The Treasury released a request for submission relating to the thorny issue of digital exclusion, and specifically the fact that some companies, in a drive to digital first, are starting to charge consumers to continue to receive paper bills, for services such as utilities. There is already legislation in some other countries to protect consumers from this.

The Treasury suggest a range of options:

- Option 1 — the status quo, with an industry led consumer education campaign;

- Option 2 — prohibition (ban) on paper billing fees;

- Option 3 — prohibiting essential service providers from charging consumers to receive paper bills;

- Option 4 — limiting paper billing fees to a cost recovery basis;

- Option 5 – promoting exemptions through behavioural approaches.

As we discussed last week, they suggest 1.2 million households are digitally excluded by not having access to the internet.

The Keep Me Posted Lobby Group (who contacted me after last week’s post) advocates there should a ban on paper billing fees.

“We clearly stated Keep Me Posted’s position to support a total ban on all billing fees, which is option 2 of the consultation paper,” said Kellie Northwood, Executive Director, Keep Me Posted.

To add weight to be debate we wanted to make two points.

FIRST – the Treasury estimate understates the number of households who are digitally excluded and so more would be potentially hit by excess bill charges.

SECOND – we believe option 2 – ban fees is the right option.

How Many Households Are Digitally Excluded?

We use data from out rolling 52,000 household surveys across Australia.

The result suggests that it is not just access to the internet which is an issue, but there are some households who just are unwilling or unable to use the internet. In fact the Treasury’s estimate of the number of households impacted is understated.

We segment households, digitally speaking into three group.

- DIGITAL NATIVES: Households who are naturally digital, using mobile devices, constantly online and using social media, often using multiple devices including tablets and smart phones.

- DIGITAL MIGRANTS: Households who are moving from terrestrial services to digital, taking up smart devices and learning to access social media and other online services.

- DIGITAL LUDDITES: Households who prefer terrestrial services, but who are now starting to migrate online and are reluctantly adopting the new paradigm. In many cases they are unwilling or unable to migrate.

We also use our master household segmentation, which is based on multi-factorial geo-demographic and behaviourial analysis, though based on our rolling 52,000 household survey.

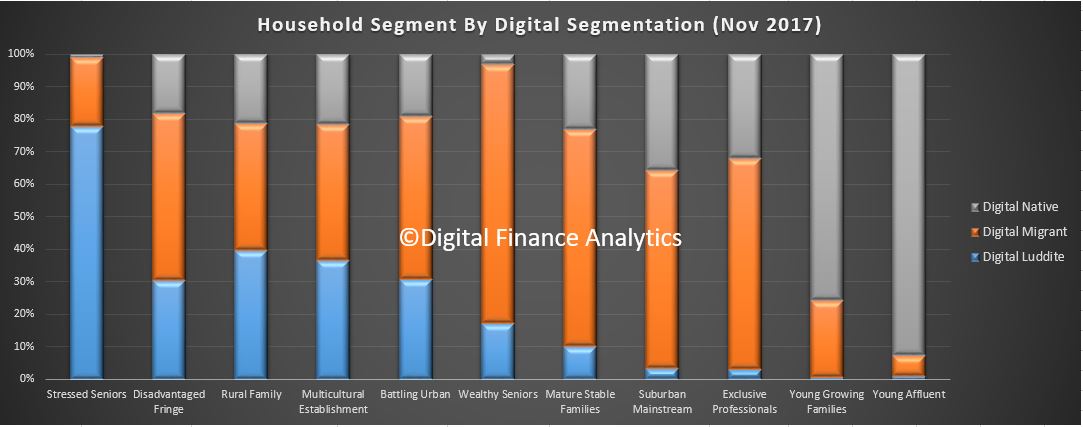

The results show that Digital Luddites are predominately in the older and less wealthy households, including Stressed Seniors, those living in the disadvantaged fringe areas around our major cities, those in a rural setting, and those from non-English speaking ethnic backgrounds. Count up all the Digital Luddites and it comes to 27% or 2.6 million households.

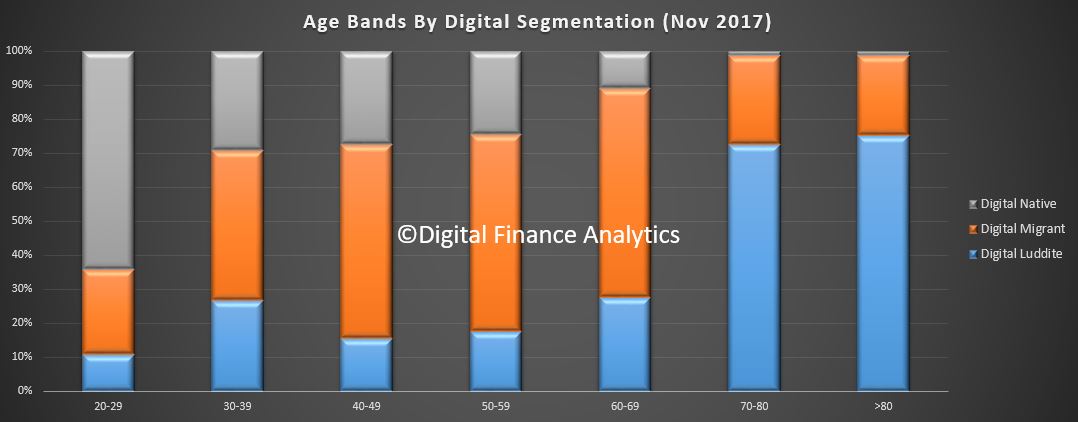

We can examine the splits by age bands, and confirm that older households are more likely to be in this group.

We can examine the splits by age bands, and confirm that older households are more likely to be in this group.

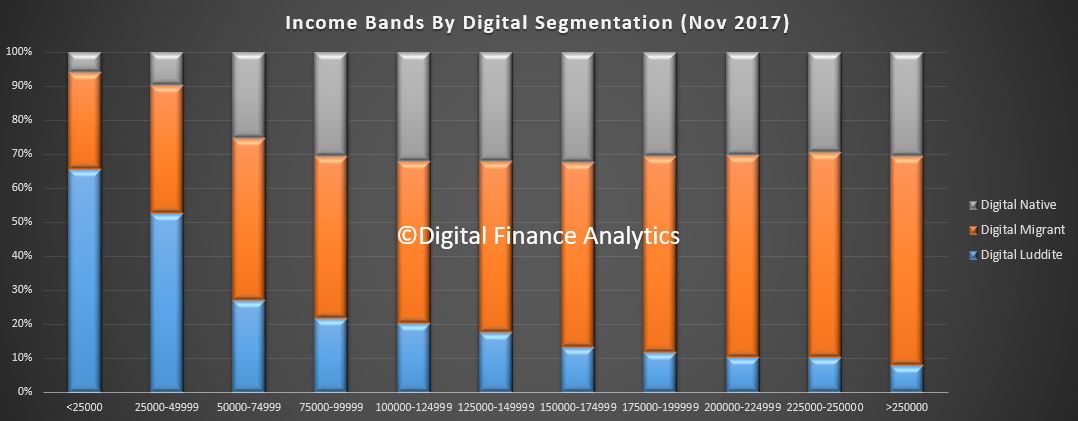

Analysis by income band highlights that significantly more are in the lowest income range, including many on pensions and Government support.

Analysis by income band highlights that significantly more are in the lowest income range, including many on pensions and Government support.

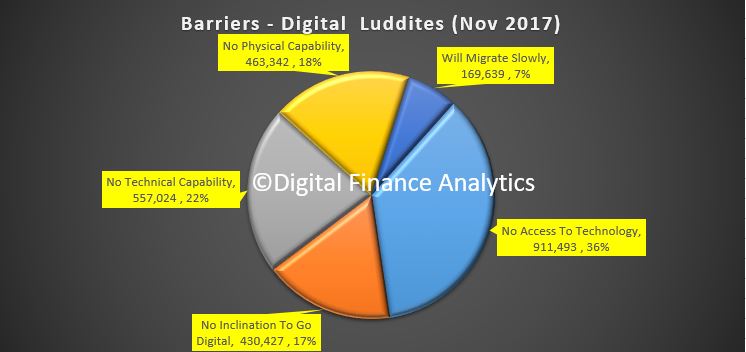

We were able to examine the barriers which were driving households into the Luddite group. We found that whilst 7% (around 170,000) are likely to migrate to digital channels, if slowly; 36% (around 911,000) households did not have access to the internet, or usable device; 17% (around 430,000) had no inclination to go digital, even if they could; 22% did not have the technical capability – could not operate a smart phone, did not know how to get to connect to the internet – (around 557,000); and 18% (around 463,000) did not have the physical capability (thanks to disability or other factors).

We were able to examine the barriers which were driving households into the Luddite group. We found that whilst 7% (around 170,000) are likely to migrate to digital channels, if slowly; 36% (around 911,000) households did not have access to the internet, or usable device; 17% (around 430,000) had no inclination to go digital, even if they could; 22% did not have the technical capability – could not operate a smart phone, did not know how to get to connect to the internet – (around 557,000); and 18% (around 463,000) did not have the physical capability (thanks to disability or other factors).

Stripping back the analysis to a financial capability (did they have the funds to purchase a device, internet access etc), then we estimate 54% of Luddites were impacted by these economic factors, or 1.36 million households.

Stripping back the analysis to a financial capability (did they have the funds to purchase a device, internet access etc), then we estimate 54% of Luddites were impacted by these economic factors, or 1.36 million households.

We believe therefore the Treasury estimate of the number of households impacted by digital exclusion is understated. This adds more weight for intervention.

The Right Choice Is: Option 2 – Fees Should Be Banned

Companies are clearly able to save money if they can stop sending out paper versions of statements, and rely on customers to receive online notification and then retrieve their statements. This economic driver is understood, though most often the initiate will be dressed up as “environmentally friendly”, or “more convenient”. It appears though that savings are not passed back to consumers directly, but flow into general funds.

Our research suggests that a considerable number of households are unable to go digital. Thus they risk having additional fees and charges imposed on them, with no mitigating option. This is in effect a price rise. Whilst education, and communication to households may assist some, many are not able to migrate. These are the least wealthy, older and more exposed households. This is not equitable.

In some cases it appears charges for bills are significantly higher than the incremental charge based on an estimate of what the incremental cost should be, and in any case, experience from the banking sector highlights suggests it is difficult to get a definitive incremental estimate of the cost of a bill. We think restricting the acceptable charge to cost to recovery, is complex, cannot be audited, and offers too much wriggle room.

We cannot support the differentiation between essential and non-essential services, not least because the threshold would potentially vary by household circumstance, and we cannot see a justification for charging for paper billing in some circumstances, but not others.

Therefore charges for paper billing should be banned.

Companies would be welcome to offer discounts to those receiving electronic delivery (although the ACCC may have to ensure that overall costs of service are not lifted to facilitate the subsequent discounting!)

We will be making this submission to Treasury.