Band Of Queensland today announced cash earnings after tax of $378 million for FY17, up 5 per cent on FY16. Statutory net profit after tax increased by 4 per cent to $352 million.

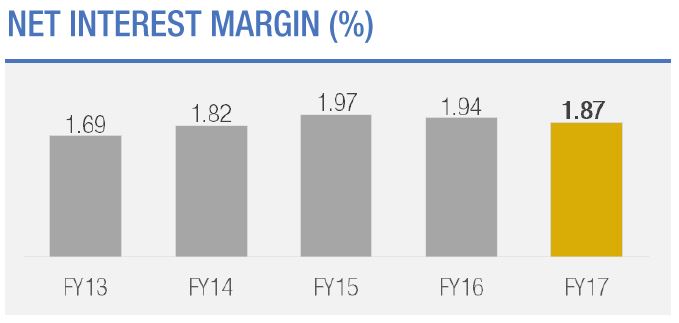

There was a one-off $16m uplift thanks to asset sales, but the stronger results were really thanks to lower bad and doubtful debts. Otherwise, pretty much as expected. The question is, can the NIM improvement be maintained in the ultra-competitive market, despite a small lift in past 90 day mortgage defaults?

Return on equity was 10.4%, just slightly better than FY16, but this included the $16m profit from asset disposals.

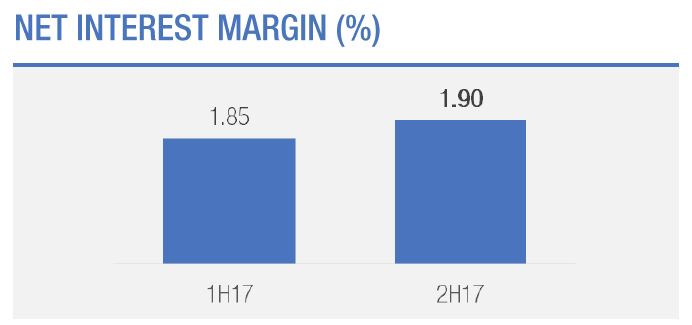

Net interest margin fell to 1.87%, but was better in 2H.

Net interest margin fell to 1.87%, but was better in 2H.

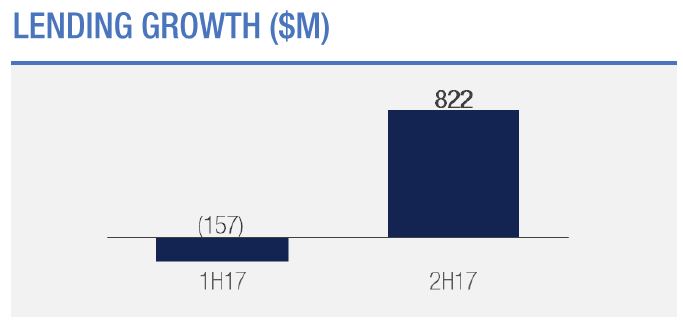

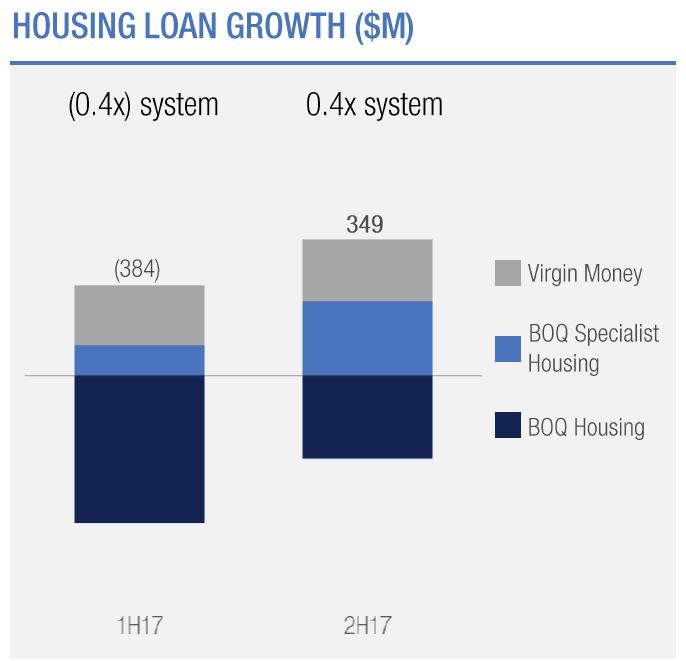

Loan growth was significantly lower in FY17, although better in 2H.

Loan growth was significantly lower in FY17, although better in 2H.

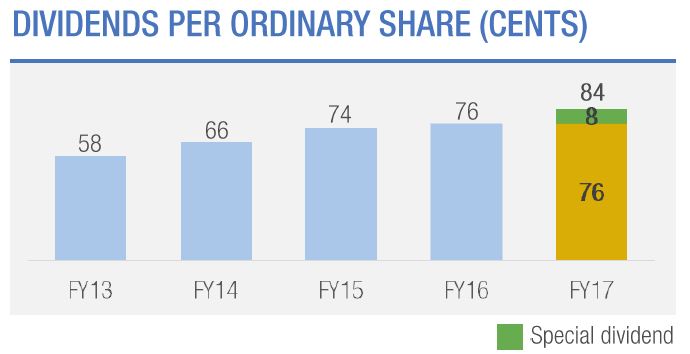

The BOQ Board has maintained a fully franked final dividend of 38 cents per ordinary share and announced a fully franked special dividend of 8 cents per ordinary share.

The BOQ Board has maintained a fully franked final dividend of 38 cents per ordinary share and announced a fully franked special dividend of 8 cents per ordinary share.

Second half cash earnings after tax increased 16 per cent on the first half result, supported by a $16 million profit on the disposal of a vendor finance entity. On an adjusted basis (excluding the vendor finance entity disposal), FY17 cash earnings after tax increased 1 per cent to $362 million and second half cash earnings after tax in creased 7 per cent on the prior half to $187 million.

Second half cash earnings after tax increased 16 per cent on the first half result, supported by a $16 million profit on the disposal of a vendor finance entity. On an adjusted basis (excluding the vendor finance entity disposal), FY17 cash earnings after tax increased 1 per cent to $362 million and second half cash earnings after tax in creased 7 per cent on the prior half to $187 million.

Lending growth improved in both the housing and commercial loan portfolios.

The Virgin Money Reward Me home loan portfolio has grown ahead of expectations.

The Virgin Money Reward Me home loan portfolio has grown ahead of expectations.

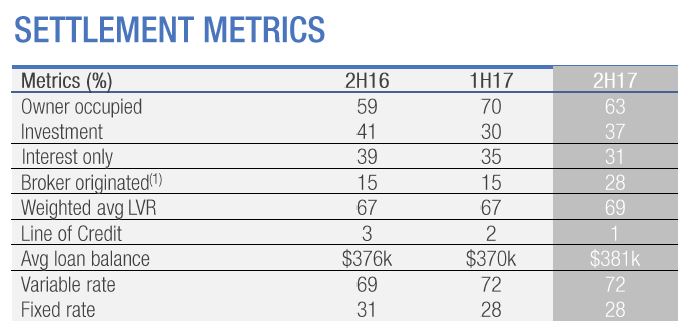

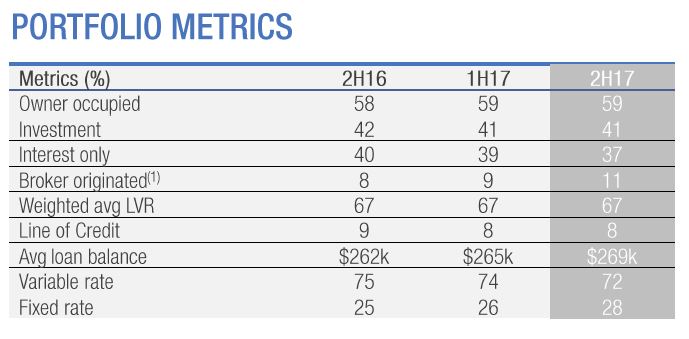

Broker settlements increased to 28%, and interest only loans was 40% in 2H16, and 39% in 1H17, but trending down, they say! 8% of loans are higher than 90% on a portfolio basis, and 19% in the 81-90% band.

These include Virgin Money home loans.

These include Virgin Money home loans.

BOQ’s niche businesses continue to grow. BOQ Specialist, BOQ Finance and other commercial lending target segments have all delivered good results.

During the year, capability has been built in the niche segment of corporate healthcare, leveraging industry expertise and contacts through BOQ Specialist. Loan balances in the niche business banking segments of agribusiness, corporate healthcare & retirement living and hospitality & tourism have grown by $309 million to $1.5 billion.

BOQ Finance also made another strong contribution. The Cashflow Finance acquisition made during the year added another dimension to the business’ suite of finance products.

BOQ’s asset quality remains sound with further improvement across a range of metrics. This is the outcome of a deliberate approach to improve risk management over the past five years. Impaired assets as a percentage of gross loans were down to 44 basis points, while loan impairment expense was just 11 basis points of gross loans during the year.

However, there was a small rise in 90 days past due mortgage arrears.

However, there was a small rise in 90 days past due mortgage arrears.

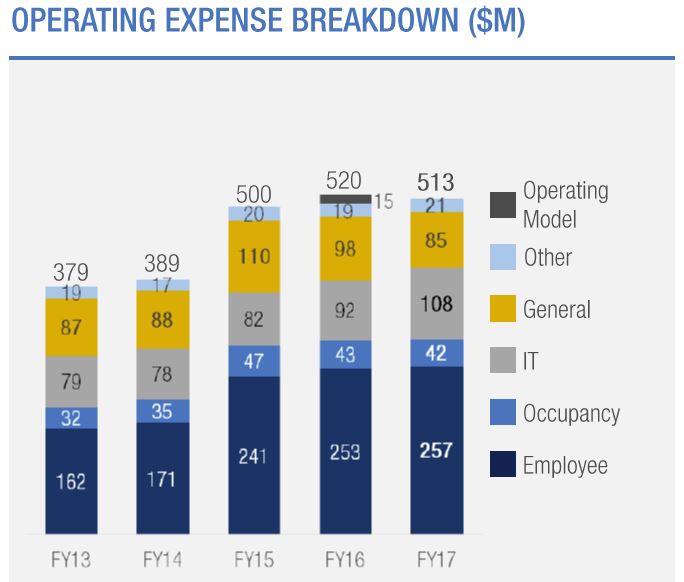

BOQ has delivered on its 1 per cent underlying expense growth target with underlying expenses of $510 million. This target was achieved while still investing in the business. BOQ is continuing to invest in digitising processes, which will have the dual benefit of improving customer experiences and improving business efficiency.

BOQ has delivered on its 1 per cent underlying expense growth target with underlying expenses of $510 million. This target was achieved while still investing in the business. BOQ is continuing to invest in digitising processes, which will have the dual benefit of improving customer experiences and improving business efficiency.

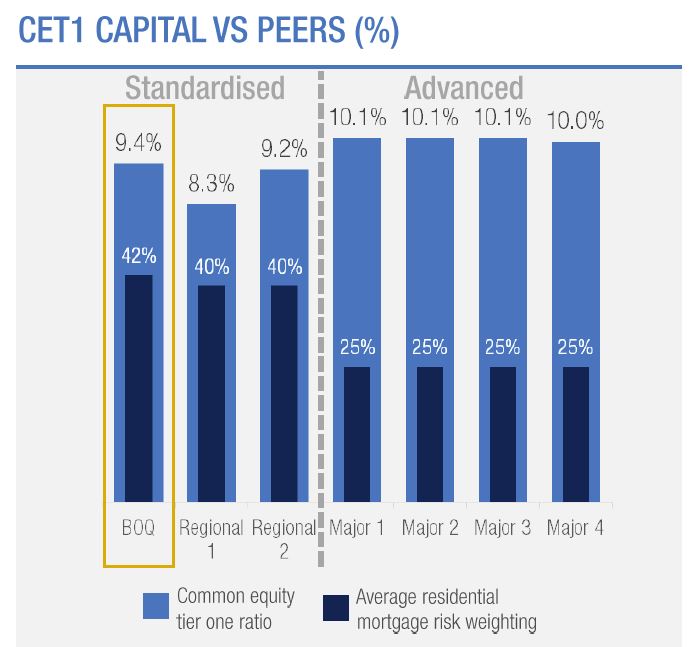

BOQ’s strong capital position further improved. The CET1 ratio was up 10 basis points over the half to 9.39 per cent.

BOQ’s strong capital position further improved. The CET1 ratio was up 10 basis points over the half to 9.39 per cent.

This position will be further strengthened by 20 to 25 basis points following business and regulatory changes expected to occur in the first half of FY2018. In response to these changes and BOQ’s position, the Board has determined that returning some of this excess capital to shareholders is the most appropriate course of action at this time.

This position will be further strengthened by 20 to 25 basis points following business and regulatory changes expected to occur in the first half of FY2018. In response to these changes and BOQ’s position, the Board has determined that returning some of this excess capital to shareholders is the most appropriate course of action at this time.

A special dividend of 8 cents per ordinary share has been announced by the Board, along with suspension of the dividend reinvestment plan for the final and special dividends on ordinary shares. This will be reinstated on 24 November 2017.