Significant lobbying is now underway to influence Treasury in the final outcome of the mortgage broker commission changes, bearing in mind the recent ASIC review called out some fundamental conflicts in the current model, and highlighted that consumers do not necessarily get the best outcomes. Importantly, ASIC says the standard model of upfront and trail commissions creates conflicts of interest.

ASIC has put forward six proposals to improve consumer outcomes and competition in the home loan market:

(a) changing the standard commission model to reduce the risk of poor consumer outcomes;

(b) moving away from bonus commissions and bonus payments, which increase the risk of poor consumer outcomes;

(c) moving away from soft dollar benefits, which increase the risk of poor consumer outcomes and can undermine competition;

(d) clearer disclosure of ownership structures within the home loan market to improve competition;

(e) establishing a new public reporting regime of consumer outcomes and competition in the home loan market; and

(f) improving the oversight of brokers by lenders and aggregators.

As we discussed in an earlier post – The Truth About Mortgage Brokers, “consumers should be using a mortgage broker with their eyes open. Ask yourself if the broker is truly working in your best interests”.

In a joint submission to the Treasury, consumer advocacy group CHOICE, along with the Financial Rights Legal Centre, Consumer Action Law Centre and Financial Counselling Australia, called for:

In a joint submission to the Treasury, consumer advocacy group CHOICE, along with the Financial Rights Legal Centre, Consumer Action Law Centre and Financial Counselling Australia, called for:

– the removal of upfront and trail commissions;

– the implementation of fixed fees (via lump sum payments or hourly rates);

– the removal of bonus commissions, bonus payments and soft dollar payments; and

– a change in law so brokers have to act in the ‘best interest’ of clients; and

– a requirement that brokers disclose ownership relationships and the lender behind any white-label loan recommended to a consumer.

CHOICE, which has strongly criticised the broker channel in the past, said it was “simply not good enough” that ASIC “has left it up to the industry to find a solution”.

The group suggested that the way mortgage brokers are currently paid “means it’s very unlikely that a customer is going to get a loan that’s best for them” and that the industry therefore needed a “major change”.

CHOICE’s head of campaigns and policy, Erin Turner said: “We’ve called for urgent action on trail commissions, monthly payments from a lender to an aggregator which is passed on to a broker over the life of a loan.

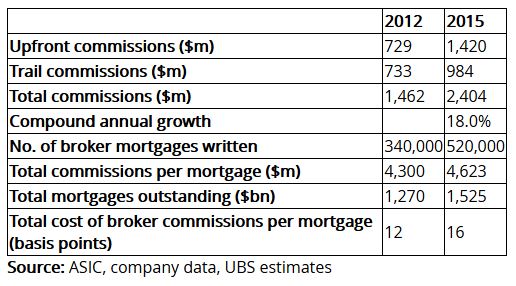

“A lender pays out an average of $750 per year for the life of a home loan through trail commissions. Trail payments are money for jam. The broker makes money for doing nothing, discouraging them from reviewing the quality of a loan long term.”

However, as reported in The Advisor, the peak broker bodies – the MFAA and FBAA have called this submission “ignorant” and “misinformed”, which perhaps is unsurprising, as these bodies are strongly aligned with the current mode of operation. They slammed the recommendations as “detrimental” to consumer interests.

The executive director of the Finance Brokers Association of Australia (FBAA), Peter White, said the groups had “no regard for the competitive position and incredible value proposition that brokers bring to home loan borrowers”.

He went on to say it was “very concerning” when “misinformation is disseminated by those claiming to be consumer advocates, but who don’t tell the truth”.

Mr White suggested that, without the competition of brokers and non-banks, interest rates would still be around the 7.5 per cent mark (rather than 4 per cent).

He added that the suggestion of a flat fee would actually lead to a rise in interest rates.

“The average loan amount nationally is around $450,000 and the average commission is 0.60 per cent, meaning a flat fee, commercially, would be around the $2,700 mark,” he said.

“In regional markets, where loan sizes are smaller, a loan of $200,000 would (in the current structures) pay around $1,200 and not $2,700 in a flat-fee model, and lenders would never wear such a loss.”

Mr White said the groups also claim that mortgage brokers are giving advice, yet that’s not the case.

“Under the regulations that govern mortgage brokers, they give credit assistance and are doing work on behalf of the lender, which is why the lender pays them a commission and it has no bearing on the interest rate the borrower pays.

“If you don’t use a broker you go to a bank which still has the administration costs for the loan, so it’s cheaper for the bank to originate a loan through a broker than at a branch.”

He said the suggestion to abolish trail commissions is “an ignorant position to take”.

Speaking of the consumer groups in question, he said: “If they knew their subject matter, they would know that trail commission is paid to brokers to offset costs of providing ongoing customer service and to manage the borrower’s ongoing and variable lending needs as required under the national consumer credit protection regulations.

“There is absolutely no evidence to suggest trail incomes harm competition.”

Changes would ‘significantly harm the interests of consumers’

The Mortgage & Finance Association of Australia (MFAA) also released a statement, saying it was “disappointed” by the consumer groups’ submissions and comments, adding that they would “significantly harm the interests of consumers they claim to represent”.

Touching on the consumer groups’ proposals, Mike Felton, CEO of the MFAA, said: “A fee-for-service model may suit lenders, but it would drive the majority of brokers out of the industry. This removal of access to brokers for Australians would severely reduce competition in the industry, which is something we are trying to avoid for consumers.

“A single, lender-funded, fee-for-service would lead to a standardisation of all fees, which we believe ASIC itself does not support and we believe would also be considered anti-competitive by the ACCC,” Mr Felton said.

He continued: “I do not see how removing brokers from the industry, and consolidating power back in the hands of banks, serves the needs of consumers.”

Mr Felton highlighted a 2015 Ernst & Young study that found that 92 percent of consumers reported they were ‘satisfied’ or ‘very satisfied’ with their broker’s performance, and highlighted that consumers have increasingly turned to brokers to arrange their home loans – with more than 53 per cent of all mortgages written by the third-party channel.

He concluded: “This is also about access to finance for Australians. If you live in a regional or rural area, you may not have access to a bank branch – or you may have access to one bank branch. Brokers provide regional Australians the same access to finance as people who live in inner Sydney or Melbourne and it is critical that we should avoid doing anything to negatively impact that.”

Mr Felton said that the proposals also did not reflect the concerns raised by ASIC.

He commented: “ASIC understands that brokers drive competition and provide a critical service to consumers that combines choice, expertise and convenience, to help them make informed choices and get the most appropriate deal…

“When you are obtaining a mortgage, there is a lot more at stake than just the interest rate. Brokers assess the needs of their customers in detail, both now and into the future and recommend products and lenders that suit these needs.”

Both associations said that they have been actively working with ASIC, Treasury and a number of other key stakeholders on different ways to improve the commission structure to enhance consumer outcomes.

Separately, a submission from Mortgage Choice, also discussed by The Adviser, has told the Treasury that the current upfront commission structure for brokers is “sound” and should not be changed to reflect the loan-to-value ratio of mortgages.

In its submission to ASIC’s Review of Mortgage Broker Remuneration, seen by The Adviser, Mortgage Choice said it was generally “supportive” of ASIC’s review, but argued that the current, standard commission model was “sound” and some proposals may be hard to implement.

Touching on the first proposal, which focuses on “improving” the standard commission model so that brokers are not “incentivised purely on the size of the loan”, Mortgage Choice suggested that no such changes should be implemented.

Writing in the submission, company secretary David Hoskins said that Mortgage Choice believed the current model is “sound and delivers positive consumer outcomes”, adding that the upfront commission structure “appropriately compensates the broker for the time and effort required to lodge an application and take it through to approval”.

He elaborated: “The time and effort involved in this process is significant, it requires the broker to forensically assess the customer’s needs, future needs, income, asset position as well as living expenses, review the current offerings in the market and match the same with a suitable solution.

“The payment of trail commission encourages the broker to put the customer in a product that will be suitable for the consumer over the long term.”

The submission also noted ASIC’s finding that there are more interest-only loans in the broker channel, and higher LVRs and loan amounts, but emphasised that this is due to “the demographics of the customers who choose to use a broker and the more complex needs they bring to the table, as well as brokers actively looking for solutions that meet their customers long-term needs”.

“We do not believe that brokers, in general, place loans with the sole intent and purpose of receiving additional commission,” it said.

Looking at ASIC’s example of changing commissions to “reflect the LVR [loan-to-value ratio]”, Mortgage Choice said it would “not be correct” to suggest that it would be effective to change the shape or quantum of broker commissions based on LVR, interest-only or lower loan amounts.

The submissions reads: “Broker economics need to line up with lender economics and consumer outcomes. Markets already price for risk and return driving both lower LVRs and higher loan amounts through discount pricing to the end customer. Unless the regulator is intent on dictating the discounting regimes set by lenders, then the only truly effective mechanism available to the regulator is through being more prescriptive in lender underwriting policy or shaping the economics at the lender end to drive an increase in consumer pricing at the higher risk end of the market.”

When it comes to bonus commissions and bonus payments, Mortgage Choice said it did not believe that these types of payments were a “significant influencer” in terms of where a broker places a loan, and revealed that it only received such payments from two lenders.

Noting that the amount received from its bonus payments was “not significant” and is “pooled and shared with brokers based on the volume of business they write across the lender panel”, it added that it was “not opposed” to the removal of these payments in the industry as it would align it with other parts of the financial industry (bonus commissions and payments have been removed from the financial planning and life insurance sectors).

The brokerage was also supportive of the removal of soft dollar benefits that could influence broker decisions, but thought lender sponsorship and aggregator conferences and events should not be removed if they are linked to broker professional development. “These are essential to the progression and increased professionalism of brokers in our industry,” it said.

Likewise, it said that hospitality benefits “such as tickets to sporting events or concerts” should be advised to the relevant aggregators to enable appropriate monitoring.

Change lender policy and pricing

Indeed, the company position said that if ASIC wishes to change the shape and nature of mortgage lending through broking or through the lending system then there are “two significant levers that need to be used: lender credit policy and lender pricing”.

Mr Hoskins writes: “Influencing lender credit policy would ensure borrowing levels are appropriate based on servicing, LVR and repayment restructure (IO v P&I). By varying lender policy, the regulator can essentially adjust the loan portfolio characteristics…

“Brokers work with borrowers to obtain the most cost-effective lending solution. To suggest that a broker would encourage a customer to borrow more or to borrow at a higher LVR would not be an effective business outcome for a broker who would very easily lose a customer relationship if they did not find a competitively priced lending solution. Furthermore, lender pricing to consumers follows the economics of lending in that the larger the loan the larger the profit for the lender and as such, lenders typically offer larger drive discounts for larger loans. Accordingly, in certain situations, customers’ needs may be well served if they were to borrow just enough to cross the next pricing tier and then place the additional funds in an offset account.”

Mortgage Choice concluded that for commissions, the current structure is “sound”, adding that the “shape and the quantum” of initial and ongoing commission is similar to the commission structures to be adopted in the life insurance industry.

Lastly, Mortgage Choice emphasised that the remuneration review and the ASIC industry funding model review were “inextricably linked” and should be considered together if the end goal is delivering positive consumer outcomes.

It explains: “Ensuring a company has responsibility for governance and oversight is critical to providing good customer outcomes.”

The response outlines that it is “comfortable” with the idea of a new public reporting regime and requirements for more broker oversight, but warned that aggregator and lender information would need to focus on a loan, customer and broker specific level, rather than an overarching view.