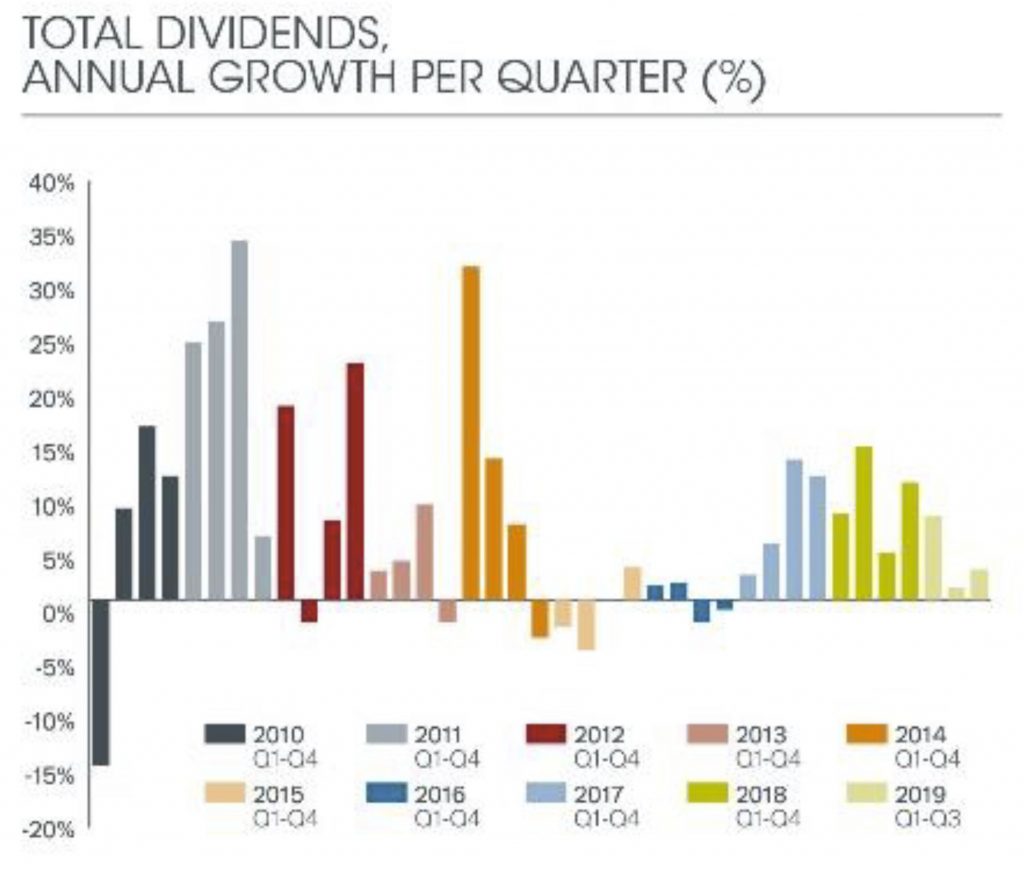

A slowdown in global dividend growth is underway, according to the latest Janus Henderson Global Dividend Index (JHGDI). The trend began in the second quarter and continued in the third. Even at their slower pace, dividends are still growing comfortably, however.

Australia saw a big decline in dividends, with two fifths of companies in the index cutting dividends. The total dropped to $18.6bn, the lowest Q3 total since 2010 in US dollar terms, down 5.9% on an underlying basis. The biggest impact came from National Australia Bank, which made its first dividend cut in a decade, and Telstra. Australia already has the lowest dividend cover in the world among the bigger economies.

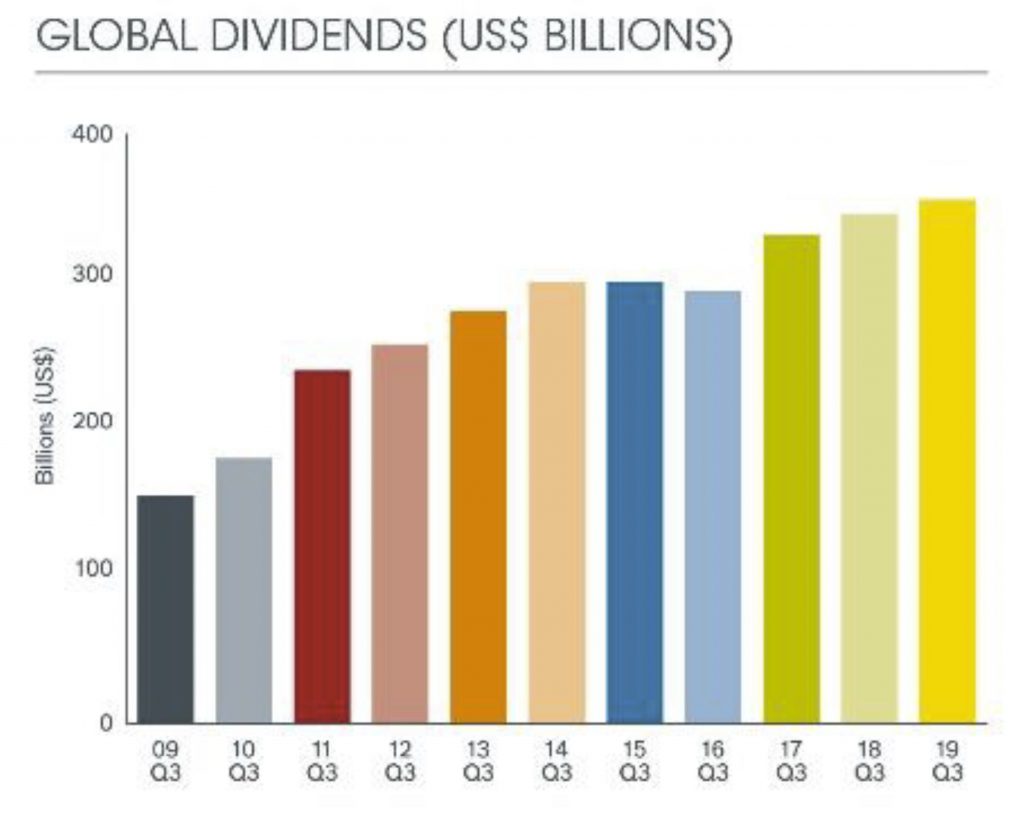

Globally, payouts rose 2.8% on a headline basis to reach a new third-quarter record of $355.3bn, equivalent to an underlying growth rate of 5.3% once the stronger dollar and minor technical factors were taken into account. This is exactly in line with the long-term trend, and Janus Henderson’s forecast. The Janus Henderson Global Dividend Index rose to 193.1, a new record.

Only US dividends reached an all-time record in Q3, up 8.0% on an underlying basis, well ahead of the global average. A slowdown in profit growth is however beginning to impact dividend payments. A rising proportion of US companies held their dividends flat – one in six companies in Q3, up from one in ten in Q1, though there remain few outright cutters. The largest dividend payer in the US this year will be AT&T, jumping ahead of Apple, Exxon Mobil and Microsoft. AT&T’s return to the top spot for the first time since 2012 is thanks to its acquisition of Time Warner in 2018; the combined company will distribute close to $14.9bn, though this will not be enough to dislodge Shell as the world’s largest payer for the fourth year in a row.

Allowing for seasonality Japan, Canada and the United Kingdom all saw third-quarter records, though in the UK’s case this was entirely due to very large special dividends from banks and miners. The underlying trend in the UK remains lacklustre with underlying growth of just 0.6%.

From a seasonal perspective, Q3 is especially important for Asia Pacific and China. Here there were distinct signs of weakness. Almost half the Chinese companies in the index reduced their payouts, and the modest growth that was achieved was dependent on big increases from one or two companies. Chinese dividends totalling $29.2bn crept ahead 3.7% year-on-year on an underlying basis and without Petrochina’s large increase, they would have been lower year-on-year. The slowdown in the Chinese economy is affecting the dividend-paying capacity of its companies, particularly since in the short-term dividends are more closely tied to profits in China than in other parts of the world such as the US and UK due to companies largely adopting a fixed payout-ratio policy.

Across Asia-Pacific, Australia and Taiwan led payouts lower, and only Hong Kong delivered strong growth. It was a difficult quarter in Australia with two fifths of companies in the index cutting dividends. The total dropped to $18.6bn, the lowest Q3 total since 2010 in US dollar terms, down 5.9% on an underlying basis. The biggest impact came from National Australia Bank, which made its first dividend cut in a decade. Australia already has the lowest dividend cover in the world among the bigger economies, so if the slowing domestic economy leads to a decline in corporate profitability, it will be bad news for income investors, highlighting the importance of taking a diversified global investment approach. Hong Kong’s payouts jumped 8.1% on an underlying basis, contrasting with the mainland trend. This was mainly due to dividends from oil company CNOOC and from the real estate sector.

Q3 marks the seasonal low point for European dividends. They rose 7.0% on an underlying basis, though the growth rate was flattered by positive developments at just a few companies, and the total will not be enough to affect the annual rate significantly.

The energy sector saw the strongest growth in Q3, with dividends up by just over a fifth on an underlying basis. Most of this came from Russian oil companies, but China and Hong Kong, Canada and the United States also made a significant contribution to the increase. Basic materials headline growth was boosted by special dividends, but telecoms companies around the world were dogged by cuts, with the biggest impact from Vodafone in the UK, China Mobile and Telstra in Australia. Only just over half of the telcos in the index increased their payouts year-on-year.

Janus Henderson has left its $1.43trillion forecast for global dividends unchanged for 2019. This represents a headline increase of 3.9%, equivalent to underlying growth of 5.4%. By contrast 2018 saw underlying growth of 8.5%. 2019 will mark the tenth consecutive year of underlying growth for dividends.