CBA released their unaudited trading update. Cash earnings were $2.4 billion in the quarter, and statutory net profit was $2.6 billion.

They say net interest income grew (pcp) supported by volume growth in key markets, offsetting margin pressures, but Group Net Interest Margin fell slightly in the quarter due to higher average liquids and competition effects. All the majors have therefore reported a NIM squeeze in this reporting round.

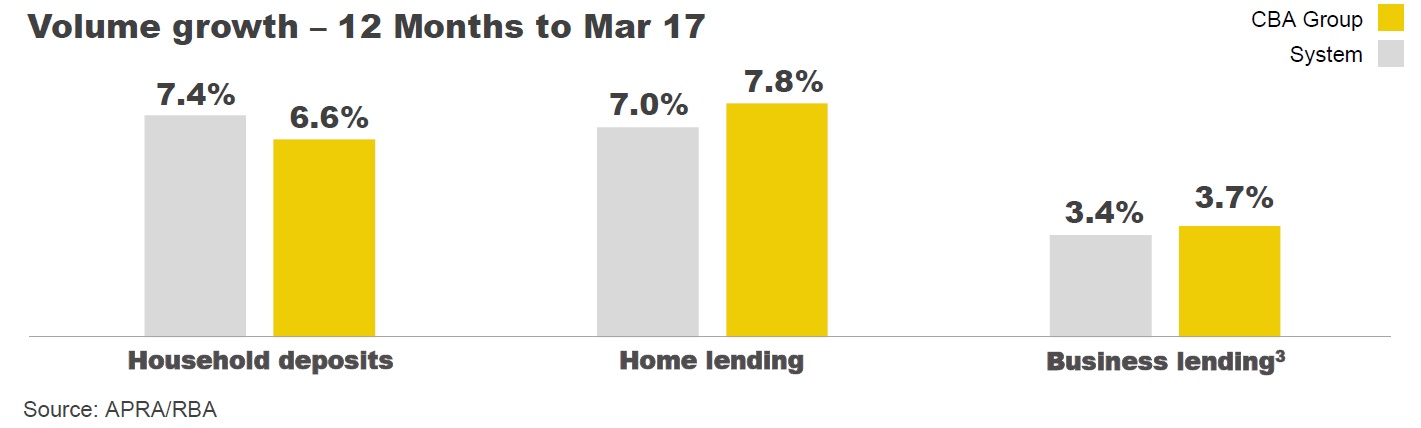

In home lending, growth continued to be underpinned by strong proprietary channel performance but defaults were higher, especially in WA.

In home lending, growth continued to be underpinned by strong proprietary channel performance but defaults were higher, especially in WA.

Business lending growth overall remained subdued, with strongest growth in Business and Private Banking.

In Wealth Management, Average Assets Under Management and Funds Under Administration rose by 6% and 7% respectively, reflecting stronger investment markets, partly offset by exchange rate movements.

In ASB, volume growth remained strong, with lending up 10% and deposits up 8% (12 months to Mar 17).

Other Banking Income was stable with higher commissions and lending fees offset by lower trading income.

Insurance income was impacted by weather events during the quarter, including Cyclone Debbie.

They continue cost discipline enabling ongoing investment.

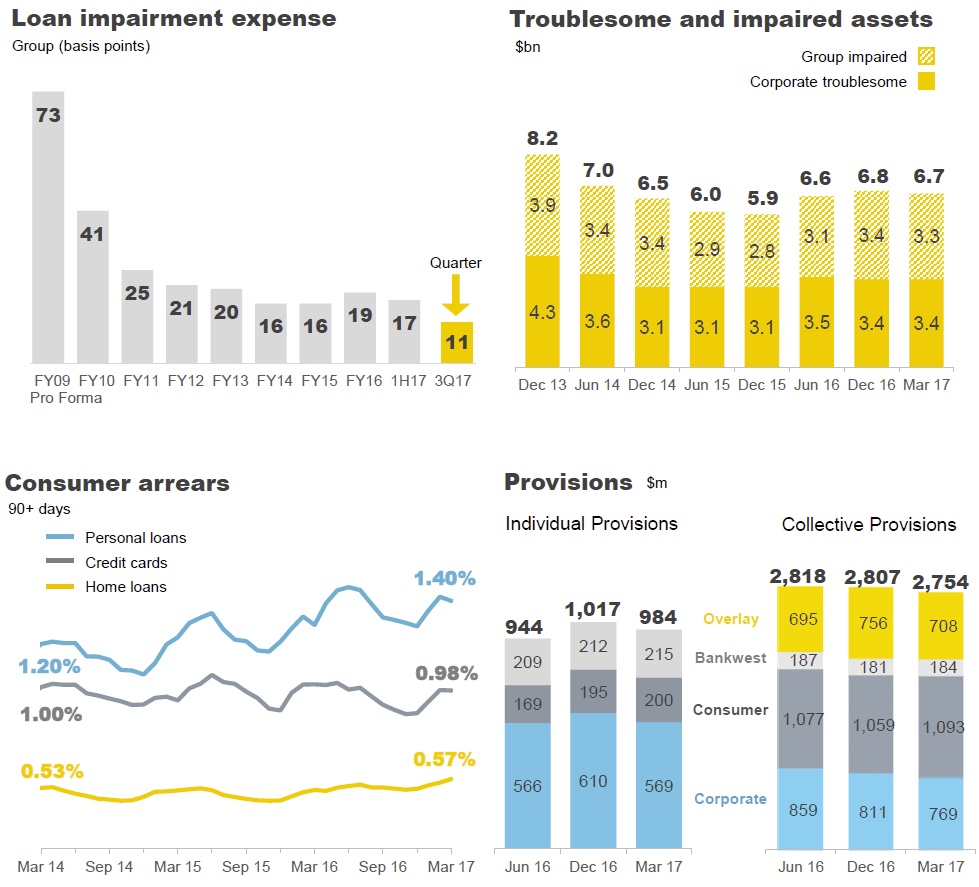

Loan Impairment Expense (LIE) was $202 million in the quarter and equated to 11 basis points of Gross Loans and Acceptances, compared to 17 basis points in 1H17.

Corporate LIE was substantially lower in the quarter. Troublesome and impaired assets were slightly lower at$6.7 billion, with broadly stable outcomes across most sectors. Apartment development exposures (Domestic residential apartment developments >$20m) reduced in the quarter.

Consumer arrears increased in line with seasonal expectations and continued to be elevated in Western Australia. In the home lending portfolio, investment lending reduced as a proportion of total new lending in the quarter and they say new interest only lending is being closely managed, consistent with regulatory guidance.

Prudent levels of provisioning were maintained, with Total Provisions at $3.7 billion and no change to overlays for economic conditions.

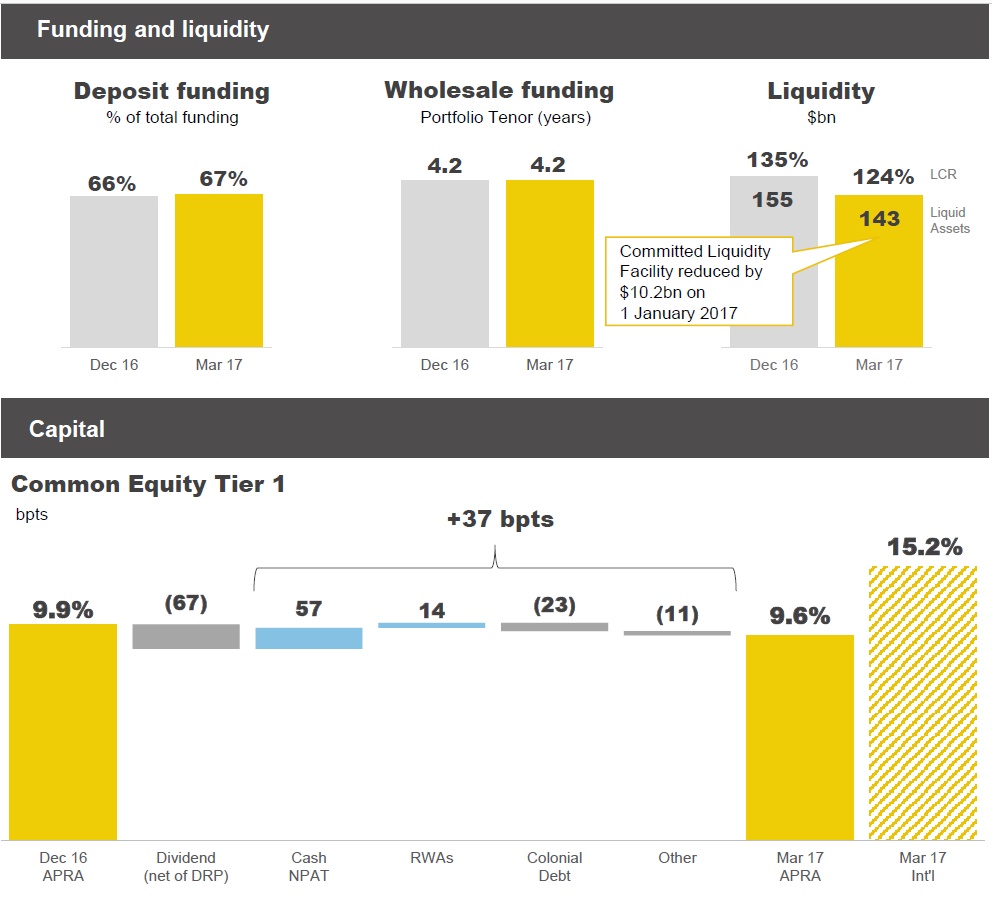

Funding and liquidity positions remained strong, with customer deposit funding at 67% and the average tenor of the wholesale funding portfolio at 4.2 years.

Funding and liquidity positions remained strong, with customer deposit funding at 67% and the average tenor of the wholesale funding portfolio at 4.2 years.

Liquid assets totalled $143 billion with the Liquidity Coverage Ratio (LCR) standing at 124%. The Group issued $14.6 billion of long term funding in the quarter, and $37 billion year to date.

The Group’s Basel III Common Equity Tier 1 (CET1) APRA ratio was 9.6% as at 31 March 2017. After allowing for the impact of the 2017 interim dividend (which included the issuance of shares in respect of the Dividend Reinvestment Plan), the CET1 (APRA) ratio increased by 37 basis points in the quarter. This was primarily driven by capital generated from earnings, and lower risk weighted assets, partially offset by the maturity of a further $1 billion of Colonial debt8. The Group’s Basel III Internationally Comparable CET1 ratio as at 31 March 2017 was 15.2%.

The Group’s Leverage Ratio was 4.9% on an APRA basis (unchanged from Dec 16) and 5.6% on an internationally comparable basis.