However, the Coalition and Labor Party did both support Commissioner Hayne’s recommendations to introduce:

a best interests duty that will legally obligate mortgage brokers to act in the best interests of consumers;

a new requirement that the value of upfront commissions be linked to the amount drawn down by consumers;

a ban on campaign and volume-based commissions; and

a two-year limit on commission clawbacks starting from 1 July 2020.

The Coalition has also recently announced a new First Home Loan Deposit Scheme that will enable first home buyers to access a mortgage with a 5 per cent deposit.

This

would make 95 per cent loan-to-value ratio mortgages available to first

home buyers earning up to $125,000 annually (or $200,000 for couples)

from 1 January 2020.

The

First Home Loan Deposit Scheme, which will partner with private lenders

and prioritise smaller lenders in a bid to “boost competition”, will be

available to qualifying first home buyers from 1 January 2020.

The

value of homes that can be purchased under the scheme will be

“determined on a regional basis, reflecting the different property

markets across Australia,” Mr Morrison said.

The

Prime Minister estimated that the scheme would help FHBs save around

$10,000 by not having to pay lenders’ mortgage insurance (LMI).

In a clear stance on Labor’s trail position, Chris Bowen MP has said that the government’s response to the banking royal commission has “got it wrong”, particularly in regard to its “backflip” on removing trail from next year; via The Adviser.

Speaking at the AFR Banking & Wealth Summit on 26 March, Chris Bowen, shadow treasurer and federal member for McMahon, reaffirmed the Australian Labor Party’s stance on trail commission payments to mortgage brokers.

In the final report for

the Royal Commission into Misconduct in the Banking, Superannuation and

Financial Services Industry, commissioner Kenneth Hayne recommended

that “changes in brokers’ remuneration should be made over a period of

two or three years, by first prohibiting lenders from paying trail

commission to mortgage brokers in respect of new loans, then prohibiting

lenders from paying other commissions to mortgage brokers”.

Following the release of the report, the Coalition government’s official response initially suggested that it would seek to ban trail for new loans from 1 July 2020, but Treasurer Josh Frydenberg announced earlier this month

that government would instead postpone any decision on removing trail

until after a review of mortgage broker remuneration has been undertaken

in three years’ time.

Meanwhile, the Labor Party’s response called

for the removal of trail for new mortgages from 1 July 2020 and for a

standardised upfront commission as a proportion of the loan amount. It

suggested that commissions should be capped at 1.1 per cent “so that

banks can’t offer brokers incentives to choose their products”.

‘A big tick to a big flick’

Speaking

at the AFR Banking & Wealth Summit today, Mr Bowen slammed the

government for its “backflip” on trail commissions, stating that they

continued to “get it wrong” on the royal commission recommendations.

He said: “I’m

normally not too partisan at these events, I normally steer away from

political commentary – at least through much of my speech, but given we

are at the business end of the term, with the federal election less than

50 days away, I’m sure you’ll appreciate some plain speaking.

“The

choice is between an opposition prepared to make big calls, and get

those calls right, versus a government that has got the big calls

wrong.”

Mr Bowen outlined that commissioner Hayne was “very clear” in his observations, which he said included the observations that “the

interest of customers was relegated to second place far too often; too

often, consumers were being left in the dark about how products or

services are acquired and delivered; and too often, financial services

entities were breaking the law and not held to account for their

actions”.

“Those actions that were revealed through the royal commission had given the entire sector a bad name,” Mr Bowen said.

“They needed, and need, to be dealt with. These are systemic failures in our financial services industry when it comes to providing community standards and expectations.”

Emphasising that the

government had previously called the royal commission a “populist

whinge”, “regrettable”, a “reckless distraction” and a “QC’s complaints

desk”, Mr Bowen added: “They got the big call wrong. And they also continue to get it wrong now, in terms of the recommendations.

“That’s probably most clear in relation to mortgage brokers.”

Mr

Bowen elaborated: “A few days after the royal commission was handed

down, the government told us that they were implementing the royal

commission recommendation on trail commissions and said the royal

commission recommendation was getting a ‘big tick’. No nuance, no discussion, just simply that this would be implemented.

“Now the reasons given by the commissioner on this issue were clear: The chief value of trail commissions to the recipient, to put it bluntly, is that they are money for nothing, [he said].

“And these are not new issues. The Productivity Commission found trail commissions have the effect of aligning the broker’s interests with those of the lender, rather than those of the borrower. The case was clear.”

Mr Bowen therefore called the government’s change in stance on trail as “a backflip with triple pike”.

“Just weeks after giving a recommendation a big tick, it was given the big flick,” he said, noting that it took “just 35 days to backflip on a major reform of phasing out trailing commissions for mortgage brokers”.

However, the shadow treasurer said that “there

was, and is, a strong case for thinking carefully about the royal

commission recommendation and ensuring we protect competition in

banking. That’s exactly what we did,” he said.

“We consulted with mortgage brokers, we consulted with banks and financial institutions – particularly the smaller ones.

“We

came up with a different way of removing conflicted remuneration for

mortgage brokers. We announced that we would have legislated a flat

upfront commission rate to avoid mortgage brokers’ advice being

conflicted by the rate of the commission offered,” he said.

Mr Bowen concluded: “It’s

one thing to achieve the objectives of the royal commission

recommendation in another way, as Labor has done; it’s another thing to

completely abrogate any policy action, as the Treasurer has done.

“When

we make big calls – and we’ve made quite a few of them – we stick to

them, fight for them, and seek to mandate for them, which is what we’ll

be doing, presumably, on the 11th of May [for the federal election].

“We

will implement 75 recommendations of the royal commission in full. The

government cannot say that and already we are seeing consumer groups

being very concerned that the government is already walking away from

other recommendations,” he said.

Broking industry continues engagement with ALP

While

the shadow treasurer has reaffirmed the party’s stance on trail

commissions, the broking industry continues its work in engaging and

educating ALP members on the benefits of trail.

Indeed, just last week, a group of nearly

100 representatives from the mortgage industry met shadow assistant

treasurer and federal member for Fenner, ACT, Dr Andrew Leigh, at the QT

Hotel in Canberra for the Future of Mortgage Lending forum, organised

by AFG in partnership with Connective and Mortgage Choice, in which the

need for trail was hotly discussed.

Speaking to The

Adviser about the event last week, AFG’s Mark Hewitt said that the

purpose of the meeting was to have a town hall type discussion with

economist-turned-politician Dr Leigh, and to outline how Labor’s plans to remove trail for new loans from next year could impact borrower outcomes.

“We

wanted to get the point across to Dr Leigh about the unintended

consequences of abolishing trail and the impacts that could have on the

brokers’ ability to provide an ongoing service to their clients,” Mr

Hewitt said.

“Labor’s focus was very centred on

talking about them being the first to move on commissions, but the

sentiment in the room was definitely around the abolition of trail and

why it was not a good idea.

“What was particularly

impressive to me was the care and concern that the brokers in the room

had for their customers and also their concern about the unintended

consequences of having their remuneration front-loaded in the way that

Labor is proposing.”

He continued: “We were talking

about the impacts that the removal of trail might have on brokers’

to provide ongoing service to clients and also the fact that

the model without trail doesn’t provide any incentive for an ongoing

customer relationship.”

Mr Hewitt told The Adviser that Dr Leigh “was very receptive to the messages in the room and was very impressive and engaging”.

“It

takes a fair bit of courage as well, as he was the only person in the

room who thought that abolishing trail was a good idea, but he stood by

the party line while still engaging and being respectful to the counter

arguments,” Mr Hewitt said.

“We were very pleased

with how it went because it’s a continuing conversation – and it was a

two-way conversation, hearing both sides, which is what we wanted to

achieve,” AFG’s general manager for broker and residential added.