Average income earners largely are the people who do get to take advantage of negative gearing – nurses, policemen and women on an average wage, investing, for instance, in a property. Most of them hold only one property, which adds to the housing stock that’s available for people as well. – Assistant Treasurer and Small Business Minister Kelly O’Dwyer, speaking on ABC TV’s Insiders, October 25, 2015

Negative gearing is a tax break available for people who own at least one other property in addition to their primary place of residence. This tax break applies only if the costs associated with the investment, including interest payments and other expenses, are greater than the rental income. Any loss made on the property can be offset against other income, thus reducing personal tax.

It’s true many nurses and police officers and other middle-income (and even much lower) people have negatively geared properties. But are these occupations and incomes the typical beneficiaries of negative gearing?

Checking the data

When asked for a source to support her statement, a spokesperson for O’Dwyer sent the following statistics.

• Taxation statistics show 66.5% of taxfilers who declare a net rental loss have a taxable income of A$80,000 or less.

• Those who use negative gearing include 22.6% of police officers, 19.2% of ambulance officers and paramedics, and 18.9% of train and tram drivers.

• Of the Australians who use negative gearing, the majority only hold one additional property.

• 73% of people with a rental property interest have only one property and 18% own two.

A$80,000 per year is not a typical taxable income. Around 84% of non-investors have a taxable income below $80,000. This compares with the 66.5% of people with negative geared property.

It is true that a relatively high proportion of the listed occupations have negatively geared properties. While it may be the popular belief that these are low or middle income occupations, these are actually reasonably highly paid occupations. For example, 73% of train and tram operators earn more than A$80,000 per year.

In our analysis, we looked at the income distribution of people who negatively gear compared to that of people who do not invest in rental properties.

The data set we used is called the 2012–13 individuals sample file. To collect this data, the Australian Taxation Office (ATO) sampled 2% of all individual tax returns filed in 2012-13.

According to this ATO data set, there are 1.26 million (10%) taxpayers who negatively gear. Their average loss was A$8,930 per year. A further 700,000 with a rental investment are positively geared (meaning their rental income was greater than their costs). About 85% of taxpayers don’t have a rental investment.

The chart shows what statisticians call the “smoothed” probability distribution (which is a smoothed histogram of the income distribution) of taxable income for people with negatively geared properties and people without rental investment properties. Marked also on the chart are the median and top 10% (P90) income points for both people with negatively geared properties and those without property investments.

The median income for negatively geared investors is A$60,000 per year, compared with $40,000 for non-investors.

A similar gap (50%) exists at the top end of the income spectrum. The taxable incomes of the top 10% of earners with negatively geared investments is around $150,000 compared to $98,000 for non-investors.

The chart shows clearly that, typically, people with negatively geared properties have significantly higher incomes than people without property investments.

In an April 2015 analysis commissioned by GetUp! for the Australia Institute, NATSEM found that 34% of the tax benefits of negative gearing accrues to the richest top 10% of families, as this chart from the report shows.

Only around 20% of the tax benefits go to the bottom half of the income distribution.

High-income families invest more money than low-income families. The tax system benefits high-income earners more than low-income earners due to higher marginal tax rates amplifying the effectiveness of deductions.

The role of capital gains

Negatively gearing property implies that the investor is making a loss on their investment. As the chart below shows, the tax savings are greatest among those in the higher tax brackets. However, it remains the case that these investors continue to make an overall loss on their investment, even after accounting for tax deductions.

The success of negative gearing as an investment strategy is reliant upon capital gains. In a property upswing, this strategy can be highly successful with lucrative gains on often minimal equity investment. During a property downswing or period of limited price growth, these strategies are very poor investments.

A recent analysis by the Grattan Institute shows that while police and nurses do invest in property, it is the higher-income occupations, such as doctors and mining engineers, who are much more likely to invest.

Adding to the housing stock?

Property investment only improves housing affordability when the purchase adds to the stock of newly constructed dwellings in affordable housing.

According to CoreLogic RP Data, in 2014 there were just under 500,000 property transactions and ABS building completions data suggest only around a third of those were newly built dwellings. It therefore stands to reason that most property transactions each year are probably existing stock.

Verdict

O’Dwyer’s assertion is not supported by the data. ATO data shows that, typically, negatively geared investors have higher incomes than people without rental investments.

The same data shows that negatively geared investors have typical incomes around 50% higher than non-investors – even after deducting their losses from negative gearing.

The top 10% of the income distribution for negatively geared investors earn around 50% more than non-investors. Incomes for this top 10% are around $150,000 per year, compared with $98,000 for non-investors, according to the ATO. – Ben Phillips and Cukkoo Joseph

Review

While I agree with everything in the above FactCheck, I would go further in criticising Kelly O’Dwyer’s statement, particularly the reference to investors adding to the housing stock.

The figure cited above for the ratio of housing purchases for new housing stock includes owner occupiers.

The impact on housing stock is tiny, but the effect on housing affordability of all those investors bidding up the prices of existing housing is likely to be substantial. – Warwick Smith

Authors: Ben Phillip, Principal Research Fellow, National Centre for Social and Economic Modelling (NATSEM), University of Canberra; Cukkoo Josep, Research Assistant, University of Canberra.

Reviewer, Warwick Smith,Research economist, University of Melbourne

As we round out the household segmentation analysis contained in the recently released Property Imperative report, today we look at residential property investment via a self managed superannuation fund.

APRA reports that Self-Managed Superannuation funds held assets were $589 billion at June 2015, a fall from $600 billion in March 2015.

Throughout the survey we noted an interest in investing in residential property via a self-managed superannuation funds (SMSFs). It is feasible to invest if the property meets certain specific criteria. In August the Government said such leveraged investments had their support, although the FSI inquiry had suggested such leverage should be banned. The rationale for this earlier recommendation was to prevent the unnecessary build-up of risk in the superannuation system and the financial system more broadly and fulfill the objective for superannuation to be a savings vehicle for retirement income, rather than a broader wealth management vehicle. Is this something which the Turnbull government might revisit?

Overall our survey showed that around 3.35% of households were holding residential property in SMSF, and a further 3% were actively considering it . Of these, 33% were motivated by the tax efficient nature of the investment, others were attracted by the prospect of appreciating prices (26%), the attractive finance offers available (15%), the potential for leverage (12%) and the prospect of better returns than from bank deposits (10%).

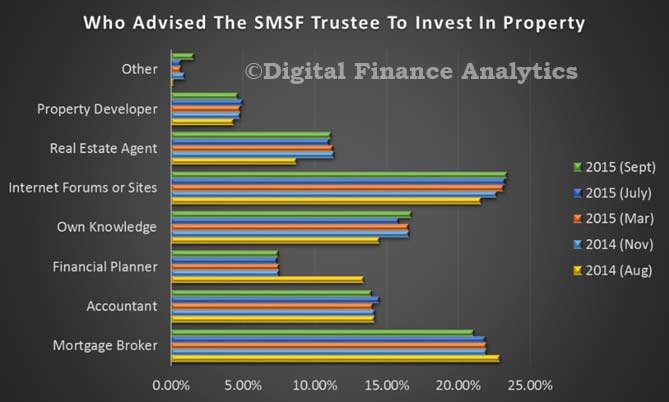

We explored where SMSF Trustees sourced advice to invest in property, 21% used a mortgage broker, 23% online information, 11% a Real Estate Agent, 14% Accountant, and 7% a Financial Planner. Financial Planners are significantly out of favour in the light of recent bank disclosures and ASIC publicity on poor advice.

The proportion of SMSF in property was on average 34%.

According to the fund level performance from APRA to June 2015, and DFA’s own research, Superannuation has become big business, with total assets now worth over $2 trillion (compare this with the $5.5 trillion in residential property in Australia), an increase of 9.9 % from last year.

In the RBA’s submission to the Inquiry on Home Ownership, they argue that negative gearing for investment property should be reviewed, because it has the potential to raise risks in the market, lift prices and distort the market.

Housing, particularly owner-‐occupied housing, receives preferential taxation treatment in many countries, and Australia is no exception. Australia’s taxation system is also relatively generous to small investors in buy-‐to-‐let property compared with some other countries, because investors can deduct losses from their investments against wage income as well as other property income, and because capital gains are taxed at concessional rates. However, there are some other countries where the tax preference for investor property is even stronger than in Australia.

Geared investment increases with age and income, though we should be cautious, as the ATO data is of course income for tax purposes, post offsets.

The Bank believes that there is a case for reviewing negative gearing, but not in isolation. Its interaction with other aspects of the tax system should be taken into account. The ability to deduct legitimate expenses incurred in the course of earning income is an important principle in Australia’s taxation system, and interest payments are no exception to this. To the extent that negative gearing induces landlords to accept a lower rental yield than otherwise (at least while continued capital gains are expected), it may be helpful for housing affordability for tenants. It is worth noting, however, that the interaction of negative gearing with other parts of the taxation system may have the effect of encouraging leveraged investment in property.

Interesting given the UK budget announcement last week to reduce negative gearing there, for the same reasons. So, is economic logic and political positioning pulling in two different directions? The evidence that removal of negative gearing would drive rents up is shaky at best, and the weight of argument is definitely for reform.

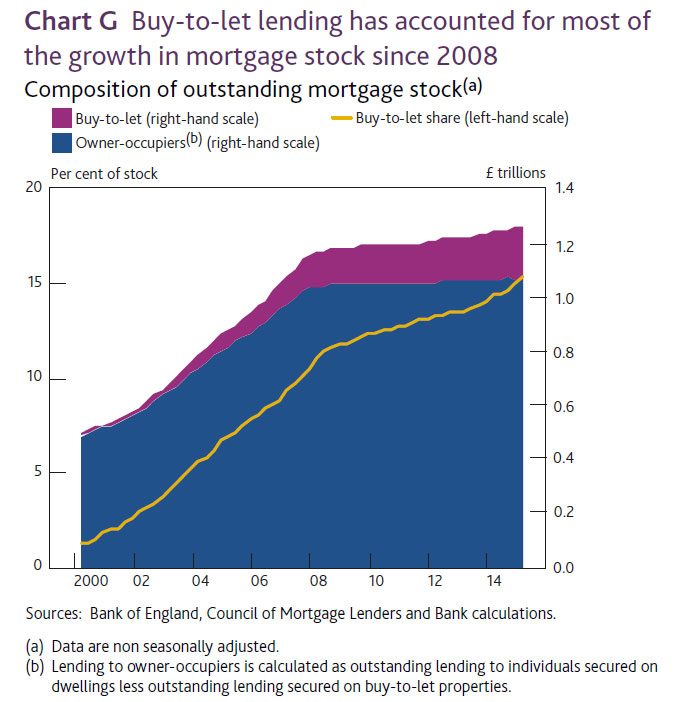

This week the UK Chancellor, George Osborne delivered his latest budget. One strong theme was the need to reduce the bias towards buy-to-let property investors against owner occupied purchasers. Currently, landlords can claim tax relief on monthly interest repayments at the top level of tax they pay of 45 per cent. Mortgage interest relief is estimated to cost £6.3billion a year. Buy-to-let lending has accounted for more than 15% of mortgages taken out – compared with 50% of new mortgages in Australia. The UK has seen the proportion grow by 8% in recent years.

“First, we will create a more level playing-field between those buying a home to let, and those who are buying a home to live in. Buy-to-let landlords have a huge advantage in the market as they can offset their mortgage interest payments against their income, whereas homebuyers cannot. And the better-off the landlord, the more tax relief they get. For the wealthiest, every pound of mortgage interest costs they incur, they get 45p back from the taxpayer. All this has contributed to the rapid growth in buy-to-let properties, which now account for over 15% of new mortgages, something the Bank of England warned us last week could pose a risk to our financial stability. So we will act – but we will act in a proportionate and gradual way, because I know that many hardworking people who’ve saved and invested in property depend on the rental income they get. So we will retain mortgage interest relief on residential property, but we will now restrict it to the basic rate of income tax. And to help people adjust, we will phase in the withdrawal of the higher rate reliefs over a four year period, and only start withdrawal in April 2017”.

So now, this will change, in a move which will ‘level the playing field for homebuyers and investors’, according to the Chancellor, the amount landlords can claim as relief will be set at the basic rate of tax – currently 20 per cent. The change will be tapered in over the next four years. The expectation is that as a result more first time buyers will be able to enter the market.

The Bank of England recently said it would monitor buy-to-let lending more closely, and analysts are concerned about the potential impact should UK rates rise, even with the current incentives in place. A record of a June 24 meeting of the BoE’s Financial Policy Committee shows the bank asked staff to gather evidence for the government consultation later this year, and to look at what action it could take before gaining further formal powers. Last week the Bank of England warned that a surging buy-to-let market could pose a risk to financial stability as landlords are potentially more vulnerable to rising interest rates.

that for a given LVR defaults are higher on investment loans

investors were an obvious driver of downturn defaults if they were identified as investors on the basis of being owners of multiple properties

a substantial fall in house prices would leave the investor much more heavily underwater relative to their labour income so diminishing their incentive to continue to service the mortgage (relative to alternatives such as entering bankruptcy)

some investors are likely to not own their own home directly (it may be in a trust and not used as security, or they may rent the home they live in), thus is likely to increase the incentive to stop servicing debt if it exceeds the value of their investment property portfolio

as property investor loans are disproportionately interest-only borrowers, they tend to remain nearer to the origination LVR, whereas owner-occupiers will tend to reduce their LVR through principal repayments. Evidence suggests that delinquency on mortgage loans is highest in the years immediately after the loan is signed. As equity in a property increases through principal repayments, the risk of a particular loan falls. However, this does not occur to the same extent with interest-only loans.

investors may face additional income volatility related to the possibility that the rental market they are operating in weakens in a severe recession (if tenants are in arrears or are hard to replace when they leave, for example). Furthermore, this income volatility is more closely correlated with the valuation of the underlying asset, since it is harder to sell an investment property that can’t find a tenant.

Reaction from the UK has been predictable, with claims the changes will put rents up, slow new property builds, and lead to a deterioration in the maintenance of existing rental property. In addition, some claim it will lead to landlord deciding to sell their property, releasing more into the market. Finally, there is debate about the comparison between investors and owner occupied property holders – Homeowners are not running businesses nor do they pay capital gains tax, for example, on disposal of their property.

That the UK is taking steps when 15% of property is buy-to-let should underscore the issues we have here when 35% of all mortgages are for investment property, and more than half of loans written last month were for investment purposes. This is bloating the banks balance sheets, inflating house prices, and making productive lending to businesses less available. The UK changes provides more evidence it is time to reconsider negative gearing in Australia

Last weekend the Property Council and the Real Estate Institute of Australia released a consultants’ report that tried to show renters would pay much more if generous tax concessions to landlords were wound back. So interesting to read an article by John Daley and Danielle Wood published by The Australian, Friday 3 July, and posted on the Institute website entitled “Rent rise fears are overstated”

With increasing public scrutiny of negative gearing and the capital gains tax discount at a time of rising budget pressures, the industry’s response was textbook: release an “independent” economic report alluding to frightening economic impacts and wait for an unquestioning media to breathlessly report them. As spooked tenants were rolled out lamenting hypothetical rent rises of $10,000 a year, no doubt the big developers congratulated themselves on a job well done.

But these misleading claims shouldn’t go untested. The report does not support the headline-grabbing $10,000-a-year rent rises. Rather, it suggests the immediate removal of negative gearing is likely to result in a portion of the average $9500 net rental loss being added to rental prices — without any attempt to define how large that impact may be.

The report’s use of the $9500 figure is highly misleading. This amount is the average loss deducted from tax for people with negatively geared investment properties. The report assumes these landlords will try to pass on some fraction of their higher tax costs by pushing up rents. But will they succeed? Many other landlords with investment properties that are profitable and therefore don’t qualify for negative gearing won’t be paying higher taxes. Tenants will try to beat rent rises by threatening to move. So competition in rental markets will limit material rent rises.

In any case, current rents are ultimately a consequence of the balance between demand and supply for rental housing. In property markets — as in other markets — returns determine asset prices, not the other way around. Rents don’t increase just to ensure that buyers of assets get their money back.

Some investors may sell their properties if tax concessions are less generous. This may reduce house prices, but it will not increase rents. Every time an investor sells a property, a current renter buys it, so there is one less rental property and one less renter, and no change to the balance between supply and demand of rental properties.

Claims that removing negative gearing will push up rents often rest on a folk memory of increasing rents in Sydney between 1985 and 1987. But as proper examination of that history shows, real rents didn’t increase in Melbourne, Brisbane and Adelaide. Other factors drove the Sydney rent rise.

The industry report argues negative gearing boosts the supply of new rental properties. But 93 per cent of all investment property lending is for existing dwellings. As the report itself points out, the main constraint on the supply of new housing is land release and zoning restrictions, not the profitability of developments. Providing tax concessions in this supply-constrained environment mainly just bids up prices for the limited new supply.

The other argument the industry advances is that “ordinary Australians” use negative gearing. Once again the numbers it uses are highly misleading. Its report shows that those with taxable incomes under $80,000 claim most tax benefits from negative gearing for property — 58 per cent of the rental losses. But people who are negatively gearing have lower taxable incomes because they are negatively gearing. Correcting for this by assessing income before rental loss deductions shows that less than one-third of rental losses are claimed by people with incomes below $80,000.

In other words, taxpayers with incomes more than $80,000 — the top 20 per cent of income earners — claim almost 70 per cent of the tax benefits of negative gearing. For capital gains, taxpayers with incomes of more than $80,000 capture 75 per cent of the gains. If we are trying to look after middle-income earners, then general changes to income tax rates would be fairer than allowing negative gearing for a small proportion of middle-income earners.

So why are the Property Council and the Real Estate Institute making such claims? Presumably because reforms would reduce the price of assets held by their members. They have a strong incentive to obscure how these tax benefits impose costs on other taxpayers, push home ownership further out of reach for young people and distort investment decisions.

Australia is one of few developed nations to allow full deductibility of losses against wage income. As other countries realise, negative gearing distorts investment decisions by allowing investors to write off losses at their marginal tax rate but pay tax on their capital gains at only half this rate. Investors who hold off selling until they are retired pay even less tax on their capital gains. As a result, investors favour assets that pay more in the way of capital gains and less in terms of steady income. It also makes debt financing of investment more attractive. It all leads to the leveraged and speculative investment of the Sydney property boom.

As well as restricting the deduction of investment losses against wage and salary income, the capital gains tax discount should also be reduced. The industry report argues capital gains should receive a discounted tax treatment to ensure the inflation component of gains is not taxed. But with inflation rates low relative to investment returns, the 50 per cent discount overcompensates most investors. The discount magnifies the tax advantages of capital gains over other investment income.

Yet despite the compelling arguments for change, it seems the industry’s aggressive lobbying efforts will be rewarded. The Treasurer and the Finance Minister have both defended negative gearing arrangements by warning, against all credible evidence, that change would bring higher rents. The message to lobby groups is clear: if you pay enough to “independent” consultants you may be able to buy favourable policy outcomes, irrespective of the costs to the community.

From The Conversation. In recent weeks, there have been signs sentiment may be changing around the contentious policy of negative gearing.

There are well-rehearsed arguments on both sides. Critics argue that the deduction of property losses from other sources of income (such as wages) is a tax shelter that imposes an unfair burden on other taxpayers. Defenders of the policy suggest that it is used by prudent savers to “get ahead”, and by high income individuals to lower unduly high tax burdens that blunt work incentives.

However, these arguments are tax policy concerns since taxpayers can negatively gear other financial investments such as shares. There are housing policy specific issues that instead warrant a focus on housing; three deserve particular attention.

The first is a familiar refrain. Given a fixed supply of land, negative gearing advantages property investors who are better able to out-bid other land users. Part of the tax break gets shifted into higher land and housing prices; some other users of land – first home buyers, for example – are “crowded-out”.

But a second reason, related to so-called tax “clientele effects” has been rarely mentioned. It is a more nuanced influence, yet it is important to an understanding of the supply side effects of reform in this area.

The Australian private rental housing stock is relatively large by international standards and mostly held by “mum and dad” investors. There are not enough high tax bracket investors willing and able to hold all the housing in this tenure. Lower tax bracket investors must be enticed into the market. These investors are often retirees looking for secure, regular flows of income, and are attracted to those segments of the market where rental yields are relatively high.

On the other hand, the appeal of property investment to the high tax bracket investor is that they can negatively gear the asset’s acquisition, yet an important part of the returns (capital gains) are lightly taxed compared to other types of investment income. The consequence is that high tax bracket investors crowd into segments of the market offering high capital growth but low rental yields. Low tax bracket investors concentrate in segments offering high rental yields but lower capital growth.

The removal of negative gearing is then likely to have supply side impacts that are not as straightforward as has been suggested in some of the media commentary. To be sure some high tax bracket investors will withdraw and as price pressures ease and rental markets tighten, rental yields will rise.

But those higher rental yields will prompt some growth in the number of low tax bracket investors, and especially so in today’s low interest rate environment. As low tax bracket investors face tighter borrowing constraints, the overall supply side impact will be negative. But it will not be the collapse in supply that some fear.

The third reason for change with respect to negative gearing and housing is perhaps the most important in the current context. The share of investment property loans in total debt has tripled from one-tenth to three-tenths in a little over two decades. Investors now take up a higher share of the value of new loans than do first home buyers.

According to the Australian Bureau of Statistics, investment housing accounted for 40% of the total value of housing finance commitments in April 2015. Of the dwellings that secured housing finance commitments within the owner occupation sector, only 15% was attributable to first home buyers. The presence of housing investors on such a large scale is a potential source of instability, especially if highly geared.

In their seminal research, the late Professor John Quigley and his colleague Karl Case note that when markets slump home owner behaviour differs from that of other investors.

They can “consume” the housing they have bought – by enjoying the surroundings and the comforts of home – and provided mortgage payments are met, they are invariably willing to “sit out” the slump. This can be an important source of stability in housing markets.

But property investors have not bought a dwelling to live in it. When prices slump some if not many will cut their losses and seek a safe haven for their capital elsewhere, especially if they are highly geared. Our research finds that negatively geared investors are more likely to terminate rental leases than equity-oriented investors. The former are also prone to churn in and out of rental investments as they refinance to preserve tax shelter benefits.

When large numbers of indebted investors come to bank on continued house price gains, and low interest rates, the resilience of housing markets is undermined. Phasing out negative gearing should be a priority for a housing policy fit for the 21st century.

Authors: Gavin Wood, Professor of Housing at RMIT University and Rachel Ong, Principal Research Fellow, Bankwest Curtin Economics Centre at Curtin University

ABC Fact Check investigates whether abolishing negative gearing in 1985 caused rents to surge. During the period negative gearing was abolished rents notably increased only in Sydney and Perth. Other factors, including high interest rates and the share market boom, were also contributors to rent increases at the time.

As property prices continue to rise across Australian capital cities, in particular Sydney, the debate around how to address housing affordability problems has intensified.

Sydney house prices have jumped more than 6 per cent since the beginning of the year, increasing pressure on first home buyers.

The Reserve Bank has raised concerns that “ongoing strong speculative demand” from property investors will exacerbate the run-up in housing prices and raise the risk of big price falls.

Negative gearing, a tax deduction for rental property investors, is an area of contention.

But Treasurer Joe Hockey says if negative gearing is abolished, there could be other serious consequences.

“If you abolish negative gearing on investment properties, there’s a strong argument that rents would increase,” Mr Hockey said on the ABC’s Q&A.

Mr Hockey said that in the 1980s, when negative gearing was briefly removed, there was a backlash from investors who increased rents to “replace the lost income” negative gearing had provided.

“The net result was you saw a surge in rents,” he said.

Mr Hockey has made similar claims a number of times in the past two months. On April 28 he said: “If you were to remove negative gearing you would see an increase in rents and I think that hurts lower income Australians who may be renting those homes.”

However, during the period that negative gearing was abolished real rents notably increased only in Sydney and Perth – where rental vacancies were at extremely low levels.

This is inconsistent with arguments that negative gearing was a significant factor, with negative gearing likely to have a uniform impact on rents in all capital cities.

At the same time, high interest rates and the share market boom of the mid 1980s increased consumer demand for rental properties, encouraged existing investors to pass on high mortgage costs to renting consumers, and discouraged additional investors from investing in the rental property market.

While the rent increases in two cities did coincide with the temporary removal of negative gearing tax deductions, it is unlikely that change had a substantial impact on rents in any major capital city in Australia.

The ABC The Business last night covered the property market, “The RBA’s Property Problem” – including comments from the RBA and APRA. Industry analysts also make the point that the tax incentives for investment property will work again the intention of macroprudential – we discussed negative gearing yesterday.

There is no doubt that negative gearing is a hot issue. As the ASIC Money Smart web site says:

Negative gearing is when your income from an investment is less than your expenses. In the case of property this means the rental income you receive is less than the interest and other expenses you pay. Your investment is making a loss which most investors hope they will make up with a capital gain when the value of the property increases. A loss can be used to reduce your taxable income which will reduce the amount of tax you pay. See the Australian Taxation Office’s section on residential rental properties for details of income you must declare and expenses you can claim. Remember, you are only reducing your tax payable because the income from your investment isn’t covering your expenses.

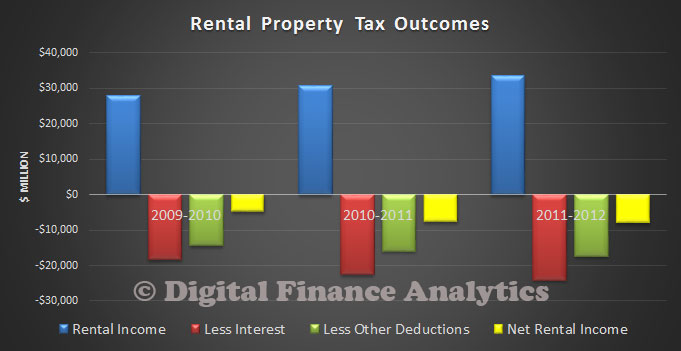

In the year to 2012, the ATO reported that whilst income from rental properties reached $33bn, the total tax offsets including interest costs were $49.6bn, leaving a net loss to the tax payer of $8bn. So, negative gearing costs. The chart below shows the trend for recent years. Well over 1.2 million households gear into property, and two in three reported a loss (to offset income elsewhere). The RBA’s Financial Stability Report, illustrated that the top fifth of income earners hold around 60 per cent of investment housing debt.

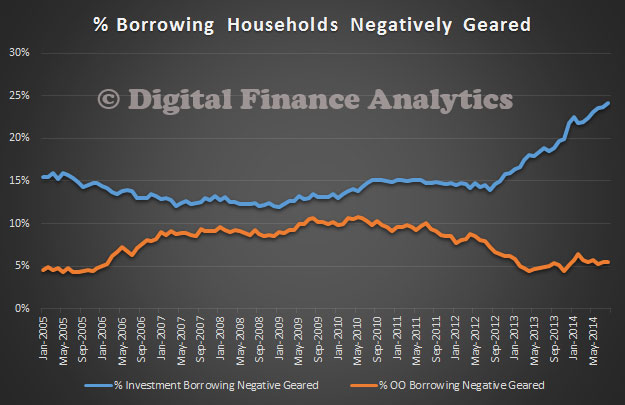

Now, many argue that negative gearing is essential to support house building and the rental sector, and should not be touched. However, the data tells a different story. We went back to our household surveys, to examine the penetration of gearing. First, we looked at those borrowing for owner occupation, versus for investment purposes. No surprise that more were property investors. However some owner occupied households also geared their property into, for example stock market investments. Recently, the growth in investment gearing has been much stronger. We already know this is being driven by expectations of future capital growth, as reported in our earlier posts.

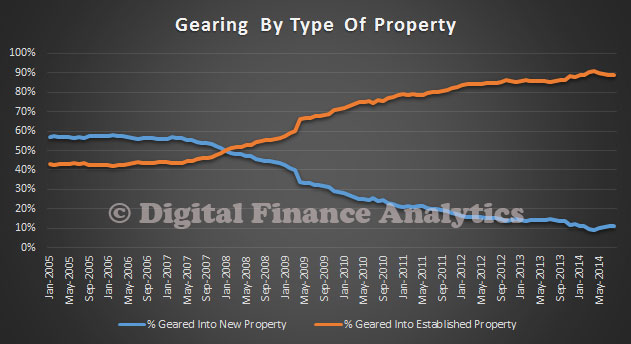

Then we looked at the type of property geared. We found that whilst a proportion were geared into new property, most were gearing into existing property, for rent.

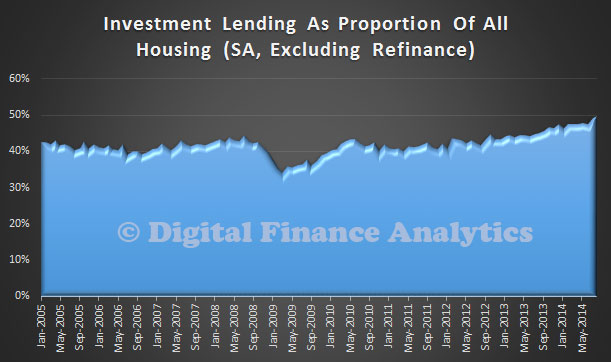

No surprise, given the growth in loans for investment purposes, and only a small proportion go towards new builds.

So, we conclude that gearing has more to do with stoking prices in the established market than directly stimulating new building. Rents are set as a combination of the costs of a property, and income levels. If prices were more realistic, rents would be lower, because loans would be lower. More rentals loose money than make money today, and the only saving grace in the minds of investors is hoped for future capital growth.

A more logical approach would be to focus, from this point forward negative gearing on new builds only, thus helping to boost supply and stabilise prices. Appropriate transition arrangements for existing gearing would be needed, but the current arrangements are not fair, and will become an even greater drain on government coffers if interest rates (and net rental losses) rise.