Christopher Joye published an interesting analysis on Livewire. “All of this analysis would look worse if we marked everything to market at the end March, as house prices have continued to fall”, he said.

Exactly, as prices fall risks rise.

In assessing whether to get long or short residential mortgage-backed securities (RMBS), we undertake a great deal of quantitative analysis, including revaluing the homes that protect these bonds at regular intervals and developing globally unique RMBS default and prepayment indices. (Regular readers will know that we exited most of our RMBS in February 2018.)

As house prices fall, the loan-to-value ratios underpinning an RMBS

issue rise in lock-step, which reduces the equity protecting the bond.

Using Bloomberg data on the current amortised value of the home loans in

all Australian RMBS pools, the LVR distribution of the loans, and the

geographic location of the properties, we have marked-to-market all the

2017, 2018 and 2019 issues after accounting for the amortisation or

pay-down of loans through to the end of February 2019.

What we find is some huge increases in the share of an RMBS issue’s

assets with LVRs over 90% compared to the leverage reported when the

bond was originally sold to investors (often jumping from 5% of loans to

15% to 20% of loans).

We have also documented some recent RMBS deals where the share of

loans that are underwater, or have LVRs over 100%, has increased

strikingly, including one transaction where more than 1-in-10 loans

appear to be underwater.

All of this analysis would look worse if we marked everything to

market at the end March, as house prices have continued to fall.

It is possible that there is a difference between the CoreLogic index

price changes and the individual property changes, but we have used the

state-wide indices and deals with metro biases (as is common) would

likely have even poorer performance than these numbers imply. Also, the

automated property valuation models used to revalue individual homes are

commonly based on the CoreLogic indices.

At the same time as the equity protecting RMBS is shrinking, we have

demonstrated that RMBS default rates are trending higher back to GFC

peaks using our compositionally-adjusted hedonic index of RMBS arrears.

This is consistent with the RBA’s data on mortgage arrears, which I have

enclosed below our index chart.

There is also the problem of declining mortgage prepayment rates,

which is blowing out the expected life of RMBS bonds (adversely

impacting assumed credit spreads) as borrowers struggle to prepay loans

at the same rate as they have done in the past.

And finally, we have had an incredible surge in RMBS supply, with the

highest level of issuance since the heady days before the GFC (about

$100bn of supply since the start of 2017), which will inevitably put

pressure on these bonds’ prices.

After we banged the table about these risks early last year, S&P belatedly warned in November:

“Falling property prices pose a greater risk for the

lower-rated tranches of less-seasoned transactions, particularly for

loans underwritten at the peak of the property cycle;”

“The RMBS sector is now facing more elevated risk than it was

12 months ago. Alongside high household debt and low wage growth are

emerging risks such as lower seasoning levels in new transactions and

increasing competition.”

“Lower-rated tranches of more recent transactions with lower

seasoning levels are more exposed to this risk, particularly for loans

underwritten in the past 12 months, at the peak of the property cycle”

“Less-seasoned loans and highly leveraged loans are most exposed to a more protracted decline in property prices.”

“Loans originated in more recent years, at the peak of the

property boom, will be more exposed to property price declines,

particularly those with higher loan-to-value (LTV) ratios.”

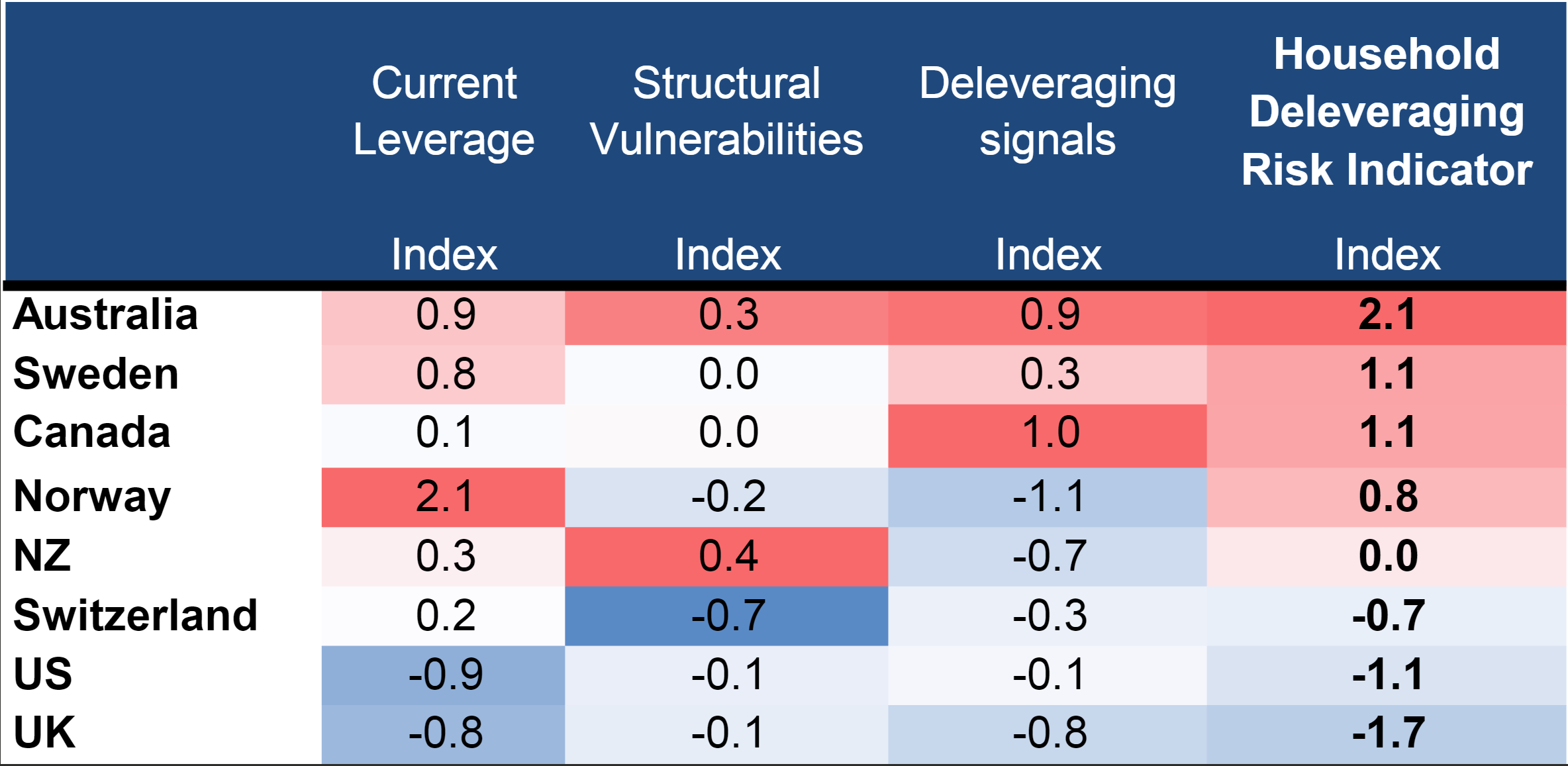

According to Morgan Stanley, via Bloomberg, Australia’s economy is most at risk in the developed world from household debt reduction because of weak house prices and potential tax changes that could curb property investments.

That’s the conclusion from the bank’s Household Deleveraging Risk Indicator, which looks at relative debt and structural weaknesses. The study of the world’s 10 leading developed economies puts Sweden and Canada as the second-most at risk, followed by Norway.

Source: Morgan Stanley Research

“These economies now face a crucial juncture as housing markets weaken, forcing a reappraisal of leverage and wealth, and global financial conditions tighten, increasing the consumption drag from debt service and rising savings,” the bank’s strategists said.

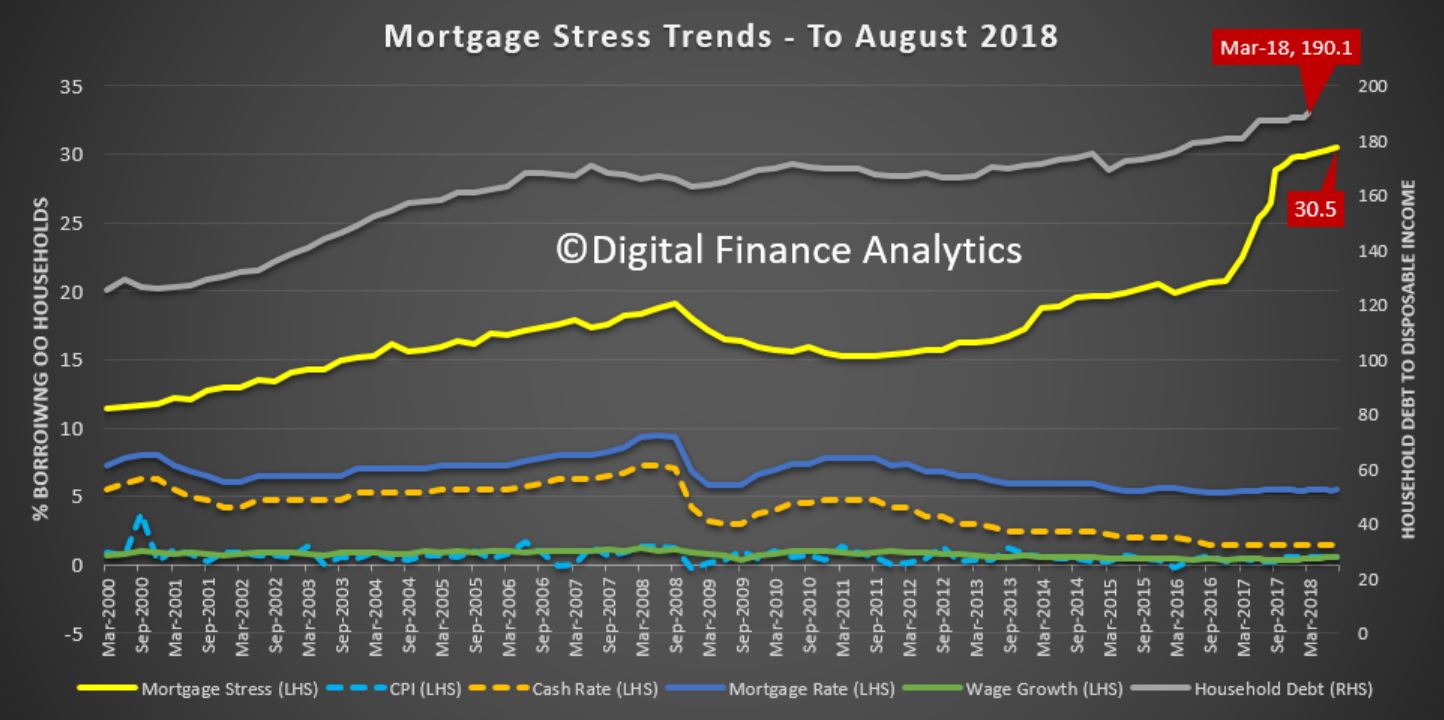

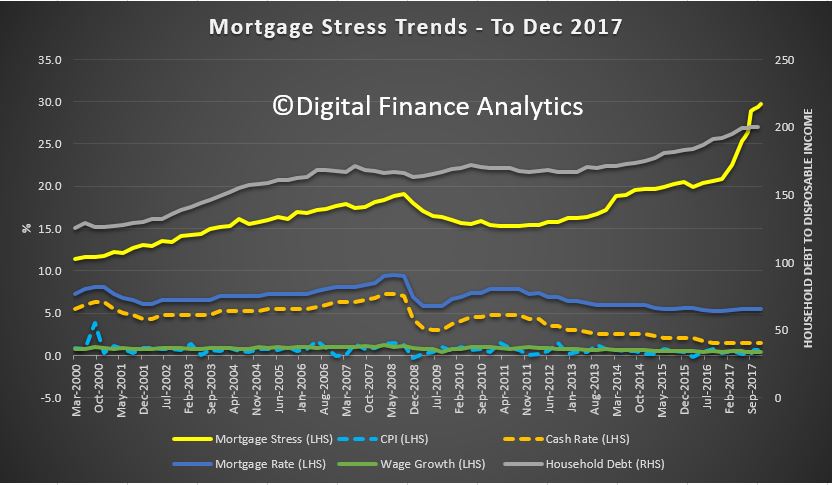

Despite the “good news” from the GDP numbers yesterday, our latest mortgage stress report, to end August 2018 continues to track higher.

The latest RBA data on household debt to income to March reached a new high of 190.1[1]. On Tuesday, the RBA said ”One continuing source of uncertainty is the outlook for household consumption. Household income has been growing slowly and debt levels are high”; and last week “the main risks to financial stability will most likely continue to relate to credit quality. Notably, banks’ large exposure to a potential deterioration in housing loan performance is expected to remain a key issue”.

Our analysis of household finance confirms this and the latest responsible lending determinations also highlight the issues.

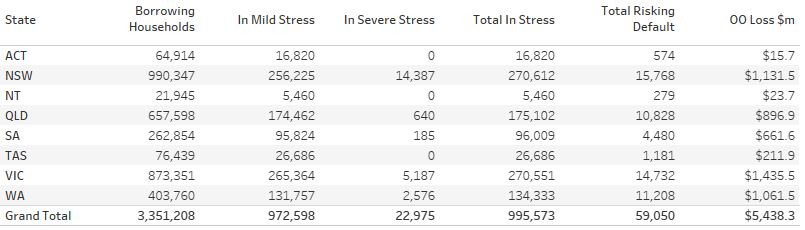

So no surprise to see mortgage stress continuing to rise. Across Australia, more than 996,000 households are estimated to be now in mortgage stress (last month 990,000). This equates to 30.5% of owner occupied borrowing households. In addition, more than 23,000 of these are in severe stress. We estimate that more than 59,000 households risk 30-day default in the next 12 months. We continue to see the impact of flat wages growth, rising living costs and higher real mortgage rates. Bank losses are likely to rise a little ahead.

Recent events, such as the lift in some mortgage rates, the latest council rate demands, rising fuel costs and flat incomes continue to hit home”. In addition, as home prices are falling in some post codes, the threat of negative equity is now rearing its ugly head.

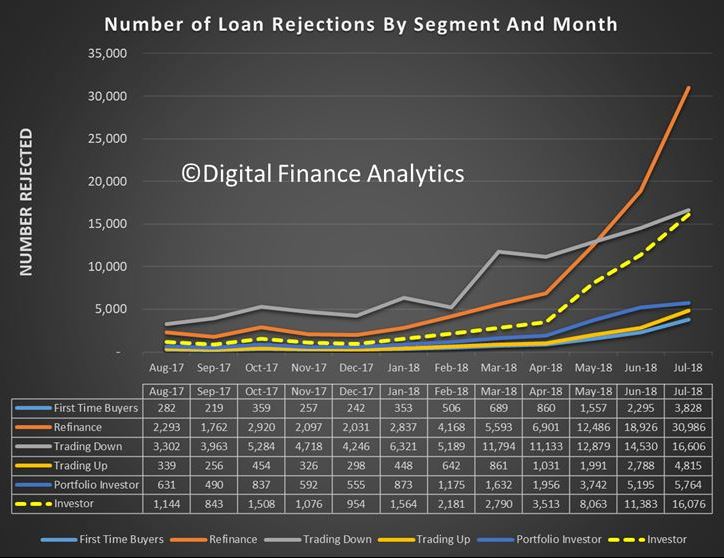

The fact that significant numbers of households have had their potential borrowing power crimped by lending standards belatedly being tightened, and are therefore mortgage prisoners, is significant. As we reported recently, up to 40% of those seeking to refinance are now having difficulty. This is strongly aligned to those who are registering as stressed. These are households urgently trying to reduce their monthly outgoings.

Continued rises in living costs – notably child care, school fees and fuel – whilst real incomes continue to fall and underemployment is causing significant pain. Many are dipping into savings to support their finances. The June 2018 household savings ratio, just reported, shows a further fall, at 1%. The ABS says [2] “moderate growth in household disposable income coupled with strength in household consumption resulted in a decline in the household saving ratio to 1.0 per cent, recording its lowest rate since December 2007”.

Our analysis uses the DFA core market model which combines information from our 52,000 household surveys, public data from the RBA, ABS and APRA; and private data from lenders and aggregators. The data is current to end August 2018. We analyse household cash flow based on real incomes, outgoings and mortgage repayments, rather than using an arbitrary 30% of income.

Households are defined as “stressed” when net income (or cash flow) does not cover ongoing costs. They may or may not have access to other available assets, and some have paid ahead, but households in mild stress have little leeway in their cash flows, whereas those in severe stress are unable to meet repayments from current income. In both cases, households manage this deficit by cutting back on spending, putting more on credit cards and seeking to refinance, restructure or sell their home. Those in severe stress are more likely to be seeking hardship assistance and are often forced to sell.

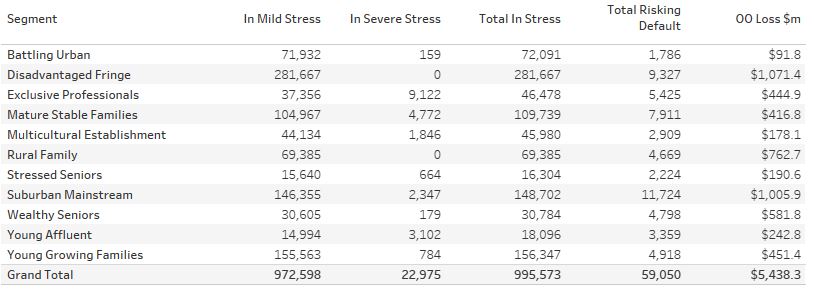

Probability of default extends our mortgage stress analysis by overlaying economic indicators such as employment, future wage growth and cpi changes. Our Core Market Model also examines the potential of portfolio risk of loss in basis point and value terms. Losses are likely to be higher among more affluent households, contrary to the popular belief that affluent households are well protected. This is shown in the segment analysis below:

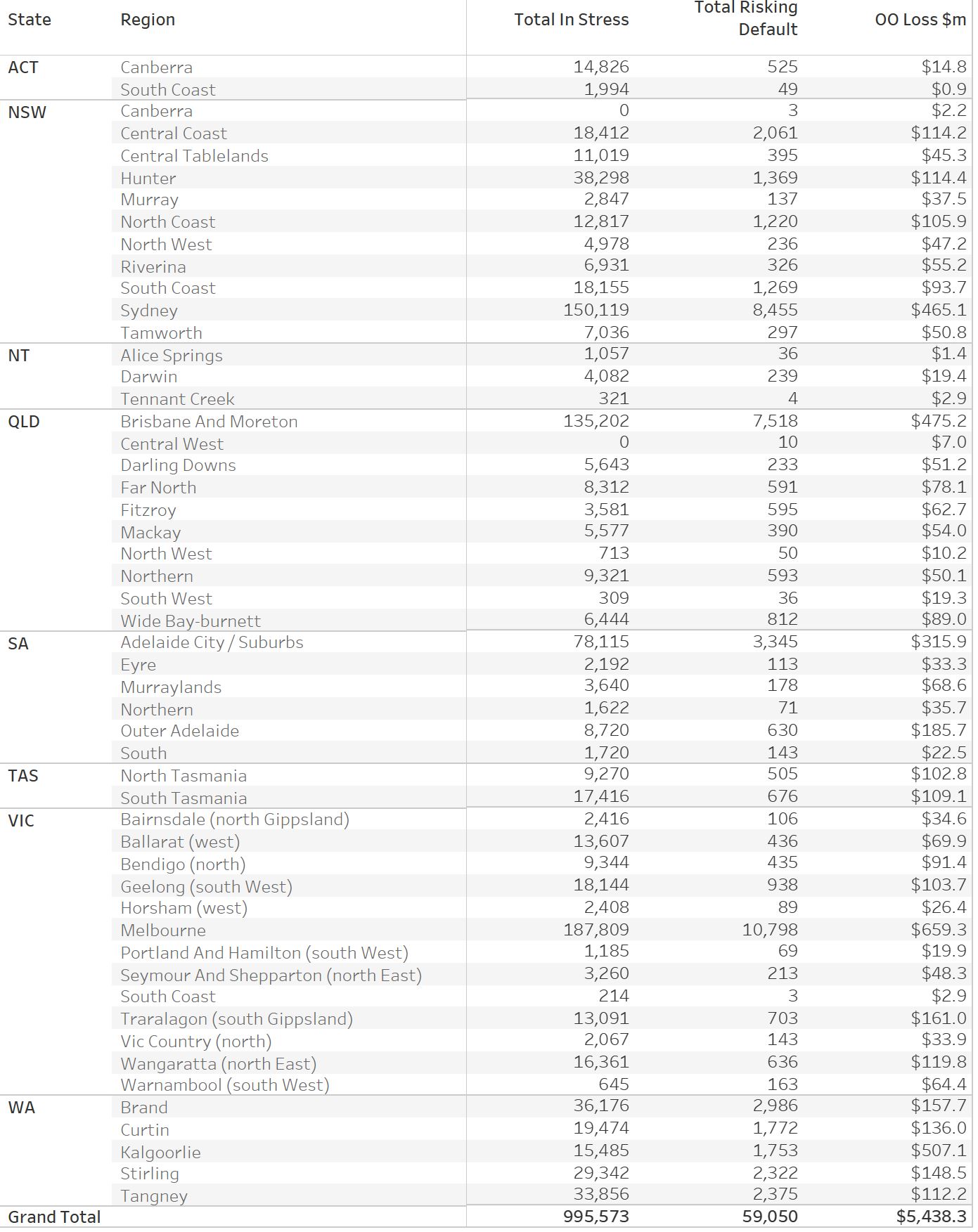

Stress by The Numbers.

Regional analysis shows that NSW has 270,612 households in stress (267,298 last month), VIC 270,551 (279,207 last month), QLD 175,102 (174,137 last month) and WA has 134,333 (132,035 last month). The probability of default over the next 12 months rose, with around 11,200 in WA, around 10,800 in QLD, 14,700 in VIC and 15,800 in NSW.

The largest financial losses relating to bank write-offs reside in NSW ($1.1 billion) from Owner Occupied borrowers) and VIC ($1.43 billion) from Owner Occupied Borrowers, though losses are likely to be highest in WA at 5.1 basis points, which equates to $744 million from Owner Occupied borrowers.

The Numbers in Context (Responsible Lending).

As indicated in our report last month, mortgage stress does not occur in a vacuum. The revelations from the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (the Commission) have highlighted deep issues in the regulatory environment that have contributed to the household debt “stress bomb”. The Commission will report on an interim basis this month and its commentary on the finance sector and the regulatory structure are likely to be scathing.

Gill North, a principal of DFA and a professor of law at Deakin University “does not expect the Commission to propose major reforms to the responsible lending rules. Instead, she predicts the Commission will consider a range of mechanism to enhance compliance with the existing rules. Conversely, Gill expects the Commission will recommend significant reforms to the law governing mortgage brokers, including some form of best interest duty that requires credit intermediaries to prioritise the interests of the customer when potential conflicts arise.”

The Commission is unlikely to change the responsible lending rules because these regimes have been successfully enforced by ASIC, including actions against the largest banks. For example, in early 2018, a case against the Australia and New Zealand Banking Group was successful, and on the 4th September an action against Westpac was settled prior to the commencement of the court hearing.

In the case against ANZ, the Federal Court found that in respect of 12 car loan applications from three brokers, ANZ failed to take reasonable steps to verify the income of the consumer and relied solely on purported pay slips in circumstances where ANZ knew that the pay slips were a type of document that was easily falsified. The Court indicated that ‘income is one of the most important parts of information about the consumer’s financial situation in the assessment of unsuitability, as it will govern the consumer’s ability to repay the loan’.

The litigation against Westpac concerned the use of an automated decision system to assess home loans during the period December 2011 and March 2015. Under this automated system, Westpac used a benchmark Household Expenditure Measure when assessing approximately 50,000 home loans, instead of actual expense information, and in these instances, the actual expenses were higher than the benchmark estimate. In addition, for approximately 50,000 home loans, Westpac used the incorrect method when assessing a consumer’s capacity to repay a home loan at the end of the interest-only period. Westpac has admitted contraventions of the National Consumer Credit Protection Act 2009 (Cth) and the parties have submitted a statement of agreed facts to the Federal Court.

These cases and other responsible lending actions consistently confirm the need for all lenders to collect and verify a customer’s actual income and expenses. The nature and scope of these obligations are highlighted in ASIC’s Regulatory Guide 209 on responsible lending conduct. This regulatory guide indicates that the obligation for lenders to make reasonable inquiries is scalable and the steps required will vary. For example, more extensive inquiries are necessary when potential negative consequences for the consumer are great, the credit contract has complex terms, the consumer has limited capacity to understand the contract, or when the consumer is a new customer.

[1] RBA E2 Household Finances – Selected Ratios March 2018

You can request our media release. Note this will NOT automatically send you our research updates, for that register here.

[contact-form to=’mnorth@digitalfinanceanalytics.com’ subject=’Request The August 2018 Stress Release’][contact-field label=’Name’ type=’name’ required=’1’/][contact-field label=’Email’ type=’email’ required=’1’/][contact-field label=’Email Me The August 2018 Media Release’ type=’radio’ required=’1′ options=’Yes Please’/][contact-field label=”Comment If You Like” type=”textarea”/][/contact-form]

Note that the detailed results from our surveys and analysis are made available to our paying clients.

The RBA has released their Corporal Plan for 2018/2019. In the section on Financial Stability they call out specific risks in the home lending market, relating to credit quality.

During 2018/19 to 2021/22, the main risks to financial stability will most likely continue to relate to credit quality. Notably, banks’ large exposure to a potential deterioration in housing loan performance is expected to remain a key issue, requiring ongoing monitoring by both banks and regulators.

They also highlight the role of the Council of Financial Regulators (CFR), and the issues raised by the Productivity Commission and Royal Commission:

The Reserve Bank works with other regulatory bodies in Australia to foster financial stability. The Governor chairs the Council of Financial Regulators (CFR) – comprising the Reserve Bank, the Australian Prudential Regulation Authority (APRA), the Australian Securities and Investments Commission (ASIC) and the Australian Treasury – whose role is to contribute to the efficiency and effectiveness of regulation and the stability of the financial system. The Bank’s central position in the financial system, and its position as the ultimate provider of liquidity to the system, gives it a key role in financial crisis management, in conjunction with the other members of the CFR.

The Reserve Bank will continue working with the other CFR agencies to support financial stability. In the period ahead this will be informed by the Financial Sector Assessment Program review of Australia being conducted by the International Monetary Fund during 2018. The Bank and other CFR agencies

will also carefully consider the implications for the resilience of the financial sector arising from findings and recommendations of the final report of the Productivity Commission’s review of competition in the financial system, as well as the outcomes of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry. The Bank will also continue working with APRA and with other regulators to monitor and, where necessary, respond to risks that may emerge from economic and financial shocks emanating from Australia or abroad.

I collaborated with https://valueofeverything.net/ in this video, in which I participated in a long form, free ranging interview about Australian housing, broader economic questions and global issues.

They did the editing and montage. I answered the questions. Recorded on 12 April 2018

Revelations of “flawed” lending practices uncovered by the royal commission could expose the property market to higher levels of risk, according to a research group.

RiskWise Property Research CEO Doron Peleg has claimed that the “flawed” provision of income and expense information identified by the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry could have an adverse effect on the Australian housing market.

“The banking royal commission has found the current processes for ensuring prospective home loan customers provide true information regarding their incomes, expenses and debts are flawed,” Mr Peleg said.

“This includes the details that are gathered by mortgage brokers, who generate about 50 per cent of the loans, regarding the living expenses customers provide in their home loan applications.”

Mr Peleg pointed to moves by the major banks to increase scrutiny on income and living expenses, making particular references to changes introduced by Westpac which require brokers to capture all living expenses under 13 categories.

The CEO claimed that such measures could lead to a sharp decline in lending activity.

“In the short term at least, this is likely to result in a lower volume of loans, as seen in the UK which had a 9 per cent drop in volume as a result of the 2014 Mortgage Market Review (MMR) to address lax lending standards,” the CEO continued.

“It is also likely that the duration to approve loans will be significantly increased, and significant reduction is projected in borrowing capacity (as per UBS, house borrowing capacity could be cut by 21 per cent to 41 per cent, depending on the borrowers’ income).”

Mr Peleg alleged that high-risk properties, which appeal to investors, would be most susceptible to a price correction if tightened lending standards are introduced.

“Investors often use creative financial planning, and they often place strong reliance on cash flow and negative gearing. Therefore, further scrutiny on property investors is likely to significantly reduce their borrowing capacity, and this will mean demand for such properties will be reduced,” the CEO added.

Further, the RiskWise executive noted that the higher-end property market would not be immune to such risks and could also be exposed to price correction.

“[Unaffordable] areas and properties at the top end of the market also carry a higher degree of risk, as many borrowers need to rely on the current borrowing capacity to purchase these properties.”

However, Mr Peleg noted that he expects capital cities experiencing strong economic and population growth, with properties that appeal to both owner-occupier investors, would be more likely to avert such risks.

As part of the discussion paper, released today APRA, says that addressing the systemic concentration of ADI portfolios in residential mortgages is an important element of the proposals. They have FINALLY woken up to the risks in the system, just years too late! We have significant numbers of loans in the system currently that would now not pass muster.

These proposals, which focus in on mortgage serviceability, would change the industry significantly, as lower risk loans will be more highly prized (so expect low rate offers for lower LVRs), whilst investment loans, and interest only loans are likely to cost more and be harder to find. Combined this could certainly move the market! The proposals introduce “standard” and “non-standard” risk categories.

The proposals are for consultation, with a closing data 18 May 2018.

As well as increasing the risk weights for some mortgages, they also continue to close the gap between the advanced (IRB) internal approach used by large lenders, and the standard approach used by smaller players. Those in transition (e.g. Bendigo Bank) may find less of an advantage in moving to advanced as a result.

Also they are proposing some simplification for small ADI’s as the cost of these measures may outweigh the benefit to prudential safety. Proportionate and tailored requirements for small ADIs could reduce regulatory burden without compromising prudential safety and soundness. Calibration of a simpler regime would be broadly aligned to the more complex regulatory capital framework, yet would be designed to suit the size, nature, complexity and risk of small ADIs.

Here are some of the key paragraphs from their paper.

APRA’s view is that there are potential systemic vulnerabilities to the financial system created from high levels of residential mortgage lending for investment purposes. As noted by the RBA, investment lending can amplify borrowing and house pricing cycles:

Periods of rapidly rising prices can create the expectation of further price rises, drawing more households in the market, increasing the willingness to pay more for a given property, and leading to an overall increase in household indebtedness.

Similarly, the significant share of interest-only housing lending, including to owner-occupiers, is a structural feature that increases the risk profile of the Australian banking system. Interest-only borrowers face a longer period of higher indebtedness, increasing the risk of falling into negative equity should housing prices fall. Borrowers may also use interest-only loans to maximise leverage, or for short-term affordability reasons. Even though loan servicing ability (serviceability) is now tested at levels that include the subsequent principal repayments, borrowers may face ‘payment shock’ when the interest-only period ends and regular repayments increase, in some cases significantly. This payment shock is particularly acute when interest rates are low.

Over the past two decades, residential mortgages in Australia as a share of ADIs’ total loans have increased significantly, from just under half to more than 60 per cent. While losses incurred on residential mortgage portfolios in this period have been limited, this level of structural concentration poses prudential and financial stability risks, particularly in an environment of high household debt, high property prices, weak income growth and strong competitive pressures among lenders. In such circumstances, households, individual ADIs and the broader banking sector are vulnerable to economic shocks.

Similar to other jurisdictions facing comparable risks, APRA has undertaken a series of actions to help contain the risks associated with ADIs’ residential mortgage portfolios. These actions include promoting significantly strengthened loan underwriting practices, increasing the amount of capital held by IRB ADIs for residential mortgage exposures and establishing benchmarks to moderate lending for property investment and lending on an interest-only basis. As set out in APRA’s July 2017 information paper on unquestionably strong capital, APRA also intends to further strengthen capital requirements for residential mortgage lending to reflect the concentration risk it poses to the banking sector.

A key focus is the appropriate capital requirement for investment and interest-only mortgage loans. Although, as a class, investment loans have typically performed well under normal economic conditions in Australia, this segment has not been tested in a nationwide downturn. Further, an increasing proportion of highly indebted households own investment property relative to past economic cycles. Experience in the United Kingdom and Ireland during the global financial crisis, for example, showed that previously better-performing investment loans can fall into arrears in higher volumes than loans to owner-occupiers in times of stress.

So now they propose to target higher-risk residential mortgage lending, balanced against the need to avoid undue complexity. Under the proposals, residential mortgage exposures would be segmented into the following categories with different capital requirements applying to each segment:

loans meeting serviceability requirements made to owner-occupiers where the borrower’s repayment is on a principal and interest (P&I) basis;

loans meeting serviceability requirements made for investment purposes or where the borrower’s repayment is on an interest-only basis; and

other residential property exposures, including those that do not meet serviceability requirements.

Specifically, for the standard approach, APRA proposes that APS 112 would require ADIs to designate as non-standard eligible mortgages those where the ADI:

did not include an interest rate buffer of at least two percentage points and a minimum floor assessment interest rate of at least seven per cent in the serviceability methodology used to approve the loan;

did not verify that a borrower is able to service the loan on an ongoing basis (i.e. positive net income surplus); and

approved the loan outside the ADI’s loan serviceability policy.

APRA is also considering excluding certain other categories of loans considered higher risk from the definition of standard eligible mortgages, such as those with very high multiples of a borrower’s income.

APRA proposes to formalise through amendments to APS 112 its existing requirement that loans to self-managed superannuation funds secured by residential property should be treated as non-standard loans, reflecting the relative complexity of these loans and the fact that ADIs do not have recourse to other assets of the fund or to the beneficiary.

APRA also proposes that reverse mortgages, which are currently risk-weighted at 50 per cent (where LVR is less than 60 per cent) or 100 per cent (for LVRs over 60 per cent), would be treated as non-standard in light of the heightened operational, legal and reputational risks associated with these loans.

Subject to final calibration, APRA proposes that all non-standard eligible mortgages would be subject to a risk weight of 100 per cent.

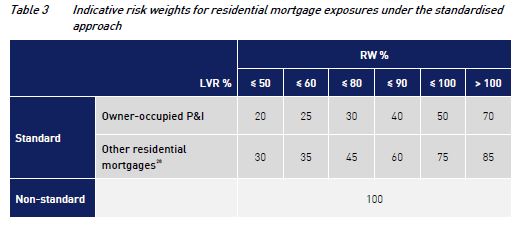

APRA proposes to segment the standard eligible mortgage portfolio into lower-risk and higher-risk exposures in addition to assigning risk weights according to LVR. This approach is aligned to, but deliberately not strictly consistent with, the Basel III ‘material dependence’ concept, to appropriately reflect Australian conditions.

For the lower-risk segment, APRA proposes to broadly align the risk weights with those under the Basel III framework loans where repayments are not materially dependent on cash flows generated by the property securing the loan. This category would include owner-occupied P&I loans and would apply after consideration of any lenders mortgage insurance (LMI).

The higher-risk segment would include interest-only loans, loans for investment property and loans to SMEs secured by residential property. The determination of higher risk weights for this segment would be either by way of a fixed risk-weight schedule, or a multiplier on the risk weights applied to owner-occupied P&I loans. The benefit of a multiplier is that APRA could more easily vary the capital uplift for these higher risk loans over time depending on prevailing prudential or financial stability objectives or concerns.

Table 3 shows the indicative proposed risk-weight schedule based on the Basel III risk weights for materially dependent residential mortgage exposures.

APRA is also considering whether exposures to individuals with a large investment portfolio (such as those with more than four residential properties) would be treated as non-standard residential mortgage loans or as loans secured by commercial property. APRA invites feedback on this issue.

APRA expects to continue to incorporate relatively lower capital requirements in the standardised approach for exposures covered by LMI. LMI can reduce the risk of loss for an ADI, subject to meeting the insurer’s conditions for valid claims and the financial capacity of the LMI to pay claims. APRA is considering the appropriate methodology to recognise LMI in the capital framework for both the standardised and IRB approaches. For the standardised approach to credit risk, APRA expects that any capital benefit would continue to apply to loans with an LVR over 80 per cent. APRA’s preferred approach is to increase the Table 3 risk weights (as finally calibrated) for standard loans with an LVR over 80 per cent that do not have LMI. For the IRB approach, APRA is considering potential options for the recognition of LMI.

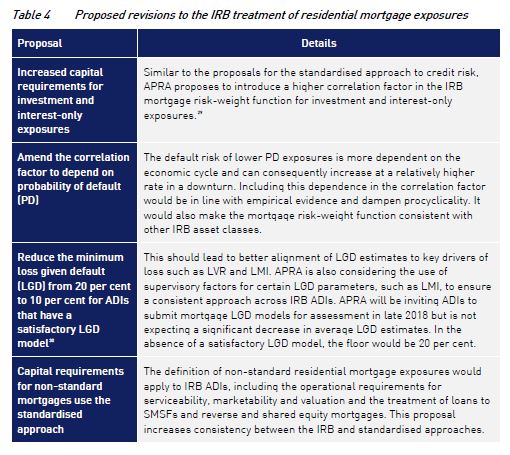

For IRB Bank (those using their own internal models, APRA believes that material changes are required in Australia in order to:

improve the alignment of capital requirements with risk for particular exposures;

further address the FSI recommendation that the difference in average mortgage risk weights between the standardised and IRB approaches is narrowed; and

ensure an appropriate overall calibration of capital for residential mortgage exposures given the concentration of IRB ADI portfolios in this segment.

On their own, however, these IRB mortgage risk-weight functions are not expected to result in a sufficient level of capital to meet APRA’s objectives for increased capital for residential mortgage exposures. However, any further increase in correlation for the IRB mortgage risk-weight function creates inconsistencies with correlation factors for other asset classes.

As a result, other adjustments are likely to be necessary to meet unquestionably strong capital expectations. For residential mortgages, this is expected to be through additional RWA overlays on top of the outputs of the IRB risk-weight function, including both an overlay specifically for residential mortgages and an overlay for total RWA.

The exact form and size of these overlays will be determined after APRA has completed its QIS analysis. In determining final calibration of the regulatory capital requirement for residential mortgage exposures, APRA will consider the appropriate difference in the average risk weights under the IRB and standardised approaches, consistent with recommendation 2 of the FSI. As detailed in the final report of the FSI, given the IRB approach is more risk sensitive, some difference between the average risk weights for residential mortgage exposures under the different approaches to credit risk may be justified; however, it should not be of a magnitude to create unwarranted competitive distortions.

SME exposures secured by residential property that meet certain serviceability criteria would be included in the same category of exposures as residential mortgages for investment purposes and interest-only loans.

In APRA’s experience, these exposures have historically had higher losses than non-SME owner-occupier residential mortgage exposures.

For SME exposures that are not secured by property, APRA proposes to reduce the 100 per cent risk weight currently applied under APS 112 to 85 per cent. This gives some recognition to the various types of collateral, other than property, that SMEs provide as security. APRA does not propose to implement the Basel III 75 per cent risk weight for retail SME exposures, as there is insufficient empirical evidence that retail SME exposures in Australia exhibit a lower default or loss experience through the cycle than corporate SME exposures. SME exposures in this category would be limited to corporate entities where consolidated group sales are less than or equal to $50 million.

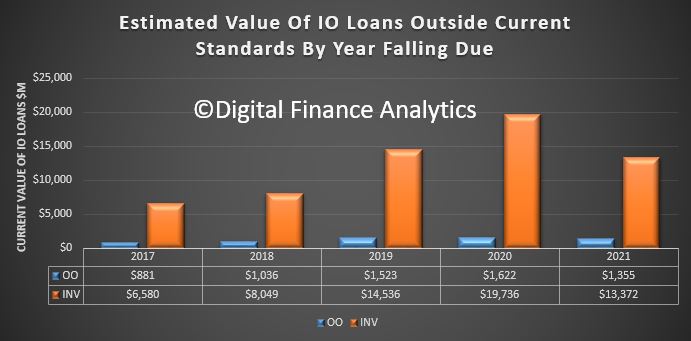

The Australian Financial Review featured some of our recent research on the problem of refinancing interest only loans (IO). Many IO loan holders simply assume they can roll their loan on the same terms when it comes up for periodic review. Many will get a nasty surprise thanks to now tighter lending standards, and higher interest rates. Others may not even realise they have an IO loan!

Thousands of home owners face a looming financial crunch as $60 billion of interest-only loans written at the height of the property boom reset at higher rates and terms, over the next four years.

Monthly repayments on a typical $1 million mortgage could increase by more than 50 per cent as borrowers start repaying the principal on their loans, stretching budgets and increasing the risk of financial distress.

DFA analysis shows that over the next few years a considerable number of interest only loans (IO) which come up for review, will fail current underwriting standards. So households will be forced to switch to more expensive P&I loans, assuming they find a lender, or even sell. The same drama played out in the UK a couple of years ago when they brought in tighter restrictions on IO loans. The value of loans is significant. And may be understated.

A few observations. ASIC in 2015, released a report that found lenders providing interest-only mortgages needed to lift their standards to meet important consumer protection laws. They identified a number of issues relating to bank underwriting practices. We would also make the point that despite the low losses on interest-only loans to date in Australia, in a downturn they are more vulnerable to credit loss.

Lenders need to throttle back new interest only loans. But this raises an important question. What happens when existing IO loans are refinanced?

Less than half of current borrowers have complete plans as to how to repay the principle amount.

Interest-only loans may seem like a convenient way to reduce monthly repayments, (and keep the interest charges as high as possible as a tax hedge), but at some time the chickens have to come home to roost, and the capital amount will need to be repaid.

Many loans are set on an interest-only basis for a set 5-year or 10-year term, at which point the lender is required to reassess the loan and to determine whether it should be rolled on the same basis. Indeed, the recent APRA guidelines contained some explicit guidance:

For interest-only loans, APRA expects ADIs to assess the ability of the borrower to meet future repayments on a principal and interest basis for the specific term over which the principal and interest repayments apply, excluding the interest-only period

But if households are not aware they have IO loans in the first place, then this raises the systemic risks to a whole new level. The findings from the follow-up study by UBS, after their “Liar-Loans” report (using their online survey of 907 Australians who recently took out a mortgage – they claim a sampling error of just +/-3.18% at a 95% confidence level) are significant.

They say their survey showed that only 23.9% of respondents (by value) took out an interest only loan in the last twelve months. This compares to APRA statistics which showed that 35.3% of loan approvals in the year to June were interest only.

They believe the most likely explanation for the lack of respondents indicating they have IO mortgages is that many customers may be unaware that they have taken out an interest only mortgage. In fact, around 1/3 of interest only borrowers do not know that they have this style of mortgage.

SMSF and accounting professionals alike are increasingly finding that clients are willing to take risky moves with their property portfolios, in an effort to reduce their mortgage stress. From SMSF Adviser.

These patterns are surfacing as instances of mortgage stress continue to climb significantly in Australian households. Research house Digital Finance Analytics (DFA) has released its mortgage stress and default analysis for December 2017, showing about 29.7 per cent of households — 921,000 — are under “mortgage stress.”

About 24,000 households are under “severe mortgage stress”, up by 3,000 from November 2017.

DFA principal Martin North believes the risk of default for Australians has increased for 2018, with an estimated 54,000 households currently at risk of 30-day debt defaults in the next 12 months.

Several accountants and financial advisers have told Accountants Daily that their clients, including high-net-worth property investors, are increasingly looking to take on more risk to sustain their levels of debt.

Director at Verante Financial Planning, and chair of the SMSF Association’s NSW state chapter, Liam Shorte, said he’s seen evidence of investors asking accountants to increase their reportable income to increase their borrowing capacity, usually where they need to refinance. Historically, clients have sought advice on how to minimise their reportable income for tax purposes.

He also told sister publication Accountants Daily that more clients are asking their parents to do a “family pledge,” or guarantee about 20 per cent of a loan to help reduce debt while refinancing.

For Lielette Calleja, director at bookkeeping firm All That Counts, mortgage stress is most pronounced with small business owners, and doesn’t necessarily only affect those at the lower end of the earning scale.

“I would have to say that small business owners are heavily affected. Your income is not always consistent, as opposed to being a PAYG. Mortgage stress is across the board I don’t believe it discriminates as it’s relative to each type of borrower. Property investors and high-net-worth individuals tend to be asset rich but lack cash flow until their development is complete and/or sold/leased out,” Ms Calleja told Accountants Daily.

Further, Ms Calleja is finding clients are modifying their behaviours and expenses to adjust to a new normal in household debt levels.

“Families that are not in a position to refinance are resorting to taking their kids out of private schools and foregoing luxury holidays, even simple things like making your own lunch instead of buying is becoming the Aussie way,” she said.

“Small business owners are coming to the conclusion that having good financials consistently all year round is critical in keeping their mortgage stress levels at bay,” she added.