APRA today released the Quarterly Authorised Deposit-taking Institution Performance publication for the June 2015 quarter. This publication contains information on ADIs’ financial performance, financial position, capital adequacy and asset quality. There were 160 ADIs operating in Australia as at 30 June 2015, compared to 165 at 31 March 2015. There were eight changes were mainly to some credit unions having their licences revoked.

Over the year ending 30 June 2015, ADIs recorded net profit after tax of $38.0 billion. This is an increase of $5.7 billion (17.6 per cent) on the year ending 30 June 2014.

As at 30 June 2015, the total assets of ADIs were $4.4 trillion, an increase of $376.4 billion (9.3 per cent) over the year. The total capital base of ADIs was $238.1 billion at 30 June 2015 and risk-weighted assets were $1.8 trillion at that date. The aggregate capital adequacy ratio for all ADIs was 13.2 per cent.

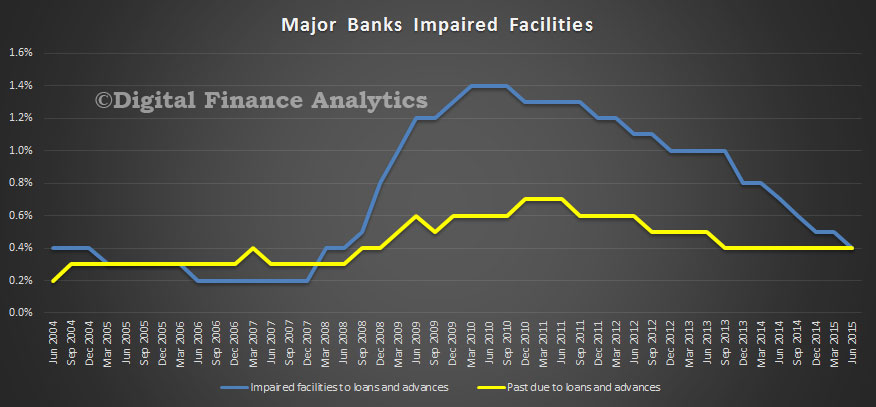

Impaired assets and past due items were $26.7 billion, a decrease of $5.4 billion (16.8 per cent) over the year. Total provisions were $13.4 billion, a decrease of $5.2 billion (27.9 per cent) over the year.

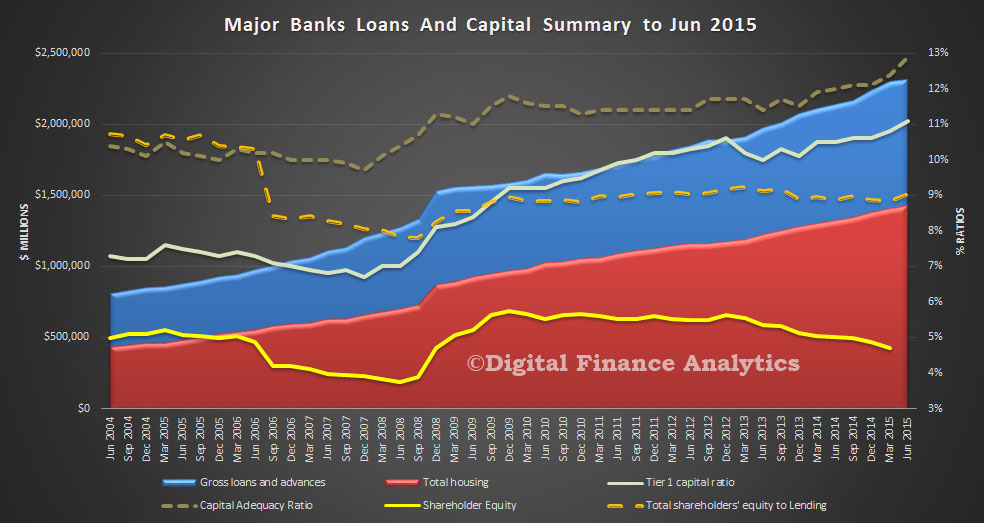

Looking in detail at the average of the four majors, we have plotted loans, housing loans and capital ratios again, to June 2015. We see the growth in lending, and the ongoing rise of housing lending. We also see the capital adequacy ratio and tier 1 ratios rising. However, the ratio of loans to shareholder equity is just 4.7% now. This should rise a bit in the next quarter reflecting recent capital raisings, but this ratio is LOWER than in 2009. This is a reflection of the greater proportion of home lending, and the more generous risk weightings which are applied under APRA’s regulatory framework. It also shows how leveraged the majors are, and that the bulk of the risk in the system sits with borrowers, including mortgage holders. No surprise then that capital ratios are being tweaked by the regulator, better late then never.

At the moment impairments are low, this of course may change if economic momentum slows, unemployment or interest rates rise, or house prices slip. Other risks include external shocks, like China and the impact of rates in the US rising.

At the moment impairments are low, this of course may change if economic momentum slows, unemployment or interest rates rise, or house prices slip. Other risks include external shocks, like China and the impact of rates in the US rising.

One thought on “APRA Data Shows Major Banks Mortgage Book Now $1.43 Trillion – But Shareholder Equity Just 4.7%”