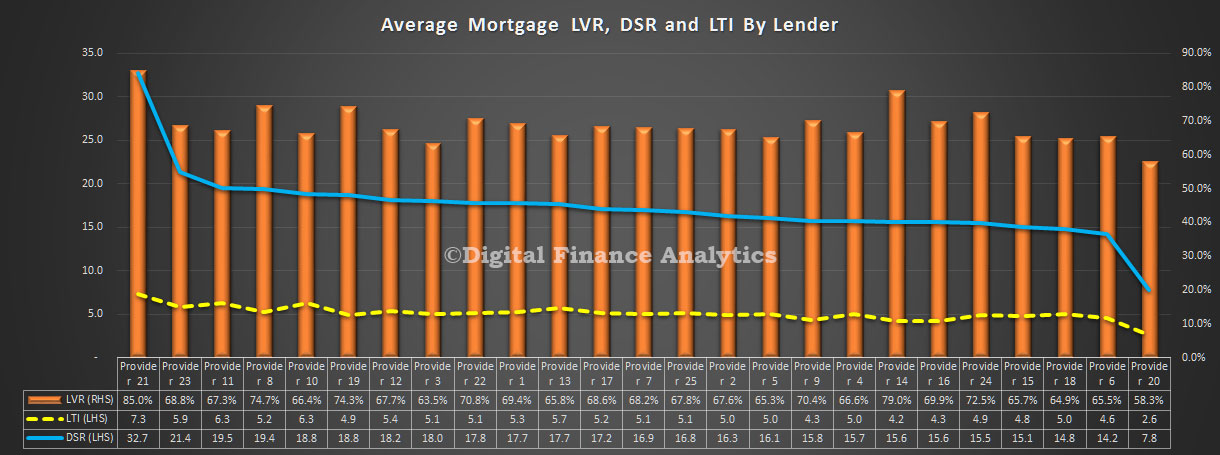

In the latest of our series on deep home loan segmentation, using DSR, LTI and LVR we compare the averages across a number of lender portfolios. The chart shows the average from a range of 20 or so lenders in our surveys, including banks, non-banks, credit unions and building societies. We have selected lenders to give an indication of the spread of the results, but have masked the individual brands. For some, the average LVR in the portfolio is sitting north of 80%, whilst others are below 60%. The highest DSR is averaging at 32, whilst the lowest in 7.8. The highest LTI is on average 7.3, compared with 2.6 for the lowest.

These findings underscore that underwriting criteria do vary, risks in the portfolio will also vary, and the mix of business does change across the market.

These findings underscore that underwriting criteria do vary, risks in the portfolio will also vary, and the mix of business does change across the market.

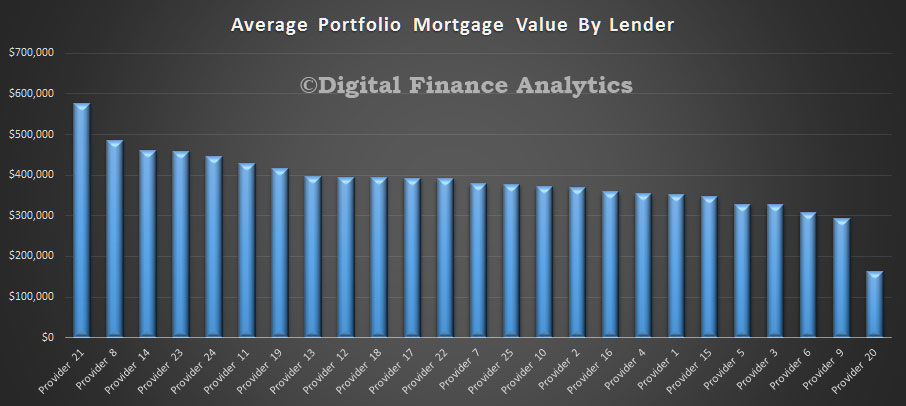

Another view is the average loan value in the portfolio. Once again we found a surprising range of values, from just below $600k, down to $180k. Many factors influence the average of course, including lending policy, type of loan, time on book, how much households have paid ahead, and other factors.

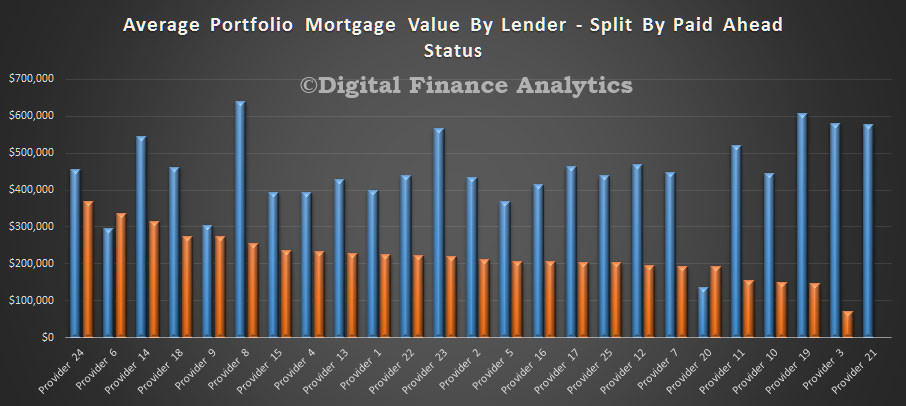

Here is a split of average balances by lender of loans paid ahead and those who are not.

Here is a split of average balances by lender of loans paid ahead and those who are not.

We see that households who are paying ahead generally have lower loan balances (reflecting differences in the LVR, LTI and DSR status). This chart provides more insight.

We see that households who are paying ahead generally have lower loan balances (reflecting differences in the LVR, LTI and DSR status). This chart provides more insight.

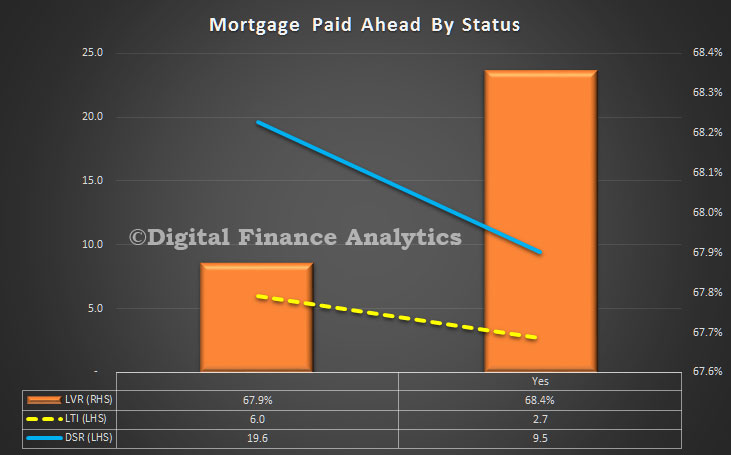

Those who have paid ahead have a lower LTI (2.7 compared with 6.0), lower DSR (9.5 compared with 19.6) but a slightly higher LVR. The portfolio averages are LTI 5.1, DSR 16.9 and LVR 68%.

Those who have paid ahead have a lower LTI (2.7 compared with 6.0), lower DSR (9.5 compared with 19.6) but a slightly higher LVR. The portfolio averages are LTI 5.1, DSR 16.9 and LVR 68%.

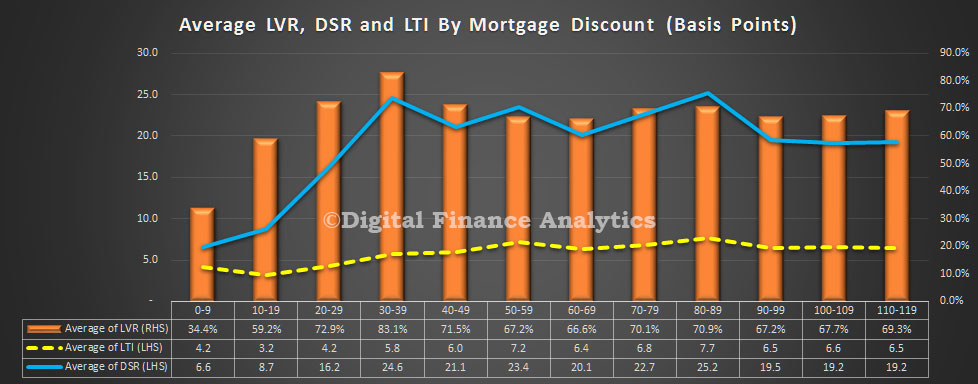

Another interesting lens is the mortgage discounts being achieved by households, compared with LVR, LTI and DSR. It appears the best discounts are being made on LVR’s below 80%, but LTI and DSR have less bearing on the achieved rates. A low DSR or LTI does not necessarily translate into a bigger discount – something which lenders may want to reconsider, given the relative risks involved.

2 thoughts on “All Lenders Are Not The Same”