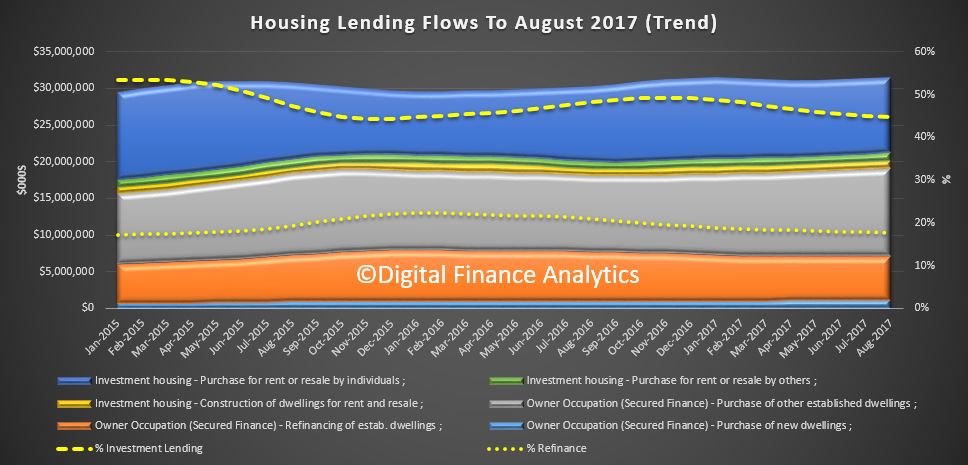

Data from the ABS today on housing finance reconfirms what we already knew, overall lending flows for housing from the ADI’s rose 0.6% in trend terms or 2.1% seasonally adjusted. Within that, lending for owner occupied housing rose 0.9%, or 2.1% seasonally adjusted and investor loans rose 0.2% in trend terms, or a massive 4.3% in seasonally adjusted terms. So lending growth is apparent, and signals more household debt ahead.

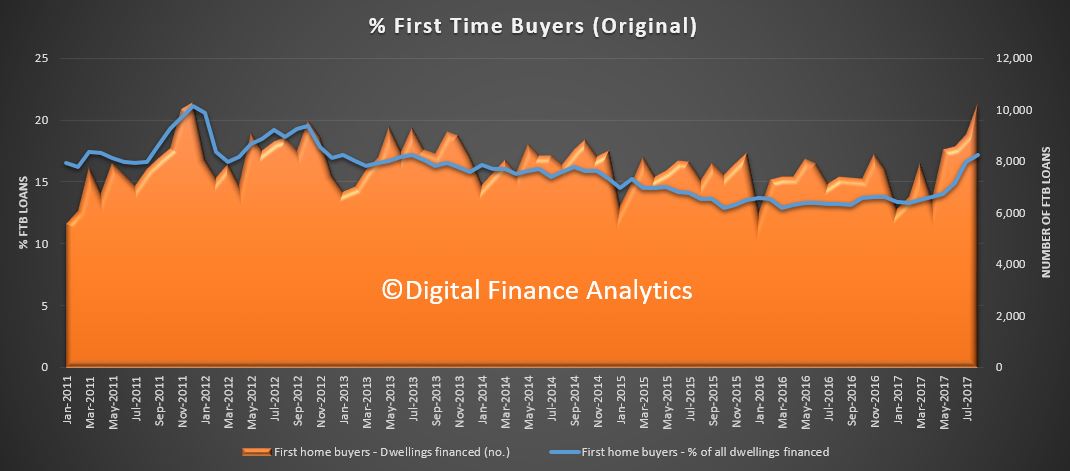

First time buyers continue to extend their reach, despite we seeing “Peak Price” for property at the moment. In original terms, the number of first home buyer commitments as a percentage of total owner occupied housing finance commitments rose to 17.2% in August 2017 from 16.6% in July 2017. But these numbers may be wobbly, as the ABS warns:

The number of loans to first home buyers increased strongly in August. The ratio of the number of first home buyer loans to the total number of owner occupier loans also increased strongly. The increase has been driven mainly by changes to first home buyer incentives made in July by the New South Wales and Victorian governments. The ABS is working with financial institutions to establish the size of the increase in first home buyer lending in recent months. These numbers may be revised and users should take care when interpreting recent ABS first home buyer statistics. The ABS is continuing to work with APRA and the financial institutions to improve the quality of first home buyer statistics.

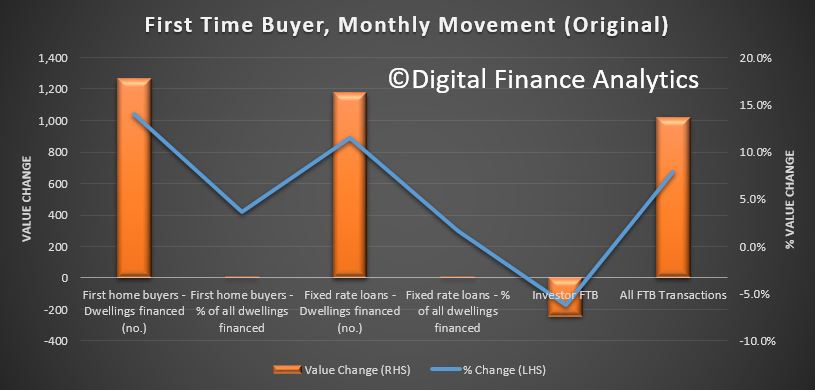

The number of investor first time buyers fell a little according to our surveys, but overall there are more active, thanks to the recent owner occupier incentives.

The number of investor first time buyers fell a little according to our surveys, but overall there are more active, thanks to the recent owner occupier incentives.

![]() The overall lending flows, in trend terms revealed a rise in all categories, other than lending for new construction to investors, which fell just a little. Also refinanced loans only grew a little and continues to slide as a proportion of all loans. No real surprise as rates are rising now. The mix of loans also continues to pivot away from investment property, down to 44.8% of all loans (ex. refinance). Still a high number though.

The overall lending flows, in trend terms revealed a rise in all categories, other than lending for new construction to investors, which fell just a little. Also refinanced loans only grew a little and continues to slide as a proportion of all loans. No real surprise as rates are rising now. The mix of loans also continues to pivot away from investment property, down to 44.8% of all loans (ex. refinance). Still a high number though.

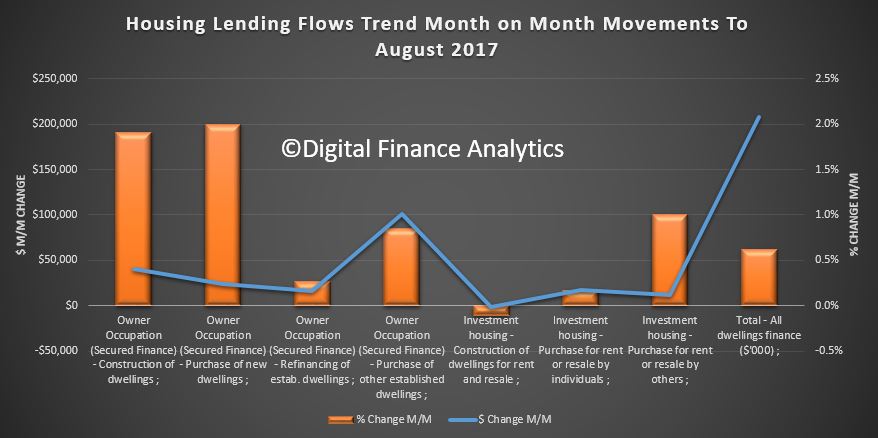

Here are the month on month movements by category.

Here are the month on month movements by category.

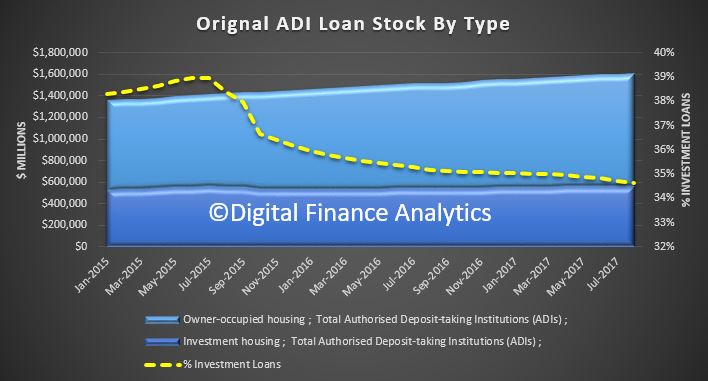

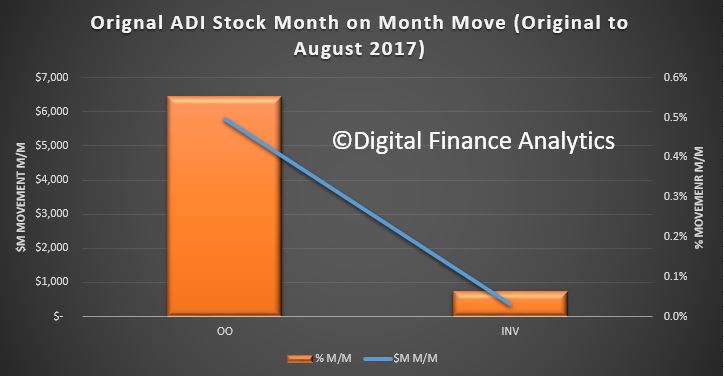

Looking at the original stock data, another $6.5 billion was added to the owner occupied category or 0.6%, while investor loans rose just 0.1% in the month.

Looking at the original stock data, another $6.5 billion was added to the owner occupied category or 0.6%, while investor loans rose just 0.1% in the month.

The portfolio mix of investment loans drifted lower overall, down to 34.6% or $550 billion, while the total value of owner occupied loans stood at $1.1 trillion.

The portfolio mix of investment loans drifted lower overall, down to 34.6% or $550 billion, while the total value of owner occupied loans stood at $1.1 trillion.