The Reserve Bank Of New Zealand is driving the OCR higher, as we saw last week. But the question is, for how long, and will they eventually have to reverse course?

New research suggests they may have to turn turtle next year as the economy stalls, and household budgets are squeezed.

Go to the Walk The World Universe at https://walktheworld.com.au/

The New Zealand Monetary Policy Committee (MPC) has decided to implement a Large Scale Asset Purchase programme (LSAP) of New Zealand government bonds.

The negative economic implications

of the coronavirus outbreak have continued to intensify. The Committee agreed

that further monetary stimulus is needed to meet its inflation and employment

objectives.

Globally, the number of

people infected with the virus has increased rapidly and measures to contain

the outbreak have become more restrictive. Global trade and travel, and

business and consumer spending have been curtailed significantly.

The severity of the impacts

on the New Zealand economy has increased. Weaker global activity is affecting

the economy through a range of channels, not just reduced trade. Domestic

measures to contain the outbreak of the virus are also reducing economic

activity. Employment and inflation are expected to fall relative to their

targets in the near term.

In addition, financial

conditions have tightened unnecessarily over the past week, reducing the impact

of the low OCR on achieving the MPC’s mandate. Heightened risk aversion has

caused a rise in interest rates on long-term New Zealand government bonds and

the cost of bank funding.

The Committee has decided to

implement a LSAP programme of New Zealand government bonds. The programme will

purchase up to $30 billion of New Zealand government bonds, across a range of

maturities, in the secondary market over the next 12 months. The programme aims

to provide further support to the economy, build confidence, and keep interest

rates on government bonds low.

The Committee will monitor

the effectiveness of the programme and make adjustments and additions if needed.

The low OCR, lower long-term interest rates, and the fiscal stimulus recently

announced together provide considerable support to the economy through this

challenging period.

Record of meeting:

Monetary Policy Committee (MPC)

20-22 March 2020

On Friday 20 March the Chair

of the MPC spoke with the external members of the MPC by phone to update them

on the Bank’s financial stability activities and the interaction with monetary

policy. These activities were public. The external MPC members were made aware

of what the other members of the Committee were involved in with regard to the

Bank’s ongoing support to financial market functioning and stability.

The Chair and the external

members also discussed the fact that any further monetary stimulus provided by

the Bank would likely be through the purchase of government bonds in a Large

Scale Asset Programme (LSAP). All MPC members were also made aware that

monetary policy recommendations were being sent to them for a decision soon,

and that there would likely be an ongoing series of Bank monetary and financial

stability actions as the economic impacts of COVID-19 unfolded.

MPC members received papers

on Friday evening containing staff advice about the ongoing deterioration in

the economic situation relating to COVID-19.

The initial view of staff

was that an MPC decision on their recommendations would be preferable by Sunday

22 March 2020. On Saturday 21 March, following advice from the Reserve Bank’s

financial markets team as to their operational and legal readiness to implement

a LSAP, the MPC Chair called for an MPC decision to be made by email. An

in-person meeting was seen as unnecessarily risky given current official

guidance about social distancing.

There was agreement amongst

members to proceed in this manner and by Sunday morning there was a consensus

MPC agreement to:

Provide further monetary policy stimulus through a Large Scale Asset Purchase (LSAP) programme of New Zealand government bonds in the secondary market.

The initial scale of the LSAP programme is up to $30 billion of government bonds, across a range of maturities, to be purchased over the next 12 months.

Communicate the decision on the morning of 23 March.

This decision was made in

response to staffs’ briefing material to the committee indicating the

increasing severity of the economic situation and deterioration in financial

market conditions.

It was noted that the

Government’s fiscal package announced on March 17 has delivered significant

spending stimulus in addition to the monetary stimulus announced on March 16.

However, the health and safety measures announced by governments over prior

days – related to the reduction in travel and large gatherings globally – would

add to inflation and employment falling below target in the near term.

Returning inflation and

employment to target over the medium term will require support from monetary

policy. How much stimulus will depend on how the COVID-19 pandemic progresses

and the actions to abate the virus.

The committee considered a

range of scenarios, and it was apparent that in light of the evolving situation

more stimulus was needed.

Committee members’ attention

was drawn to the tightening in financial conditions over the past week.

Interest rates on long-term New Zealand government bonds had risen

significantly, affecting the cost of wholesale funding for any banks accessing

the market at this time. Such increases mean that the reduction in the OCR

announced on March 16 was not effectively passing through into interest rates

faced by borrowers. The depreciation in the exchange rate had helped ease

conditions at the margin but not sufficiently.

The staff briefing material

also included updates on global economic developments and other countries’

economic policy responses to the pandemic.

Committee members were

advised that the recommendation of a $30 billion LSAP program reflected a

current assessment of the maximum effective stimulus achievable while

maintaining a well-functioning government bond market. Staff noted the importance

for liquidity to remain in the bond market and for multiple market makers.

Staff recommended that

purchases up to $30 billion should be spread over at least 12 months and across

a range of maturities, in order to leave enough liquidity for the New Zealand

government bond market to function effectively. And that the Bank’s

communications should emphasise that the LSAP programme would provide

confidence and support for the government bond market, and monetary stimulus

through keeping longer-term interest rates low.

Members noted that the exact

amount of stimulus needed is difficult to quantify, and that the range of

economic scenarios they had seen were consistent with a need to deliver

significant stimulus.

Briefing material also

included information about the implications of an LSAP program to the Reserve

Bank’s balance sheet, and about the governance arrangements in place between

the Reserve Bank and the Minister of Finance. It was noted that MPC agreement would

be sought if further stimulus was needed to be provided, either by increasing

the size of the LSAP programme, or through the use of other instruments.

The Committee reached a

consensus to:

Approve a programme of Large Scale Asset Purchases to a total volume of $30 billion of NZ Government bonds over 12 months

Delegate to staff the implementation decisions of the LSAP programme

Communicate the program in terms of the total volume to be purchased

The Reserve Bank and the banking system have plenty of cash on

hand to meet demand under any circumstances,” says Assistant Governor Christian

Hawkesby. Mr Hawkesby made the statement today after public interest and

discussion about cash availability and use.

“We work closely with New

Zealand’s banks, the companies that transport cash, and those that supply

cash-handling equipment. They are all prepared for operating during all

circumstances, including any unusual challenges that COVID-19 may pose.” he

says.

“As an example, the Reserve

Bank has at least two years’ worth of replacement cash available to feed into

the system if required. We can keep cash flowing to and from branches and ATMs

in the event of staff shortages or other difficulties anywhere in the cash

system.”

“The banks and electronic

payments systems are prepared, resilient, and will keep operating. When people

are shopping, there will be cash and other payments systems available to

support that,” he says.

The Reserve Bank is also

reminding shoppers and retailers to practice good hand hygiene.

“Cash is just one of a

number of frequently touched surfaces we encounter. The same is true for any

other payment device whether it’s a card, phone or watch. This reinforces the

need for good hand hygiene regardless of the way you pay or accept payment.”

“Retailers should use

common-sense when it comes to cash. Businesses are not obliged to accept cash,

but declining it may end up disadvantaging people who rely on its use. These

people are more likely to be young, elderly, poor, disabled or financially

excluded. Have respect and care for each other,” says Mr Hawkesby.

In a statement, the Reserve Bank of New Zealand says New Zealand’s financial system is sound, with strong capital and liquidity buffers, but faces significant uncertainties from the impacts of COVID-19. The Reserve Bank is announcing additional measures to support the provision of credit and market functioning.

Reserve Bank Deputy Governor

Geoff Bascand says the situation around COVID-19 is evolving rapidly, and there

is much uncertainty.

“To support credit

availability, the Bank has decided to delay the start date of increased capital requirements for banks by 12 months –

to 1 July 2021. Should conditions warrant it next year, the Reserve Bank will

consider whether further delays are necessary.”

“We are taking this action

now to help support lending in the economy at time when there is a lot of

uncertainty. The Reserve Bank’s expectation is that banks will utilise this

flexibility to maintain lending to households and businesses. Banks have

significant buffers above current regulatory minimums, and we encourage them to

use them,” Mr Bascand said.

“Deferring the capital

framework implementation provides banks with significant capital headroom. We

estimate that this headroom will enable banks to supply up to around $47

billion more lending than would have been the case, had the decisions been

implemented as planned.”

Mr Bascand said the Reserve

Bank is currently identifying other regulatory initiatives that can be deferred,

to reduce the burden on financial institutions at this time of uncertainty.

These will be announced in coming days. The Reserve Bank is working closely

with the Council of Financial Regulators and international regulators.

Assistant Governor Christian

Hawkesby said the Bank is also ensuring there is sufficient liquidity in the

financial system, through regular market operations.

“The Bank has a number of

operational tools at its disposal to support liquidity and market functioning

in New Zealand. This has helped the domestic cash market and foreign exchange

swap market to continue to function effectively over recent weeks,” Mr Hawkesby

says.

“Banks currently have robust

liquidity and funding positions and can manage short-term disruptions to

offshore funding markets. We will continue to monitor developments closely and

engage regularly with market participants to ensure we are ready to provide

support if needed.”

The Reserve Bank also

announced the following changes to the pricing of its standing facilities and

ESAS accounts, in part to assist cash market functioning at a lower OCR:

Cash that ESAS account holders have on deposit at the Reserve Bank that is in excess of their allocated ESAS credit tier will be remunerated at the OCR less 25 basis points (from OCR less 75 basis points).

Bonds lent through the Bond Lending Facility well be lent at the OCR less 50 basis points (from OCR less 75 basis points).

A maximum rate will be set for bonds lent through the Repo Facility at the OCR less 50 basis points (from OCR less 75 basis points).

Cash will continue to be lent via the Overnight Reverse Repo Facility at the OCR plus 25 basis points until further notice.

The Reserve Bank has a

number of tools to provide additional liquidity, and support to market

functioning, should these be required in the future:

The ability to provide term funding through a Term Auction Facility (TAF) which can provide collateralised loans out to 12 months. This facility was previously provided from 2008 to 2010.

The Bank has an established role to provide liquidity in the New Zealand dollar foreign exchange market in periods of illiquidity or dysfunction, and is operationally ready to undertake this role if required.

The ability to provide liquidity to the NZ government bond market to support market functioning.

Mr Hawkesby says the Reserve

Bank continues to monitor developments, and is ready to act to ensure markets

and the financial system operate in a stable and efficient manner.

New Zealand banks are ready to respond to the impacts of

coronavirus, the Reserve Bank of New Zealand and New Zealand Bankers’

Association say.

The COVID-19 outbreak has

the potential to impact the operations of New Zealand’s banking sector by

affecting banks’ staff, their funding and their customers.

The Reserve Bank has asked

all banks about their risk management approaches and preparedness for COVID-19.

Reserve Bank Governor Adrian Orr said the responses show the banks are

prepared.

“Much of the banks’ focus

has been on staff health and safety, and their ability to sustain their

operations should the outbreak expand significantly. However, the banks are

also well attuned to any impacts on their customers’ businesses, employment,

and incomes,” Mr Orr says.

New Zealand Bankers’

Association chief executive Roger Beaumont says customers financially affected

by COVID-19, particularly small to medium sized businesses, are encouraged to

contact their bank.

Depending on the customers’ individual

circumstances potential options for support include:

Reducing or suspending principal payments on loans and temporarily moving to interest-only repayments

Helping with restructuring business loans

Consolidating loans to help make repayments more manageable

Providing access to short-term funding

Referring individual customers to budgeting services.

“Each bank will have their

own credit policies and approach to providing assistance. It’s important for

affected customers to talk to their bank as soon as possible. That gives banks

the best chance of offering assistance. Helping customers through any financial

stress depends on good two-way communication,” Mr Beaumont says.

The Reserve Bank team are in

regular dialogue with bank executives and are watching for signs of funding

market pressures or emerging signs of credit stress.

“While we have not seen any

significant pressures at this stage, we remain in regular contact with

stakeholders across the financial sector. At the Reserve Bank we are prepared

in our business continuity role to ensure a well-functioning financial system,

including enabling access to cash, ensuring sufficient liquidity in the banking

system, and managing a stable payments and settlements system,” Mr Orr says.

“All

businesses should be preparing for possible disruptions from COVID-19. Think

about how best to operate if staff are temporarily unavailable, or if suppliers

have restricted stock, cash-flows are interrupted, and sales decline in some sectors,”

Mr Orr says.

The New Zealand Reserve Bank has launched a new future-proofed payment settlement system, replacing New Zealand’s inter-bank settlement system and central securities depository.

The new platform replaces a

20-year-old system with two separate systems, ESAS 2.0 and NZClear 2.0. The new

platform comprises the Real Time Gross Settlement (RTGS) and Central Security

Depository (CSD) applications supplied by SIA – a European technology and

banking infrastructure leader and its wholly owned subsidiary Perago.

Infrastructure support services are supplied by Datacom Systems Limited.

The extent of change is

significant, says Assistant Governor/Chief Financial Officer Mike Wolyncewicz.

“Every day, transactions

with a value of more than $30 billion are settled, so there has been a focus on

getting this right, and not rushing out a replacement until we were confident

that it was ready.

“The buy-in from the

industry has been fantastic. This week’s successful changeover is the result of

months of rigorous testing and we appreciate the cooperation of the system’s

key users.”

The Reserve Bank’s payment

settlement system is used by 57 member organisations including banks,

custodians, registries and brokers. This equates to around 600 users of the

system, from New Zealand, Australia and Asia.

“Our members now have access

to far more modern, future-proofed and leading edge systems for them to manage

their day-to-day interactions with the Reserve Bank,” Mr Wolyncewicz says.

The systems replacement

follows a strategic review of the incumbent payment and settlement systems

operated by the Reserve Bank, completed in 2014 in anticipation of the need to

align with today’s operational and technological standards.

According to Moody’s, on 5 December, the Reserve Bank of New Zealand (RBNZ) announced the finalisation of its capital requirements for New Zealand banks. The RBNZ’s decision to raise capital requirements – although slightly watered down from its earlier proposal – is broadly credit positive, because it will make the banking system more resilient to shocks. At the same time, the higher capital requirements will weigh on the banks’ return on equity. We expect the new measures will prompt higher lending rates in efforts to boost profitability and constrain growth in more capital-intensive lending.

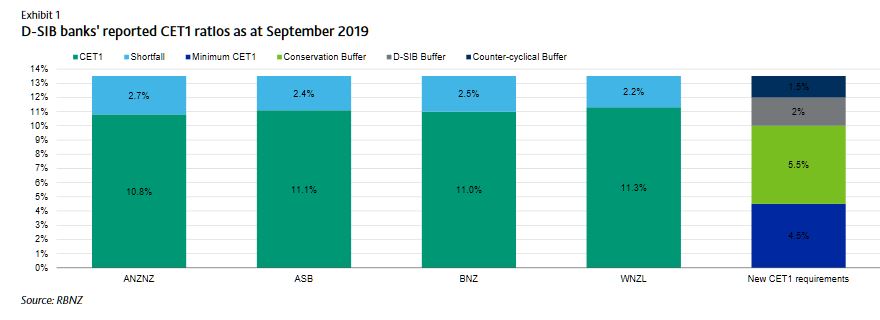

For domestic systemically important banks (D-SIBs), which are New Zealand’s four largest banks, ANZ Bank New Zealand Limited, ASB Bank Limited, Bank of New Zealand, and Westpac New Zealand Limited, the Common Equity Tier 1 (CET1), Tier 1 and Total Capital requirements have risen to 13.5%, 16% and 18% of risk weighted assets (RWA), respectively. While the new rules are a slight relaxation from the RBNZ’s initial proposal of 14.5%, 16% and 18% announced in December 2018, they represent a significant increase from the current requirements of 7%, 8.5% and 10.5%. For all other banks, the CET1, Tier 1 and total capital ratio requirements will be 11.5%, 14% and 16%, respectively.

The RBNZ also announced that existing Additional Tier 1 and Tier 2 securities will no longer count towards regulatory capital. Replacing them will be redeemable, perpetual, preference shares and subordinated debt, provided these securities do not have any contractual contingent features such as conversion or write-off at the point of non-viability.

The higher requirements will be implemented by maintaining a regulatory minimum Tier 1 ratio of 7%, of which 4.5 percentage points must be CET1 capital, and introducing a number of prudential capital buffers, which total 9 percentage points (see Exhibit 1). Under the new framework, banks can temporarily operate below 13.5%, but above 4.5%, without triggering a breach of regulatory requirements. However, they will be subject to more intensive supervision and other consequences such as dividend restrictions. On average, the D-SIB CET1 ratios are around 2.5 percentage points lower than the new requirement of 13.5% (Exhibit 1).

The RBNZ is also limiting the difference between the calculation of RWAs by D-SIBs, which use the internal ratings based approach (IRB), and other banks that use the Standardised approach. This will be done by recalibrating the calculation IRB banks’ RWAs to around 90% of the outcome under the Standardised approach. The combination of higher capital ratio targets and higher RWAs imposed on D-SIBs could spur more competition by reducing some of the capital advantage previously enjoyed by banks using the IRB approach.

The new capital regime will take effect from 1 July 2020 and the banks will have up to seven years to meet the new rules, an increase from the five years initially proposed. The RBNZ’s decision to extend the transition period will ensure banks are well placed to meet the new targets, especially given the Australian Prudential Regulation Authority’s (APRA) recent changes to Australian Prudential Standards (APS) 222 to further restrict how much equity support Australia’s largest banks can provide to their New Zealand subsidiaries, and proposed changes to APS 111, which will increase the capital requirements of providing such support.

The Australian parents of the New Zealand D-SIBs Australia and New Zealand Banking Group Limited, Commonwealth Bank of Australia, National Australia Bank Limited, and Westpac Banking Corporation have all disclosed the estimated impact of the new rules (Exhibit 2).

The additional capital requirements imposed on the big four by the Reserve Bank of New Zealand has seen analysts downgrade their forecasted return on equity across the major institutions. Via InvestorDaily.

The Reserve Bank of New Zealand (RBNZ)

has demanded the local arms of the big four raise their total capital

ratio from a minimum of around 10.5 per cent to 18 per cent over the

next seven years. The central bank had previously estimated that this

would see a collective raise of around $19.1 billion.

Currently, banks in New Zealand hold an average of around 14.3 per cent.

According

to an analysis from Morningstar, the big four’s raise will be a

combined $12.4 billion (NZ$13 billion) to meet the new tier 1 capital

requirements amounting to 16 per cent of risk weighted assets, versus

the current 8.5 per cent.

S&P Global has placed the figure at around $15.7 billion (NZ$16.4 billion).

The

changes, which come into effect from next year, have been made to

protect consumers against loan losses and to prevent the banks from

reaching a point of failure.

But the

time frame is key, as the central bank extended it from its original

proposed five years for the raise to soften any economic shocks.

Morningstar said the longer period will see banks organically retaining

additional capital from earnings, instead of triggering equity raisings

or dividend cuts.

Analysts at the

investment bank expect the Australian majors to respond to the new

measures by repricing loans and deposits and by reducing exposure to

higher-risk sectors and borrowers.

Further,

S&P Global noted the implementation of the measures should not

materially reduce the availability of credit in New Zealand, but the

banks could cut lending to customer segments that would require

increased regulatory capital.

“RBNZ’s

initiatives strengthen bank-capital levels, which provides a greater

buffer to manage a potential increase in loan losses,” the Morningstar

analysis read.

It has made no changes

to its earnings forecasts or valuations of the banks, however, despite

expecting the summation of flat or slightly higher loan books and higher

net interest margins will lead to moderately lower cash NPATs across

the New Zealand divisions.

“The effect on group earnings is immaterial though,” Morningstar said.

“The drag on the banks’ returns on equity is larger.”

The

assessment has predicted a reduction in return on equity for CBA by 46

basis points to 14.8 per cent, Westpac by 22 basis points to 11.4 per

cent, ANZ by 16 basis points to 11.5 per cent and NAB by 36 basis points

to 11.3 per cent.

S&P Global has said likewise, expecting ROE to “considerably decline”.

The

Morningstar analysts also believe the major banks can maintain current

dividend levels, but retaining a greater portion of New Zealand profits

leaves less headroom to offset unexpected hits on earnings or capital.

Westpac

and NAB have slashed their dividend payouts, and ANZ cut its dividend

franking level recently, reflecting impacts on profit from unexpected

remediation.

ANZ in particular is

raising capital at the group level to meet the RBNZ rules, holding a

larger investment in its New Zealand division than the other banks.

None of the other banks have indicated any intention to raise capital, but the possibility remains in the future.

“Seven

years is a long time, and this view will need to be reviewed as the

banks’ strategic response takes shape,” the Morningstar analysts stated.

“The

New Zealand operations of the banks will remain highly profitable

despite the additional capital, hence we do not expect a divestment to

be on the cards.”

The Reserve Bank of New Zealand today released its final decisions following its comprehensive review of its capital framework for banks, known as the Capital Review. The trajectory will be over a longer period, with more flexibility, but the banks will still need to hold more capital.

Governor Adrian Orr said the

decisions to increase capital requirements are about making the banking system

safer for all New Zealanders, and will ensure bank owners have a meaningful

stake in their businesses. The changes will be implemented over seven years,

giving plenty of time for banks to manage a smooth transition and minimise any

adjustment costs.

“Our decisions are not just

about dollars and cents. More capital in the banking system better enables

banks to weather economic volatility and maintain good, long-term, customer

outcomes,” Mr Orr says.

“More capital also reduces

the likelihood of a bank failure. Banking crises cause not only harmful

economic costs but also distressful social issues, such as the general decline

in mental and physical health brought about by higher rates of unemployment.

These effects are felt for generations,” Mr Orr says.

The key decisions, which start to take effect from 1 July 2020, include banks’ total capital increasing from a minimum of 10.5% now, to 18% for the four large banks and 16% for the remaining smaller banks. The average level of capital currently held by banks is 14.1%.

Relative to the Reserve

Bank’s initial proposals, the final decisions also include:

More flexibility for banks on the use of specific capital instruments;

A more cost-effective mix of funding options for banks;

A lesser increase in capital for the smaller banks consistent with their more limited impact on society should they fail;

A more level capital regime for all banks – with the four large banks having to measure the risks of their exposures (lending) more conservatively, more in line with the smaller banks; and

More transparency in capital reporting.

The adjustments to the original proposals reflect our analysis and industry feedback over the past two years. All of these changes will be phased in over a seven-year period, rather than over five years as originally proposed, in order to reduce the economic impacts of these changes.

Deputy Governor and General

Manager of Financial Stability Geoff Bascand says the decisions were shaped by

valuable public input and insight received through an unprecedented number of

submissions as well as public focus groups. Three international experts also

provided supportive perspectives on the proposals.

“We’ve listened to feedback

and reviewed all the data, and are confident the decisions are the right ones

for New Zealand,” Mr Bascand says.

“We have amended our

original proposals in a number of ways so we achieve a high level of resilience

at lower potential cost, with a smoother transition path for all participants.

Our analysis shows that the benefits of these changes will greatly outweigh any

potential costs.”

“Following the Global

Financial Crisis, many regulators around the world have been taking steps to

improve the safety of their banking systems. We’re confident we have the

calibrations right for New Zealand conditions. These changes will be subject to

monitoring, with the Reserve Bank reporting publicly on implementation during

the transition period,” Mr Bascand says.

The New Zealand Reserve Bank has increased its supervisory monitoring of the Bank of New Zealand (BNZ) and applied precautionary adjustments to its capital requirements following the identification of weaknesses in BNZ’s capital calculation processes.

BNZ identified a number of

errors while undertaking a programme of remediation, which began in early 2018

and is expected to continue into 2020. These included three capital calculation

errors, which resulted in misreported risk weighted assets over a number of

years.

It is now required to

increase the risk weight floor of its operational risk capital model from $350

million to $600 million capital. The $250m increase is a supervisory capital

overlay.

The Reserve Bank requires

banks to maintain a minimum amount of capital, which is determined relative to

the risk of each bank’s business. BNZ has not been in breach of minimum capital

requirements at any point.

“However given the

likelihood that further compliance issues will be discovered during the review

and remediation, the Reserve Bank regards a precautionary capital adjustment as

prudent,” Deputy Governor Geoff Bascand says.

In 2017, the Reserve Bank

conducted a review of bank director attestation processes and noted that many

banks were attesting to compliance on the basis of negative assurance, ie they

did not have evidence to suggest that they were not in compliance.

Breaches are now being

identified as banks review their governance, control and assurance processes

and move from a negative assurance to a positive evidence-based assurance

framework. Over the past year, a number of banks have disclosed breaches of

their conditions of registration, Mr Bascand says. Many of these have related

to errors in the calculation of their regulatory capital or liquidity which, in

some cases, have gone undetected for a number of years.

“We are reassured by BNZ’s response to the issues along with the independent oversight from PWC,” Mr Bascand says. “BNZ has committed to providing the Reserve Bank with regular and timely updates of the details of issues as they are discovered and the remedial activity as this work progresses. “The additional capital overlay will be removed when remediation is complete. It is the Reserve Bank’s expectation that the current review will identify all outstanding compliance issues and potential breaches.”