The latest economic and finance data appears to be pulling in two directions, so we discuss the trends.

Welcome to the Property Imperative Weekly to 21st October 2017. Watch the video, or read the transcript!

Welcome to the Property Imperative Weekly to 21st October 2017. Watch the video, or read the transcript!

In this week’s review of the latest finance and property news, we start with data from the Australian Institute of Health and Welfare in their newly released report Australian Welfare 2017. This is a distillation of data from various public sources, rather than offering new research.

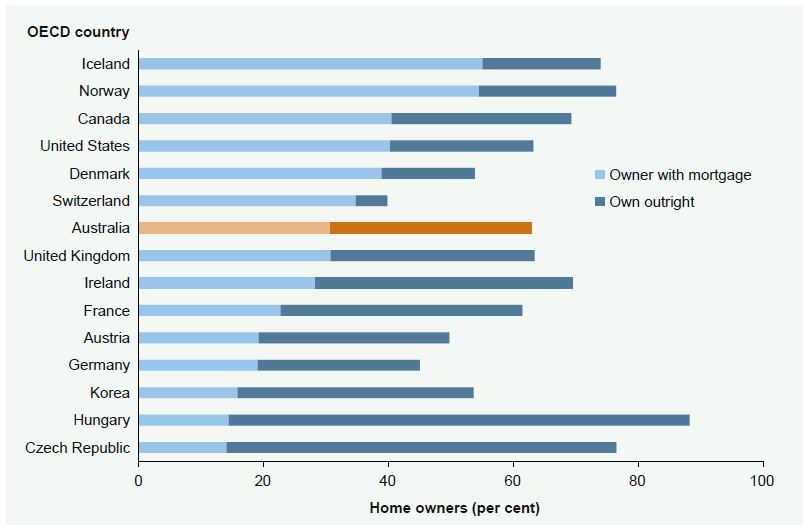

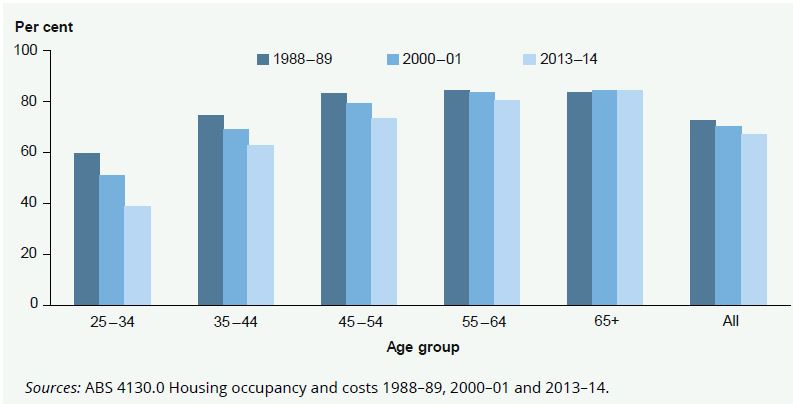

In the housing chapter, they reinforce the well-known fact that home ownership is falling in Australia, while rates have been rising in a number of other comparable countries. Contributing to this trend overseas, at least in part, they say, are changes in the characteristics of households (including population ageing, household structure, and income and education) and policy influences, such as mortgage market innovations (including the relaxation of deposit constraints, increasing home ownership rates among lower income households, and tax reliefs on mortgage debt financing). In Australia, the steepest decline in home ownership rates across the 25 years to 2013–14 has been for people aged 25–34. This is typically the age at which first transitions into home ownership are made. But, fewer and fewer people in this age group are entering home ownership, with a 21 percentage point decline to just 39% in 2013–14 (compared with 60% in 1988–89). Home ownership rates for people aged 35–44 also fell, but not so much (12 percentage points).

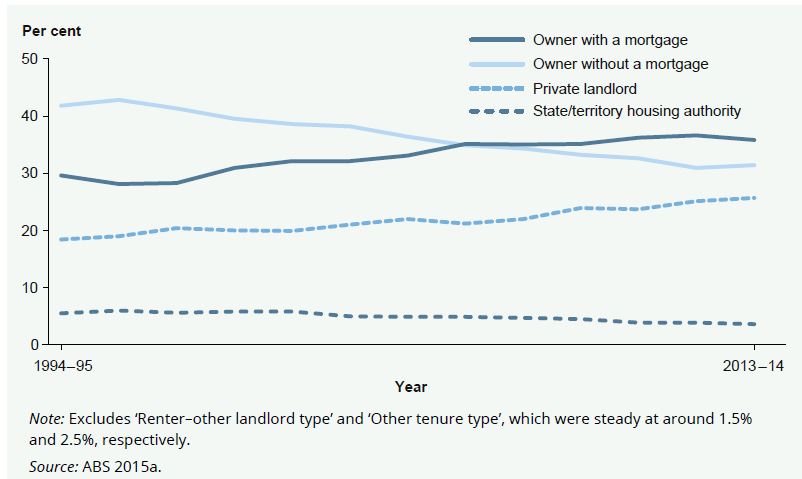

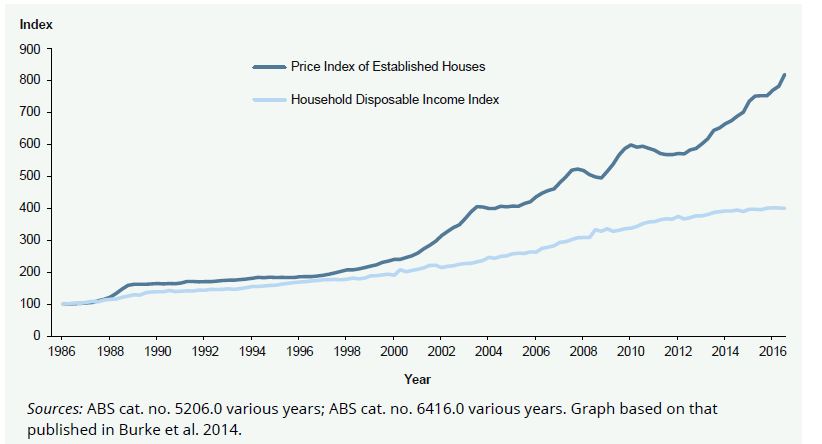

Also, the proportion of home owners without a mortgage has continued to fall, while the proportion of renters has increased. Now more home owners have a mortgage, compared with those who own their property outright. Another fact is the startling gap between the rise in home prices, relative to disposable incomes, creating a barrier to home ownership for many. This gap has been fuelled by rapid house price growth (up 250% since the 1990’s), after the financial system was deregulated, with the total value of Australian housing estimated to be more than $6.5 trillion. Of course, the impact of higher house prices has been partially offset by lower mortgage interest rates, increased credit availability and changes in financial agency practices. These favourable lending conditions and low interest rates have encouraged buyers into the market, despite the growth in house prices themselves. This could all got wrong should mortgage rates rise.

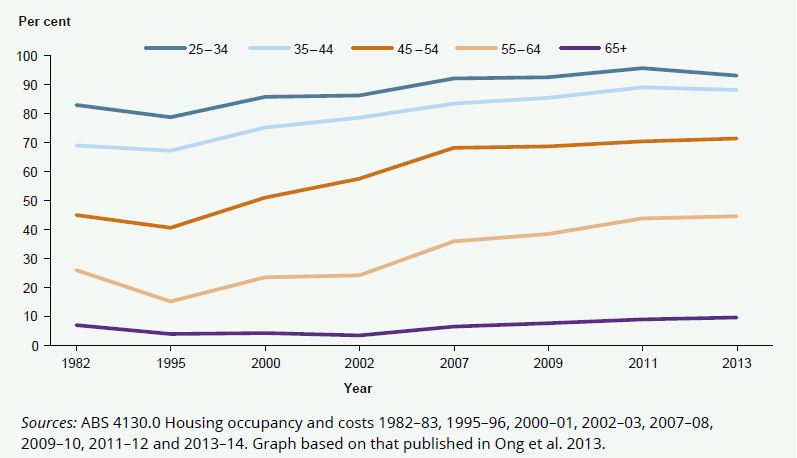

The final piece of data shows that households are getting a mortgage later in life, and holding it longer, often well into retirement. In 2013, 71% of people born between 1957 and 1966 (mainly baby boomers), were financing a mortgage when aged 45–54. This trend is of particular concern as these households’ approach retirement without their home and asset base being paid off. For people looking to retire in the next 10 years, 45% of 55–64-year-olds in 2013 were still servicing a mortgage, compared with just 26% in 1982.

As the recent Citi report emphasises, and using our Core Market Data, the large level of debt outstanding by borrowers aged in their 50s and 60s means many investors will need to sell property to discharge their debts, especially those holding interest only loans. Given that the average age of wealthy seniors is 63 and the average IO debt is $236,400, Citi expressed concern that this cohort will not have enough time to repay the principal “without a significant hit to household cash flows”.

We still think the mortgage underwriting standards are too lose in Australia, as regulators try to balance slowing the market, but not killing the goose which is laying the golden economic egg. So we found the Canadian regulators intervention in their mortgage market this week significant. There the index of house prices to disposable income has increased 25%, from 2000, raising the prospect that real estate overvaluation is driving up overall household debt and overextending borrowers. So they tightened serviceability requirements and imposed loan to value limits on lenders.

Good news on housing affordability this week from the HIA, at least for some. Their Housing Affordability index for Australia improved by 0.5 per cent in the September 2017 quarter but still remains 4.4 per cent below the level recorded a year ago. It also showed that while some owner occupied borrowers had seen their mortgage rates drop, many property investors, has seen their rates rise. Sydney remains the least affordable market they say.

Our friends at Mozo wrote a blog post for us on the impact of the APRA changes to mortgage rates, which underscored the movements by type of loan.

More good news from the ABS. The monthly trend unemployment rate decreased by 0.2 per cent over the past year to 5.5 per cent in September, the lowest rate seen since March 2013. The participation rate remained steady at 65.2 per cent, within that male participation rate was 70.8 per cent, while the female participation rate reached a record high of 59.9 per cent. Over the past year, the states with the strongest annual growth in employment were Queensland (4.1 per cent), Tasmania (3.9 per cent), Victoria (3.1 per cent) and Western Australia (2.9 per cent). However, the underemployment trend rate still does not look that flash, especially in TAS, SA and WA, and we have a very high unemployment rate among younger workers as well as a rise in more casual, part-time work. All of this translates to lower wages.

The latest data from S&P showed a small decline in mortgage defaults in August. S&P said arrears decreased in all states and territories except the Australian Capital Territory (ACT) over the month, with noticeable improvements in Australia’s mining states and territories. The Northern Territory recorded the largest improvement, with arrears declining to 1.63% from 1.98% a month earlier. In Western Australia, arrears fell to 2.22% in August from a historic high of 2.38% in July. They still warned of potential risks in the system, especially from higher LVR IO loans written before 2015. And of course, this is looking a selection of securitised loans which may not be typical, and in any case, in most places home price rises mean struggling borrowers should have the capacity to sell and repay the bank. That would change if prices started to fall seriously.

Talking of risks, there were interesting comments from ASIC this week, suggesting that whilst brokers may be having appropriate conversations with their interest only mortgage customers, there was evidence of poor record keeping. This follows the regulator’s announcement they would commence a loan file review, to ensure that consumers are not paying for more expensive products that are unsuitable. Without good documentation brokers and lenders leave themselves open to the charge of making unsuitable loans, which can have significant consequences.

Another indicator of potential risks in the system is the rise in the number of households seeking short term loans from pay day lenders and other providers. Our surveys show that more than 1.4 million of the 9.5 million households in Australia are looking for finance (and it is rising fast as cash flows are stressed). Not all will successfully obtain a loan. We think more than $1 billion in loans are out there, and our research shows that such short term loans really do not solve household financial issues. However, when people are desperate, they will tend to grasp at any straw in the wind, regardless of cost or consequences. We also find these households are within certain household segments, who tend to be less affluent, and less well educated.

The RBA minutes, release this week, did not tell us much more, but contained this morsel. “Members noted that housing loans as a share of banks’ domestic credit had increased markedly over the preceding two decades. APRA intended to publish a discussion paper later in 2017 addressing the concentration of banks’ exposures to housing. Members also noted that APRA had intensified its focus on Australian banks strengthening their risk culture”. We can barely contain our excitement at the prospect! A discussion paper later in the year!

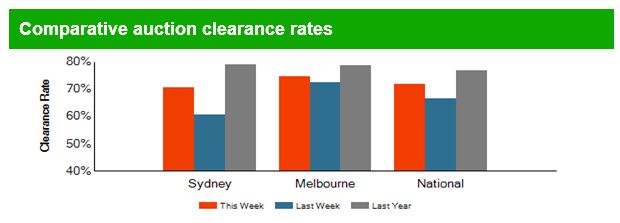

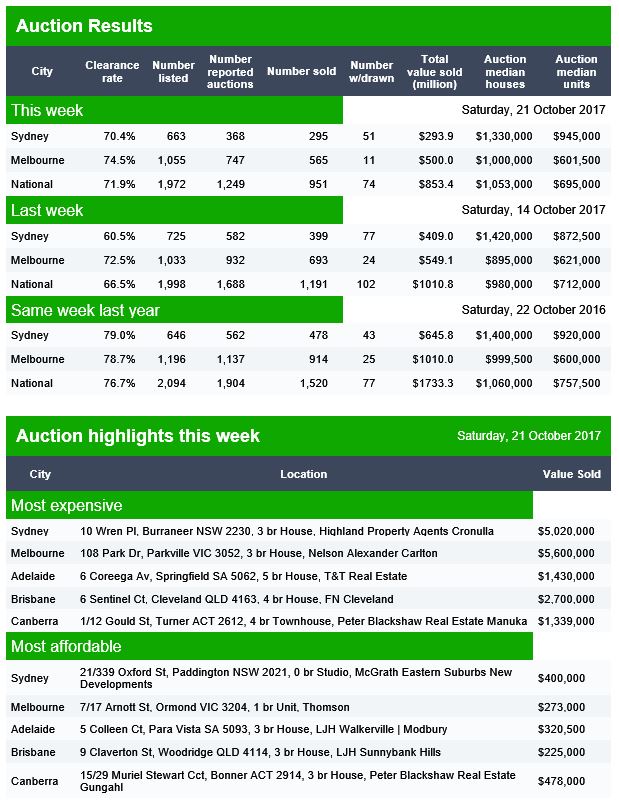

CoreLogic’s latest auction clearance results showed there is still demand for property, with a preliminary clearance rate of 70.6 per cent, and increase from last week when the final clearance rate slipped to 64.4 per cent, the lowest clearance rate since January 2016.

Finally, we released our latest flagship report – The Property Imperative, Volume 9. This is available free on request from our web site and is a distillation of our research into the finance and property market, using data from our household surveys and other public data. Whilst we provide these weekly updates via our blog, twice a year we publish a full report. Volume 9 offers, in one place, a unique summary of the finance and property markets, from a household perspective, over more than 70 pages.

What really struck us as we wrote the report was the amount of change in the property and finance sector, with significant regulatory tightening, changes in mortgage pricing and a rotation in mortgage lending. But the underlying facts of high prices, mortgage stress and rising risks in the system appear unchanged. The number of reports highlighting the risks have risen substantially.

Standing back, sure the data is pulling to two directions, with employment higher, auction clearance rates firm and affordability for some manageable. But the bigger picture contains a number of risks, stemming from the divergence of incomes and home prices, the lose lending standards over the past few years, and the risks from the more recent tightening of the rules, at a time when interest rates are more likely to rise than fall. Without a significant rise in incomes in real terms – and we cannot see where this will come from – the risks to growth and financial stability are still not fully understood.

And that’s the Property Imperative to 21st October 2017. Follow this link to request the Volume 9 Property Imperative Report.