Productivity is going backward – why might that be? Is technology to blame?

Go to the Walk The World Universe at https://walktheworld.com.au/

Digital Finance Analytics (DFA) Blog

"Intelligent Insight"

Productivity is going backward – why might that be? Is technology to blame?

Go to the Walk The World Universe at https://walktheworld.com.au/

From The St. Louis Fed On The Economy Blog.

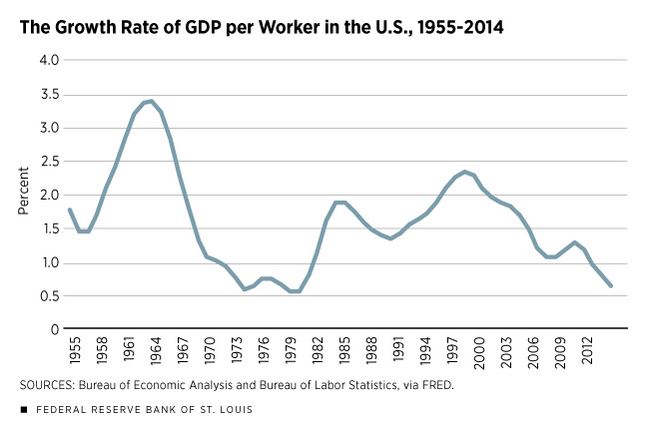

The U.S. economy is currently experiencing a prolonged productivity slowdown, comparable to another slowdown during in the 1970s.

Economists have debated the causes for these slowdowns: The reasons range from the 1970s oil price shock to the 2007-08 financial crisis.

But did the baby boom generation partly cause both periods of slowing productivity growth?

A Demographic Shift

Guillaume Vandenbroucke, an economist at the St. Louis Fed, explored the role of the baby boom generation—specifically, those born in the period of 1946 to 1957 when the birth rate increased by 20 percent—in these slowdowns.

In a recent article in the Regional Economist, he pointed out a demographic shift: Many baby boomers began entering the labor market as young, inexperienced workers during the 1970s, and now they’ve begun retiring after becoming skilled, experienced workers.

“This hypothesis is not to say that the baby boom was entirely responsible for these two episodes of low productivity growth,” the author wrote. “Rather, it is to point out the mechanism through which the baby boom contributed to both.”

Productivity 101

One measure of productivity is labor productivity, which can be measured as gross domestic product (GDP) per worker. By this measure, the growth of labor productivity was low in the 1970s. Between 1980 and 2000, this growth accelerated, but then has slowed since 2000.

“It is interesting to note that the current state of low labor productivity growth is comparable to that of the 1970s and that it results from a decline that started before the 2007 recession,” Vandenbroucke wrote.

How does a worker’s age affect an individual’s productivity? According to economic theory, young workers have relatively low human capital; as they grow older, they accumulate human capital, Vandenbroucke wrote.

“Human capital is what makes a worker productive: The more human capital, the more output a worker produces in a day’s work,” the author wrote.

The Demographic Link

Vandenbroucke gave an example of how this simple idea could affect overall productivity. His example looked at a world in which there are only young and old workers. Each young worker produces one unit of a good, while the older worker—who has more human capital—can produce two goods. If there were 50 young workers and 50 old workers in this simple economy, the total number of goods produced would be by 150, which gives labor productivity of 1.5 goods per worker.

Now, suppose the demographics changed, with this economy having 75 young workers and 25 old workers. Overall output would be only 125 goods. Therefore, labor productivity would be 1.25.

“Thus, the increased proportion of young workers reduces labor productivity as we measure it via output per worker,” he wrote. “The mechanism just described is exactly how the baby boom may have affected the growth rate of U.S. labor productivity.”

The Link between Boomers and Productivity Growth

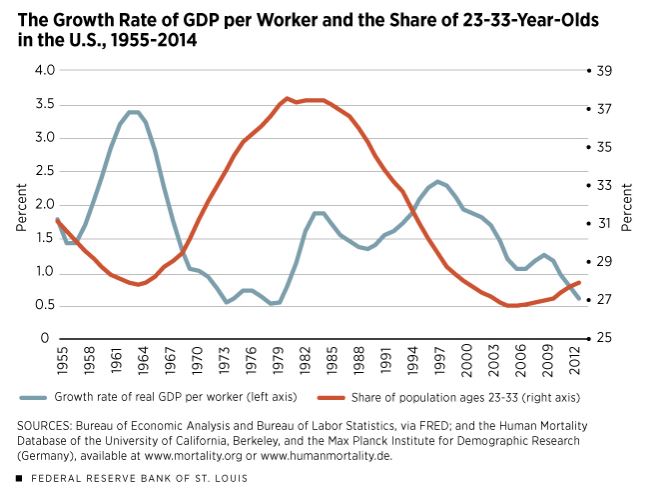

Vandenbroucke then compared the growth rate of GDP per worker (labor productivity) with the share of the population 23 to 33 years old, which he used as a proxy for young workers.

This measure of young workers began steadily increasing in the late 1960s before peaking circa 1980, which represented the time when baby boomers entered the labor force.

Looking at these variables from 1955 to 2014, he found the two lines move mostly in opposite directions (the share of young people growing as labor productivity growth declined) except in the 2000s.

(To see these trends, see the Regional Economist article, “Boomers Have Played a Role in Changes in Productivity.”)

“The correlation between the two lines is, indeed, –37 percent,” Vandenbroucke wrote.1

The share of the population who were 23 to 33 years old began to increase in the late 2000s, which can be viewed as the result of baby boomers retiring and making the working-age population younger.

“This trend is noticeably less pronounced, however, during the 2000s than it was during the 1970s,” the author wrote. “Thus, the mechanism discussed here is likely to be a stronger contributor to the 1970s slowdown than to the current one.”

Conclusion

If this theory is correct, it may be that the productivity of individual workers did not change at all during the 1970s, but that the change in the composition of the workforce caused the productivity slowdown, he wrote.

“In a way, therefore, there is nothing to be fixed via government programs,” Vandenbroucke wrote. “Productivity slows down because of the changing composition of the labor force, and that results from births that took place at least 20 years before.”

Notes and References

1 A correlation of 100 percent means a perfect positive relationship, zero percent means no relationship and -100 percent means a perfect negative relationship.

Silvana Tenreyro, External MPC Member, Bank of England, spoke on “The fall in productivity growth: causes and implications” as the 2018 Maurice Peston Lecture.

She explores the problem of low productivity since the GFC, and using UK data shows that the brake on productivity growth is from finance, manufacturing followed by ICT and services. But finance appears to be the number one sector causing the problem. It had the fastest-growing labour productivity of any sector in the run-up to the crisis, at 5% per year. Since 2009, productivity has actually shrunk by 2.1% per year. Indeed, key contributors to the crisis itself – risk illusion and increasing financial-sector leverage – may have increased (correctly measured) pre-crisis productivity growth.

Reading from this, as the finance sector continues to respond to pressure on margins, increased regulation, and lower growth, we think it will continue to be a brake on productivity, and it is possible that the growth of financial activities somehow crowded out the growth in the rest of the economy in a competition for talent and resources. Echoes of our recent discussion on Zombie firms! Relying more on the finance sector for growth looks like a problem.

Here is a summary of the speech.

Though commentators have referred to different measures of productivity, most have focused on aggregate labour productivity, defined as the total value added of the economy divided by the total number of hours worked.

Productivity matters for welfare. Over time and across countries, higher productivity is reliably associated with higher wages, higher consumption levels and improved health indicators.

Productivity is crucial to setting monetary policy. The MPC’s remit sets out a 2% inflation target over an appropriate time horizon with the rationale that inflation stability can lay the foundations for strong and sustainable growth. Productivity growth is the key determinant of how much demand can grow without creating inflation and hence it is a critical input into our forecast and deliberations.

The blue solid lines show a scenario where a 1% growth rate for potential productivity was overly pessimistic. The blue solid lines show a scenario where a 1% growth rate for potential productivity was overly pessimistic.

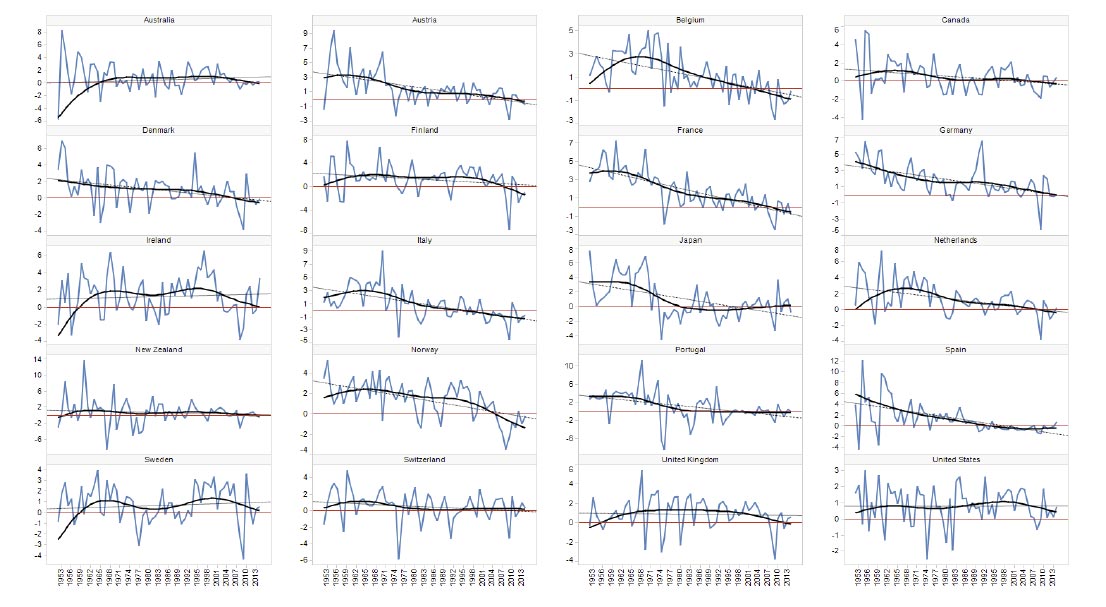

Over the three decades before the global financial crisis, productivity growth averaged 2.3% per year. Productivity fell in 2008 and 2009 as the financial crisis hit, and, in the seven years since, it has only grown by an average 0.4% per year. As a result, the typical worker in 2016, while still twice as productive as the 1970s, could only produce 1% more than in 2007.

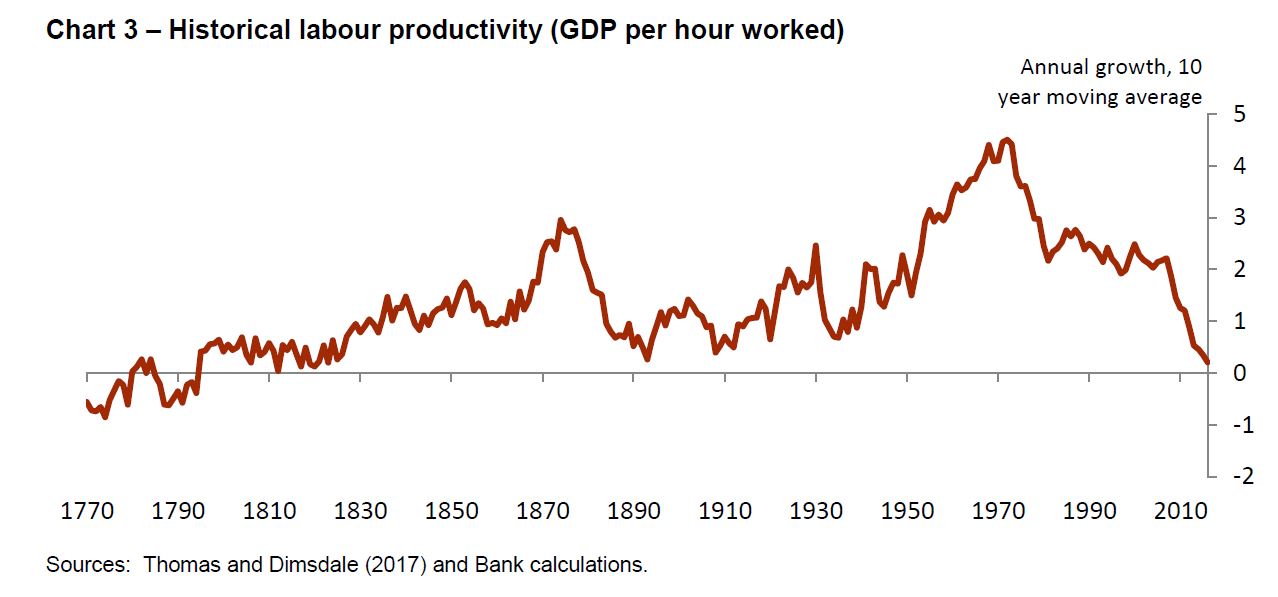

Focusing just on the past half-century, the decade since the crisis looks like an aberration. Productivity growth barely deviated from its 2% trend until 2007 (Chart 2). It is little wonder, therefore – looking at these data – that forecasters (the Bank of England included) consistently predicted that productivity growth would recover to a rate close to its 1970s-2000s average.

Over a longer sweep of history, the past decade is far from unusual. Chart 3 shows annual UK labour productivity growth since 1760. Prior to the 1970s, there were often large shifts in the average growth rate of productivity from one decade to the next. Depending on how you interpret the chart, that could be a good-news or a bad-news story.

The ‘glass half full’ reading might note that we have been through several temporary periods of weak productivity growth before, but have always recovered. But there is also a ‘glass half empty’ interpretation. Robert Gordon from Northwestern University has argued that the hundred years spanning from 1870 to 1970 were exceptional in the number and scope of life-changing break-through innovations and there is absolutely no reason to expect growth to be as high and broad-based now. The progress since 1970, he argues, has been concentrated in a relatively narrow part of the economy: entertainment, communication and information processing. But in other essential areas like food, clothing and shelter, progress has been much slower.

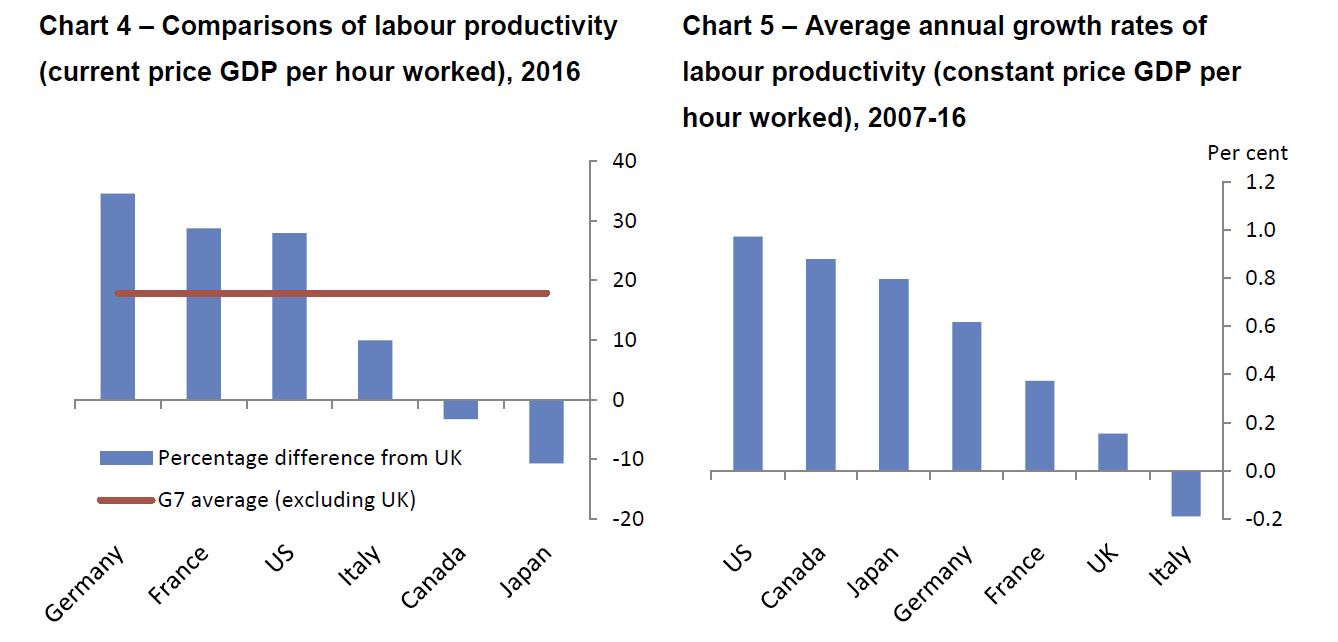

Cross-country comparisons are tricky, but the ONS estimates that compared to the UK, labour productivity is on average 18% higher in the other six members of the G7, 28% higher in the US and 35% higher in Germany (Chart 4). These are significant differences. If British workers were able to catch-up to the G7 average, what currently takes us five days’ work to produce could be done in little over four. If we were able to catch up to Germany, we might all be able to go home from work on Thursday afternoon each week without any fall in GDP.

The plots have illustrated the UK productivity slowdown, both relative to other countries and also relative to the UK’s own recent past.

The plots have illustrated the UK productivity slowdown, both relative to other countries and also relative to the UK’s own recent past.

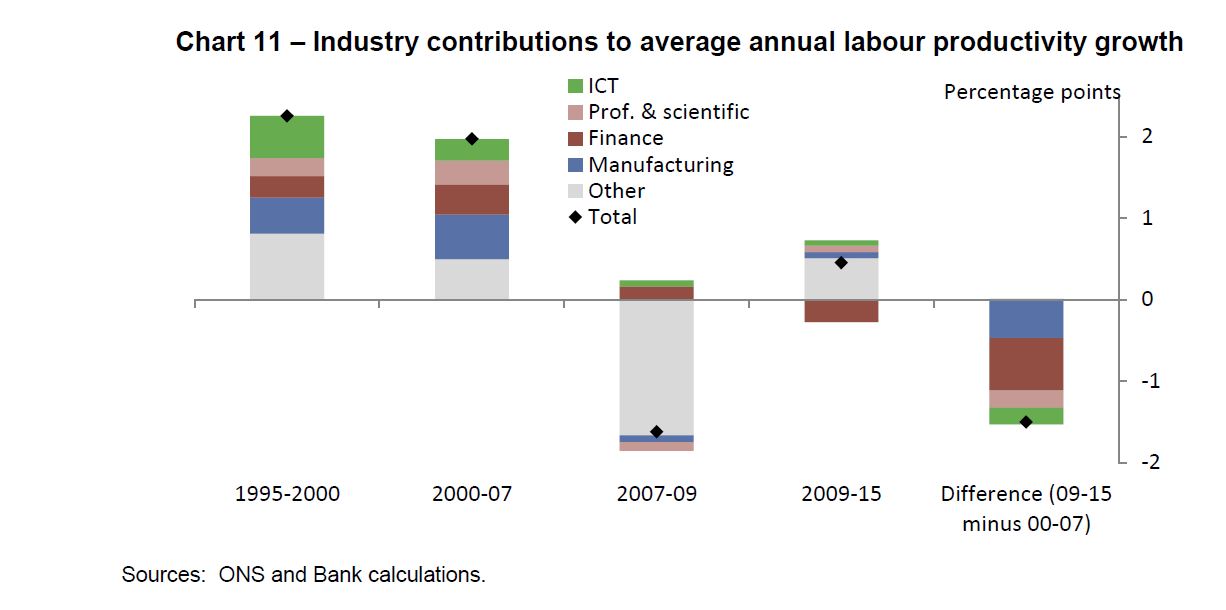

To attempt an answer, why productivity got lost, it is helpful to carry out a sectoral analysis, breaking down the productivity slowdown by industry. The sectoral distribution of productivity growth can help us locate where it has slowed. The slowdown, or difference in the aggregate productivity growth rates between the pre- and post-crisis periods for the UK economy amounted to (a negative) 1.5 percentage points. Remarkably, three-quarters of this productivity growth shortfall is accounted for by just two sectors: manufacturing and finance.

A further quarter of the slowdown is explained by two more sectors: information and communication technologies (ICT); and professional, scientific and technical services. The remaining 14 sectors contributed 0.5pp to productivity growth, both pre- and post-crisis. In other words, productivity outside those four sectors has been growing at a roughly constant, modest rate.

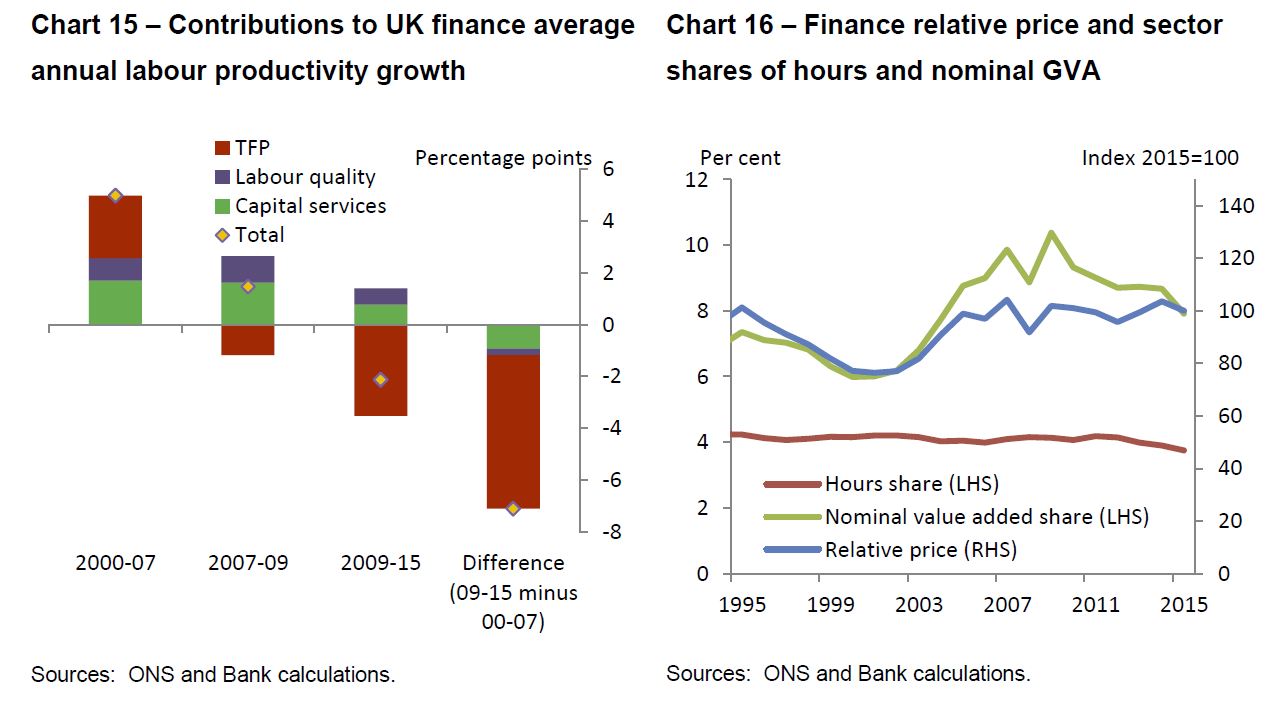

The finance sector is the biggest contributor to the productivity slowdown. It had the fastest-growing labour productivity of any sector in the run-up to the crisis, at 5% per year. Since 2009, productivity has actually shrunk by 2.1% per year.

It is unlikely that the entire slowdown in financial sector TFP is down to mismeasurement. A complementary explanation is that the key contributors to the crisis itself – risk illusion and increasing financial-sector leverage – may have increased (correctly measured) pre-crisis productivity growth. In doing so, they may also have sowed the seeds of the crisis and subsequent weakness. Increased leverage and higher risk tolerance boosted profits, earnings and output. That may have attracted capital and employees from other sectors of the economy. More broadly, rapid credit growth and low risk premia fed into higher asset prices, with positive spillovers to demand elsewhere in the economy. As the crisis hit, these channels went into reverse, leading to falls in wealth and higher uncertainty. Both lowered spending and output and probably also increased households’ labour supply.

Whatever the ultimate trigger of the finance-sector slowdown, its contributions to measured GDP and productivity growth are unlikely to pick up to those we saw in its pre-crisis boom. To achieve that would require a repeat of the type of unsustainable increases in leverage that we saw in the 2000s. The sector’s post-crisis performance has been as poor as its pre-crisis performance was strong. Credit and deposit growth have been weak as banks and households have sought to deleverage. It is possible that the growth of financial activities somehow crowded out the growth in the rest of the economy in a competition for talent and resources.

The financial-stability reforms we have seen since the crisis were put in place precisely to prevent the damaging consequences of those episodes.

Note: The views are not necessarily those of the Bank of England or the Monetary Policy Committee.

The Productivity Commission has released the first in a planned series of five-yearly updates on productivity in Australia. The report shows that there is much the Australian government can do to boost productivity and living standards.

These include changing how government delivers or controls education and health, and how it manages infrastructure. Interestingly, for the Commission, policy to improve productivity in the private sector (primarily tax and regulation), while still important, plays second fiddle.

The Commission backs up its recommendations in these huge domains by a compendium of analyses spread over hundreds of pages in 16 supporting papers.

The Productivity Commission’s review comes amid a period of slow productivity growth in Australia and around the developed world. Fifteen years ago, most economists expected that the internet revolution and the rapid shift of manufacturing to China would, for all the disruption they entailed, sustain strong growth in the rich world. But those hopes were dashed.

A wide range of research has identified many possible culprits for the productivity slowdown. These include mismeasurement, that “easy wins” such as universal education have already been used up, ageing, risk aversion, and a hit to investment and innovation from the global financial crisis.

One of the Commission’s background papers covers many of these contributors to slow growth.

Australian productivity has grown faster than in many other high-income economies since the financial crisis, largely thanks to the mining boom and to our having avoided a deep recession.

But productivity growth has not been strong enough to keep wage growth strong in the face of declining export prices and some broader weakness as the mining investment boom comes off. Getting policy settings right is urgent to reduce the risk that Australia slides into the stagnation that other high-income economies have experienced.

The recommendations

The new report identifies five priorities to revitalise productivity: health, education, cities, market competition, and more effective government.

The Commission’s estimates imply that its policies would eventually boost GDP by at least two per cent, with additional non-market benefits in longer lives and quality of life.

In health, the report recommends changing funding arrangements, cutting low-value treatments, putting the person at the centre of health care, shifting to automated pharmacy dispensing in many locations, and moving to tax alcohol content on all drinks. The Commission estimates that the value of these reforms is at least A$8.5 billion over 5 years.

In education, the report makes recommendations to build teacher skills, better measure student and worker proficiency, extend consumer law to cover universities, and improve lifetime learning, including better information about the performance of institutions. The Commission does not put a dollar value on these reforms.

In cities and transport, the report recommends improved governance to stop poor projects being built, budget and planning practices to properly provide for growth and infrastructure, and policies to get more value out of existing and new assets (including road user charges, extending competition policy principles to cover land use regulation, and replacing stamp duties with land tax). The Commission estimates that these reforms would be worth at least A$29 billion per year in time.

To improve market competition, the report suggests a single effective price be placed on carbon, an end to ad-hoc interventions in the energy market, better consumer control of and access to data, and reforms to intellectual property to support innovation. The Commission estimates that these reforms would be worth at least A$3.4 billion per year.

Finally, to improve government, the report recommends that the states and the Commonwealth develop a new formal reform agenda that clarifies who has responsibility for what, tax changes, measures to improve fiscal discipline, and tougher accountability for implementation of agreed initiatives. The Commission does not put a dollar value on these reforms.

What’s missing?

The review’s omissions are informative, and some are glaring.

First, cutting company taxes is conspicuously absent from the proposals. It seems unlikely this omission is an oversight. It would seem, instead, that the Commission does not see a company tax cut as a priority for productivity growth, and is happy for government to make its own case for a tax cut.

Still, the report would have been stronger had it considered the tax mix more fully. There is credible case for a company tax cut, though it is not the only way to stimulate investment, it would take years to pay off, and it would hit the budget without increase in other taxes or spending cuts.

Second, the report gives short shrift to population growth. Governments are racing to keep pace with population growth in Melbourne and Sydney in particular, yet the report does not consider how population contributes to congestion, how it dilutes the value of natural resource rents, and how the challenges it creates for governments make it more difficult for them to deliver reforms that would boost productivity.

Third, the report does not give enough attention to reforms to improve market functioning. Many consumers in retail markets for services like energy and superannuation do not know how to identify good products, and so consumers often bear the costs of excess marketing or an excess of providers.

It seems likely that the Commission did not want to prejudge the subject of a current Commission inquiry on superannuation, but other markets have similar problems.

There are other gaps. The report does not give enough attention to macroeconomic stability, or even note the risks posed by the Australian house price boom. It does not mention the problematic National Broadband Network. It pays too little attention to the role of social safety nets in helping people manage risks and making the economy more flexible.

And finally, the report could have made stronger recommendations for better measurement. It is ironic that it finds the biggest opportunities in the health and education sectors, whose output is not measured with much accuracy.

Overall, the report is something of a landmark, and the Treasurer deserves credit for commissioning it. It condenses much of the policy advice the Productivity Commission has made in recent years, and adds new insights (for example, on land use).

It provides credible, if incomplete recommendations for improving health and education, and cities and transport. It undersells the value of further reforms to private sector regulation and tax. But it underscores how much governments can do on the “home turf” of the things they control most directly.

Now it is up to Commonwealth and state governments to absorb its insights, integrate them into their agendas, and put them into action.

Author: Jim Minifie, Productivity Growth Program Director, Grattan Institute

While productivity is once again growing in Australia, we face a big challenge in getting it to a level that would restore the rate of improvement in our living standards of the last few decades.

Yet the measures required to meet this challenge may not be the ones usually promoted by economists and editorial writers. We need innovation not just in the technologies we use but in our business models and management practices as well.

The problem, according to new Treasury research, is that national income growth can no longer be propped up by the favourable terms of trade associated with our once-in-a-generation mining boom.

Does this mean we are back to the hard grind of productivity-enhancing reform? There are (at least) two opposing schools of thought on this. Some believe reform is needed, but mainly corporate tax cuts and labour market deregulation. Others deny any such reform is even necessary.

What has happened to productivity?

Productivity is a complex issue, but may be simply defined as output produced per worker, measured by the number of hours worked. On this basis we have seen a modest spike in productivity growth over the last five years to 1.8% per year.

This is primarily due to “capital deepening”, an increase in the ratio of capital to labour. Contemporary examples include driverless trucks in iron ore mines, advanced robotics in manufacturing and ATMs in banking.

Before this five-year period, productivity growth was much lower, even negative. This was especially the case during the mining boom itself when capital investment was taking place but had not yet translated into increased output.

The Treasury paper argues that to achieve our long-run trend rate of growth in living standards of 2% a year, measured as per capita income, we now need to increase average annual productivity growth to around 2.5%.

This will require not just capital deepening, but also improvements in the efficiency with which labour and capital inputs are used, otherwise known as “multifactor productivity”.

The hype cycle

Australia is not alone in facing this productivity challenge. Globally, amidst what would appear to be an unprecedented wave of technological change and innovation, developed economies are experiencing a productivity slowdown.

Again, explanations for this vary. Some economists question whether the current wave of innovation is really as transformative as earlier ones involving urban sanitation, telecommunications and commercial flight.

Others have wondered whether it is still feasible to measure productivity at all when innovation comprises such intangible factors as cloud computing, artificial intelligence and machine learning, let alone widespread application of the “internet of things”.

However, there is an emerging consensus that we are merely in the “installation” phase of these innovations, and the “deployment” phase will be played out over coming decades.

This has also been called the “hype cycle”. New technologies move from a “peak of inflated expectations” to a “trough of disillusionment” and then only after much prototyping and experimentation to the “plateau of productivity”. Think blockchain in financial transactions and augmented reality for consumer products.

The world is bifurcating between “frontier firms”, whose ready adoption of digital technologies and skills is reflected in superior productivity, and the “laggards”, which are seemingly unable to benefit from technology diffusion.

These latter firms drag down average productivity growth and, lacking competitiveness, they inevitably find it more difficult to access global markets and value chains.

The increasing gap between high- and low-productivity firms is less a matter of technology as such than the capacity for non-technology innovation. In particular, this encompasses the development of new business models, systems integration and high-performance work and management practices.

Many of the world’s most successful companies, such as Apple, gained market leadership not by inventing new technologies but by embedding them in new products, whose value is driven by service design and customer experience.

Engaging our creativity

Recent international studies have shown that a major explanatory variable for productivity differences between firms, and between countries, is management capability.

It is noteworthy that Australian managers lag most behind world-best practice in a survey category titled “instilling a talent mindset”. In other words, how well they engage talent and creativity in the workplace.

Most organisations today would claim that “people are our greatest asset”, but much fewer provide genuine opportunities for participation in the decisions that affect them and the future of the business. Those that do are generally better positioned to outperform competitors and demonstrate greater capacity for change.

More survey work on this issue is under way.

A more inclusive approach

Wages are also related to productivity but not always in the way that is commonly assumed. It is said that productivity performance determines the wages a company can afford to pay, with gains shared among stakeholders, including the workforce.

But evidence is emerging that causation might equally run in the reverse direction, with wage increases driving capital investment and efficiency.

This casts the current debate on productivity-enhancing reform in a very different light. It may now be a stretch to argue that corporate tax cuts will be much of a game-changer in the absence of any incentive to invest in new technologies and skills. The same may be said about the ideological insistence on labour market deregulation, if all that results is a low-wage, low-productivity economy.

The populist revolt against technological change and globalisation has its roots not just in the failure to distribute fairly the gains from productivity growth, but in a longstanding effort in some countries to fragment the structures of wage bargaining and to exclude workers from any strategic role in business transformation. This has assigned the costs of change to those least able to resist, let alone benefit from it.

The next wave of productivity improvement, if it is to succeed, must be based on a more “inclusive” approach to innovation policy and management.

As jobs change or disappear altogether, Australia’s workforce can make a positive contribution. But workers will only be able to do so if they have the skills and confidence to take advantage of new jobs and new opportunities in a high-wage, high-productivity economy.

Author: Roy Green, Dean of UTS Business School, University of Technology Sydney

Hal Varian, chief economist at Google, says that if technology cannot boost productivity, then we are in real trouble.

In a podcast interview, Varian says thirty years from now, the global labor force will look very different, as working age populations in many countries, especially in advanced economies, start to shrink. While some workers today worry they will lose their jobs because of technology, economists are wondering if it will boost productivity enough to compensate for the shifting demographics—the so-called productivity paradox.

“I would say there are at least three forces at work,” says Varian. “One of these is the investment hangover from the recession—companies have been slow to reestablish their previous levels of investment. The second has been the diffusion of technology—the increasing gap between some of the more advanced companies and less advanced companies. And third, existing metrics are facing some strains in terms of adapting to the new economy.”

Varian believes demographics is important, particularly now that baby boomers, who made up most of the labor force from the 1970s through 1990s, are now retiring but will continue to be consumers.

“Today, the working labor force is growing at less than half of the rate of population growth, which is a concern in terms of how to make the amount produced equal to the amount that people want to consume,” he said.

Varian’s answer to the concern of older workers who are afraid robots will take over their jobs:

“There’s a saying in Silicon Valley that we overestimate what can happen in two years, and we underestimate what can happen in ten years—this has proven true time and again. What the 40- and 50-year-olds should be doing is continuing to learn. Lifetime learning is the norm now.”

Andy Haldane, the Bank of England’s Chief Economist, explores possible reasons for why productivity growth has consistently been underperforming in relation to expectations – the so-called ‘productivity puzzle’. He suggests that there should be more focus on the “long tail” of less efficient and productive firms, and that cross pollination with more innovative firms may assist. “There is unlikely to be any single measure which puts productivity growth back on track. But measures which support the long tail of companies, currently operating at low levels of productivity, have the potential to do considerable good”. Harnessing digital platforms in this context may be important.

He says the slowdown of productivity growth has clearly been a global phenomenon, not a UK-specific one. From 1950 to 1970, median global productivity growth averaged 1.9% per year. Since 1980, it has averaged 0.3% per year. Whatever is driving the productivity puzzle, it has global rather than local roots. It seems to have started in the 1970’s and it impacts both advanced and emerging markets.

Productivity growth has consistently underperformed relative to expectations, since at least the global financial crisis. This tale of productivity disappointment, in forecasting and in performance, has been extensively debated and analysed over recent years. Some have called it the “productivity puzzle”.

With each year that passes, and as each new turning point in productivity has failed to materialise, this mystery has deepened. This has led some to conjecture that the world may have entered a new epoch of sub-par productivity growth, an era of secular stagnation. The secular stagnation hypothesis is striking in its gloomy implications for future growth in living standards.

It contrasts with a second topical hypothesis. This posits that we may be on the cusp of a Second Machine Age or Fourth Industrial Revolution, an era of secular innovation.4 This might arise from the rise of the robots, artificial intelligence, Big Data, the Internet of Things and the like. Because of its impact on future living standards, the winner of this secular struggle – stagnation versus innovation – carries enormous societal implications.

A second issue, every bit as topical and important, concerns the distribution of gains in living standards. Specifically, there has been mounting concern over a number of years about rising levels of within-country inequality across a number of countries.

What are the causes of this trend? Is it mere mismeasurement? A fall-out from the financial crisis? The result of monetary policy? Slowing Innovation? Or slowing diffusion rates of innovation?

Sectoral shifts in the economy could plausibly account for some of the fall in productivity growth. There has been a secular shift over time away from manufacturing and towards services, with the employment share in manufacturing having fallen from 17% to 7% since 1990. Because productivity growth in manufacturing is higher than in services, this shift could plausibly account for some of the fall in aggregate productivity growth. Even if we correct for this compositional effect, however, the slowdown in UK productivity growth remains.

Tackling the Productivity Puzzle

There has been no shortage of public policy ideas over recent years for boosting productivity growth. Reports by the IMF and OECD have suggested measures ranging from increased infrastructure spending to improved education and training programmes.58 Earlier this year, the UK Government issued a Green Paper setting out various pillars to support productivity.

In generic terms, these policy measures fall into three categories. First, there are measures which support all companies, irrespective of sector, region or characteristic.

Second, there are measures which support technological innovation – the creation and growth of frontier firms.

A third category of policy measure focusses on the fortunes, not of innovative frontier companies, but the long tail of low-productivity non-frontier firms. These companies have tended to be focussed on somewhat less historically. Indeed, their large numbers and disparate characteristics may be one reason why this is the case. Yet given their scale, the returns to modest improvements in these firms could be dramatic.

As a thought experiment, imagine productivity growth in the second, third and fourth quartiles of the distribution of UK firms’ productivity could be boosted to match the productivity of the quartile above. That sounds ambitious but achievable. Arithmetically, that would deliver a boost to aggregate UK productivity of around 13%, taking the UK to within 90-95% of German and French levels of productivity respectively.

One practical way of doing so is by pairing up companies, frontier and non-frontier, to enable the sharing of best practices. This is effectively a mentoring scheme for firms, the like of which is already common among individuals. What would be in it for frontier companies? A more productive supply chain is clearly in their interests. The public sector could also play a useful nudging role in its procurement practices.

A more ambitious idea still, which I have been considering with Philip Bond, is to develop a virtual environment which would enable companies to simulate changes to their business processes and practices. These platforms are already used by many frontier firms to assess the impact of new technologies and processes on their business. These tools can be created, and tailored to companies’ circumstances, at relatively low cost. This makes them a potentially cost-effective way of facilitating diffusion to the long tail.