We had significant reaction to yesterday’s post on the “normal” status of high household debt. So today we take the argument further using data from the RBA Household Balance Sheet series (E1) and the recent ABS data on income growth.

The traditional argument trotted out is that household wealth is greater than ever, this despite low income growth and rising debt. But of course wealth is significantly linked to home prices, which in turn is linked to debt, so this is a circular argument. You get a different perspective by looking at some additional trends.

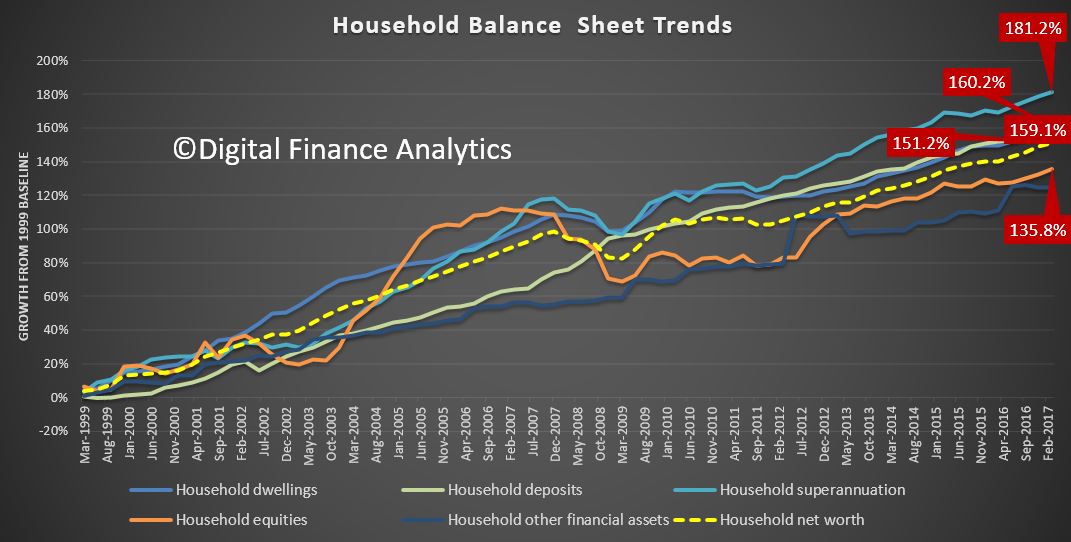

But lets start with the asset side of the ledger. We have base-lined the data series from 1999. Since then, superannuation has grown by 181.2%, and at the fastest rate. But it is arguably the least accessible asset class.

Residential property values rose 160.2% over the same period, and grew significantly faster than equities which achieved 135.8% growth, no wonder people want to invest in property – the capital returns have been significantly more robust. Deposit savings grew 159.1% (but the savings ratio has been declining recently). Overall household net worth rose 151.2%. So the story about households being more affluent can be supported on this view of the data. But it is myopic.

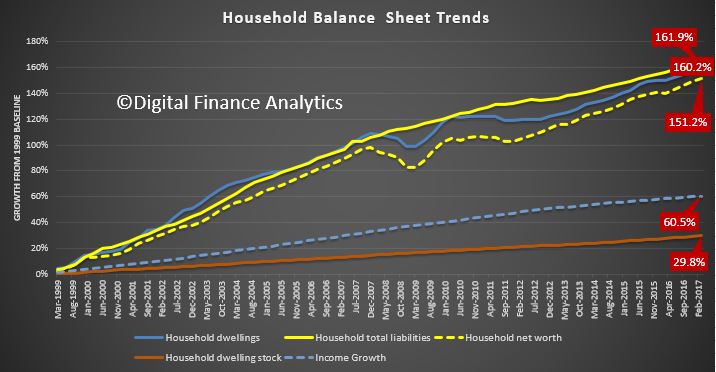

The chart below tracks overall household debt, house prices, household net worth, income growth and the growth in the number of residential properties.

The chart below tracks overall household debt, house prices, household net worth, income growth and the growth in the number of residential properties.

Overall household debt rose 161.9%, a growth rate which is higher than residential property values, at 160.2% and above overall household net worth at 151.2%.

Overall household debt rose 161.9%, a growth rate which is higher than residential property values, at 160.2% and above overall household net worth at 151.2%.

But look at the growth in income, which is 60.5%, under half the asset growth. OK, interest rates are lower now, but this increase in leverage is phenomenal – and explains the “debt is normal” findings from our focus groups. I accept debt is not equally spread across the population, but there are significant pockets of high borrowing, as can be seen from our mortgage stress analysis – and its not just among battling urban fringe mortgage holders.

Finally, it is worth noting the growth in the number of residential properties rose by just 29.8% over the same period. So the average value of individual properties have increased significantly. On paper.

To me this highlights we have learned nothing from the GFC, our appetite for debt, supported by the low interest rate monetary policy, significant tax breaks, and salted by population growth has created a debt monster, which has the capacity to consume many if interest rates were to rise towards more normal levels. Unlike Governments, household debt has to be repaid, eventually.

This data series shows clearly the relationship between more debt and home prices, they feed of each other, and this explains why the banks have enjoyed such strong balance sheet growth. But the impact on households is profound, and long term.

Our current attitude to debt will be destructive eventually.

One thought on “Another Perspective On Debt”